Showing results for tags 'then'.

-

Hi all, in 2008 I took out a secured loan of over £10k from Welcome and within a few years struggled to make the payments. The loan went to Cabot on Welcome's demise and then to Ascent. 2 years ago, instead of consulting this site(!), I started paying Ascent less than £100 a month (don't want to be specific, in case they're on here) and this has brought the amount down. The balance is still over £10k and there is a charge on my property. Having spoken to Ascent, I have asked for a settlement figure and they want and income/expenditure thing (not something I trust, it's just to see what they can squeeze out of you I think) before giving me one. I have offered around £4k. My main priority is to get the second charge removed. And hopefully for a substantial discount or nothing. Any advice from here please?!? I understand now that I shouldn't have paid them anything but as there is still a charge on my property I felt I had to.

Hi all, in 2008 I took out a secured loan of over £10k from Welcome and within a few years struggled to make the payments. The loan went to Cabot on Welcome's demise and then to Ascent. 2 years ago, instead of consulting this site(!), I started paying Ascent less than £100 a month (don't want to be specific, in case they're on here) and this has brought the amount down. The balance is still over £10k and there is a charge on my property. Having spoken to Ascent, I have asked for a settlement figure and they want and income/expenditure thing (not something I trust, it's just to see what they can squeeze out of you I think) before giving me one. I have offered around £4k. My main priority is to get the second charge removed. And hopefully for a substantial discount or nothing. Any advice from here please?!? I understand now that I shouldn't have paid them anything but as there is still a charge on my property I felt I had to. -

Please advise Parcel2Go have lost a laptop I was returning to Argos for a full refund, They have lead me a merry dance with lots of excuses and won't compensate. What now please?

Please advise Parcel2Go have lost a laptop I was returning to Argos for a full refund, They have lead me a merry dance with lots of excuses and won't compensate. What now please? -

Sorry guys, i took the lazy approach and ignored everything again. I have received nothing for a long time and then suddenly a letter from Cabot saying they are passing my debt to Ruthbridge, a debt collection agency. In the same envelope (is money too tight to post 2 letters?) A letter from Ruthbridge saying to contact them. I had a message on my answerphone.. This is a call for (silence) Please contact us using your reference. Thats it. I googled the number to see Ruthbridge mentioned. This is a Citi card debt with the last payment in 2006. So long past being statute barred. Its time to move on now and put a stop to these letters dragging up a period i would rather forget. Will they stop or will they write forever? Thank you. PS i know i am a pain the the bottom and so lazy when it comes to dealing with these people but its time to do something. (if possible) PS. Do i phone, email or write to them? Thanks

Sorry guys, i took the lazy approach and ignored everything again. I have received nothing for a long time and then suddenly a letter from Cabot saying they are passing my debt to Ruthbridge, a debt collection agency. In the same envelope (is money too tight to post 2 letters?) A letter from Ruthbridge saying to contact them. I had a message on my answerphone.. This is a call for (silence) Please contact us using your reference. Thats it. I googled the number to see Ruthbridge mentioned. This is a Citi card debt with the last payment in 2006. So long past being statute barred. Its time to move on now and put a stop to these letters dragging up a period i would rather forget. Will they stop or will they write forever? Thank you. PS i know i am a pain the the bottom and so lazy when it comes to dealing with these people but its time to do something. (if possible) PS. Do i phone, email or write to them? Thanks -

Hello everyone I’m looking to get some help if possible please my partner recently applied to open a new HSBC bank account for the cash incentive via the online system. The account she applied for some reason was declined but then instantly offered a standard basic account instead which she accepted and the card and pin arrived a few days later. The following week another letter arrived in a large envelope again from hsbc this time stating they had now closed the account without warning or notice due to not meeting the banks criteria. Strange but ok fair enough she’s not wanted as a customer until she noticed it was hand signed by someone from the fraud analyst department Becoming very worried she contacted the bank who refused to tell her anything and was then advised to send a SAR request to HSBC bank and also CIFAS. Friday she received a letter from CIFAS with a Single CIFAS FRAUD listing from HSBC BANK under the heading APPLICATION FRAUD that she did not list a previous address with adverse history APPLICATION GRANTED This is absolutely disgusting she’s done nothing wrong currently been living in the same house since June 2014 so we’ll over 4 years now. HSBC application page clearly asks for 3 years address history which she’s obviously listed her current address so nothing makes sense at all. She’s sent the HSBC ceo a email who’s replied today with this ( I can understand your frustration in that we ask for any addresses in the last three years and you moved four years ago, so shouldn't have to supply another address. However, we had information there was adverse credit data accrued in your name at a different address within the last three years. I'm very sorry for any confusion caused but we have correctly followed our process. We also correctly reported the instance to CIFAS, as we have an obligation to do. I'm understand this may not be the outcome you were looking for but I hope this has helped to explain our position. If you feel the information we had was incorrect, you may want to check with the Credit Reference Agencies. We use three agencies, Experian, Equifax and Call Credit. ) We are both extremely upset and worried about this issue as she’s done absolutely nothing wrong and is now obviously petrified that all her other financial dealings with other banks etc will see this and close everything down. What do you suggest we now do and has anyone else had issues like this previously that could advise we would be very grateful

-

I’ve never needed a mobile phone except when travelling up north to see my mum who’s in a care home. Just before Christmas 2014 I got a mobile phone from EE so I could stay in touch with work, etc., while visiting my mum. When I set it up it was clear that it didn’t work. I tried all sorts of things and it still wouldn’t work. But I forgot about it for a few days. When I got back after Christmas I decided to phone EE and tell them that it didn’t work. The problem was that they said I didn’t pass the security questions; as a result I could not speak to anyone. Couldn’t report that my mobile didn’t work! The weeks went on and I made other calls to EE, but was told each time that I had failed the security questions. Meanwhile, of course, I was paying for this non-working phone every month by direct debit (or standing order, I forget which). This went on for month after month, and still I was paying for a service which didn’t work with no way of getting the issue resolved. It was such a small matter (as I never need to use my mobile except at Christmas when I am away with family) it was out of my mind for 99% of the time. Eventually I reasoned that I was going to be paying for this broken thing for years – and they were never going to listen to me because they would always say that I had failed the security questions. I took the only option which was then open to me. I cancelled the monthly payment to EE. Now things actually made sense, and at last I was not paying regularly for something that had never worked. At this point let me be clear about something. I could install apps on the phone and I could use it for playing solitaire and other stuff like that. But I could not do what you are expected to be able to do with a phone, i.e. communicate. EE themselves will be aware, as they would have access to such data, that: Number of phone call I made while in that contract = 0 Number of phone calls I received while in that contract = 0 Number of text messages I sent while in that contract = 0 Number of text messages I received while in that contract = 0 That is the level of service I was getting from my EE mobile phone. In the meantime I had paid over £650 for this nonsense. I phoned EE again. again I was told that I had not passed the security questions. But by this time I was aware that the operator at the other end was reading a large amount of text which had been written on my account, EE was obviously well aware of the issue. Also EE would have been aware of the 0 calls and 0 SMS aspect of my strange account. It’s just that they obviously didn’t give a monkey’s. I asked how I could resolve this. How could I prove my identity? I was told to go to my local EE store with some ID and I would be given a password which I could use in subsequent phone calls to the help centre. I did. I phoned EE with my new password and asked for my money back. I was put on hold for several minutes and then told that the account had been passed to the Collections department as it was in arrears (of course they would have been flagged as in arrears: the only way to stop being mugged every month was to cancel the monthly debit!). (Oh yes, and to add insult to injury, because of the misperception that I was in the wrong EE was allowed to put a black mark against my credit rating. I also had debt collectors writing to me. But I was able to explain to the debt collections agency what had happened and they just dropped the case against me immediately- no excuse with security questions there: I just TALKED to them and they LISTENED! It's what people do.) The person I spoke to in the Collections department acted exactly as Collections people behave and said that I could not have my money back. When I explained that consumer law was on my side he said that I had “failed data protection laws”. I reminded him that data protection laws were there to protect consumers, not corporations who sought to rip consumers off as EE was obviously very keen to do to me. I also said that I wanted EE to delete the black mark that they had put against my credit rating. Characteristically he said that he couldn’t do that either, again, because I had “failed data protection laws”. EE is yet another company who uses data protection laws to their own advantage; to clobber consumers with them! I wonder if anyone else has been treated in this way by EE or another supplier. I’m also wondering how to get my money back – and to clear up my credit rating – from such a bunch of intractable people.

I’ve never needed a mobile phone except when travelling up north to see my mum who’s in a care home. Just before Christmas 2014 I got a mobile phone from EE so I could stay in touch with work, etc., while visiting my mum. When I set it up it was clear that it didn’t work. I tried all sorts of things and it still wouldn’t work. But I forgot about it for a few days. When I got back after Christmas I decided to phone EE and tell them that it didn’t work. The problem was that they said I didn’t pass the security questions; as a result I could not speak to anyone. Couldn’t report that my mobile didn’t work! The weeks went on and I made other calls to EE, but was told each time that I had failed the security questions. Meanwhile, of course, I was paying for this non-working phone every month by direct debit (or standing order, I forget which). This went on for month after month, and still I was paying for a service which didn’t work with no way of getting the issue resolved. It was such a small matter (as I never need to use my mobile except at Christmas when I am away with family) it was out of my mind for 99% of the time. Eventually I reasoned that I was going to be paying for this broken thing for years – and they were never going to listen to me because they would always say that I had failed the security questions. I took the only option which was then open to me. I cancelled the monthly payment to EE. Now things actually made sense, and at last I was not paying regularly for something that had never worked. At this point let me be clear about something. I could install apps on the phone and I could use it for playing solitaire and other stuff like that. But I could not do what you are expected to be able to do with a phone, i.e. communicate. EE themselves will be aware, as they would have access to such data, that: Number of phone call I made while in that contract = 0 Number of phone calls I received while in that contract = 0 Number of text messages I sent while in that contract = 0 Number of text messages I received while in that contract = 0 That is the level of service I was getting from my EE mobile phone. In the meantime I had paid over £650 for this nonsense. I phoned EE again. again I was told that I had not passed the security questions. But by this time I was aware that the operator at the other end was reading a large amount of text which had been written on my account, EE was obviously well aware of the issue. Also EE would have been aware of the 0 calls and 0 SMS aspect of my strange account. It’s just that they obviously didn’t give a monkey’s. I asked how I could resolve this. How could I prove my identity? I was told to go to my local EE store with some ID and I would be given a password which I could use in subsequent phone calls to the help centre. I did. I phoned EE with my new password and asked for my money back. I was put on hold for several minutes and then told that the account had been passed to the Collections department as it was in arrears (of course they would have been flagged as in arrears: the only way to stop being mugged every month was to cancel the monthly debit!). (Oh yes, and to add insult to injury, because of the misperception that I was in the wrong EE was allowed to put a black mark against my credit rating. I also had debt collectors writing to me. But I was able to explain to the debt collections agency what had happened and they just dropped the case against me immediately- no excuse with security questions there: I just TALKED to them and they LISTENED! It's what people do.) The person I spoke to in the Collections department acted exactly as Collections people behave and said that I could not have my money back. When I explained that consumer law was on my side he said that I had “failed data protection laws”. I reminded him that data protection laws were there to protect consumers, not corporations who sought to rip consumers off as EE was obviously very keen to do to me. I also said that I wanted EE to delete the black mark that they had put against my credit rating. Characteristically he said that he couldn’t do that either, again, because I had “failed data protection laws”. EE is yet another company who uses data protection laws to their own advantage; to clobber consumers with them! I wonder if anyone else has been treated in this way by EE or another supplier. I’m also wondering how to get my money back – and to clear up my credit rating – from such a bunch of intractable people. -

Hi, before Christmas I sent a laptop through Parcel2Go. I did not buy insurance because I usually think it's a waste of time dealing with claims if something goes wrong - and it has never gone wrong. Until now. They lost the parcel which I had to open a claim for, after which they found the parcel to my relief. Hermes who was the carrier, then tried to attempt delivery to the recipient and found that they were out (I have been in communication with the person I sold the laptop to the whole time). Hermes left a note ( I have a picture of this note) saying it was unsafe to leave the parcel anywhere - IE. the front garden . On the second delivery attempt, Hermes decided to leave it in the front garden ( I had to penetrate through Parcel2Go's chat system to gleam this information, as they did not leave a note this time!) of the recipient which happens to be in a dodgy London area on a main street (my recipient tells me, and sends me a photo too). The parcel goes missing, and I've had to refund my buyer for £240. I have already sent a 'Signed For' letter before action via Royal Mail to Parcel2Go and am counting down the 14 days. I would just like a bit of advice on what sort of grounds I have to go against them - I know that they have broken the contract by not delivering the parcel. And if it goes as far as court - some idea of what I need to go into court - ie an argument etc..

Hi, before Christmas I sent a laptop through Parcel2Go. I did not buy insurance because I usually think it's a waste of time dealing with claims if something goes wrong - and it has never gone wrong. Until now. They lost the parcel which I had to open a claim for, after which they found the parcel to my relief. Hermes who was the carrier, then tried to attempt delivery to the recipient and found that they were out (I have been in communication with the person I sold the laptop to the whole time). Hermes left a note ( I have a picture of this note) saying it was unsafe to leave the parcel anywhere - IE. the front garden . On the second delivery attempt, Hermes decided to leave it in the front garden ( I had to penetrate through Parcel2Go's chat system to gleam this information, as they did not leave a note this time!) of the recipient which happens to be in a dodgy London area on a main street (my recipient tells me, and sends me a photo too). The parcel goes missing, and I've had to refund my buyer for £240. I have already sent a 'Signed For' letter before action via Royal Mail to Parcel2Go and am counting down the 14 days. I would just like a bit of advice on what sort of grounds I have to go against them - I know that they have broken the contract by not delivering the parcel. And if it goes as far as court - some idea of what I need to go into court - ie an argument etc.. -

That's right, our lovely DWP and JCP who want you to get back in to employment but when it comes to the crunch are unwilling to help you when you need a little bit of help and this set you up to FAIL! As you know I am on UC, I lost £95.00pm when moved from ESA and HB so am struggling. I have been applying for work but getting nowhere my work coach (work coach LOL) says to me "try registering with agencies and seeing if they can help" ... OK, I email a few agencies and I geta reply from Hays and speak with them on the phone about my work history and background etc. They tell me that they may have a few openings and would like to meet me - fine, train fare to town return is £9.40. As I am on UC almost £10 means a lot of food shopping and it is an amount that I can hardly 'lose' at the moment given my financial circumstances. I email my 'work coach' and say I have arranged an appt with the agency and I would like to claim my fare back. Guess what? DWP WON'T PAY IT as it is not an actual interview just registration. So I say "if I want interviews I need to register so I am on their books" - the answer (like a robot) "No we cannot pay your fare" Fine, end of story, appointment cancelled - you want to know why I have not been doing as you say and seeing agencies? BECAUSE YOU (DWP) ARE NOT HELPING ME AT ALL WHEN I AM TRYING TO BE PROACTIVE FINDING WORK!!!! What part of I am on UC and struggle with rent/food do you not understand? Want me back in work and off UC then HELP ME WITH A LOUSY TRAIN FARE! Angry? Yeah, expected this? Yeah ... DWP ... no help at all, just keep cutting peoples money and offering no help at all. Pathetic.

That's right, our lovely DWP and JCP who want you to get back in to employment but when it comes to the crunch are unwilling to help you when you need a little bit of help and this set you up to FAIL! As you know I am on UC, I lost £95.00pm when moved from ESA and HB so am struggling. I have been applying for work but getting nowhere my work coach (work coach LOL) says to me "try registering with agencies and seeing if they can help" ... OK, I email a few agencies and I geta reply from Hays and speak with them on the phone about my work history and background etc. They tell me that they may have a few openings and would like to meet me - fine, train fare to town return is £9.40. As I am on UC almost £10 means a lot of food shopping and it is an amount that I can hardly 'lose' at the moment given my financial circumstances. I email my 'work coach' and say I have arranged an appt with the agency and I would like to claim my fare back. Guess what? DWP WON'T PAY IT as it is not an actual interview just registration. So I say "if I want interviews I need to register so I am on their books" - the answer (like a robot) "No we cannot pay your fare" Fine, end of story, appointment cancelled - you want to know why I have not been doing as you say and seeing agencies? BECAUSE YOU (DWP) ARE NOT HELPING ME AT ALL WHEN I AM TRYING TO BE PROACTIVE FINDING WORK!!!! What part of I am on UC and struggle with rent/food do you not understand? Want me back in work and off UC then HELP ME WITH A LOUSY TRAIN FARE! Angry? Yeah, expected this? Yeah ... DWP ... no help at all, just keep cutting peoples money and offering no help at all. Pathetic. -

hi all i took a contract out in sep 2016, couldnt use it, called to send back but they said i'd had it over 2 weeks so no. i never paid anything and forgot about it as they didnt take my compliant serious. they in november 2017 i they put a default on my file. just wondering if i have any recourse to get it took off or anything? Thanks in advance

hi all i took a contract out in sep 2016, couldnt use it, called to send back but they said i'd had it over 2 weeks so no. i never paid anything and forgot about it as they didnt take my compliant serious. they in november 2017 i they put a default on my file. just wondering if i have any recourse to get it took off or anything? Thanks in advance -

Hi guys, I took part in a WCA not long ago (I've been on ESA WRAG for the last year and this was a reassessment). They found me fit for work but I hadn't been able to secure all my medical evidence in time so instead submitted it along with my MR and the decision was overturned and I got letter saying I had scored the 15 points. Now here is the confusing part..... before I had all my evidence (and could submit my MR) I had to claim universal credit for around 4-5 weeks. I didn't fit the gateway conditions but I didn't have a choice at the time. I wasn't informed I am living in a "Live service" area and should have claimed old style JSA instead of UC I was just told to claim UC, now that my decision has been overturned will I go back onto ESA or will they try keep me on UC? I'm concerned as it means I lose out on money and apparently will be subjected to harsher conditionality (And shouldn't be on UC in the first place). I don't even live in a full service area. Does anyone have any idea what will happen? or what my next steps should be? There wasn't a change in my circunstances at all I was just forced to wait for more medical evidence and then appeal the decision and had to make a claim for UC or i'd have been without money. Thanks in advance for any help. Universal credit is really making a big mess of things.

-

Hi guys Simple question really, when on JSA is it possible to get bills reduced? I've heard of people doing it i.e. getting money off their water bills for example. I'm 25 single fyi no kids anything like that live in shared accommodation. Does anybody have any info about this? I live up north.

-

I don't want to go into a 1000 word essay so I've tried to summarise this down into valid points and be as brief but detailed as possible. On 24th December 2014, I visited Halfords and purchased engine oil 5L bottle and engine oil top up service. When the gentlemen from the 'we fit' team came to my car he just had a orange pouring beaker and nothing else. On pouring the engine oil into the vehicle and inspecting the dipstick I was slightly alarmed that the staff member wasn't using any measuring device and was seeming freely pouring at his hearts content, I decided to take a photograph of the top op occurring. My partner and her son where in the car whilst this was all on going. I assumed being a Halfords 'we fit' member it was probably just my own paranoia that he wasn't using a measuring device or jug. On completing the top up the staff member told me I was ready to go and it was complete and was about to shut the bonnet when I quickly noticed and informed him that the engine oil cap had not been reapplied and closed to the engine oil unit. The staff member apologised saying he had been at work since 6am and was very tired. So I left the store. On driving approximately 1-2 miles from the store smoke started coming out of the exhaust of the vehicle which i noticed from my rear view mirror and wing mirror. I immediately stopped the vehicle and as smoke was starting to appear from the exhaust and engine decided to check the engine oil top up. I at this time read the engine oil dipstick and saw that it was 3 times past the maximum mark. I took a photograph with it getting into the evening and at this point it became dark quite early and also for proof of the dipstick. I then returned to the store. On this point on returning to the store a 'engine malfunction' light appeared on my vehicle. I informed them of what had occurred and 2 members of staff inspected the engine oil. The supervisor told me she'd get equipment to drain the engine oil with the staff member. When they got this equipment because of the size of my vehicle it would not fit. Therefore the supervisor said she would ring halfords autocentre and see if an 'engine oil overfill' would cause any danger to drive. After ringing them she came back and told me that a mechanic at Halfords autocentre said the vehicle would be safe to drive with engine oil overfilled. I asked why the engine malfunction light was occurring and was told it was probably a false sensor alarm on the trip computer because the car was just 'slightly' over on engine oil. I asked what would happen if my vehicle was damaged or stopped working because of this and was told by the supervisor that I would have to seek reimbursement after purchasing the repair from Halfords Autocentre by bringing the receipt in store. To me this did not make logical sense and after googling the dangers of 'engine oil overfills' on my phone I decided to go into the store and speak to the staff to get some form of written liability and promise in writing. On speaking to the original staff member in store and his colleague they would not provide me anything in writing. I therefore decided to covertly record the conversation so I had some form of proof of the incident occurring and evidence. On speaking to the staff instore the store manager was at a till behind them. The staff told me to not worry and if anything did occur that 'Halfords would pay for it' as they had 'insurance in place for these kind of things'. I was told that mistakes did happen and before staff had fitted batteries in wrong and Halfords had paid the repair. The store manager then said that he drives his car which has 150k mileage on it with overfilled engine oil all the time and it does no damage. With this recorded I left and drove my vehicle home. I decided that something still did not seem right as I had been told 2-3 different things about reimbursement (insurance being involved...paying it myself and being reimbursed..halfords paying the repair costs..). These were three different things and to me it was not logical to drive a vehicle with a engine malfunction light. I kept the vehicle parked up and switched off and did no further driving. I rang my breakdown cover and asked them to send a mechanic out for an opinion. When the mechanic arrived he told me the car was unsafe to drive and the advice Halfords gave me was wrong. It was not safe to drive a car with overfilled engine oil as it was as bad as driving the vehicle with underfilled engine oil. He put this into a report of the breakdown he emailed to customer services, which I later requested. I therefore waited until Boxing Day and in the meanwhile i was left without a car because Halfords was not open during this period. When I rang the customer services on 26/12/14 at 2pm I spoke to someone there and they promised me that my car would be repaired until I was 'happy'. I asked them provide this in writing in which they did in the form of 'case notes' that were forwarded to me. I was told this would be done ASAP and the store would be instructed on how to do this. On being taken home by my mother at approximately 5pm I got a phonecall from someone claiming to work for Halfords claim team. I therefore spoke to them and they told me that they would require proof of the breakdown report and that the car was unsafe to drive as a result of the store's misadvice and negligence. I therefore asked them to put in writing this. Which they did in a email to me on 26/12/14 at 5.23pm I sent them the breakdown report, dipstick reading and audio recording on 26/12/14 at 9.58pm On the 29/12/14 I was contacted by the claims team via telephone on Monday throughout the day who said they would get the car towed to an autocentre to be flushed. This was done and I then awaited the car to be repaired. I asked about what would happen to any charges such as taxi for transport because of Halford's error and as since Xmas eve I had been without a car. I was told to email any costs in form of receipts and they would be reimbursed. On the 30/12/14 I was told the car would be repaired at 5pm. I decided to ring the autocentre repairing the car and ask them to specifically look at the catalytic converter and gasket and do a emissions test and thorough check of all components of the car as I was worried that from seeking advice these could be damaged. I was told this would be done. I picked the car up at 5pm and was given no receipt or invoice and was told that the car was done. Neither did I sign anything. On picking the vehicle up I noticed that before the car had been towed it had 3/4 full of petrol. It now only had below half so i took a photograph of this and asked for 25% of the petrol to be reimbursed to me, as I would not have lost this petrol if the matter had not happened and I sent Halfords the original receipt. The following day I noticed that the A/C was no longer working and neither was the audio system/CD player and these components of the vehicle had been before. I therefore tried to call Halfords but was told by the customer services team that the claims handler was busy and so they would get him to ring me back. I tried to call Halfords two more times within that week with the same response. On the 6th January (6 days) later I sent Halfords a email to the email address they had been corresponding to me at informing them of the problems with the vehicle and my concerns. I received no response and when I called on the 7th January was told that the claims handler who was dealing with my case did not work weekends and had been off so to allow a few days for a call back. On driving to Nottingham on the 9/1/15 M1 the same engine malfunction light that appeared on the engine oil overfill re-appeared on my car's trip computer and dashboard with a weird smell. I decided to pull in and call Halfords customer service and demand to speak to a manager. On calling them they put me through to the claims handler who told me to take the car to my nearest autocentre. I did this and on the 10/1/15 the autocentre confirmed that the diagnosis was that the car had a 'emissions fault' and the 'catalytic converter' needed replacing. Halfords claim team called me on the 10/1/15 and told me that the repair would be started on Monday. On Monday 12/1/15 I was called by the claims handler and told the repair would take upto 1 working day but as this autocentre was under staffed that they would require further time, so a courtesy car in the form of car hire had been sorted for me with Enterprise locally to me. I was told I had to pay the deposit amount on the vehicle but the rental fees would be covered by Halfords. Therefore with no other choice I accepted the rental vehicle. I did this and got the courtesy car. On Wednesday 14/1/15 I was called by the claims handler to say that 'due to the cost of the catalytic converter' an 'investigation' was going to take place to see how the catalytic converter had been damaged and not spotted before. I accepted Halfords to do this as I knew nothing had been done. On 23/1/15 I received an email from the claims handler saying that Halfords staff had given 3 witness statements stating that only 1 litre of engine oil was entered to the vehicle which all staff witnessed and the engine oil dipstick was seen by 3 members of staff who all said it was at minimum, thus the autocentre found the engine oil amounts to be between 1.5-2 litres over therefore this did not match amounts. The autocentre had raised no concerns at the time but the investigation concluded the engine oil amounts did not match and thus Halfords stated that after Halfords topped up the oil i must have added more oil to the vehicle and damaged the vehicle myself, therefore Halfords were no longer liable for the damage/s and expense/s and the car hire would be ended on 29/1/15. On the 30/1/15 I rang the customer services and informed them I would like to speak to someone above the claims handler as at the time of the incident occurring and the engine oil top up happening my partner who was a witness to it all was there and could testify that 3 people did not check/supervise the top up. I also informed Halfords that i had a photograph of the engine oil top up occurring which had a time/date linked to it which was further evidence. I was promised that I would get a phonecall from a higher up member of the team on the Monday 26/1/15 as the claims team did not work on a Saturday. I received no call on the 26/1/15 from anyone higher up and instead was greeted by this email from the claims handler: Dear XXXXX, I understand that you have contacted us over the weekend in regards our response dated the 23rd. I can confirm that I have already discussed this case in detail with Halfords' High Level Complaints Manager, XXXXXXXX, prior to sending the email on the 23rd and that she has confirmed our stance. As previously advised if you do wish to take this further then I can only advise that you seek independent legal advice and address any correspondence to Halfords Legal, as we will not be giving this further consideration at Customer Services. Kind regards XXXXX Claims Consultant I then decided to reply with a letter before action (LBA) and sent one via post to the address I was told to send further consideration to only (the legal team at halfords) via recorded delivery and one via email to the address for Halfords I had. I yesterday received the below response to my LBA. Dear Mr XXXXXX, I confirm receipt of your email. Taking into account our prior correspondence, we are comfortable that this is our final position on this matter, and we do not propose to respond to you further in this circumstance. We refute your assertion that liability has been accepted at any point and recommend that you do seek legal advice should you wish to take this further. We await service of your claims paperwork from your legal representative and would ask that your case number of XXXXXXX is on all paperwork submitted. Yours Sincerely XXXXXX Claims Consultant I am now fed up over the matter. I am going to commence a MCOL. But need help in writing the particulars section. I have looked on the internet but found no examples of applicable use and don't know if what I have done is good enough. Can anyone help? Oh and I forgot to mention have still not had my vehicle back..and car hire was cancelled 24 hours earlier than what I was told!

I don't want to go into a 1000 word essay so I've tried to summarise this down into valid points and be as brief but detailed as possible. On 24th December 2014, I visited Halfords and purchased engine oil 5L bottle and engine oil top up service. When the gentlemen from the 'we fit' team came to my car he just had a orange pouring beaker and nothing else. On pouring the engine oil into the vehicle and inspecting the dipstick I was slightly alarmed that the staff member wasn't using any measuring device and was seeming freely pouring at his hearts content, I decided to take a photograph of the top op occurring. My partner and her son where in the car whilst this was all on going. I assumed being a Halfords 'we fit' member it was probably just my own paranoia that he wasn't using a measuring device or jug. On completing the top up the staff member told me I was ready to go and it was complete and was about to shut the bonnet when I quickly noticed and informed him that the engine oil cap had not been reapplied and closed to the engine oil unit. The staff member apologised saying he had been at work since 6am and was very tired. So I left the store. On driving approximately 1-2 miles from the store smoke started coming out of the exhaust of the vehicle which i noticed from my rear view mirror and wing mirror. I immediately stopped the vehicle and as smoke was starting to appear from the exhaust and engine decided to check the engine oil top up. I at this time read the engine oil dipstick and saw that it was 3 times past the maximum mark. I took a photograph with it getting into the evening and at this point it became dark quite early and also for proof of the dipstick. I then returned to the store. On this point on returning to the store a 'engine malfunction' light appeared on my vehicle. I informed them of what had occurred and 2 members of staff inspected the engine oil. The supervisor told me she'd get equipment to drain the engine oil with the staff member. When they got this equipment because of the size of my vehicle it would not fit. Therefore the supervisor said she would ring halfords autocentre and see if an 'engine oil overfill' would cause any danger to drive. After ringing them she came back and told me that a mechanic at Halfords autocentre said the vehicle would be safe to drive with engine oil overfilled. I asked why the engine malfunction light was occurring and was told it was probably a false sensor alarm on the trip computer because the car was just 'slightly' over on engine oil. I asked what would happen if my vehicle was damaged or stopped working because of this and was told by the supervisor that I would have to seek reimbursement after purchasing the repair from Halfords Autocentre by bringing the receipt in store. To me this did not make logical sense and after googling the dangers of 'engine oil overfills' on my phone I decided to go into the store and speak to the staff to get some form of written liability and promise in writing. On speaking to the original staff member in store and his colleague they would not provide me anything in writing. I therefore decided to covertly record the conversation so I had some form of proof of the incident occurring and evidence. On speaking to the staff instore the store manager was at a till behind them. The staff told me to not worry and if anything did occur that 'Halfords would pay for it' as they had 'insurance in place for these kind of things'. I was told that mistakes did happen and before staff had fitted batteries in wrong and Halfords had paid the repair. The store manager then said that he drives his car which has 150k mileage on it with overfilled engine oil all the time and it does no damage. With this recorded I left and drove my vehicle home. I decided that something still did not seem right as I had been told 2-3 different things about reimbursement (insurance being involved...paying it myself and being reimbursed..halfords paying the repair costs..). These were three different things and to me it was not logical to drive a vehicle with a engine malfunction light. I kept the vehicle parked up and switched off and did no further driving. I rang my breakdown cover and asked them to send a mechanic out for an opinion. When the mechanic arrived he told me the car was unsafe to drive and the advice Halfords gave me was wrong. It was not safe to drive a car with overfilled engine oil as it was as bad as driving the vehicle with underfilled engine oil. He put this into a report of the breakdown he emailed to customer services, which I later requested. I therefore waited until Boxing Day and in the meanwhile i was left without a car because Halfords was not open during this period. When I rang the customer services on 26/12/14 at 2pm I spoke to someone there and they promised me that my car would be repaired until I was 'happy'. I asked them provide this in writing in which they did in the form of 'case notes' that were forwarded to me. I was told this would be done ASAP and the store would be instructed on how to do this. On being taken home by my mother at approximately 5pm I got a phonecall from someone claiming to work for Halfords claim team. I therefore spoke to them and they told me that they would require proof of the breakdown report and that the car was unsafe to drive as a result of the store's misadvice and negligence. I therefore asked them to put in writing this. Which they did in a email to me on 26/12/14 at 5.23pm I sent them the breakdown report, dipstick reading and audio recording on 26/12/14 at 9.58pm On the 29/12/14 I was contacted by the claims team via telephone on Monday throughout the day who said they would get the car towed to an autocentre to be flushed. This was done and I then awaited the car to be repaired. I asked about what would happen to any charges such as taxi for transport because of Halford's error and as since Xmas eve I had been without a car. I was told to email any costs in form of receipts and they would be reimbursed. On the 30/12/14 I was told the car would be repaired at 5pm. I decided to ring the autocentre repairing the car and ask them to specifically look at the catalytic converter and gasket and do a emissions test and thorough check of all components of the car as I was worried that from seeking advice these could be damaged. I was told this would be done. I picked the car up at 5pm and was given no receipt or invoice and was told that the car was done. Neither did I sign anything. On picking the vehicle up I noticed that before the car had been towed it had 3/4 full of petrol. It now only had below half so i took a photograph of this and asked for 25% of the petrol to be reimbursed to me, as I would not have lost this petrol if the matter had not happened and I sent Halfords the original receipt. The following day I noticed that the A/C was no longer working and neither was the audio system/CD player and these components of the vehicle had been before. I therefore tried to call Halfords but was told by the customer services team that the claims handler was busy and so they would get him to ring me back. I tried to call Halfords two more times within that week with the same response. On the 6th January (6 days) later I sent Halfords a email to the email address they had been corresponding to me at informing them of the problems with the vehicle and my concerns. I received no response and when I called on the 7th January was told that the claims handler who was dealing with my case did not work weekends and had been off so to allow a few days for a call back. On driving to Nottingham on the 9/1/15 M1 the same engine malfunction light that appeared on the engine oil overfill re-appeared on my car's trip computer and dashboard with a weird smell. I decided to pull in and call Halfords customer service and demand to speak to a manager. On calling them they put me through to the claims handler who told me to take the car to my nearest autocentre. I did this and on the 10/1/15 the autocentre confirmed that the diagnosis was that the car had a 'emissions fault' and the 'catalytic converter' needed replacing. Halfords claim team called me on the 10/1/15 and told me that the repair would be started on Monday. On Monday 12/1/15 I was called by the claims handler and told the repair would take upto 1 working day but as this autocentre was under staffed that they would require further time, so a courtesy car in the form of car hire had been sorted for me with Enterprise locally to me. I was told I had to pay the deposit amount on the vehicle but the rental fees would be covered by Halfords. Therefore with no other choice I accepted the rental vehicle. I did this and got the courtesy car. On Wednesday 14/1/15 I was called by the claims handler to say that 'due to the cost of the catalytic converter' an 'investigation' was going to take place to see how the catalytic converter had been damaged and not spotted before. I accepted Halfords to do this as I knew nothing had been done. On 23/1/15 I received an email from the claims handler saying that Halfords staff had given 3 witness statements stating that only 1 litre of engine oil was entered to the vehicle which all staff witnessed and the engine oil dipstick was seen by 3 members of staff who all said it was at minimum, thus the autocentre found the engine oil amounts to be between 1.5-2 litres over therefore this did not match amounts. The autocentre had raised no concerns at the time but the investigation concluded the engine oil amounts did not match and thus Halfords stated that after Halfords topped up the oil i must have added more oil to the vehicle and damaged the vehicle myself, therefore Halfords were no longer liable for the damage/s and expense/s and the car hire would be ended on 29/1/15. On the 30/1/15 I rang the customer services and informed them I would like to speak to someone above the claims handler as at the time of the incident occurring and the engine oil top up happening my partner who was a witness to it all was there and could testify that 3 people did not check/supervise the top up. I also informed Halfords that i had a photograph of the engine oil top up occurring which had a time/date linked to it which was further evidence. I was promised that I would get a phonecall from a higher up member of the team on the Monday 26/1/15 as the claims team did not work on a Saturday. I received no call on the 26/1/15 from anyone higher up and instead was greeted by this email from the claims handler: Dear XXXXX, I understand that you have contacted us over the weekend in regards our response dated the 23rd. I can confirm that I have already discussed this case in detail with Halfords' High Level Complaints Manager, XXXXXXXX, prior to sending the email on the 23rd and that she has confirmed our stance. As previously advised if you do wish to take this further then I can only advise that you seek independent legal advice and address any correspondence to Halfords Legal, as we will not be giving this further consideration at Customer Services. Kind regards XXXXX Claims Consultant I then decided to reply with a letter before action (LBA) and sent one via post to the address I was told to send further consideration to only (the legal team at halfords) via recorded delivery and one via email to the address for Halfords I had. I yesterday received the below response to my LBA. Dear Mr XXXXXX, I confirm receipt of your email. Taking into account our prior correspondence, we are comfortable that this is our final position on this matter, and we do not propose to respond to you further in this circumstance. We refute your assertion that liability has been accepted at any point and recommend that you do seek legal advice should you wish to take this further. We await service of your claims paperwork from your legal representative and would ask that your case number of XXXXXXX is on all paperwork submitted. Yours Sincerely XXXXXX Claims Consultant I am now fed up over the matter. I am going to commence a MCOL. But need help in writing the particulars section. I have looked on the internet but found no examples of applicable use and don't know if what I have done is good enough. Can anyone help? Oh and I forgot to mention have still not had my vehicle back..and car hire was cancelled 24 hours earlier than what I was told! -

I am making a query on behalf of a friend. She is a carer for her autistic sister and made her employers (local government) aware of this 5 years ago when she started work as a Registries and Ceremonies Officer. She was frequently late for work as she had to wait for the transport to collect her to take her to the day centre daily due to this she asked to start work later instead of the normal 9 am. During her period of employment she felt bullied and harassed by her supervisor who complained about her lateness consistently and belittled her by calling her 'Oi you' and not as part of the team. Through the stress of caring for her sister daily and harassment my friend put in a complaint about her supervisor on 3rd June 2016. The councils policy on complaints is stated as: complaint received, investigation and response - within 5 working days any investigation necessary - with 10 working days She did not receive any response to this complaint and there was no investigation. She was asked whether she could undertake a ceremony on 24th July 2016 at 1pm however due to her caring responsibilities she was unable to do this. She informed her supervisor of this on 23rd July whilst at work and it appears that there was a disagreement and her supervisor stated that ' she behaved in a threatening and intimidating manner' towards her during this discussion. My friend stated that she did not but was very anxious and stressed on this day due to the pressure of her caring responsibilities and has been supported by her GP but felt very unsupported by her employers and her supervisor. Allegations made by the supervisor were stated as correct by people that worked with her but not regarded as colleagues due to their exclusion of her. Anyway following the allegations she was suspended from work on 25th July 2016 and interviews were taken in September, November and December 2016 from my friend, the supervision and other witnesses. During this period my friend sent further complaints of harassment and bullying on 9th and 14th September bearing in mind that her initial complaint made in June was not investigated which she also highlighted. She was ill advised by a union representative to accept the charge of gross misconduct and was dismissed on 26th April 2017 and placed on the redeployment list for 12 weeks, in which she was seen weekly for any suitable positions. 12 weeks was also her notice period. The documents state that any complaints made during the periods of disciplinary will be dealt with within the hearing but they were brushed over and the initial complaint has never been discussed or addressed. She has appealed against her dismissal citing that she was wrongly advised, she had a nervous breakdown and they refused to re-schedule the meeting as she was unable to contribute and agreed to everything, she worked with the local authority since 2002 and had a clean record. It was recommended by the Investigating Officer that she was transferred to another role not dismissed or redeployed. She now needs to write another appeal and after seeing a solicitor she would like to still list the above but also add associative disability discrimination as she has caring duties which have been confirmed by the local authority in writing and also been supported through this ordeal by her GP, harassment as they refused to allow her flexi time to attend to her sister and also the behaviour of her supervision by calling her 'oi you' and the conduct of her employers. (The later has been suggested by a Solicitor who looked over the papers). Can anyone advise as she needs to write an appeal to hand in on monday:sad:

I am making a query on behalf of a friend. She is a carer for her autistic sister and made her employers (local government) aware of this 5 years ago when she started work as a Registries and Ceremonies Officer. She was frequently late for work as she had to wait for the transport to collect her to take her to the day centre daily due to this she asked to start work later instead of the normal 9 am. During her period of employment she felt bullied and harassed by her supervisor who complained about her lateness consistently and belittled her by calling her 'Oi you' and not as part of the team. Through the stress of caring for her sister daily and harassment my friend put in a complaint about her supervisor on 3rd June 2016. The councils policy on complaints is stated as: complaint received, investigation and response - within 5 working days any investigation necessary - with 10 working days She did not receive any response to this complaint and there was no investigation. She was asked whether she could undertake a ceremony on 24th July 2016 at 1pm however due to her caring responsibilities she was unable to do this. She informed her supervisor of this on 23rd July whilst at work and it appears that there was a disagreement and her supervisor stated that ' she behaved in a threatening and intimidating manner' towards her during this discussion. My friend stated that she did not but was very anxious and stressed on this day due to the pressure of her caring responsibilities and has been supported by her GP but felt very unsupported by her employers and her supervisor. Allegations made by the supervisor were stated as correct by people that worked with her but not regarded as colleagues due to their exclusion of her. Anyway following the allegations she was suspended from work on 25th July 2016 and interviews were taken in September, November and December 2016 from my friend, the supervision and other witnesses. During this period my friend sent further complaints of harassment and bullying on 9th and 14th September bearing in mind that her initial complaint made in June was not investigated which she also highlighted. She was ill advised by a union representative to accept the charge of gross misconduct and was dismissed on 26th April 2017 and placed on the redeployment list for 12 weeks, in which she was seen weekly for any suitable positions. 12 weeks was also her notice period. The documents state that any complaints made during the periods of disciplinary will be dealt with within the hearing but they were brushed over and the initial complaint has never been discussed or addressed. She has appealed against her dismissal citing that she was wrongly advised, she had a nervous breakdown and they refused to re-schedule the meeting as she was unable to contribute and agreed to everything, she worked with the local authority since 2002 and had a clean record. It was recommended by the Investigating Officer that she was transferred to another role not dismissed or redeployed. She now needs to write another appeal and after seeing a solicitor she would like to still list the above but also add associative disability discrimination as she has caring duties which have been confirmed by the local authority in writing and also been supported through this ordeal by her GP, harassment as they refused to allow her flexi time to attend to her sister and also the behaviour of her supervision by calling her 'oi you' and the conduct of her employers. (The later has been suggested by a Solicitor who looked over the papers). Can anyone advise as she needs to write an appeal to hand in on monday:sad: -

RBS made me an offer of £2k for ppi from 2003 They said they would pay me by cheque. However, the other day I had a message saying "we have deposited the money into your current account. On checking this I found that they hadn't deposited into my account, but to their own holding account pending further investigations. I phoned the ppi office to be told that the loan on which I claimed the ppi had arrears and so they were investigating. However, I then phoned RBS credit management and they confirmed I had no outstanding debts, but then claimed they still need to investigate. If they suspected this, why did they agree that ppi was refundable and why can't they find any evidence. Really frustrating! I have to wait another 28 days now while they investigate. Anyone dealt with this before?

RBS made me an offer of £2k for ppi from 2003 They said they would pay me by cheque. However, the other day I had a message saying "we have deposited the money into your current account. On checking this I found that they hadn't deposited into my account, but to their own holding account pending further investigations. I phoned the ppi office to be told that the loan on which I claimed the ppi had arrears and so they were investigating. However, I then phoned RBS credit management and they confirmed I had no outstanding debts, but then claimed they still need to investigate. If they suspected this, why did they agree that ppi was refundable and why can't they find any evidence. Really frustrating! I have to wait another 28 days now while they investigate. Anyone dealt with this before? -

Hi first time poster after advice and assurance ! My daughter is a student in Derby and moved into a rented city centre flat in July 2016. There are no parking spaces allocated to the flats but the roads around the area state they are 'pay at machine' or 'permit holders'. She visited the local authority with her tenancy agreement and proof of car ownership and was issued a residents permit, which she was charged for, valid until July 2017. She has parked regularly in these streets without problems 19th Jan 2017 when she received a PCN. She then received a letter dated 20th Jan stating that her flats were not included in the permit area and that the Permit was issued by mistake. She queried this with the Authority and was told on 9th Feb 2017 that her permit was no longer valid and she would be liable for any further PCNs ( they have cancelled the one dated 19th Jan ). However to find an alternative private parking space took time - she eventually secured one on 12th March 2017, in the meantime she received a further four PCNs which we contested and they have refused to cancel. My argument is that they issued the permit - albeit mistakenly - and should either let the permit run to expiry or at least cancel it with sufficient notice to allow suitable alternative arrangements to be made. Our next step is to go to trafficpenaltytribunal.gov any help or advice would be gratefully received !

Hi first time poster after advice and assurance ! My daughter is a student in Derby and moved into a rented city centre flat in July 2016. There are no parking spaces allocated to the flats but the roads around the area state they are 'pay at machine' or 'permit holders'. She visited the local authority with her tenancy agreement and proof of car ownership and was issued a residents permit, which she was charged for, valid until July 2017. She has parked regularly in these streets without problems 19th Jan 2017 when she received a PCN. She then received a letter dated 20th Jan stating that her flats were not included in the permit area and that the Permit was issued by mistake. She queried this with the Authority and was told on 9th Feb 2017 that her permit was no longer valid and she would be liable for any further PCNs ( they have cancelled the one dated 19th Jan ). However to find an alternative private parking space took time - she eventually secured one on 12th March 2017, in the meantime she received a further four PCNs which we contested and they have refused to cancel. My argument is that they issued the permit - albeit mistakenly - and should either let the permit run to expiry or at least cancel it with sufficient notice to allow suitable alternative arrangements to be made. Our next step is to go to trafficpenaltytribunal.gov any help or advice would be gratefully received ! -

Hi people from the forum, I am in a situation where I would appreciate assistance. I am not a native speaker so apologies in advance for any mistake that might be in there! I got into a one-year contract with a gym in July, consisting of monthly payments of 60 pounds; in October I was accepted in a masters degree (which I had not applied for at the time I registered at the gym) in a foreign country. I enrolled and left the UK, but I left my bank account open and there was some money on it, I did not hear from the gym until January, when it turns out the money had been depleted and they had been unable to collect payment. I immediately contacted the gym and asked if I could cancel on the grounds that I now didn't have a job anymore (I had one prior to my enrollment but obviously had to quit) and wasn't even in the UK. I assumed this would be valid as an unforeseen change of circumstances. The person asked me for proof that I did not work anymore, so I directed her to my former HR. I did not hear back so I assumed everything was well, and I stopped the debit from my account. Two months later, another representative from the gym contacted me, notifying me that I owed two months. I referred him to my prior emails, and he showed me an email the first person had sent me, which I had not seen, where she stated that since I had quit and had not been fired, I still owed the money. I re-explained my situation, that I had no income now and was living in a different country, and the guy told me he understood, that he would put a note on my account and that I should notify him of when I would be able to make payment again. I told him next October (as my masters will be finished and I will have a job -hopefully), and thanked him for his understanding. I assumed everything was fine. Then last week my former roommate told me I had received a letter from ARC Europe (I asked her to open it in case it might be something administrative I had overlooked). Though I am two months late (120 pounds) and have gotten an email from the guy at the Gym that I would be able to resume payment later, a "J. Turner" requests I pay 299 pounds within ten days or he may go to court. Now I know this is more or less typical behavior from solicitors, but I don't really understand why they would come after me after the guy at the Gym emailed that I was fine, and why they'd ask for 299 pounds. What do you think of this situation? What is my best course of action, considering I will probably not be coming back to the UK in the near future, even after my masters? Thank you!

Hi people from the forum, I am in a situation where I would appreciate assistance. I am not a native speaker so apologies in advance for any mistake that might be in there! I got into a one-year contract with a gym in July, consisting of monthly payments of 60 pounds; in October I was accepted in a masters degree (which I had not applied for at the time I registered at the gym) in a foreign country. I enrolled and left the UK, but I left my bank account open and there was some money on it, I did not hear from the gym until January, when it turns out the money had been depleted and they had been unable to collect payment. I immediately contacted the gym and asked if I could cancel on the grounds that I now didn't have a job anymore (I had one prior to my enrollment but obviously had to quit) and wasn't even in the UK. I assumed this would be valid as an unforeseen change of circumstances. The person asked me for proof that I did not work anymore, so I directed her to my former HR. I did not hear back so I assumed everything was well, and I stopped the debit from my account. Two months later, another representative from the gym contacted me, notifying me that I owed two months. I referred him to my prior emails, and he showed me an email the first person had sent me, which I had not seen, where she stated that since I had quit and had not been fired, I still owed the money. I re-explained my situation, that I had no income now and was living in a different country, and the guy told me he understood, that he would put a note on my account and that I should notify him of when I would be able to make payment again. I told him next October (as my masters will be finished and I will have a job -hopefully), and thanked him for his understanding. I assumed everything was fine. Then last week my former roommate told me I had received a letter from ARC Europe (I asked her to open it in case it might be something administrative I had overlooked). Though I am two months late (120 pounds) and have gotten an email from the guy at the Gym that I would be able to resume payment later, a "J. Turner" requests I pay 299 pounds within ten days or he may go to court. Now I know this is more or less typical behavior from solicitors, but I don't really understand why they would come after me after the guy at the Gym emailed that I was fine, and why they'd ask for 299 pounds. What do you think of this situation? What is my best course of action, considering I will probably not be coming back to the UK in the near future, even after my masters? Thank you! -

Hi all My Wife was dissmised for alleged gross misconduct for chasing on social media about work all though no mention of her work name or any second names used during conversation ( she thought she was in chat mode with a friend not on live site). Went to C.A.B. got told can't do anything as she had only been at her job nine months. Today she has received her final wage slip after waiting a month they paid the 3 weeks wages and any owed holiday pay then took back the full wages for the month before. What I need to know is can we appellant the sacking and what do I do about the wages they also owe her for 300 pound worth of overtime short paid over Christmas.

Hi all My Wife was dissmised for alleged gross misconduct for chasing on social media about work all though no mention of her work name or any second names used during conversation ( she thought she was in chat mode with a friend not on live site). Went to C.A.B. got told can't do anything as she had only been at her job nine months. Today she has received her final wage slip after waiting a month they paid the 3 weeks wages and any owed holiday pay then took back the full wages for the month before. What I need to know is can we appellant the sacking and what do I do about the wages they also owe her for 300 pound worth of overtime short paid over Christmas. -

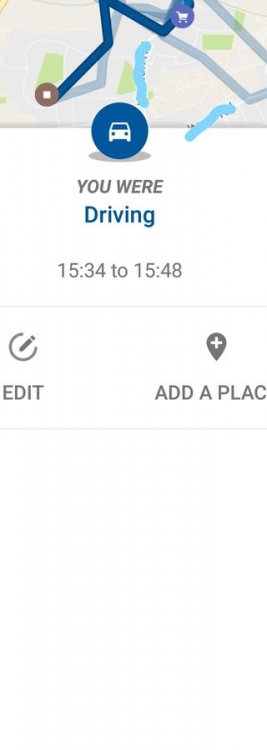

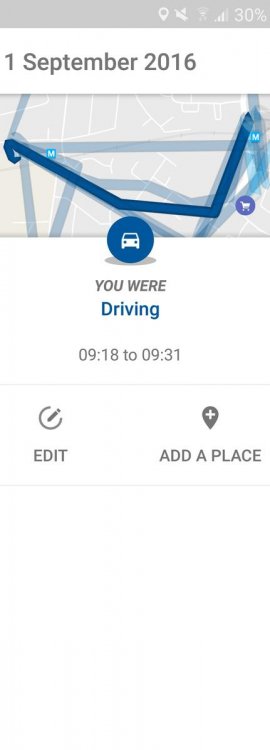

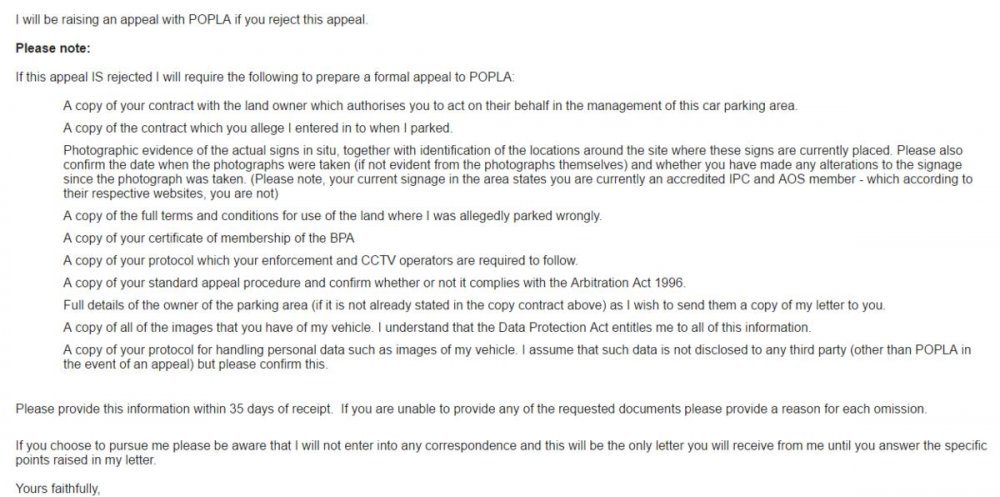

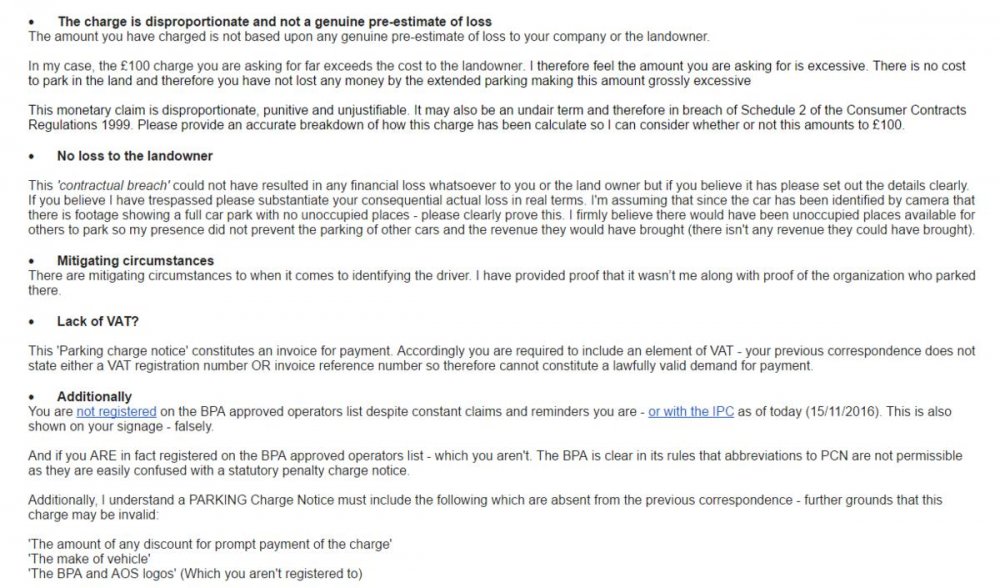

Hi everybody, I've been pointed in this direction by a reddit user for help relating to a Parking Charge Notice. I took my car to my local garage to get an MOT check done on 01/09/2016. The owner then drove the car to the MOT garage and parked it up inside and then returned back to his garage. A few hours later I hadn't received a phone call yet to say it had been completed so I rang up to find out that my car was OK to collect. I then made my way there and collected my car from the (private) parking lot less than 30 meters away from the MOT garage. Fast-forward a week or so and I've received a letter in the post saying my car was broke the allowed parking period in the car park and I need to pay a fine for £100, I replied to the letter stating the address of my local garage and to take it up with them - I then received an email a month later saying that the time period had ran out and I had to pay urgently - I reminded them that I sent a letter in the post some time later I received this response I then replied with this email (1, 2) using a template I was advised to use. I then explained to take this matter up with my local garage and the MOT centre. I then received this. What should my next action be? I'm really not in a position to be able to afford £100 so close to Christmas. My local garage has told me that they can vouch that I wasn't the person who drove the car there/parked it in the space. Any ideas? Thanks in advance EDIT: I now have a signed and stamped note from the doctors saying I was there when this incident took place. I've managed to find my google location history showing the time I dropped the car off at my local garage and when I picked it up from the MOT centre, this is attached. My local garage has said if it goes to court they will provide further evidence that I didn't have the car after 9am until Also included text to girlfriend with date and timestamp. Omitted names etc for confidentiality EDIT 2 - it turns out I cant include links or images, any idea on this first?

Hi everybody, I've been pointed in this direction by a reddit user for help relating to a Parking Charge Notice. I took my car to my local garage to get an MOT check done on 01/09/2016. The owner then drove the car to the MOT garage and parked it up inside and then returned back to his garage. A few hours later I hadn't received a phone call yet to say it had been completed so I rang up to find out that my car was OK to collect. I then made my way there and collected my car from the (private) parking lot less than 30 meters away from the MOT garage. Fast-forward a week or so and I've received a letter in the post saying my car was broke the allowed parking period in the car park and I need to pay a fine for £100, I replied to the letter stating the address of my local garage and to take it up with them - I then received an email a month later saying that the time period had ran out and I had to pay urgently - I reminded them that I sent a letter in the post some time later I received this response I then replied with this email (1, 2) using a template I was advised to use. I then explained to take this matter up with my local garage and the MOT centre. I then received this. What should my next action be? I'm really not in a position to be able to afford £100 so close to Christmas. My local garage has told me that they can vouch that I wasn't the person who drove the car there/parked it in the space. Any ideas? Thanks in advance EDIT: I now have a signed and stamped note from the doctors saying I was there when this incident took place. I've managed to find my google location history showing the time I dropped the car off at my local garage and when I picked it up from the MOT centre, this is attached. My local garage has said if it goes to court they will provide further evidence that I didn't have the car after 9am until Also included text to girlfriend with date and timestamp. Omitted names etc for confidentiality EDIT 2 - it turns out I cant include links or images, any idea on this first?.thumb.jpg.b57560183b11d2f268a05ddebc499501.jpg)

-

NPower took me to court i got CCJ then gave me a refund???

wag posted a topic in General Debt Issues

Hi, I was taken to Court by NPower about 2 years ago for a utilities debt of around £750.00, i was allowed to pay it off in 3 monthly payments which i did, a couple of months ago i got a letter and a refund of £282.00 and an apology for the delay in spotting that i had been overcharged. the annoying thing is, that if the original debt had been £282.00 less i could have borrowed the money to pay it off and avoid getting a CCJ. Can a CCJ be removed if the company later realises they made a mistake? thanks -

Got a bit of an annoying issue with Royal Mail. Will try and keep this as brief as possible. I sent a parcel to friends in Germany containing some baby clothing for which I paid just over four pound to go as a small parcel (airmail). The parcel never arrived and six weeks after sending it out it came back to me, in a clear plastic bag from Royal Mail, my parcel was more or less obliterated, the shipping bag I used was totally shredded with the contents falling out. The address was no longer visible as that part of the mailing bag was totally ripped away. Only my return address was still legible, so it was returned to me by what the enclosed apology letter says was Royal Mail’s lost mail centre. The contents although partly visible / fallen out were still undamaged, just a bit blackened from whatever caused the bag to be destroyed. (A machine ?) I managed to clean the contents (clothing ) but had to pay again to re-send them. I decided to make a claim against Royal Mail for the wasted postage costs for the first attempt to send the parcel. I submitted evidence of the destroyed packing and my proof of posting slip. Royal Mail then requested from me proof of value of the contents as otherwise apparently they couldn’t process my claim. I wrote back to them stating that I managed to salvage the contents and I didn’t have any receipts for the clothing as it wasn’t new and even if it had been I would not have kept the receipts. I couldn’t have anticipated that Royal Mail would destroy the parcel and then asking to see receipts for the contents to be honest. I told them I only wanted a refund for the wasted postage costs as they failed to deliver the parcel to Germany, which is what I paid for. They wrote to me today refusing any compensation / refund, because (I quote) “a postage refund is only available in the event of loss. In the event of damage to an item, we will look to compensate for the damaged iten, but still no potage refund is available.” They apologised for the inconvenience and that was it. I am not happy about this and would still like to pursue this as they charged me for a service they failed to carry out. What are my next options if any ?

Got a bit of an annoying issue with Royal Mail. Will try and keep this as brief as possible. I sent a parcel to friends in Germany containing some baby clothing for which I paid just over four pound to go as a small parcel (airmail). The parcel never arrived and six weeks after sending it out it came back to me, in a clear plastic bag from Royal Mail, my parcel was more or less obliterated, the shipping bag I used was totally shredded with the contents falling out. The address was no longer visible as that part of the mailing bag was totally ripped away. Only my return address was still legible, so it was returned to me by what the enclosed apology letter says was Royal Mail’s lost mail centre. The contents although partly visible / fallen out were still undamaged, just a bit blackened from whatever caused the bag to be destroyed. (A machine ?) I managed to clean the contents (clothing ) but had to pay again to re-send them. I decided to make a claim against Royal Mail for the wasted postage costs for the first attempt to send the parcel. I submitted evidence of the destroyed packing and my proof of posting slip. Royal Mail then requested from me proof of value of the contents as otherwise apparently they couldn’t process my claim. I wrote back to them stating that I managed to salvage the contents and I didn’t have any receipts for the clothing as it wasn’t new and even if it had been I would not have kept the receipts. I couldn’t have anticipated that Royal Mail would destroy the parcel and then asking to see receipts for the contents to be honest. I told them I only wanted a refund for the wasted postage costs as they failed to deliver the parcel to Germany, which is what I paid for. They wrote to me today refusing any compensation / refund, because (I quote) “a postage refund is only available in the event of loss. In the event of damage to an item, we will look to compensate for the damaged iten, but still no potage refund is available.” They apologised for the inconvenience and that was it. I am not happy about this and would still like to pursue this as they charged me for a service they failed to carry out. What are my next options if any ? -

We had a loan with welcome finance many years ago. Phoned them up last month regarding miss selling of ppi to which they said there was some on the account so we started the claim. Everything on the phone was fine no issues, the loan account was closed. We've had our decision letter today saying they were using the compensation to settle the loan. It was secured against our house, we sold the property in 2004. It seems there was was some of the loan left outstanding after the sale. We've had no correspondence or notifications regarding any outstanding sums on the loan. We've been easily findable (plenty of other DCA's have found us in the past) They've said that the loan was written off and closed in 2010, their own words. My question is, if the loans written off and closed can they use PPi compensation against it?

We had a loan with welcome finance many years ago. Phoned them up last month regarding miss selling of ppi to which they said there was some on the account so we started the claim. Everything on the phone was fine no issues, the loan account was closed. We've had our decision letter today saying they were using the compensation to settle the loan. It was secured against our house, we sold the property in 2004. It seems there was was some of the loan left outstanding after the sale. We've had no correspondence or notifications regarding any outstanding sums on the loan. We've been easily findable (plenty of other DCA's have found us in the past) They've said that the loan was written off and closed in 2010, their own words. My question is, if the loans written off and closed can they use PPi compensation against it? -

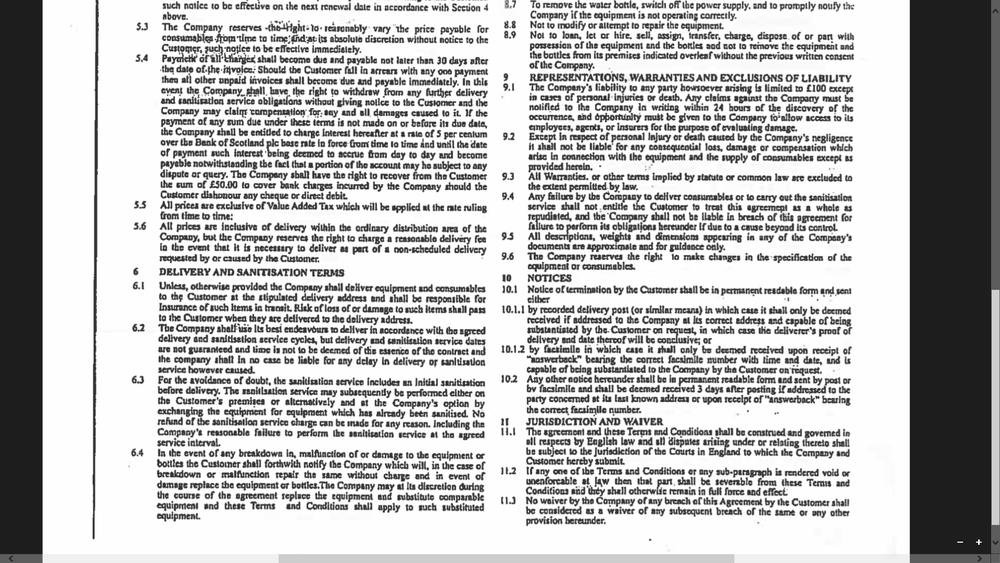

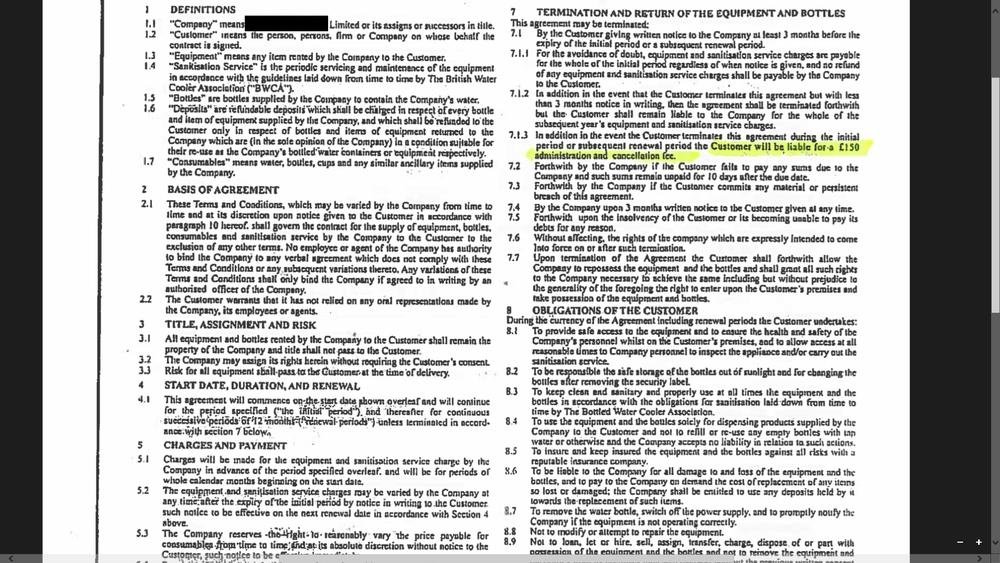

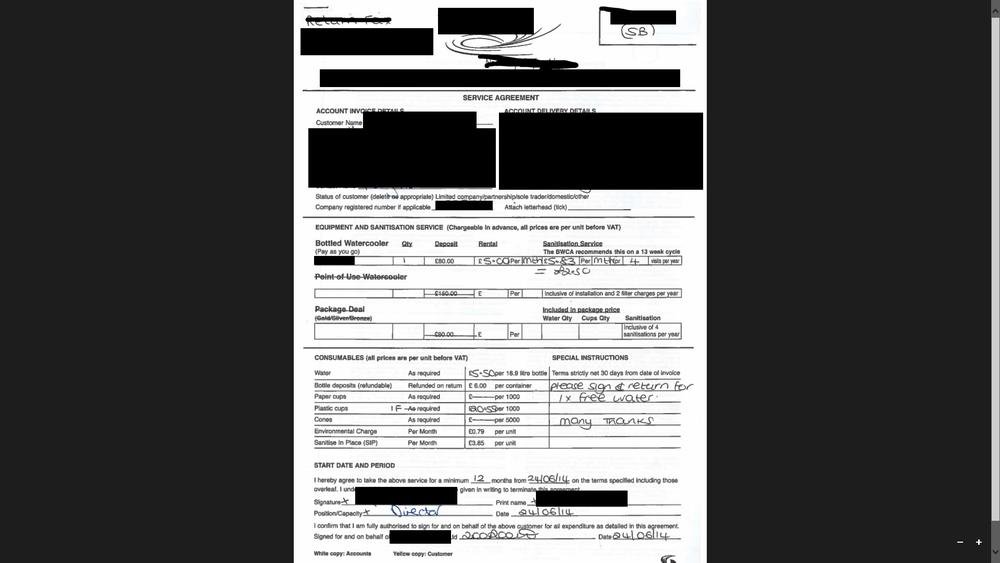

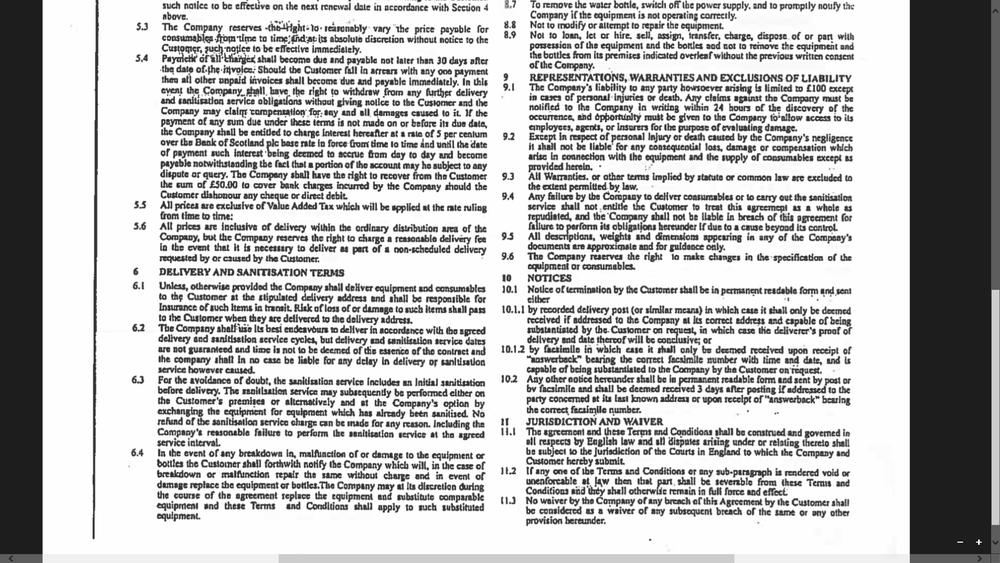

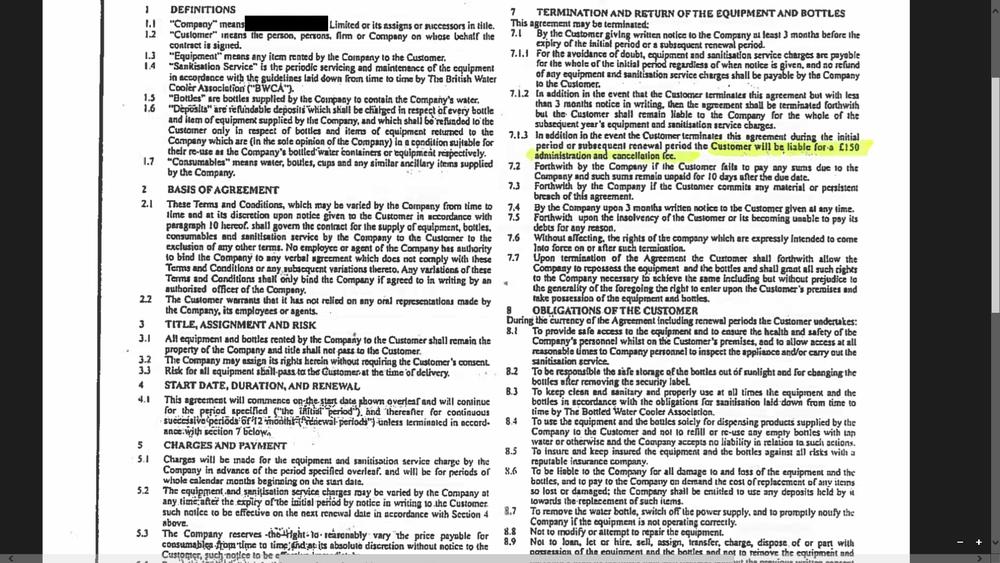

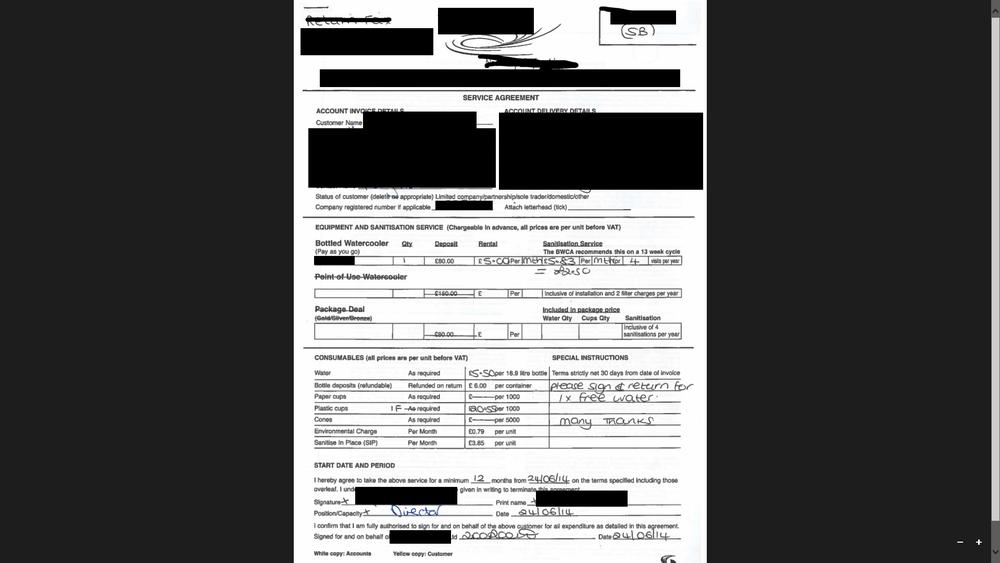

So, long story short, we caught the Water bottle provider (for office water) filling his pockets with mints from the meeting room. He was only supposed to, and trusted with, being in there to change the water bottles over. we dont want this little thief in the building any longer we called to terminate the water contract - they have stated a) they dont give two hoots about their staff and b) they wont cancel the water order, will, come to premises and take the goods and continue to bill us c) "bring it on, we have lawyers" No apology, nothing. here is the agreement enclosed that we signed, yes we can give three months notice as its dated 2014. what rights do I have - without court, bearing in mind its a civil agreement not a criminal one - yet my issue is technically criminal (ok its only mints but the principle is there). we threatend the fact we may call the police about this and for them to just take their stuff and go - but he proceeded to take that as blackmail! We just dont want them in the building ever again nor do we want to pay them a penny more! They are also member sof: http://safecontractor.com/ and http://bwca.org.uk/