Showing results for tags 'agreement'.

-

hi , i have a loan from welcome F (secured) but on the credit agreement my address does not have the flat number of my home , only the address of the whole building as there is 8 houses in the building does this mean the agreement is not complete right?

hi , i have a loan from welcome F (secured) but on the credit agreement my address does not have the flat number of my home , only the address of the whole building as there is 8 houses in the building does this mean the agreement is not complete right? -

.. I sent off a CCA request six months ago which has not been provided, the account is in dispute, i have been receiving 'arrears' letters since. My question is, would it help to send back the latest arrears letter with a "No contract. Return to sender" label, or sit on my hands? Thanks Pencil.

.. I sent off a CCA request six months ago which has not been provided, the account is in dispute, i have been receiving 'arrears' letters since. My question is, would it help to send back the latest arrears letter with a "No contract. Return to sender" label, or sit on my hands? Thanks Pencil. -

Hi guys, Been helping out yet another friend with some advice and as its some time since I advised on here regulary I thought i would get up to speed. My mate took out a Conditional Sale Agreement for a car with one of the subprime car finance companies. He made his first 3 payments of approx £260 Being self employed sometimes money doesn't come in quick enough and he was late with his next payment. They sent him a default notice The arrears consisted of 1 month instalment £48 of charges stated as administration costs He paid the 1 month arrears (but not the admin costs) 1 day late after the deadline. He then came home to a letter put through his door and a contact number. he rang it, it was a man who said he had a repossession order for the car. My mate sent him photos of the payments he had made in the 4 months he had the car and the repo man said he was going to refer it back to his office. In the mean time my mate spoke to me and I looked through his paperwork and noticed that he had overpaid 1 month by £20 . on his behalf I rang the finance company pretending to be him. They told me that the contract had been terminated and he had to either pay a final settlement or the car would be repossessed the next day. I said how much currently is the arrears, £48 they replied. So your repossessing for £48? Yes . Cant he just pay the £48? No its too late, your contracts been terminated , there is nothing you can do about it. i said lets go through the payments and he agreed that there there was an overpayment of £20 they hadn't accounted for . I said so your default amount is incorrect then? He said that doesn't matter, I argued. In the end I said you get us a settlement figure and I will look for your invalid default notice (I hadn't seen it at this point) 30 mins later my mate has a missed call from them, he phones back and offices are closed. 10 mins later they phoned again (this is out of hours) and said "Mr ***** , i wasn't very happy with the whole situation , i have spoken with my manager and am delighted to say he has agreed to reinstate your agreement tomorrow as long as you ring up and pay the £48 arrears and this months payment which becomes due in the next few days" he does all this and its all back on. A month later, he hadn't reinstated his direct debit , so he pays online using their payment portal onvtime. 5 days later he gets a default sums notice- payment not received by DD £18 charge This just raises a few questions for me 1 Can they default him in the first instance for being just 1 payment in arrears? 2 Can they add charges onto the default for £18 admin fees for non payment by DD? 3 Obviously the default was invalid otherwise they wouldn't of panicked and reinstated it, but if the default is on his credit file can we get it removed? 4 Is there a difference between a default sums notice and a default notice? Thanks in advance

Hi guys, Been helping out yet another friend with some advice and as its some time since I advised on here regulary I thought i would get up to speed. My mate took out a Conditional Sale Agreement for a car with one of the subprime car finance companies. He made his first 3 payments of approx £260 Being self employed sometimes money doesn't come in quick enough and he was late with his next payment. They sent him a default notice The arrears consisted of 1 month instalment £48 of charges stated as administration costs He paid the 1 month arrears (but not the admin costs) 1 day late after the deadline. He then came home to a letter put through his door and a contact number. he rang it, it was a man who said he had a repossession order for the car. My mate sent him photos of the payments he had made in the 4 months he had the car and the repo man said he was going to refer it back to his office. In the mean time my mate spoke to me and I looked through his paperwork and noticed that he had overpaid 1 month by £20 . on his behalf I rang the finance company pretending to be him. They told me that the contract had been terminated and he had to either pay a final settlement or the car would be repossessed the next day. I said how much currently is the arrears, £48 they replied. So your repossessing for £48? Yes . Cant he just pay the £48? No its too late, your contracts been terminated , there is nothing you can do about it. i said lets go through the payments and he agreed that there there was an overpayment of £20 they hadn't accounted for . I said so your default amount is incorrect then? He said that doesn't matter, I argued. In the end I said you get us a settlement figure and I will look for your invalid default notice (I hadn't seen it at this point) 30 mins later my mate has a missed call from them, he phones back and offices are closed. 10 mins later they phoned again (this is out of hours) and said "Mr ***** , i wasn't very happy with the whole situation , i have spoken with my manager and am delighted to say he has agreed to reinstate your agreement tomorrow as long as you ring up and pay the £48 arrears and this months payment which becomes due in the next few days" he does all this and its all back on. A month later, he hadn't reinstated his direct debit , so he pays online using their payment portal onvtime. 5 days later he gets a default sums notice- payment not received by DD £18 charge This just raises a few questions for me 1 Can they default him in the first instance for being just 1 payment in arrears? 2 Can they add charges onto the default for £18 admin fees for non payment by DD? 3 Obviously the default was invalid otherwise they wouldn't of panicked and reinstated it, but if the default is on his credit file can we get it removed? 4 Is there a difference between a default sums notice and a default notice? Thanks in advance -

Hi All, Was on here some time ago (7 odd years) and received some incredible help. Sadly 2 years ago i fell into some issues and couldnt work at the time. Thus accumulating some debts. One of them is a credit card with Halifax , approx £5500, that had been passed to Moorcroft. I have sent them a 'prove it' style letter They have replied to me with 1 page which is a personal details page and 1 page which is the signed CCA, from Halifax (photocopies) I am happy to settle this debt but want to know peoples advice, opinions and the best way about it. i do remember a fair bit and have been reading up. Seen the settlement letters, but also conscious the debt seems no longer with Halifax or is do Moorcroft just act on the clients behalf as opposed to buying the debt? I aslso have 4 others than are with Capquest, but rather than making this post complicated, i'll post a new thread. Thanking you all in advance again

Hi All, Was on here some time ago (7 odd years) and received some incredible help. Sadly 2 years ago i fell into some issues and couldnt work at the time. Thus accumulating some debts. One of them is a credit card with Halifax , approx £5500, that had been passed to Moorcroft. I have sent them a 'prove it' style letter They have replied to me with 1 page which is a personal details page and 1 page which is the signed CCA, from Halifax (photocopies) I am happy to settle this debt but want to know peoples advice, opinions and the best way about it. i do remember a fair bit and have been reading up. Seen the settlement letters, but also conscious the debt seems no longer with Halifax or is do Moorcroft just act on the clients behalf as opposed to buying the debt? I aslso have 4 others than are with Capquest, but rather than making this post complicated, i'll post a new thread. Thanking you all in advance again -

Hi All I was hoping for some help with this credit agreement that was sent over from Capquest in reply to my CCA request. It's a shop Direct agreement and to my eyes it appears to have all the ingredients of an enforceable agreement. There is no actual signature but my name and date is printed in the signature line, there are terms and conditions along with a date. The debt will slip off my Credit file on the 27th August 2019. If it is unenforceable I am inclined just to leave it and let it fall off my file in 2 years. However if it is enforceable I would like to be able to prevent Capquest issuing me with a CCJ? Any advice would be appreciated. PS The attachments are in the form of a Zip file, as it wouldn't allow me to directly upload the JPEG. Regards Jonathan Doc 3 Sep 2017, 16-28.pdf

-

Can someone kindly advise how to calculate possible PPI reclaim amount ? I have calculated my monthly PPI interest amount figure using forum details located in which I have already paid over120 months but still have 60 months to expiry. Any assistance would be appreciated as I would like to know a possible figure in order to compare with Welcome's offer if successful.

Can someone kindly advise how to calculate possible PPI reclaim amount ? I have calculated my monthly PPI interest amount figure using forum details located in which I have already paid over120 months but still have 60 months to expiry. Any assistance would be appreciated as I would like to know a possible figure in order to compare with Welcome's offer if successful. -

Today I received a white county courtclaim form from northampton for the MBNA Credit card 2008 – now with PRA GROUP - £2723 – defaulted 2012. On 12th Nov PRA Group wrote to me in response to my returned PAP form where I stated I dispute the debt because I need more documents or information Specifically I wrote: I need a copy of (1) the Default Notice, (2) the Notice of Assignment, (3) a complete set of statements detailing exactly how the debt has accrued detailing: (a) All Transactions, (b) Any additional charges, be them by the original creditor or you PRA Group (UK) Limited, the debt purchaser or any predecessor, © Details of all contractual interest added by whom and on what date, (d) List of ALL Payments made toward the Agreement. The PRA group letter on the 12th said, that in response to my query (PAP form) please find enclosed copy of statement of account from MBNA and a copy of the credit agreement (was an online application 2008) plus statements from the MBNA credit card (virgin). The letter goes on to say that they will put the account on hold for 30 days until 12th December to allow sufficient time to receive the letter and contact them. Today I received the county court claim form. I don't know what to do now? Please advise. Should I try to a negotiate an offer with PRA or will I have to pay in full somehow! I don't want a CCJ registered.

-

I will be concise as this is not a confessional, if helpers need more information I will respond promptly. I am 67 years old and have seven creditors, one with CCJ. I followed the advice of CAG and offered what I could, a token £5 a month to each. These payments were set up and have run without apparent fault for about seven years. Since doing this I was evicted from my home of sixteen years (the reluctant CCJ with a very patient landlord) and had no valid postal address for some time. In 2013 I had to move to Germany for family reasons. My only income is my state pension and a very, very small private pension. In short, absolutely no spare cash as the pension has to cover room rent and everything else. My assets fit into two suitcases and have no value My sister who is in the UK received a letter from Robinson Way addressed to me. She has told them to remove her address from my file as I do not and never have lived at that address. They have agreed to do this. They are talking as if this were a recent matter, insisting on the establishment of a repayment plan. Obviously I have nothing to offer them and their threats of legal action are not particularly concerning. When the CCJ was issued the judge noted that the matter would not be pursued unless there were substantial assets, which is oddly reassuring now. I intend to contact RW by email so that everything is recorded but before I do I wanted to gather any advice from you good folks. Incidental to this, I do not know what my credit record looks like now. I have lost my CRA access details and it seems not to be possible to open a new subscription from Germany. Finally, (because it is stupidly embarrassing) I have noticed an error in Robinson Way's payments. When I agreed to the monthly payment I established a standing order which is still running. I periodically check that all payments are going out as they should. What I did not notice was that RW established a direct debit, with the same reference number in addition to the standing order. So they have been receiving and taking twice the payment I agreed and this seems to have been going on for the whole period.

I will be concise as this is not a confessional, if helpers need more information I will respond promptly. I am 67 years old and have seven creditors, one with CCJ. I followed the advice of CAG and offered what I could, a token £5 a month to each. These payments were set up and have run without apparent fault for about seven years. Since doing this I was evicted from my home of sixteen years (the reluctant CCJ with a very patient landlord) and had no valid postal address for some time. In 2013 I had to move to Germany for family reasons. My only income is my state pension and a very, very small private pension. In short, absolutely no spare cash as the pension has to cover room rent and everything else. My assets fit into two suitcases and have no value My sister who is in the UK received a letter from Robinson Way addressed to me. She has told them to remove her address from my file as I do not and never have lived at that address. They have agreed to do this. They are talking as if this were a recent matter, insisting on the establishment of a repayment plan. Obviously I have nothing to offer them and their threats of legal action are not particularly concerning. When the CCJ was issued the judge noted that the matter would not be pursued unless there were substantial assets, which is oddly reassuring now. I intend to contact RW by email so that everything is recorded but before I do I wanted to gather any advice from you good folks. Incidental to this, I do not know what my credit record looks like now. I have lost my CRA access details and it seems not to be possible to open a new subscription from Germany. Finally, (because it is stupidly embarrassing) I have noticed an error in Robinson Way's payments. When I agreed to the monthly payment I established a standing order which is still running. I periodically check that all payments are going out as they should. What I did not notice was that RW established a direct debit, with the same reference number in addition to the standing order. So they have been receiving and taking twice the payment I agreed and this seems to have been going on for the whole period. -

Hi Everybody, Not sure this is the correct place for this but as I bought the item from Curry's I thought it was the best place. I am after some advice regarding a washer/dryer that is protected by a 12 month Mastercare support agreement. The washer dryer is 8 years old but we have always been protected by Mastercare and they have always fixed the problem throughout the years. However a few weeks ago we had a the common problem of the dryer not getting hot and requested an engineer to come out and clean the condenser. If this was an easy job I would have done it myself, but it is buried at the bottom of the washer dryer and we have been told not to do the job ourself. Anyway, he found a piece of plastic in the pump and claimed this was the problem. We asked him to clean the condenser and he said "no". We were not surprised when the dryer was exactly the same and on the first wash after he left the drum started making a loud noise so we reported both faults. On the second visit (12th November) he said we can still use the washer but we need a new drum. He also ordered a new condenser and said there is no need to clean the condenser as a new one is coming. The day after he ordered the drum and condenser I got a text saying they were out of stock and we would be contacted when they come in. I have used the washer a few times but it is getting nosier and nosier and it really is not washing clothes very well. I rang today for am update and they said there is no expected date for the drum, so i asked if they can send an engineer to fix the condenser, and this is where i need advice... She told me I can not have an engineer because I have already had two visits with the same problem. Despite explaining that neither of them actually bothered to empty the condenser, she was adamant that no visit can be booked and I need to speak to my home insurance company and ask them to fix the problem. I have never heard this rubbish before and doubt it is true but she would not budge. The new condenser is also out of stock and I will have to wait for it to arrive. I am basically without a washer or a dryer, no engineer can be booked and they have no date of when the machine will be fixed. The agreement says "For the life of your support agreement we will carry out as many repairs as your product needs" it makes no mention of two visits only. I can not find on the warranty an explanation of how long they have to fix the problems which is already becoming an inconvenience. Does anybody know what a reasonable time to fix the problems is? I have been offered another 12 month agreement which is due to start next month but do not know if I should take out the cover. I hope I explained my problem properly Kind Regards Jimbo

-

Hello I wonder if you can advise me. My son has had a loan from Money barn. He picked the car up and its been one problem after another with the car. He has phoned moneybarn to tell them, and they say they have opened a case but he should take it up with the garage. It is 14 days on Wednesday so does he still have time to cancel the loan and if he does should he send an email as well as phone them, he wouldnt have time to send a letter would he? Thank you for any help you can give.

-

I attach a copy of a gym membership agreement, can I get out of it or have I just got to pay up please. clacton council leisure centre .pdf

I attach a copy of a gym membership agreement, can I get out of it or have I just got to pay up please. clacton council leisure centre .pdf -

Hi, I am posting this as I require some urgent advice regarding a minor and an agreement. I am 17 years old and I got onto an online car auction and won. The vehicle is for £7,900 + VAT + 20% commission + vat, therefore the total plaice is around £11,300. However I don’t have the money to buy the car and I did not think that I will win the auction. I contacted the auctioneer about this and they said that in there terms and condition (which I agreed to over email) they clearly state the following: 1) if a buyer wants to cancel they must pay the 20% commission+ vat. Which works out at £1580+ Vat 2) it is a trade sale so consumer right do not apply 3) there is a 2% interest each day for late payment 4) if an under 18 bids in a vehicle the parent or legal guardian is liable to pay. 5) is payment is not received within the allotted time they will use legal action. 6) If the reserve price is not met the seller may still sell the vehicle to the highest bidder. I need to cancel the bid as I have not got the money to purchase the vehicle but I don’t even have the enough money to pay for the cancellation charge. The auctioneer have got a copy of my driving licence and are saying that I have till 5pm otherwise they will go to court and most likely I will get a CCJ in my name which will be for the full amount of approx £11,300 plus 2% interest each day. I would like to know if they will still be able to take me to court even if I am under the age of 18 and classed as a minor, and I did not think this would happen. My parents are not aware of the situation and even they do not have that hind of money. Adobe is greatly appreciated. Thanks Thanks in advance.

Hi, I am posting this as I require some urgent advice regarding a minor and an agreement. I am 17 years old and I got onto an online car auction and won. The vehicle is for £7,900 + VAT + 20% commission + vat, therefore the total plaice is around £11,300. However I don’t have the money to buy the car and I did not think that I will win the auction. I contacted the auctioneer about this and they said that in there terms and condition (which I agreed to over email) they clearly state the following: 1) if a buyer wants to cancel they must pay the 20% commission+ vat. Which works out at £1580+ Vat 2) it is a trade sale so consumer right do not apply 3) there is a 2% interest each day for late payment 4) if an under 18 bids in a vehicle the parent or legal guardian is liable to pay. 5) is payment is not received within the allotted time they will use legal action. 6) If the reserve price is not met the seller may still sell the vehicle to the highest bidder. I need to cancel the bid as I have not got the money to purchase the vehicle but I don’t even have the enough money to pay for the cancellation charge. The auctioneer have got a copy of my driving licence and are saying that I have till 5pm otherwise they will go to court and most likely I will get a CCJ in my name which will be for the full amount of approx £11,300 plus 2% interest each day. I would like to know if they will still be able to take me to court even if I am under the age of 18 and classed as a minor, and I did not think this would happen. My parents are not aware of the situation and even they do not have that hind of money. Adobe is greatly appreciated. Thanks Thanks in advance. -

Hello all, I'm in the process of renting a flat through an established letting agent and they are taking a long time to send the tenancy agreement. I have signed a contact with the agency and made the initial payment for the first months rent 15 days ago, and should be moving in soon. Whats the course of action to take to ensure i get something in writing asap, as txt messages and phone calls do not work, it's always "will be with you soon".

Hello all, I'm in the process of renting a flat through an established letting agent and they are taking a long time to send the tenancy agreement. I have signed a contact with the agency and made the initial payment for the first months rent 15 days ago, and should be moving in soon. Whats the course of action to take to ensure i get something in writing asap, as txt messages and phone calls do not work, it's always "will be with you soon". -

Hi all I am new the CAG i would just like to see if anyone could help or give me the best advice on bankruptcy on a personal agreement my partner and i are directors of a LTD company The LTD company had a debt with a supplier (not sure if i can post their name ) the debt was 11938.71 in March this year they sent us a statutory demand / winding up petition which we did not want to happen as thats our monthly income so if they wound the company up me and my partner would have no income to pay the debt off we agreed with their solicitors a payment plan of £500 per month ( under the understanding the winding up petition would still be in place but on hold if we fail to make our payments ) and they would look into it in 6 months time to see if we can pay more off the debt we paid them on time each month and stuck to our word then at the beginning of July the winding up petition went active again we called to see the reason why as we stuck to our word and never missed a payment their reply was they want their money sooner rather than later we have sold the LTD company on but because me and my partner signed a Personal Agreement they are coming after us personally (also the personal agreement does not have my correct D.O.B ) i had a gentleman come out to my house trying to serve me with a bankruptcy petition he has been twice and posted a letter saying he will arrive on such a day at such a time to serve me with the petition he came but i never answered to him he has been out in total of 4 times am not sure whats the best thing to do do i take the petition off him or not ? i am willing to set up a payment plan instead of going bankrupt just do not want the same to happen where i pay them a few months then they try to make me bankrupt again can anyone help please

Hi all I am new the CAG i would just like to see if anyone could help or give me the best advice on bankruptcy on a personal agreement my partner and i are directors of a LTD company The LTD company had a debt with a supplier (not sure if i can post their name ) the debt was 11938.71 in March this year they sent us a statutory demand / winding up petition which we did not want to happen as thats our monthly income so if they wound the company up me and my partner would have no income to pay the debt off we agreed with their solicitors a payment plan of £500 per month ( under the understanding the winding up petition would still be in place but on hold if we fail to make our payments ) and they would look into it in 6 months time to see if we can pay more off the debt we paid them on time each month and stuck to our word then at the beginning of July the winding up petition went active again we called to see the reason why as we stuck to our word and never missed a payment their reply was they want their money sooner rather than later we have sold the LTD company on but because me and my partner signed a Personal Agreement they are coming after us personally (also the personal agreement does not have my correct D.O.B ) i had a gentleman come out to my house trying to serve me with a bankruptcy petition he has been twice and posted a letter saying he will arrive on such a day at such a time to serve me with the petition he came but i never answered to him he has been out in total of 4 times am not sure whats the best thing to do do i take the petition off him or not ? i am willing to set up a payment plan instead of going bankrupt just do not want the same to happen where i pay them a few months then they try to make me bankrupt again can anyone help please -

Hi all, I have no idea if the reconstituted agreement I have received from Link Financial is enforceable. It is a £6k debt with Barclaycard. Please can somebody advise me how to upload this for somebody to check if it is enforceable? Thanks,

Hi all, I have no idea if the reconstituted agreement I have received from Link Financial is enforceable. It is a £6k debt with Barclaycard. Please can somebody advise me how to upload this for somebody to check if it is enforceable? Thanks, -

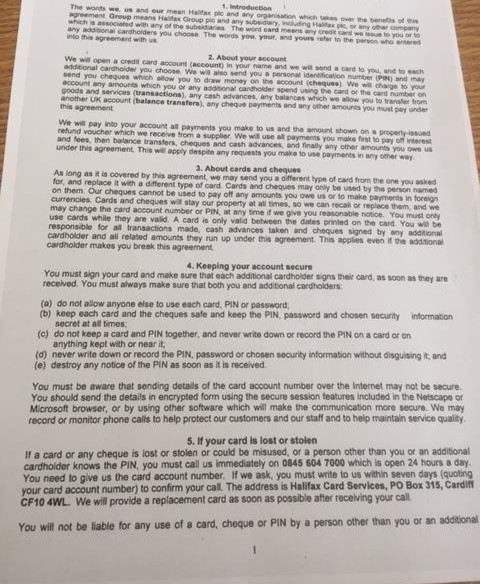

Hi fellow caggers, looking a bit of advice for my partner She opened a Halifax Rewards account in 2002 with her Ex husband They separated in 2011 and there was an OD on the account He sub sequentially left all the debt to her, he managed to remove himself from the account by paying a small amount, I will say he was a Halifax employee. The last payment into the account was feb 13 by my partner and the account was defaulted on her credit report in Dec 13 It was sold onto Hoist and is being managed by Wescot, we have not acknowledged the debt and sent them a prove it in January which they still havent complied with and the account is on hold My partner never received a termination notice and we have sub sequentially SAR'd Halifax and received a mountain of paperwork today. I can upload any thing that you need to see Looking through it there is no reference to a termination notice and have noticed from an initial balance of ~£300 the debt stands at ~£800 which is all charges Can she challenge Halifax to remove the default? Also can she reclaim the charges under BCOBS?

Hi fellow caggers, looking a bit of advice for my partner She opened a Halifax Rewards account in 2002 with her Ex husband They separated in 2011 and there was an OD on the account He sub sequentially left all the debt to her, he managed to remove himself from the account by paying a small amount, I will say he was a Halifax employee. The last payment into the account was feb 13 by my partner and the account was defaulted on her credit report in Dec 13 It was sold onto Hoist and is being managed by Wescot, we have not acknowledged the debt and sent them a prove it in January which they still havent complied with and the account is on hold My partner never received a termination notice and we have sub sequentially SAR'd Halifax and received a mountain of paperwork today. I can upload any thing that you need to see Looking through it there is no reference to a termination notice and have noticed from an initial balance of ~£300 the debt stands at ~£800 which is all charges Can she challenge Halifax to remove the default? Also can she reclaim the charges under BCOBS? -

Hi everyone, I was wondering if anyone could advise on what I should do with regards to the following. Around 12 years ago due to various issues I found myself in debt for about 35K. I went on a DMP which for majority of creditors is still going, paying off regularly the agreed amount. About 4 years ago MBNA stopped taking the payment, I have now discovered that they sold the debt to Arrow Global. Over the past couple of weeks I have received some letters from Shoosmith on behalf of Arrow for the credit card etc. Would anyone be able to advise if I shoudl ask for a CCA on the debt (I genuinely do not know if MBNA was paid in full or not! but I am doubting even my name at the moment panic is back!) . What steps should I take? Any advice is welcome (sorry if the above does not make much sense but after 10 years of paying things back this has brought me back onto "put your head on the sand mode")....

-

I had a loan via satsuma loans (provident financial ltd) I started to find unaffordable. I did the right thing and rather than paying late I contacted them being honest and setup a payment agreement, which I have stuck to 100% and not missed a single payment since it was setup in may 2017. Despite this and the fact ive made major strides to improve my debt handling and credit record over the last 12 months its still had something dragging it down and ive just found out that its provident financial ltd. The record for them on my credit file is still showing as per the original loan agreement which I haven't been paying for almost 12 months now however this is no longer valid as the new payment agreement I had with them superseded this original agreement which explains why I haven't been making payments towards it. I have requested via experian and noodle that satsuma update this record to reflect the new agreement but they have refused to do so. My question is, is this legal? I dont see how when ive setup a payment agreement with a company's approval that the original payment agreement is still valid as surely you cannot have 2 payment agreements with 1 company for 1 loan.. ...the payment agreement I setup surely supersedes the original one? and I dont see how its fair that im being penalised for late payments on a loan agreement I no longer have any agreement to pay. this whole thing has utterly tanked my credit file despite the fact ive worked really hard over the last year to sort myself out and until I find someway to correct it it will keep on tanking my credit file. So just wondering what my options are here? Is there anyway I can force satsuma to update my file to show the new agreement rather then the out of date invalid one? Can I get some advice please?

I had a loan via satsuma loans (provident financial ltd) I started to find unaffordable. I did the right thing and rather than paying late I contacted them being honest and setup a payment agreement, which I have stuck to 100% and not missed a single payment since it was setup in may 2017. Despite this and the fact ive made major strides to improve my debt handling and credit record over the last 12 months its still had something dragging it down and ive just found out that its provident financial ltd. The record for them on my credit file is still showing as per the original loan agreement which I haven't been paying for almost 12 months now however this is no longer valid as the new payment agreement I had with them superseded this original agreement which explains why I haven't been making payments towards it. I have requested via experian and noodle that satsuma update this record to reflect the new agreement but they have refused to do so. My question is, is this legal? I dont see how when ive setup a payment agreement with a company's approval that the original payment agreement is still valid as surely you cannot have 2 payment agreements with 1 company for 1 loan.. ...the payment agreement I setup surely supersedes the original one? and I dont see how its fair that im being penalised for late payments on a loan agreement I no longer have any agreement to pay. this whole thing has utterly tanked my credit file despite the fact ive worked really hard over the last year to sort myself out and until I find someway to correct it it will keep on tanking my credit file. So just wondering what my options are here? Is there anyway I can force satsuma to update my file to show the new agreement rather then the out of date invalid one? Can I get some advice please? -

Hi, hope someone can advise me on this. My letting agent is telling me that at the end of my current contract, they want me to sign a 12 month contract otherwise I will have to leave. I looked on my tenancy agreement and it states the following TWELVE MONTHS beginning 6th july 2017. If the tenant does not leave at the end of the fixed term, the tenancy will continue, still subject to the terms and conditions set out in this agreement, from month to month from the end of the fixed term until either the tenant gives notice that he wishes to end the agreement as set out in clauses 6 and 7 below or the landlord serves on the tenant a notice under section 21 of the housing act 1988, or a new form of agreement is entered into, or this agreement is ended by consent or court order" clause 6 and 7 talk about giving the landlord 1 months notice before I want to leave. Am I within my rights to ask to stay on a monthly rolling contract based on the above? Thanks

Hi, hope someone can advise me on this. My letting agent is telling me that at the end of my current contract, they want me to sign a 12 month contract otherwise I will have to leave. I looked on my tenancy agreement and it states the following TWELVE MONTHS beginning 6th july 2017. If the tenant does not leave at the end of the fixed term, the tenancy will continue, still subject to the terms and conditions set out in this agreement, from month to month from the end of the fixed term until either the tenant gives notice that he wishes to end the agreement as set out in clauses 6 and 7 below or the landlord serves on the tenant a notice under section 21 of the housing act 1988, or a new form of agreement is entered into, or this agreement is ended by consent or court order" clause 6 and 7 talk about giving the landlord 1 months notice before I want to leave. Am I within my rights to ask to stay on a monthly rolling contract based on the above? Thanks -

HMRC calls on online marketplaces to sign agreement tackling VAT fraud READ MORE HERE: https://www.gov.uk/government/news/hmrc-calls-on-online-marketplaces-to-sign-agreement-tackling-vat-fraud

-

Hi there I am guessing this is a common problem. Around 2 years ago, I received a threat from Cabrot regarding an £8k credit card from Halifax taken out in 2000 (I think - may have been 2001). I followed instructions and sent them a letter requesting a copy of the CCA and got the usual BS saying they couldn't find the file but I am still liable for the debt, the last I heard from them was August 2016. Anyhow, out of the blue. Yesterday, I received a letter from our beloved friends stating they had found said documents and they believe these were enforceable to obtain a CCJ. There is no signature on the forms and the page numbers do not correspond properly with corresponding numbers either missing or duplicated (I have copies attached with details blanked out - I can only upload 5 but have another 5 or 6). Additionally, there is no credit limit either, just a note to say that it will be determined and could vary. They do however, have my name & address on the top of the form. Based on this would it be enforceable and accordingly, how should I reply? I had hoped this had been put to bed but sadly not and I'm hoping I am not screwed. Thanks in anticipation. KR

Hi there I am guessing this is a common problem. Around 2 years ago, I received a threat from Cabrot regarding an £8k credit card from Halifax taken out in 2000 (I think - may have been 2001). I followed instructions and sent them a letter requesting a copy of the CCA and got the usual BS saying they couldn't find the file but I am still liable for the debt, the last I heard from them was August 2016. Anyhow, out of the blue. Yesterday, I received a letter from our beloved friends stating they had found said documents and they believe these were enforceable to obtain a CCJ. There is no signature on the forms and the page numbers do not correspond properly with corresponding numbers either missing or duplicated (I have copies attached with details blanked out - I can only upload 5 but have another 5 or 6). Additionally, there is no credit limit either, just a note to say that it will be determined and could vary. They do however, have my name & address on the top of the form. Based on this would it be enforceable and accordingly, how should I reply? I had hoped this had been put to bed but sadly not and I'm hoping I am not screwed. Thanks in anticipation. KR

-

Hi all, ive had a credit agreement back from IDEM servicing re my mbna credit card, please can you take a look over it please, thanks in advance Scan mbna.pdf

-

I am a non-resident parent who has been paying maintenance via the CSA for years. I was aware that my agreement would be ending and fully expected to start a new agreement and continue paying for my non-resident daughter. My question is, as no-one seems to be able to answer it at present, if my agreement with the CSA ended on 13 February why should I have paid a full months worth of money to them in February? My new agreement with CMS starts on 14 February (some valentine lol) so technically I will end up paying twice for the second half of February. Now as this money is for my daughter this wouldn't be a problem but 1 her mum has aways made things difficult for me and 2 when I needed assistance from the CSA many years back they well and truly shafted me. So my thoughts are I want my money back? Is this going to be likely or possible? Thanks, Rich

I am a non-resident parent who has been paying maintenance via the CSA for years. I was aware that my agreement would be ending and fully expected to start a new agreement and continue paying for my non-resident daughter. My question is, as no-one seems to be able to answer it at present, if my agreement with the CSA ended on 13 February why should I have paid a full months worth of money to them in February? My new agreement with CMS starts on 14 February (some valentine lol) so technically I will end up paying twice for the second half of February. Now as this money is for my daughter this wouldn't be a problem but 1 her mum has aways made things difficult for me and 2 when I needed assistance from the CSA many years back they well and truly shafted me. So my thoughts are I want my money back? Is this going to be likely or possible? Thanks, Rich -

Good afternoon I currently have an ongoing complaint which has recently progressed to a complaint being made to the financial-ombudsman. I recently received some letters from bright house regarding a late payment fee which say's on all 3 letters that the date of Agreement being 21-11-2017. Is this the actual day they claim the agreement/contract was made? As One of the items is a Television id took an agreement on in november 2014 and should of been paid of by now but which they claim over £1000 is owing on When challenged about this i stated that we had items 2-3 years after that and told them they would of not allowed us more items if we that far in arrears at which he said he only knows what was written on his pda (called to our home)

Good afternoon I currently have an ongoing complaint which has recently progressed to a complaint being made to the financial-ombudsman. I recently received some letters from bright house regarding a late payment fee which say's on all 3 letters that the date of Agreement being 21-11-2017. Is this the actual day they claim the agreement/contract was made? As One of the items is a Television id took an agreement on in november 2014 and should of been paid of by now but which they claim over £1000 is owing on When challenged about this i stated that we had items 2-3 years after that and told them they would of not allowed us more items if we that far in arrears at which he said he only knows what was written on his pda (called to our home) -

Background 4 years service continuous, rocky employment. Currently working my notice period due to evident constructive dismissal. Despite a grievance being submitted with my resignation no investigation has been commenced and a meeting was held where i was offered a PILON payment to leave that day. How do I approach a settlement agreement proposal with the employer it's an evident breakdown and It will save a lengthy tribunal process

Background 4 years service continuous, rocky employment. Currently working my notice period due to evident constructive dismissal. Despite a grievance being submitted with my resignation no investigation has been commenced and a meeting was held where i was offered a PILON payment to leave that day. How do I approach a settlement agreement proposal with the employer it's an evident breakdown and It will save a lengthy tribunal process

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS