Showing results for tags 'though'.

Found 18 results

-

Over the last 4years I have been receiving letters from N Power at my address, but for the previous occupants. As I used to be an Npower customer I have opened a couple of these thinking they were my bills etc. and have found that the previous owner of my house is getting gas and electricity supplied to another address,but having all correspondence sent to my address still. I have tried contacting Npower dozens of times to stop this and every time they have said it will stop,but it never has. About 18 months ago they offered me £20 credit as compensation/goodwill gesture onto my account for the hassle it has caused. I have now left Npower and changed supplier yet despite their most recent promises I am still receiving mail to my address for this other account. Last night I called Npower again and once again explained the situation. I am now told that as I am not the account holder, that they cannot do anything and that they will keep sending mail to my address. I have explained that I am worried that somebody could be racking a debt up against my address and that if they are, that they could end up sending bailiffs etc. round to my house. Is thereanything I can do, or do I just have to accept that these clowns will continuesending me somebody elses mail.

Over the last 4years I have been receiving letters from N Power at my address, but for the previous occupants. As I used to be an Npower customer I have opened a couple of these thinking they were my bills etc. and have found that the previous owner of my house is getting gas and electricity supplied to another address,but having all correspondence sent to my address still. I have tried contacting Npower dozens of times to stop this and every time they have said it will stop,but it never has. About 18 months ago they offered me £20 credit as compensation/goodwill gesture onto my account for the hassle it has caused. I have now left Npower and changed supplier yet despite their most recent promises I am still receiving mail to my address for this other account. Last night I called Npower again and once again explained the situation. I am now told that as I am not the account holder, that they cannot do anything and that they will keep sending mail to my address. I have explained that I am worried that somebody could be racking a debt up against my address and that if they are, that they could end up sending bailiffs etc. round to my house. Is thereanything I can do, or do I just have to accept that these clowns will continuesending me somebody elses mail. -

Hi, hope someone can advise me on this. My letting agent is telling me that at the end of my current contract, they want me to sign a 12 month contract otherwise I will have to leave. I looked on my tenancy agreement and it states the following TWELVE MONTHS beginning 6th july 2017. If the tenant does not leave at the end of the fixed term, the tenancy will continue, still subject to the terms and conditions set out in this agreement, from month to month from the end of the fixed term until either the tenant gives notice that he wishes to end the agreement as set out in clauses 6 and 7 below or the landlord serves on the tenant a notice under section 21 of the housing act 1988, or a new form of agreement is entered into, or this agreement is ended by consent or court order" clause 6 and 7 talk about giving the landlord 1 months notice before I want to leave. Am I within my rights to ask to stay on a monthly rolling contract based on the above? Thanks

Hi, hope someone can advise me on this. My letting agent is telling me that at the end of my current contract, they want me to sign a 12 month contract otherwise I will have to leave. I looked on my tenancy agreement and it states the following TWELVE MONTHS beginning 6th july 2017. If the tenant does not leave at the end of the fixed term, the tenancy will continue, still subject to the terms and conditions set out in this agreement, from month to month from the end of the fixed term until either the tenant gives notice that he wishes to end the agreement as set out in clauses 6 and 7 below or the landlord serves on the tenant a notice under section 21 of the housing act 1988, or a new form of agreement is entered into, or this agreement is ended by consent or court order" clause 6 and 7 talk about giving the landlord 1 months notice before I want to leave. Am I within my rights to ask to stay on a monthly rolling contract based on the above? Thanks -

I recently found a PCN attached to my windscreen from UKPC even though I was displaying a permit. The PCN stated that I was not displaying a valid permit, although the out of focus pictures taken by them, and displayed on their site, show the permit on my dashboard. I have appealed the PCN and asked that they stop harassing me, as this is the second time I have had a ticket whilst displaying a permit. What I find frustrating is that rather than cancel the first PCN, they simply waited 2 months for it to expire, and my guess is this one will probably go the same way. As this means I have to not only waste my time appealing these PCN's but also have to wait 2 months for a resolution, is there any way I can force them to issue a cancellation in a timely manner and to stop this happening repeatedly? As it stands,this series of events could go on infinitely and I have far better things to do with my time.

I recently found a PCN attached to my windscreen from UKPC even though I was displaying a permit. The PCN stated that I was not displaying a valid permit, although the out of focus pictures taken by them, and displayed on their site, show the permit on my dashboard. I have appealed the PCN and asked that they stop harassing me, as this is the second time I have had a ticket whilst displaying a permit. What I find frustrating is that rather than cancel the first PCN, they simply waited 2 months for it to expire, and my guess is this one will probably go the same way. As this means I have to not only waste my time appealing these PCN's but also have to wait 2 months for a resolution, is there any way I can force them to issue a cancellation in a timely manner and to stop this happening repeatedly? As it stands,this series of events could go on infinitely and I have far better things to do with my time. -

Hi all, I ordered things yesterday online, I selected next day delivery, but when I have just checked now, they aren't estimated to arrive until Friday? Something I ordered today is also due to arrive Friday and not tomorrow. All were prime eligible products. So I jumped onto their webchat, and spoke to someone. Turns out they have suyspended next day delivery until they can catch up from Xmas and get their drivers back. In fact here is a snip from the web chat. "Ojas: I can truly understand your concern however as you must have been aware that we had loads of deliveries on Christmas season so the inventory at our fulfillment centers is revising so they are not getting shipped on the same day as they are placed. This is the reason the next day delivery is extended however please be assured that it will be in its original form once again in 2 to 3 days as all of our carriers are also returning back to work. Me: hmm so it's down to the fact you are behind on deliveries, that's fine as long as you say that Ojas: So please be assured that the prime one day delivery service will be in effect within a couple of days." Isn't this a breach of contract? A warning for anyone else expecting their deliveries they day after they are placed as usual.

Hi all, I ordered things yesterday online, I selected next day delivery, but when I have just checked now, they aren't estimated to arrive until Friday? Something I ordered today is also due to arrive Friday and not tomorrow. All were prime eligible products. So I jumped onto their webchat, and spoke to someone. Turns out they have suyspended next day delivery until they can catch up from Xmas and get their drivers back. In fact here is a snip from the web chat. "Ojas: I can truly understand your concern however as you must have been aware that we had loads of deliveries on Christmas season so the inventory at our fulfillment centers is revising so they are not getting shipped on the same day as they are placed. This is the reason the next day delivery is extended however please be assured that it will be in its original form once again in 2 to 3 days as all of our carriers are also returning back to work. Me: hmm so it's down to the fact you are behind on deliveries, that's fine as long as you say that Ojas: So please be assured that the prime one day delivery service will be in effect within a couple of days." Isn't this a breach of contract? A warning for anyone else expecting their deliveries they day after they are placed as usual. -

Hi, long time no post. asfaiwa my finances were now in a good place. I got a massive shock when I did a credit check on Experian two days ago to discover that a debt originally defaulted by Monument back in 2006 was now showing as a default to Arrow Global. This case was dealt with by the court around 2006 who agreed a payment of £1 a month to Arrow Global who had purchased the debt from Monument, and I set up a standing order for £1 a month. I was also paying £10 a month to Arrow Global for an RBS debt. In July 2015 the £10 a month payments stopped as the RBS debt was paid off. I can find no records of any £1 standing order payments to Arrow Global for the Monument debt since 2010 (as far back as my bank records go.) In November 2015 standing order payments for £1 a month started to Capquest, who had apparently bought the debt from Arrow. The first one was £5, (coincidentally 5 months after July 2015 ie 5 x £1 payments), going down to £1 a month after that. Arrow say they never stopped receiving £1 a month payment from me and that I had been paying by order book. I have no recollection of this at all and have no order book with them, nor any memory of cancelling the standing order to Arrow for £1 a month set up years ago, and no memory of setting up a payment with Capquest for £1 month in November 2015. Arrow then informed me that when they sold the debt to Capquest, I defaulted, and the default date on my credit report dates back to November 2015, long after the original default date with Monument. I didn't understand what was going on (I still don’t) and asked if there was any way the default could be removed. Their representative told me it was against the law for them to remove defaulted entries from CRAs. But the default shouldn't be on there in the first place, should it? It is my understanding that defaults should date only to the date of the default with the original creditor. Is this correct? Now, thinking that the Monument debt had been well and truly dealt with I (mistakenly, shoot me now ) chucked out all my correspondence with Monument a few months ago during a filing session. Ditto Arrow Global and Capquest. (yes I'm an idiot. ) I then rang Capquest who confirmed they started receiving £1 a month from me in November 2015. So why the default? Because, they said, I'd defaulted when they bought the debt from Arrow. Taking them at their word I asked for them to suggest a settlement figure and they took a list of all my incomings and outgoings and said they'd pass on my details back to Arrow for them to see if my settlement figure was acceptable. I suggested £500 on a £2,300 original debt. But once I got off the phone my husband said to me that something was fishy about all this, and that's when after discussing it we realised that the default shouldn't even be showing on my credit file. Both Arrow Global and Capquest were insistent that I'd defaulted when the debt was transferred from Arrow to Capquest. So what do I do? This has caused me untold stress and completely ruined my otherwise squeaky clean credit record. Gutted.

-

Hi All, need some help please. I will list the points below: 1, 2013 - changed supplied to Eon, never got a final bill from Npower (they say they did send it) 2, Never got any bills of any reminds or red letters from them at all. 3, then got a letter from them out of the blue in Oct 2014 saying i owe them for gas/elec and i have to pay before debt collection agencies get involved. 4, i contacted them, and told them about back billing as they were chasing me for something which was 18 months old. 5, then i get letters from DCA, 2015, was told to ignore which i did. 6, small claims court arrives from county court, Jan 2016 7, i dispute it and regarding back billing and I win. 8, not heard anything for until Apr 2017, another DCA called Arvato started calling me to pay. 9, I told them the situation, they put the account on hold, they liased with Npower, then decided to carry on harrassing me. 10, 14th July Npower send a letter telling me i have to pay in full or they will default my file. 11, the amount is £467.35, yet when i log into the account and look back it says I owe £616!!! 12, I have sent an email to Npower to cease chasing me for this. I need to know, what other things can I do to stop this default? n.b. i don't have any paperwork as I won in court, and as it was a year old in jan this year, i binned it all (daft i know) Any help is much appreciated Thanks Paul

Hi All, need some help please. I will list the points below: 1, 2013 - changed supplied to Eon, never got a final bill from Npower (they say they did send it) 2, Never got any bills of any reminds or red letters from them at all. 3, then got a letter from them out of the blue in Oct 2014 saying i owe them for gas/elec and i have to pay before debt collection agencies get involved. 4, i contacted them, and told them about back billing as they were chasing me for something which was 18 months old. 5, then i get letters from DCA, 2015, was told to ignore which i did. 6, small claims court arrives from county court, Jan 2016 7, i dispute it and regarding back billing and I win. 8, not heard anything for until Apr 2017, another DCA called Arvato started calling me to pay. 9, I told them the situation, they put the account on hold, they liased with Npower, then decided to carry on harrassing me. 10, 14th July Npower send a letter telling me i have to pay in full or they will default my file. 11, the amount is £467.35, yet when i log into the account and look back it says I owe £616!!! 12, I have sent an email to Npower to cease chasing me for this. I need to know, what other things can I do to stop this default? n.b. i don't have any paperwork as I won in court, and as it was a year old in jan this year, i binned it all (daft i know) Any help is much appreciated Thanks Paul -

Can anyone help me on how to proceed with the following Recieved county court claim today from mortimer clark solicitors acting on behalf of claiment cabot particulars of claim by an agreement between goldfish bank ltd and the defendant on or around 25/11/2002(the agreement) goldfish bank ltd agreed to issue the defendant with a credit card.the defendant failed to make the minimium payments due and the agreement was terminated.the agreement was assigned to the claiment. The claiment therefore claims £XXXX I have a letter dated april 2008 stating cabot have bought the debt and that the agreed monthly repayment plan with goldfish bank now needs to be maintained with cabot. I have kept up the plan and have never missed a payment. I dont understand why they are now taking me to court can some one please advise how to proceed Thanks

Can anyone help me on how to proceed with the following Recieved county court claim today from mortimer clark solicitors acting on behalf of claiment cabot particulars of claim by an agreement between goldfish bank ltd and the defendant on or around 25/11/2002(the agreement) goldfish bank ltd agreed to issue the defendant with a credit card.the defendant failed to make the minimium payments due and the agreement was terminated.the agreement was assigned to the claiment. The claiment therefore claims £XXXX I have a letter dated april 2008 stating cabot have bought the debt and that the agreed monthly repayment plan with goldfish bank now needs to be maintained with cabot. I have kept up the plan and have never missed a payment. I dont understand why they are now taking me to court can some one please advise how to proceed Thanks -

Hi I've attached a PDF with information about the ticket received, not much information on it as I've not received a NTK as yet, but before I waste everyone's time I wanted to ask if I should even be contesting the charge. In a nutshell, parked and bought my hour's ticket, car park was pretty much empty, my ticket was until 4.40pm, parking charge issued at 4.51pm and I got back to my car at 4.52pm, so bottom line is I was in the wrong, however I think being charged £60 rising to £100 is a bit much seeing as the car park was practically empty and I wasn't hours and hours late. In my mind the company has not lost £100 by me being a few minutes late to an empty car park. If the general consensus is that I should suck it up and pay, then I will, but if you think it's worth contesting, I'd be really grateful of advice as to how to go about it. For windscreen tickets (NTD) please answer the following questions. 1 The date of infringement? 08/02/17 2 Did you appeal to the parking company? Not yet If yes, has there been any response? If no, have you received a Notice To Keeper? (NTK) Did the NTK provide photographic evidence? No NTK received as yet 3 Did the NTK mention Schedule 4 of the Protection of Freedoms Act 2012 (PoFA) 4 If you appealed after receiving the NTK, did the parking company give you any information regarding the further appeals process? [it is well known that parking companies will reject any appeal whatever the circumstances] 5 Who is the parking company? UK Parking Control Ltd thanks WeldersWife Parking.pdf

Hi I've attached a PDF with information about the ticket received, not much information on it as I've not received a NTK as yet, but before I waste everyone's time I wanted to ask if I should even be contesting the charge. In a nutshell, parked and bought my hour's ticket, car park was pretty much empty, my ticket was until 4.40pm, parking charge issued at 4.51pm and I got back to my car at 4.52pm, so bottom line is I was in the wrong, however I think being charged £60 rising to £100 is a bit much seeing as the car park was practically empty and I wasn't hours and hours late. In my mind the company has not lost £100 by me being a few minutes late to an empty car park. If the general consensus is that I should suck it up and pay, then I will, but if you think it's worth contesting, I'd be really grateful of advice as to how to go about it. For windscreen tickets (NTD) please answer the following questions. 1 The date of infringement? 08/02/17 2 Did you appeal to the parking company? Not yet If yes, has there been any response? If no, have you received a Notice To Keeper? (NTK) Did the NTK provide photographic evidence? No NTK received as yet 3 Did the NTK mention Schedule 4 of the Protection of Freedoms Act 2012 (PoFA) 4 If you appealed after receiving the NTK, did the parking company give you any information regarding the further appeals process? [it is well known that parking companies will reject any appeal whatever the circumstances] 5 Who is the parking company? UK Parking Control Ltd thanks WeldersWife Parking.pdf -

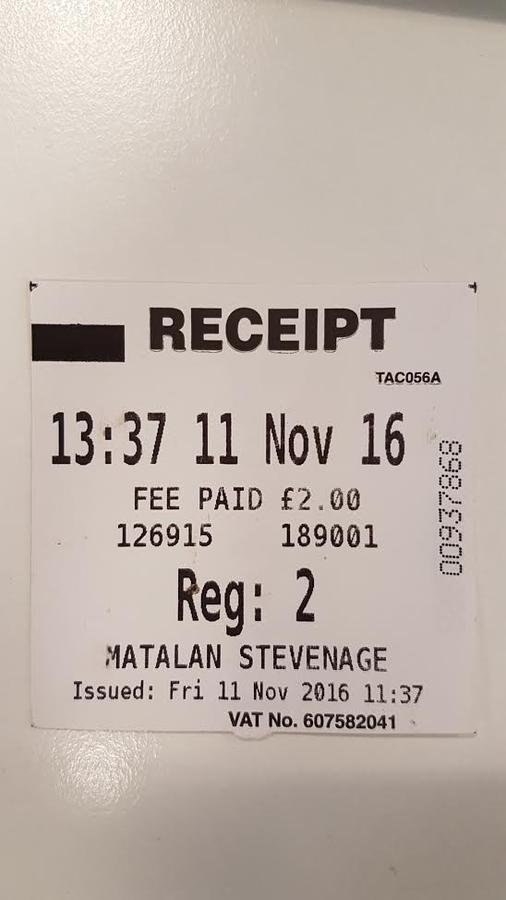

On the 11th November I have parked my car at the Matalan Stevenage car park serviced by Smart Parking. I didn’t have any chance on me so I went into the store to get a £10 note changed. After about 7 minutes from entering the car park I have purchased a parking ticket. I never remember my car registration number and so was glad to have parked near the machine so I could type in the reg number while looking at it on my car . The ticket came out (together with the refund voucher) and I placed it in a visible place in my car and went shopping in town. I never checked if the ticket was printed correctly assuming it would be. I have this ticket still and can see that in fact all the machine printed was the number “2” instead my full registration number. I just didn’t notice that when collecting this ticket. On the 23rd November I have received Parking Charge Notice for £50 for not paying for my parking. I have made an online appeal on the same day explaining the above situation . On the 10th December I received another letter from Smart Parking rejecting my appeal and asking me to pay the charge I would really like to find out what can I do next as I believe I was charged unfairly - I have made my payment and have my ticket to prove this. My only mistake was not checking if the car registration number is actually printed on the ticket that came out. Please help

On the 11th November I have parked my car at the Matalan Stevenage car park serviced by Smart Parking. I didn’t have any chance on me so I went into the store to get a £10 note changed. After about 7 minutes from entering the car park I have purchased a parking ticket. I never remember my car registration number and so was glad to have parked near the machine so I could type in the reg number while looking at it on my car . The ticket came out (together with the refund voucher) and I placed it in a visible place in my car and went shopping in town. I never checked if the ticket was printed correctly assuming it would be. I have this ticket still and can see that in fact all the machine printed was the number “2” instead my full registration number. I just didn’t notice that when collecting this ticket. On the 23rd November I have received Parking Charge Notice for £50 for not paying for my parking. I have made an online appeal on the same day explaining the above situation . On the 10th December I received another letter from Smart Parking rejecting my appeal and asking me to pay the charge I would really like to find out what can I do next as I believe I was charged unfairly - I have made my payment and have my ticket to prove this. My only mistake was not checking if the car registration number is actually printed on the ticket that came out. Please help

-

I qualified to become a driving intructor in 2012 and in Oct 2015 I gave my ADI badge back to the Driving Standards Agency (DSA) as I was no longer teaching due to being in a full time job. The DSA sent me a letter to confirm they received my ADI badge in Oct 2015 also confirmed they removed my name off the Driving Instructors Register. The DSA said in a letter I had ..."12 months from the date your name was removed from the ADI register on 30th Oct2015 to re-register without taking the driving instructor qualifying exams..." So in late Oct 2016 a few days before the 12 months was coming up, I sent in my application to the DSA to re-register, along with my card details for payment of £300. I also did a CRB check a few months before, which was required. The DSA received my application on the 27th Oct (The 12 months deadline was on the 30th, so they received it with 3 days left) I heard nothing for 2 weeks, then I received my application form back (stamped received 27th Oct 2016) and a letter saying my application was unfortunately being rejected because I had not made payment in the last 12 months (I was not teaching in the last 12 months - I had given my badge back and was off the register) as mentioned above. I called the DSA and was told I did not make payment within the 12 months deadline of wanting to re-register with my application form - I explained I sent my application within the 12 months deadline and my card details were on the form. I also explained I had a letter from the DSA from Oct 2015 telling me I had 12 months to re-apply from the date my name was removed off the register. I was told the ADI department was looking for my letter from Oct 2015 and would email me (which they did not) The next day I rang again and this time I again explained - I sent my application within the 12 months time period and wrote my card details on the application form. That my application was returned back to me stamped 'received 27th Oct 2106' - within the 12 month deadline. I was bluntly told my application was being rejected (even though I applied within the 12month period to re-register) because according to the the DSA 1. The DSA needed the 3 digit security number on the back of my card to take payment and they supposedly tried to ring me several times and my number was not working (I explained my number was working all the time and to ring me back to confirm it was working, but the person on the line said no). I explained I received no missed calls. 2. They said they sent me emails as well which I did not have in my inbox I was told bluntly I had to re-apply from scratch and do all the 3 driving instructor tests again and to re-qualify!! - I was feeling very angry because I did nothing wrong in my application and sent it in within 12 months. The DSA received my application on the 23rd Oct and the letter they sent me to say it was being rejected, was dated the 24th Oct, but it was sent out to me a via recorded delivery a whole 12 days later on the 4th Dec 2016 (why was my letter dated 24th Oct 2016 and then sent out to me on the 4th Dec 2016??) they wasted 12 days on purpose to send me the letter. The DSA received my application on 23rd Oct 2016, why did they not send me a letter telling me they needed the 3 digit security number from my card or why did they not send me a text message. The DSA received my application within 12 months and they should have sent me a letter to request my card details, if according to them my phone number was not working (which is a lie) I want to appeal the DSA decision on the basis of 1. I sent my application within 12 months of the deadline to re-register. 2. I need dates/times of the when the DSA called me and according to them my phone was not working (a down right lie) so I can get confirmation from my phone network provider to confirm my phone was working and they was no problem with the phone network - which would break the DSA false argument. 3. Why did not the DSA send me a letter to request the security number or try sending me a text message. 4. The DSA received my letter on the 27th Oct, (application form shows "received 27th Oct) - 3 days before the 12 month deadline. 5. Why did the DSA produce the rejection letter on the 24th Oct and take a whole 12 days to send it out to me on the 4th Dec via recorded delivery - they on purpose took 12 days to delay it being sent to me, so they could say I did not appeal within 14 days!! - thats how sneaky they are!! Please can you help me draft up a letter I need to send the DSA tommorow please

I qualified to become a driving intructor in 2012 and in Oct 2015 I gave my ADI badge back to the Driving Standards Agency (DSA) as I was no longer teaching due to being in a full time job. The DSA sent me a letter to confirm they received my ADI badge in Oct 2015 also confirmed they removed my name off the Driving Instructors Register. The DSA said in a letter I had ..."12 months from the date your name was removed from the ADI register on 30th Oct2015 to re-register without taking the driving instructor qualifying exams..." So in late Oct 2016 a few days before the 12 months was coming up, I sent in my application to the DSA to re-register, along with my card details for payment of £300. I also did a CRB check a few months before, which was required. The DSA received my application on the 27th Oct (The 12 months deadline was on the 30th, so they received it with 3 days left) I heard nothing for 2 weeks, then I received my application form back (stamped received 27th Oct 2016) and a letter saying my application was unfortunately being rejected because I had not made payment in the last 12 months (I was not teaching in the last 12 months - I had given my badge back and was off the register) as mentioned above. I called the DSA and was told I did not make payment within the 12 months deadline of wanting to re-register with my application form - I explained I sent my application within the 12 months deadline and my card details were on the form. I also explained I had a letter from the DSA from Oct 2015 telling me I had 12 months to re-apply from the date my name was removed off the register. I was told the ADI department was looking for my letter from Oct 2015 and would email me (which they did not) The next day I rang again and this time I again explained - I sent my application within the 12 months time period and wrote my card details on the application form. That my application was returned back to me stamped 'received 27th Oct 2106' - within the 12 month deadline. I was bluntly told my application was being rejected (even though I applied within the 12month period to re-register) because according to the the DSA 1. The DSA needed the 3 digit security number on the back of my card to take payment and they supposedly tried to ring me several times and my number was not working (I explained my number was working all the time and to ring me back to confirm it was working, but the person on the line said no). I explained I received no missed calls. 2. They said they sent me emails as well which I did not have in my inbox I was told bluntly I had to re-apply from scratch and do all the 3 driving instructor tests again and to re-qualify!! - I was feeling very angry because I did nothing wrong in my application and sent it in within 12 months. The DSA received my application on the 23rd Oct and the letter they sent me to say it was being rejected, was dated the 24th Oct, but it was sent out to me a via recorded delivery a whole 12 days later on the 4th Dec 2016 (why was my letter dated 24th Oct 2016 and then sent out to me on the 4th Dec 2016??) they wasted 12 days on purpose to send me the letter. The DSA received my application on 23rd Oct 2016, why did they not send me a letter telling me they needed the 3 digit security number from my card or why did they not send me a text message. The DSA received my application within 12 months and they should have sent me a letter to request my card details, if according to them my phone number was not working (which is a lie) I want to appeal the DSA decision on the basis of 1. I sent my application within 12 months of the deadline to re-register. 2. I need dates/times of the when the DSA called me and according to them my phone was not working (a down right lie) so I can get confirmation from my phone network provider to confirm my phone was working and they was no problem with the phone network - which would break the DSA false argument. 3. Why did not the DSA send me a letter to request the security number or try sending me a text message. 4. The DSA received my letter on the 27th Oct, (application form shows "received 27th Oct) - 3 days before the 12 month deadline. 5. Why did the DSA produce the rejection letter on the 24th Oct and take a whole 12 days to send it out to me on the 4th Dec via recorded delivery - they on purpose took 12 days to delay it being sent to me, so they could say I did not appeal within 14 days!! - thats how sneaky they are!! Please can you help me draft up a letter I need to send the DSA tommorow please -

Hi all I've started a complaint with Santander about my mis-sold MPPI. We were FTB's in April 2009 and being the cautious person I am asked the IFA doing our mortgage about Income Protection. Low and behold we ended up with MPPI the only covered the mortgage payment and the house insurance not a penny more up to the value of £750, not what we asked for. However I did not pick on this at the time and it only came to light recently while sorting though some old paperwork and came across the policy document. This is where I finally read the small print properly. I've sent back the MPPI questionnaire to Santander only to be told my claim is with the IFA not them as they didn't sell the original policy. ( They took all the payments for 2 years though ). The IFA is no longer trading which they informed me in the letter and have suggested that I may have a claim through the Compensation Scheme. I think I'm being fobbed off. Any help as to how to proceed would be great. I have the original policy letter from them and all bank statements showing payments etc. Regards Ed

-

I currently work as a Deputy Manager (one of 300) for one of the big four supermarkets, and they have recently announced a new contract change that comes into force on Monday 18th April. In effect we are being demoted to a lesser position, that being of a duty manager. They argue that our job role is not really changing as we will still be doing the same job we have always done and they will not be reducing our pay. However it is a HUGE drop in status as our current contract states we are 'autonomous decisions makers' which classes us as senior business leaders and opts us out of working time regulations. On our new contract we are not classed as this and we are therefore opted in to working time regulations. In addition we also recieve free fuel and a car allowance which will also be taken off us although they have given us over a years notice before they take this away. However this is in our current contract that this can be removed at any time so do not think that we can argue the point much there. The main issue is as Deputy Store Manager you are above all the other senior managers in the shop and now will be dropping to the same level as them so surely this counts as a drop in status, even though my salary will not be affected. It also effectively puts my career back 10 years as I was doing that job 10 years ago! There have been various 1-2-1 meetings held with the outcome already decided, however I asked questions weeks ago which have still not been answered and I also have not got a copy of my new contract as yet. From what I have read online if i work on Monday then I am effectively accepting the new contract and will have no means to put a claim in, in the future. Do I have a case for constructive dismissal?? Please help!! Thanks in advance

I currently work as a Deputy Manager (one of 300) for one of the big four supermarkets, and they have recently announced a new contract change that comes into force on Monday 18th April. In effect we are being demoted to a lesser position, that being of a duty manager. They argue that our job role is not really changing as we will still be doing the same job we have always done and they will not be reducing our pay. However it is a HUGE drop in status as our current contract states we are 'autonomous decisions makers' which classes us as senior business leaders and opts us out of working time regulations. On our new contract we are not classed as this and we are therefore opted in to working time regulations. In addition we also recieve free fuel and a car allowance which will also be taken off us although they have given us over a years notice before they take this away. However this is in our current contract that this can be removed at any time so do not think that we can argue the point much there. The main issue is as Deputy Store Manager you are above all the other senior managers in the shop and now will be dropping to the same level as them so surely this counts as a drop in status, even though my salary will not be affected. It also effectively puts my career back 10 years as I was doing that job 10 years ago! There have been various 1-2-1 meetings held with the outcome already decided, however I asked questions weeks ago which have still not been answered and I also have not got a copy of my new contract as yet. From what I have read online if i work on Monday then I am effectively accepting the new contract and will have no means to put a claim in, in the future. Do I have a case for constructive dismissal?? Please help!! Thanks in advance -

The iron is a Breville 2400W Digital iron. This morning, like every Monday, I was heating up the iron (2/5th setting) like normal. I put my trousers on the board and then as soon as the iron touched the nylon trousers, it stuck to it and burnt a hole in them. They were my only decent pair, and fairly new which were £40 from Debenhams. I've done this many times before without any issues, it just looks like now that the iron heated up much more than it should have. I could prove this too with an infrared heat sensor. http://imglnk.uk/img?i=yepJVY http://imglnk.uk/img?i=BYuVIZ Even the ironing board cover melted slightly. What shall I do about this?

-

Hi everyone I got issued a penalty fare on a bus even though I touched in with my oyster card, because the oyster card is very old and does not always work so the ticket inspectors couldn't read it on their things. However I definitely remember it responded when I touched in on the bus (the green light and the beep, etc), it just didnt work when the inspecters tried to read it. I appealed on the website and they asked me to send them the card number and a 'details/usage statement'. Problem is its such an old battered card that its impossible to read the card number. I don't know how to get a usage statement, or if thats even possible without the card number? The card works very occasionally albeit less and less frequently, so IF I did manage to get it to respond on a machine would there be a way of finding the number? Also surely TFL will have a record on the data from the bus that day? The CCTV would show me touching in, if it still exists (the incident was at the end of August). I'm not sure what to do so please give some advice Thanks

Hi everyone I got issued a penalty fare on a bus even though I touched in with my oyster card, because the oyster card is very old and does not always work so the ticket inspectors couldn't read it on their things. However I definitely remember it responded when I touched in on the bus (the green light and the beep, etc), it just didnt work when the inspecters tried to read it. I appealed on the website and they asked me to send them the card number and a 'details/usage statement'. Problem is its such an old battered card that its impossible to read the card number. I don't know how to get a usage statement, or if thats even possible without the card number? The card works very occasionally albeit less and less frequently, so IF I did manage to get it to respond on a machine would there be a way of finding the number? Also surely TFL will have a record on the data from the bus that day? The CCTV would show me touching in, if it still exists (the incident was at the end of August). I'm not sure what to do so please give some advice Thanks -

I took a free trial of 30 days from CheckMyFile.Com on the 29th July 15 & Cancelled on 28th August 15 the 30th Day. on the 1st Sept they charged my account £8.99 making it go overdrawn, i noticed the next day & called them I explained that i cancelled on the 28th and my account is now overdrawn for which i will be charged i demanded a refund & the charges that i will incur, they agreed to refund the £8.99 but not the bank charges. They claim that i cancelled outside the 30 day period and refuse the accept liability for the charges. My question is are they right & as anyone else suffered a similar experience

I took a free trial of 30 days from CheckMyFile.Com on the 29th July 15 & Cancelled on 28th August 15 the 30th Day. on the 1st Sept they charged my account £8.99 making it go overdrawn, i noticed the next day & called them I explained that i cancelled on the 28th and my account is now overdrawn for which i will be charged i demanded a refund & the charges that i will incur, they agreed to refund the £8.99 but not the bank charges. They claim that i cancelled outside the 30 day period and refuse the accept liability for the charges. My question is are they right & as anyone else suffered a similar experience -

I requested my credit file from Experian and it states I am not on the electoral roll: "No Electoral Roll Information available from the addresses provided". I registered to be on the Electoral Roll a few months ago. This was confirmed to me by my local authority and I also received a voting card for the last general election. Therefore this has shocked me. I have been applying for bank current accounts over the last few weeks and, disappointingly, been rejected by all of them. I am already in a weaker position than most people as I have a non UK passport, not even an EU one, and mine is from a country which many financial institutions classify as a 'high risk' one. And then to also mark me as not being on the electoral roll would be another negative when banks check my credit record. I had some questions please: - if Experian say I'm not on the electoral roll, is it likely the two other credit reference agencies will state the same thing as well? - what could have gone wrong? - how long does it normally take for the records of the credit reference agencies to be updated about somebody being on a local authority's database? - how may I get this rectified please? How long does it take for the credit records to be corrected? - last, but not least, is it worth me applying to more banks? Or should I wait until the records are updated, even if it takes many weeks? How fussy are banks about somebody being on the electoral roll please? Thanks a lot in advance for the advice.

I requested my credit file from Experian and it states I am not on the electoral roll: "No Electoral Roll Information available from the addresses provided". I registered to be on the Electoral Roll a few months ago. This was confirmed to me by my local authority and I also received a voting card for the last general election. Therefore this has shocked me. I have been applying for bank current accounts over the last few weeks and, disappointingly, been rejected by all of them. I am already in a weaker position than most people as I have a non UK passport, not even an EU one, and mine is from a country which many financial institutions classify as a 'high risk' one. And then to also mark me as not being on the electoral roll would be another negative when banks check my credit record. I had some questions please: - if Experian say I'm not on the electoral roll, is it likely the two other credit reference agencies will state the same thing as well? - what could have gone wrong? - how long does it normally take for the records of the credit reference agencies to be updated about somebody being on a local authority's database? - how may I get this rectified please? How long does it take for the credit records to be corrected? - last, but not least, is it worth me applying to more banks? Or should I wait until the records are updated, even if it takes many weeks? How fussy are banks about somebody being on the electoral roll please? Thanks a lot in advance for the advice. -

Hi. I am currently going through with a DRO (debt relief order) and it's taking longer than I would wish, plus the guy from Citz Advice is not really helping at all. I get back tonight and 2 letters. One is from Collectica, saying I now owe them £215, £140 of the remainder of the fine and £75 for their BS fees. I have been paying this weekly, missed a week here and there but generally up to date, it was for a motor fine with courts. This is not in the DRO as fines can not go in dro. However the 2nd letter is off CCS Collect. Saying I owe upto £300 for variou HMRC stuff. This fine is in DRO. They have 'threatened' with action if I do not pay them etc. They say 'our clent hmrc has authed us to recover full amount due. we regret that if no payment in 7 days or an offer to pay etc we will advice cliebnt to litigate amount due with court costs and court fees. This is in the DRO so what's going on? Can anyone shed light on these 2? I have been working in the library on new business ideas all day and the last thing I want to come home to is this ****!

Hi. I am currently going through with a DRO (debt relief order) and it's taking longer than I would wish, plus the guy from Citz Advice is not really helping at all. I get back tonight and 2 letters. One is from Collectica, saying I now owe them £215, £140 of the remainder of the fine and £75 for their BS fees. I have been paying this weekly, missed a week here and there but generally up to date, it was for a motor fine with courts. This is not in the DRO as fines can not go in dro. However the 2nd letter is off CCS Collect. Saying I owe upto £300 for variou HMRC stuff. This fine is in DRO. They have 'threatened' with action if I do not pay them etc. They say 'our clent hmrc has authed us to recover full amount due. we regret that if no payment in 7 days or an offer to pay etc we will advice cliebnt to litigate amount due with court costs and court fees. This is in the DRO so what's going on? Can anyone shed light on these 2? I have been working in the library on new business ideas all day and the last thing I want to come home to is this ****! -

Hi all, Defaulted on a Direct Line loan some years ago and after dealing with CCCS, I have been paying off a manageable amount back. Direct Line put a charging order on my house to secure the debt, should I choose to ever sell my house. After many years of paying monthly via CCCS and the debt being sold on at least twice, if not three times, I am now contemplating selling my house. My question is this, if I now sell my house, will the solicitors just pay the charging order for the outstanding money to Direct Line regardless or will the fact that the debt has been sold on, now mean that they cannot pay it to Direct Line and nor can they give it to the company that bought the debt as the charging order is not in their name ?

Hi all, Defaulted on a Direct Line loan some years ago and after dealing with CCCS, I have been paying off a manageable amount back. Direct Line put a charging order on my house to secure the debt, should I choose to ever sell my house. After many years of paying monthly via CCCS and the debt being sold on at least twice, if not three times, I am now contemplating selling my house. My question is this, if I now sell my house, will the solicitors just pay the charging order for the outstanding money to Direct Line regardless or will the fact that the debt has been sold on, now mean that they cannot pay it to Direct Line and nor can they give it to the company that bought the debt as the charging order is not in their name ?

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS