Showing results for tags 'fraud'.

-

Did you know Lloyds Banking Group (LBG) has a Fraud & Frequent Complainers Team? If you make one too many complaints to LBG, they will refer any and all future complaints to this team to complaint manage! I have recently had cause to complain to LBG about a number of issues (e.g. not putting service first and not being treated as a customer fairly). Having contacted LBG to find out about the progress of my complaint, I was informed by one of their Customer Service Advisors (CSAs) that my complaint was taking longer than normal, to be allocated to a complaint manager. When I enquired as to why it was taking longer than normal, the CSA advised me it was because my complaint had been reallocated to one of their specialist teams. I asked for some clarity around what that meant and also what specialist team, they were referring too. The CSA then advised me that my complaint had been passed to the PCA Fraud & Frequent Complainers Team. I have seen internal documentation, which shows LBG refer to this team as the “F&F Team”. So for clarity, if you make several complaints to LBG, at some stage they will stop dealing with your complaint as a normal everyday customer, and start allocating your complaints to one of a small team of Case Complaint Managers, within this “F&F Team. To give you some sort of indication on the possible trigger point for this “specialist team” I have probably put in about 9 complaints over a 20 year banking history with them, so I assume the referral threshold for allocation, to the “F&F Team”, isn’t that high! As a result of this experience, my impression is that LBG must have an automatic flag marker system in place. I would be really interested to know what their policy is on this and whether the processing of this data is manual or automatic. On a separate note, one of the Data Subject Access Team’s CSAs, has recently advised me that LBG customers can now submit SARs online. This is done via an Online DSAR Form. https://apply.lloydsbank.co.uk/personal/a/gforms?formId=F010&prodType=GN PROs You do not have to pay the £10 statutory fee, it’s free! I have used this new service twice and it is much quicker in comparison to the conventional route of submission (i.e. recorded delivery directly to the DSAR Team or via your local branch in person). CONs Once you complete the Online DSAR Form, it moves to the next screen and tells you that you have successfully submitted the Form. However, it doesn’t give you a URN to prove this, and it doesn’t send you a copy of the Form to your email address. You then literally have to wait for the DSAR Team at LBG to write to you and acknowledge receipt of your DSAR. I am not saying this is the best thing since slice bread, but certainly another option for us consumers! They don’t advertise this new SAR submission route, and even there CSAs aren’t aware of it.

-

I got spoofed out of £1,000 by these fraudsters and the bank have refused to give me my money back. I was stupid enough to fill in the form on line and then I found it strange called bank to stop cards and they said it was online Sc@m. They said they would watch my account, not to worry, and issued new card and pin. 3 days later my cards came and i got a call from "the bank" but it was the sc@mmers. (They had my number from the online form I filled out for the fake refund). They said they would send me a code to my phone and to confirm the code for security reasons. I gave them the code and they started talking to me about what had happened and said someone tried to take £500 out my account but they blocked it and was calling to make sure it was not me. During this time, they downloaded the bank app onto their phone and using the code, transferred online 3 transactions totalling £994. After the call, I checked my account and noted then called the bank who stopped the account but could not stop the transactions. After an investigation they said because I gave this code to them I am liable. I have complained and they said I won't get my money back. I want to know if this is right. They knew this fraud was happening but did nothing to warn me and had a duty of care to watch out for me and protect my money. I did not authorise these transactions, even though they had the code to download the app, the actual authorisation and transfers were not done by me. I have been sick and unwell because of this and wondered if there was anything I can do because the bank should have done more to protect me and the transactions were not authorised.

I got spoofed out of £1,000 by these fraudsters and the bank have refused to give me my money back. I was stupid enough to fill in the form on line and then I found it strange called bank to stop cards and they said it was online Sc@m. They said they would watch my account, not to worry, and issued new card and pin. 3 days later my cards came and i got a call from "the bank" but it was the sc@mmers. (They had my number from the online form I filled out for the fake refund). They said they would send me a code to my phone and to confirm the code for security reasons. I gave them the code and they started talking to me about what had happened and said someone tried to take £500 out my account but they blocked it and was calling to make sure it was not me. During this time, they downloaded the bank app onto their phone and using the code, transferred online 3 transactions totalling £994. After the call, I checked my account and noted then called the bank who stopped the account but could not stop the transactions. After an investigation they said because I gave this code to them I am liable. I have complained and they said I won't get my money back. I want to know if this is right. They knew this fraud was happening but did nothing to warn me and had a duty of care to watch out for me and protect my money. I did not authorise these transactions, even though they had the code to download the app, the actual authorisation and transfers were not done by me. I have been sick and unwell because of this and wondered if there was anything I can do because the bank should have done more to protect me and the transactions were not authorised. -

I took a telephone contract out in 2015 and had issues with the provider from the onset and entered into a dispute which lasted several years before finally taking my case to the ombudsman which I won and the provider was deemed to have mis-sold the contract. All adverse on my credit file was wiped clean. The provider also accused me of face to face category six fraud and entered my details onto the National Fraud Database which has caused me untold grief and countless sleepless nights amongst other hardships. This is not dealt with by the Ombudsman services and was made clear by the Ombudsman that this is a criminal offence/accusation outside their jurisdiction. I believe that I can now take legal action for false accusations of fraud as this has not been included in the Ombudsman rulings and the contract that I was accused of fraudulent activity on has now been deemed mis-sold and void. Does anyone have any views or experience on this type of case and is it the type of case that should take the small claims court route or maybe high court. Constructive comments would be most appreciated.

-

I am so stressed at the moment because Barclays have pulled a real good'un from their bag if crap. An old customer accidentally sent us £6000 by bank transfer on Wednesday morning, rang us up to explain and asked if we could get it back to him. Stupid us rang Barclays and told them what had happened and to return it back to the account it came from because it wasn't our money. After an hour on the phone, a reversal was done on the payment. Next morning, another £6000 gets removed out of the account. No warning, nothing. Several long calls to call centres abroad (around 4hrs worth) and it may be that the fraud department has pulled the funds and investigating. They've said it will take 10 days. We've got bills to pay and none of this is our fault. All we did was tell Barclays to put the original £6k back where it came from. Have we been caught up in some weird [problem] where the guy who transferred the funds gets his money back twice or are Barclays incompetent. We raised the issue, we are getting penalised. No wonder people keep their mouths shut when unexpected money lands in their account!

-

Hey,I met the same situation as you. How are you doing now? can you contact me? if you read the comment. sorry you cant post phone numbers on CAG we are anon.

-

Is there any organisation that investigates Motability for aiding and abetting Motability fraud?

-

Hello all, My sister in law received what she thought was a message from her friend asking her to accept some money from her Paypal account and transfer it down into her bank then transfer it to her friend’s bank. She received two payments from two different sources, downloaded £500 and duly transferred it to her “friend’s” bank account. Turned out that the message she received was from a fraudster and the money she received was from two hacked PayPal accounts and the bank account she sent the money to was not her friend’s account. I know she should have questioned why her friend did not download the money herself, she should also have questioned why the money came from two unknown paypal accounts and maybe also double checked where she was sending it. All good things to have done but she is a busy working mum and acted in good faith and was victim to a fairly smart fraud. Paypal is now wanting the money back and has set Debt Collectors onto her. Has she got any defence against Paypal?

-

A description of the issue : I am an oversea student in Manchester. original student additions:1790 pounds. original every saver:18680 pounds. accommodation installment is 1793 pounds. After paying my accommodation installment on 22/01/2019, all my money in my both account has been deducted on 23/01/2019. It shows "to reconcile" with reference: "fraud prevent GIA ADV". I reported it to the nearest Barclay branch on 23/01/2019. a staff told me that someone will contact me but until now(02/02/2019) no one has contacted me. I am very sad and afraid because on 08/02/2019 I will pay my tuition installment but now I really have no money at all and I don't know what I should do next.

-

Good afternoon all I have taken a very vital case against Lloyds and this time it will be us (consumers) who are in a stronger position than the Bank. I have taken them to court and despite the fact that they have tried everything to drop the case; the Judge has given us a date. They are throwing money at me to stop the case "as a gesture of goodwill" I am a very specialised Financial analyst and I believe that I caught them in a fine line which will potentially cost them millions of pounds hence wise they are trying to close all the back doors for others to follow me and changed their T&Cs in legal phrases. Now can anyone please explain to me what is the difference between "Planned" and "Arranged" in legal terms? the phrase in banking term will be "planned overdraft" vs "arranged overdraft" Secondly can anyone please guide me where it is referenced on Government's websites for the phrase of "Business Days/working days" as well as "Bank Holidays" Thank you in advance for your help Regards

-

Hi, I’m new - after reading so many posts over the last few days I thought this may be the best place to ask for advice. So, last year my sister got caught receiving tax credit payments whilst her partner was still living there, she received a £300 penalty and was asked to pay back the £8k she received. A few months after this she did actually split with her partner and, to make ends meet (she has 3 children and works part time) she started a new claim as a single parent and started receiving tax credits again. She started seeing her ex again, he was staying a few nights a week and they were constantly on/off however he was providing her with financial support. A few days ago she received a letter from tax credits saying they suspect he is living there again and they now want bank statements, agreements for rent and council tax etc etc. Now officially they were on/off, and she did many times go to call them but then she’d split with her partner and wasn’t sure if they’d get back together etc and put off calling them as she was worried about money. I have looked through the bank statements during the dates TC have asked for as there are multiple payments from him which would look as though he was living there the whole time. My sister is absolutely petrified at what might happen, she’s calculated what she thinks they’ll want back and it’s around £6k. As this is her second offence, what might happen? If she’s completely honest and agrees to pay whatever she can back, would she get a penalty? Or as it’s now happened a second time, is prosecution more likely? I’m so worried for her, she has 3 young child (the youngest is 18 months) - any advice will be appreciated.

-

Hi Someone I know of is, I believe, claiming tax credits that they are not entitled to. They have substantial income from various places including rental income and the sale of another of their property. The child they are claiming for is with this individual half the week so 50/50 with the other parent, however they are claiming the child is with them 100% of the time. They refuse to share the money and ignore all requests to do so. He is self employed and is known to the CMS for hiding his income, it took them two years to get arrears off him. Any thoughts?

-

Hi, I have a BW Legal court case going on at the moment. Today I received another county court claim from BW Legal for a different company. This is fraud too. Name of the Claimant ? PRAC Financial Ltd Date of issue – 29/09/17 What is the claim for – 1.The Claimant's claim is for the sum of £300 being monies due from the Defendant to the Claimant, under a loan agreement regulated by the consumer credit Act 1974 between the Defendant and Instant Cash Loans Limited t/a Payday UK under account reference xxxxxxx and assigned to the Claimant on 09/12/2016 notice of which has been given to the Defendant. 2. The Defendant has failed to maintain the contractual payment under the terms of the agreement and a default notice has been served and not complied with. 3. The claim also includes the statutory interest pursuant to section 69 of the County Courts Act 1984 at a rate of 8% per annum (a daily rate of £0.06p from the date of assignment of the agreement to 28/09/17 being an amount of £18). What is the value of the claim? £360 Is the claim for - a Bank Account (Overdraft) or credit card or loan or catalogue or mobile phone account? loan When did you enter into the original agreement before or after 2007? After Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. debt collector Were you aware the account had been assigned – did you receive a Notice of Assignment? The account was opened at a different address to mine. I lived at this address about 20 years ago but have moved twice since then. I received a debt collector letter in 2013 for this and I wrote and said they have the wrong person but I did not hear a thing until March this year when I got a county court summons. Did you receive a Default Notice from the original creditor? No Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? I have never made any payments What was the date of your last payment? None Was there a dispute with the original creditor that remains unresolved? Yes, there will be now. I did not know anything about this loan. Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management? No

Hi, I have a BW Legal court case going on at the moment. Today I received another county court claim from BW Legal for a different company. This is fraud too. Name of the Claimant ? PRAC Financial Ltd Date of issue – 29/09/17 What is the claim for – 1.The Claimant's claim is for the sum of £300 being monies due from the Defendant to the Claimant, under a loan agreement regulated by the consumer credit Act 1974 between the Defendant and Instant Cash Loans Limited t/a Payday UK under account reference xxxxxxx and assigned to the Claimant on 09/12/2016 notice of which has been given to the Defendant. 2. The Defendant has failed to maintain the contractual payment under the terms of the agreement and a default notice has been served and not complied with. 3. The claim also includes the statutory interest pursuant to section 69 of the County Courts Act 1984 at a rate of 8% per annum (a daily rate of £0.06p from the date of assignment of the agreement to 28/09/17 being an amount of £18). What is the value of the claim? £360 Is the claim for - a Bank Account (Overdraft) or credit card or loan or catalogue or mobile phone account? loan When did you enter into the original agreement before or after 2007? After Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. debt collector Were you aware the account had been assigned – did you receive a Notice of Assignment? The account was opened at a different address to mine. I lived at this address about 20 years ago but have moved twice since then. I received a debt collector letter in 2013 for this and I wrote and said they have the wrong person but I did not hear a thing until March this year when I got a county court summons. Did you receive a Default Notice from the original creditor? No Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? I have never made any payments What was the date of your last payment? None Was there a dispute with the original creditor that remains unresolved? Yes, there will be now. I did not know anything about this loan. Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management? No -

I'm doing the cardinal sin and posting this on behalf of a friend who doesn't have access to the Internet from home. My friend has had £200 stolen from their account by debit card and are currently on ESA/PIP due to serious medical issues and mental health conditions. My understanding is the transactions were taken by debit card. The Fraudster attempted a payment of £500 and then £400 and then £200 the formers were declined and the latter was accepted. The card in question has now been cancelled and it was reported as soon as they became aware. Barclays are insisting that an investigation be done before any money is refunded taking at least up to 10 working days. We all know that isn't true per the FCA rules here: https://www.fca.org.uk/consumers/unauthorised-payments-account This is going to cause them serious problems as they need to attend medical appointments and put food on the table etc. They have offered a £35 GOGW payment in the first instance. The question becomes, how does one quote the legislation over the phone to effectively force the bank to behave themselves and issue those 'temporary refunds' until the case is investigated? Whilst I am sure they would be happy to make complaints to the FoS etc.. They need access to their funds and the bank are being deliberately obstructive. They want me to speak to them later today to see if quoting the FCA rules has any effect. But is there anything else you could advise in the second instance. Friend is classed as vulnerable adult with serious mental health issues too.

-

I was in a relationship with a man who was both physically and emotionally abusive. He had used my bank account to commit fraud and HSBC held me liable for the debt from the fraud which is £9,566. I managed to find another place to move to and made sure I was virtually untraceable on social media and the internet. I never told the police about the abuse at the time for fear of him being arrested then released and onto me. However I did report the fraud to the police through Action Fraud and they replied a few months later saying that they cannot follow up on it as there is not enough evidence. Now HSBC are harassing me to pay back the debt, I'm a 22 year old student who cannot pay back such a large amount. Although I am terrified of him I tried to locate him so the police can find him yet he is nowhere to be found and I believe now that he had been using a fake identity whilst with me. HSBC have been immensely unhelpful, I have gone back and forth into branches and made numerous phone calls which have all been useless and I cannot take out debt relief management plans or file for bankruptcy because the debt is from fraud. They also filed a CIFAS flag marker against my name so I have to use an online bank now and will not be able to get jobs in many sectors when I finish uni, for 6 years. I opened a case with the Financial Ombudsman which is taking a long time but have been studying hundreds of their decisions on similar cases and they never rule in the favour of the victim/consumer, so I am not confident. What do I do?

I was in a relationship with a man who was both physically and emotionally abusive. He had used my bank account to commit fraud and HSBC held me liable for the debt from the fraud which is £9,566. I managed to find another place to move to and made sure I was virtually untraceable on social media and the internet. I never told the police about the abuse at the time for fear of him being arrested then released and onto me. However I did report the fraud to the police through Action Fraud and they replied a few months later saying that they cannot follow up on it as there is not enough evidence. Now HSBC are harassing me to pay back the debt, I'm a 22 year old student who cannot pay back such a large amount. Although I am terrified of him I tried to locate him so the police can find him yet he is nowhere to be found and I believe now that he had been using a fake identity whilst with me. HSBC have been immensely unhelpful, I have gone back and forth into branches and made numerous phone calls which have all been useless and I cannot take out debt relief management plans or file for bankruptcy because the debt is from fraud. They also filed a CIFAS flag marker against my name so I have to use an online bank now and will not be able to get jobs in many sectors when I finish uni, for 6 years. I opened a case with the Financial Ombudsman which is taking a long time but have been studying hundreds of their decisions on similar cases and they never rule in the favour of the victim/consumer, so I am not confident. What do I do? -

Hi, I have run an eBay shop for over 15 years now and just had this happen to me: A company purchased a 10kg Netgear switch in September. Opens a case as they have changed has mind and returns item. Item never arrives, the tracking number shows delivered, spoke to eBay twice before the dead line and told them this and got the normal brick wall approach. Buyer then escalates the case and gets his money back. Raise a claim with ebay and Royal Mail. My local post woman finds the item, the buyer had sent it to another address, brought it to me this morning and it is a letter not the 10kg item I was expecting. Ebay's fraud team are looking into this. The return address on the letter is a youth group in London that as I can see has nothing to do with the company that brought the item. In total it has taken up at least 3 hours of my time trying to get this sorted. I am going to report this to Action Fraud as well, tempted to start court action for my time. Rant over JJ

-

Hello, all Today I received an intention to prosecute from Thamleslink railway in relation to an incident some weeks ago. To provide some background, I was having a pretty forgetful few days... I left my coat & gloves on the train, forget my suit when attending a wedding and in relation to this post, I forget to get a train ticket. For context, I was extremely sleep deprived as I recently became a father for the first time and was under a ton of pressure. At around 6am, I arrived at my train station late for my train which I was under pressure to make as I had a job interview (the company I work for has been recently bought so I don't have job security & I have bought a new house). I use carnet tickets where I fill in the ticket with the appropriate date. I had forgotten to pick up a new blank ticket that morning and proceeded to use an old ticket unintentionally to enter the barriers and board the train (I didnt check). I suddenly realised the mistake I had made and in my panic, I changed the date of the old ticket to the day of travel. I appreciate this is an error of judgement but in my haze of sleep deprivation and panic, I made a bad choice. A revenue inspector asked me to produce my ticket, which I did and he accused me of changing the dates. I attempted to explain myself and convince him it wasn't premeditated but he informed me of rights and took my details. I admitted my mistake to the officer and admitted to changing the dates. This is my first caution and I am now obviously worried about the outcome (fine, criminal record, prison sentence etc). I am obviously happy to pay a fine as I did a bad thing but I dont want to lose my job over this. I have tickets to prove I had a blank ticket at home and have never done this before. My offences are listed as; - Altering a ticket with intent - entering a train for the purpose of travelling without a ticket Any advice on how I should respond to the prosecution letter and guidance on what penalty they could impose would be appreciated. Thank you so much.

Hello, all Today I received an intention to prosecute from Thamleslink railway in relation to an incident some weeks ago. To provide some background, I was having a pretty forgetful few days... I left my coat & gloves on the train, forget my suit when attending a wedding and in relation to this post, I forget to get a train ticket. For context, I was extremely sleep deprived as I recently became a father for the first time and was under a ton of pressure. At around 6am, I arrived at my train station late for my train which I was under pressure to make as I had a job interview (the company I work for has been recently bought so I don't have job security & I have bought a new house). I use carnet tickets where I fill in the ticket with the appropriate date. I had forgotten to pick up a new blank ticket that morning and proceeded to use an old ticket unintentionally to enter the barriers and board the train (I didnt check). I suddenly realised the mistake I had made and in my panic, I changed the date of the old ticket to the day of travel. I appreciate this is an error of judgement but in my haze of sleep deprivation and panic, I made a bad choice. A revenue inspector asked me to produce my ticket, which I did and he accused me of changing the dates. I attempted to explain myself and convince him it wasn't premeditated but he informed me of rights and took my details. I admitted my mistake to the officer and admitted to changing the dates. This is my first caution and I am now obviously worried about the outcome (fine, criminal record, prison sentence etc). I am obviously happy to pay a fine as I did a bad thing but I dont want to lose my job over this. I have tickets to prove I had a blank ticket at home and have never done this before. My offences are listed as; - Altering a ticket with intent - entering a train for the purpose of travelling without a ticket Any advice on how I should respond to the prosecution letter and guidance on what penalty they could impose would be appreciated. Thank you so much. -

Hi I have been reading a lot of threads on here which all say to ignore RLP letters. I have done so far but am now worried sick. I am past the 21 days it gave me to respond. I got one a few weeks ago after being stopped by security for switching tags in a store and also returning an item that I did buy from TK Maxx but not on that day as I had lost the receipt for it. Bought a similar item that I liked better that was the same price and returned the original one - stupidly justifying in my mind that I was still paying so I wasn't stealing re the tag switching and yes I know that I was and I also know that that it was fraud. The letter I received from RLP is a Letter Before Claim - it says there are no losses due to fraudulent refund transactions not recovered and £150 to cover time etc - total £150 owed. Having read quite a few forum posts it seems it is worse to do a label switch than to steal an item... and I am not proud of what I did. I have also returned the wrong items in the past too (new TK Maxx items that I had bought and was unsure about keeping - then the receipt return date had expired so I bought another and then returned as above but didn't get stopped on those occasions). I am obviously banned from TK Maxx and 100% appreciate that things could have been a lot worse as the security staff didn't call the police at the time . I could have had a criminal record.... I am also relieved that I was stopped because I became a total shopaholic at the fine old age of 52 since I split up with my wife a few years ago and I truly needed to stop. Since this incident, I have stopped wasting hours wandering around stores and buying stuff I don't need - so I am thinking that the £150 fine is a small amount to pay to have stopped this mindless shopping. A friend I confided in also has convinced me to make an appointment with my doctor as she thinks I am depressed and using shopping to replace my wife... , I will do this. But @Maxxer as all holding rooms have audio and video and I admitted what I did (switching tags and returning wrong item) would it be better to just pay the RLP letter? Did you mean on a comment on another thread you made that they would need to get another fraudulent return by me after this incident (which I won't do) and then they can make a case or will they go back on previous purchases/returns on my card and then get the police involved? I suppose I am asking if I pay would that be the end of it or would it be the end of it anyway unless I go back into TK Maxx again? I hope this makes sense. I am sorry this is so long but thanks for reading. From one idiotic man who has made stupid mistakes not thinking about the consequences and now worried sick.

Hi I have been reading a lot of threads on here which all say to ignore RLP letters. I have done so far but am now worried sick. I am past the 21 days it gave me to respond. I got one a few weeks ago after being stopped by security for switching tags in a store and also returning an item that I did buy from TK Maxx but not on that day as I had lost the receipt for it. Bought a similar item that I liked better that was the same price and returned the original one - stupidly justifying in my mind that I was still paying so I wasn't stealing re the tag switching and yes I know that I was and I also know that that it was fraud. The letter I received from RLP is a Letter Before Claim - it says there are no losses due to fraudulent refund transactions not recovered and £150 to cover time etc - total £150 owed. Having read quite a few forum posts it seems it is worse to do a label switch than to steal an item... and I am not proud of what I did. I have also returned the wrong items in the past too (new TK Maxx items that I had bought and was unsure about keeping - then the receipt return date had expired so I bought another and then returned as above but didn't get stopped on those occasions). I am obviously banned from TK Maxx and 100% appreciate that things could have been a lot worse as the security staff didn't call the police at the time . I could have had a criminal record.... I am also relieved that I was stopped because I became a total shopaholic at the fine old age of 52 since I split up with my wife a few years ago and I truly needed to stop. Since this incident, I have stopped wasting hours wandering around stores and buying stuff I don't need - so I am thinking that the £150 fine is a small amount to pay to have stopped this mindless shopping. A friend I confided in also has convinced me to make an appointment with my doctor as she thinks I am depressed and using shopping to replace my wife... , I will do this. But @Maxxer as all holding rooms have audio and video and I admitted what I did (switching tags and returning wrong item) would it be better to just pay the RLP letter? Did you mean on a comment on another thread you made that they would need to get another fraudulent return by me after this incident (which I won't do) and then they can make a case or will they go back on previous purchases/returns on my card and then get the police involved? I suppose I am asking if I pay would that be the end of it or would it be the end of it anyway unless I go back into TK Maxx again? I hope this makes sense. I am sorry this is so long but thanks for reading. From one idiotic man who has made stupid mistakes not thinking about the consequences and now worried sick. -

I am posting on behalf of a neighbour, not sure if anyone can help here as its beyond me. Husband and wife window company, based at home. They were both working in the business until 3 years ago. Sadly their youngest child was born very ill and she was doing less and less and less work. They claimed carers allowance and took on a part time bookkeeper. The wife hours were reduced and the wages dropped to reflect this. Last year, the accountant upped her wages to be above the threshold and for 10 months they have been claiming illegally. They were not aware of this as the accountant doesn't send weekly wage slips and the wage is more of an entry into the books rather than an actual sum paid into an account each week/month. The accountant has told them that he knew about the benefits and forgot. He refuses to put this in writing! As a layman it seems that they are very naive, trusted an accountant and landed themselves in hot water without going out to defraud the system. Anyone have any advice and able to recommend a specialist solicitor?

I am posting on behalf of a neighbour, not sure if anyone can help here as its beyond me. Husband and wife window company, based at home. They were both working in the business until 3 years ago. Sadly their youngest child was born very ill and she was doing less and less and less work. They claimed carers allowance and took on a part time bookkeeper. The wife hours were reduced and the wages dropped to reflect this. Last year, the accountant upped her wages to be above the threshold and for 10 months they have been claiming illegally. They were not aware of this as the accountant doesn't send weekly wage slips and the wage is more of an entry into the books rather than an actual sum paid into an account each week/month. The accountant has told them that he knew about the benefits and forgot. He refuses to put this in writing! As a layman it seems that they are very naive, trusted an accountant and landed themselves in hot water without going out to defraud the system. Anyone have any advice and able to recommend a specialist solicitor? -

https://www.consumeractiongroup.co.uk/forum/showthread.php?296513-296513&p=3317951#post3317951 I am just considering this and contemplating taking court action against unregulated property manger who took a secret commission

https://www.consumeractiongroup.co.uk/forum/showthread.php?296513-296513&p=3317951#post3317951 I am just considering this and contemplating taking court action against unregulated property manger who took a secret commission -

Hi, its been a while since Ive been here. Just logging on and telling my story about TSB and a sim swap that emptied our accounts for a while. TSB have changed the way customers have to log in via an APP, whereas before we had a card reader. I never use the app as it doesn't work on Win phone. TSB facilitated a fraud on our account after a sim swap was made. They sent a one time password to someone, who then logged in and emptied the account. Once I tried to log in, I spoke to TSB and noticed this. I then tried contacting their fraud dept, but because it was a business account, they couldn't help ( infuriating). After long waits on the phone ( over 5 hours ) I had to take time out from my contracted hours, to go to the branch, where I waited most of the day for them to contact fraud with no answer. Went the next day and pretty much same thing. Id lost 2 days of work which we cannot recover. I issued an invoice, which TSB have totally ignored, even though good ole Paul pester promised that no customer would be out of pocket. We are now at the stage where, the invoice is overdue (14 days) plus an extra 10 business days to pay up. My next task is LBA, with further 10 to rectify. If anyone wants to chip in feel free, I am so annoyed with them not even writing to us to acknowledge anything, I am hoping to get my day in Court. Just had a look through CPR and the rules are a little different for a business to make a claim, Its 30 days from a LBA. I do like the reply forms that have to fill in, this could be fun. Additionally, they also owe us 70 odd quid because they blocked the accounts and a payment wasn't received, It was taken from a suppliers account and not applied to ours, even though TSB have said its been processed. Second LBA going off next week

-

Hi All, I have been chased since 2007 on a Northern Rock mortgage shortfall from 2002. I have never admitted liability for said debt and I have never made a payment. Shoosmiths on behalf of Arrow are now saying that I made a payment in 2008 which re-sets the statute barred status that I told them it has. I have never ever made a payment, the only money that has been sent was to cover the cost of a SAR in late 2007. After 2007 everything went quiet until 2013, eventually when I wrote back and forth a few times the DCA said their "case was closed" on this matter. Roll forward to 2017 and they start again until November 2017 then quiet again until last week. I believe that fraud is being committed here and wondered what others in my situation would do? I am thinking of going direct to Action Fraud and reporting them, I am, tbh, sick and tired of this harassment. I apologise if I delay to respond to anyone who replies as I am busy through this afternoon. Thank you in advance.

Hi All, I have been chased since 2007 on a Northern Rock mortgage shortfall from 2002. I have never admitted liability for said debt and I have never made a payment. Shoosmiths on behalf of Arrow are now saying that I made a payment in 2008 which re-sets the statute barred status that I told them it has. I have never ever made a payment, the only money that has been sent was to cover the cost of a SAR in late 2007. After 2007 everything went quiet until 2013, eventually when I wrote back and forth a few times the DCA said their "case was closed" on this matter. Roll forward to 2017 and they start again until November 2017 then quiet again until last week. I believe that fraud is being committed here and wondered what others in my situation would do? I am thinking of going direct to Action Fraud and reporting them, I am, tbh, sick and tired of this harassment. I apologise if I delay to respond to anyone who replies as I am busy through this afternoon. Thank you in advance. -

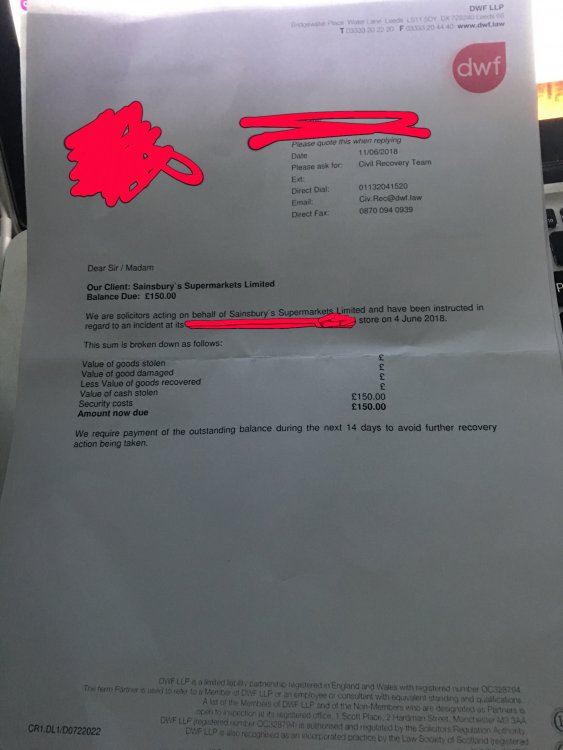

Hi all, I resigned from my part-time job in Sainsbury's on 4th June 2018 for theft of Nectar points on the till, i.e. crediting my Nectar card with £110 worth of points. I was in absolute bits when I was hauled in and questioned over it because it was only then that it hit me, although at the time of course I knew what I was doing. I was a genuine dickhead for doing what I did because he was a decent manager and I abused his trust. At first the store manager wasn't sympathetic and alluded to the fact that police might be involved. However later on because of the dates (I had been working there for more than a year and the first occurrence of this was on 21st May 2018) and because he knew my character and that I really didn't enjoy working there at all we had a chat was very kind and advised me to resign so I wouldn't have to attend the investigatory meetings during my contracted working hours (I also had a holiday booked at that time so it couldn't have been worse timing). My Nectar card (registered with a false name and details) and colleague discount card were also taken. I've gotten back from holiday today to a letter form the DWP stating that I must pay £150 within 14 days to cover 'security costs' (by 25th June), however a breakdown of the sum I am supposed to pay back doesn't detail figures of any sort, simply £ signs, and then underneath this sum they say I'm supposed to pay. in addition it states that it was one incident that occurred on 4th June when I wasn't even in the country let alone still working there, as opposed to when it actually first occurred on 21st May, I used the points on a small number of basic groceries in store which to my understanding is what they could legitimately pursue me for (£12/£13 at stretch), but vast majority of the points were spent on eBay so I'm wondering if it would go that far since my Nectar card was taken. From what I've read so far I'm supposed to ignore the letters however as I was a former employee I don't know what could happen if i don't pay up. Also I would like to know what sort of reference would be given in this instance when applying for jobs (I have a degree and have been applying for jobs for the past year but with no joy). there is nothing stated relating to police charges and fines I haven't received any direct correspondence from Sainsbury's themselves. I'm already out of a job, can't seem to find something that utilises my degree and my parents are always extremely unhelpful and always demanding unreasonable amounts of money for unclear reasons directly and indirectly so paying the fine would put me in an even tighter spot financially. They do not know about this and of course would kick up an almighty fuss if they did, so any advice on what to say in terms of my newfound availability of time would be great. This was a hard lesson learned and although I grew to hate working there, I'm more disappointed in myself for letting down my former boss and the people I worked with (a couple of who contacted me afterwards and said they thought it wasn't a big deal, but I'm still paranoid about it). At no point did I take money from any till and have never done so in any previous job. I have attached a picture of the letter for reference. Any help would be greatly appreciated and thank you to CAG and co for what is already available.

Hi all, I resigned from my part-time job in Sainsbury's on 4th June 2018 for theft of Nectar points on the till, i.e. crediting my Nectar card with £110 worth of points. I was in absolute bits when I was hauled in and questioned over it because it was only then that it hit me, although at the time of course I knew what I was doing. I was a genuine dickhead for doing what I did because he was a decent manager and I abused his trust. At first the store manager wasn't sympathetic and alluded to the fact that police might be involved. However later on because of the dates (I had been working there for more than a year and the first occurrence of this was on 21st May 2018) and because he knew my character and that I really didn't enjoy working there at all we had a chat was very kind and advised me to resign so I wouldn't have to attend the investigatory meetings during my contracted working hours (I also had a holiday booked at that time so it couldn't have been worse timing). My Nectar card (registered with a false name and details) and colleague discount card were also taken. I've gotten back from holiday today to a letter form the DWP stating that I must pay £150 within 14 days to cover 'security costs' (by 25th June), however a breakdown of the sum I am supposed to pay back doesn't detail figures of any sort, simply £ signs, and then underneath this sum they say I'm supposed to pay. in addition it states that it was one incident that occurred on 4th June when I wasn't even in the country let alone still working there, as opposed to when it actually first occurred on 21st May, I used the points on a small number of basic groceries in store which to my understanding is what they could legitimately pursue me for (£12/£13 at stretch), but vast majority of the points were spent on eBay so I'm wondering if it would go that far since my Nectar card was taken. From what I've read so far I'm supposed to ignore the letters however as I was a former employee I don't know what could happen if i don't pay up. Also I would like to know what sort of reference would be given in this instance when applying for jobs (I have a degree and have been applying for jobs for the past year but with no joy). there is nothing stated relating to police charges and fines I haven't received any direct correspondence from Sainsbury's themselves. I'm already out of a job, can't seem to find something that utilises my degree and my parents are always extremely unhelpful and always demanding unreasonable amounts of money for unclear reasons directly and indirectly so paying the fine would put me in an even tighter spot financially. They do not know about this and of course would kick up an almighty fuss if they did, so any advice on what to say in terms of my newfound availability of time would be great. This was a hard lesson learned and although I grew to hate working there, I'm more disappointed in myself for letting down my former boss and the people I worked with (a couple of who contacted me afterwards and said they thought it wasn't a big deal, but I'm still paranoid about it). At no point did I take money from any till and have never done so in any previous job. I have attached a picture of the letter for reference. Any help would be greatly appreciated and thank you to CAG and co for what is already available.

-

Hi All, Firstly, this isn't strictly a PCN issue but it is related to one, so I'm not sure if this the appropriate forum and please let me know if not. My vehicle was clamped on 30th June and I discovered this and spoke to the bailiff on 1st July. I've submitted TE7 & TE9 forms to TEC so this should all be resolved this afternoon. However, I am going to make several complaints about the bailiff's actions as he was not only extremely rude and unprofessional when dealing with me, but also probably broke the law. Some background info: I called the bailiff (MO) on Sunday afternoon (01/07) but he didn't answer; he then called me at 10pm Sunday evening to discuss. During this conversation he told me the vehicle in question had been clamped previously and I had cut it off, telling me that because of this the vehicle would be towed immediately if I didn't pay the outstanding balance. When I contested this and asked for info his response was along the lines of "I dunno, that's just what the system says" and refused to give any further evidence. I was pretty incensed by the accusation so told him it was utterly false (exact words) and he hung up on me, refusing to answer again. Today I called him to get the PCN number then did my relevant homework and called him back to let him know I'd submitted forms with TEC and he should hear from the issuing authority by the end of the day. I asked him to give me his full name and registration details so I could submit a complaint about his behaviour last night and he outright refused, saying he didn't have to. When I told him he was legally obligated to give me his information he got increasingly angry and doubled down. He said he would show his certificate when releasing the vehicle but would not give details to me - to which I responded by saying we both know that will never happen as he will most likely quietly remove the clamp and then be gone. I eventually gave up with no information. I checked his name on the immobilisation certificate then checked the Certified Bailiff Register and found his full name and the court / company he's registered with, so am going to submit my complaints there first. My most serious complaint is that his attempt to extort me into payment by claiming I had removed a previous clamp (let me just state - I hadn't) is a violation of The Fraud Act 2006 Section 2 and his refusal to provide any evidence for this, despite it being "on his system" is also a violation of Section 3. So my question is this: who do I report this to and how? I'm currently drafting a complaint to Hertford County Court (where MO is registered) with all of this included, but would like to take this much, much further so he never attempts this stuff again. Having never submitted any kind of criminal charges before I have no idea where to start.

Hi All, Firstly, this isn't strictly a PCN issue but it is related to one, so I'm not sure if this the appropriate forum and please let me know if not. My vehicle was clamped on 30th June and I discovered this and spoke to the bailiff on 1st July. I've submitted TE7 & TE9 forms to TEC so this should all be resolved this afternoon. However, I am going to make several complaints about the bailiff's actions as he was not only extremely rude and unprofessional when dealing with me, but also probably broke the law. Some background info: I called the bailiff (MO) on Sunday afternoon (01/07) but he didn't answer; he then called me at 10pm Sunday evening to discuss. During this conversation he told me the vehicle in question had been clamped previously and I had cut it off, telling me that because of this the vehicle would be towed immediately if I didn't pay the outstanding balance. When I contested this and asked for info his response was along the lines of "I dunno, that's just what the system says" and refused to give any further evidence. I was pretty incensed by the accusation so told him it was utterly false (exact words) and he hung up on me, refusing to answer again. Today I called him to get the PCN number then did my relevant homework and called him back to let him know I'd submitted forms with TEC and he should hear from the issuing authority by the end of the day. I asked him to give me his full name and registration details so I could submit a complaint about his behaviour last night and he outright refused, saying he didn't have to. When I told him he was legally obligated to give me his information he got increasingly angry and doubled down. He said he would show his certificate when releasing the vehicle but would not give details to me - to which I responded by saying we both know that will never happen as he will most likely quietly remove the clamp and then be gone. I eventually gave up with no information. I checked his name on the immobilisation certificate then checked the Certified Bailiff Register and found his full name and the court / company he's registered with, so am going to submit my complaints there first. My most serious complaint is that his attempt to extort me into payment by claiming I had removed a previous clamp (let me just state - I hadn't) is a violation of The Fraud Act 2006 Section 2 and his refusal to provide any evidence for this, despite it being "on his system" is also a violation of Section 3. So my question is this: who do I report this to and how? I'm currently drafting a complaint to Hertford County Court (where MO is registered) with all of this included, but would like to take this much, much further so he never attempts this stuff again. Having never submitted any kind of criminal charges before I have no idea where to start. -

Hello All, I have Banked with Barclays as a personal customer for several years. Recently I opened a Barclays Business account and 2 weeks later following our first transaction received funds of approx 20k followed by several additional purchases from the same Business client totalling some 80k. The money was used to pay the overseas supplier, (supplier A) and balance used as down payment for additional import stock. The following month approx 40k was received from a customer for building supplies, we had secured 30 days credit terms with the supplier, (supplier B). The same day the money was put to use by making a payment to supplier A with whom we had already placed a deposit. The next day the account was locked pending a review. Initially we thought money in and out same day likely triggered the review, and had ready relevant invoices and purchase orders. Barclays did not ask for any information, so we waited for the review to complete. After the review period, Barclays closed both Personal and Business accounts with the following letter: We phoned Barclays wanting answers and they simply advised there was nothing they could do and we should submit proof of funds to barclayspof#barclayscorp.com which we did. We had to wait 10 working days for a response. So far the timeline goes like this: Dec 2017 Business Account opened Feb 13, 2018 Money received for building supply customer - 40k made up of 4 x 10k payments Feb 13, 2018 Request made in Branch to have 38k transferred to overseas Escrow platform, awaited supplier invoice, then payment was released. Feb 14, Payment via Swift leaves Barclays and they locks accounts. Feb 15, I enquire in branch about accessing funds, they release some wages from my current account. I enquire about review, they say very little, go around the back make phone calls etc. I enquire about Swift payment, and manager quietly tells cashier to 'place a marker on the notes', they explain swift is en-route and should arrive within 3-5 working days. Feb 22 Letter above received. I send supporting docs to my local business manager via email, and request they release funds as per their instructions: "Make alternative arrangements for your banking services immediately and withdraw any outstanding credit balance from your account(s)." Response received is they can't help and email the docs to Pof@barclays. 5 March, Comprehensive email sent to POF and in the meantime, we approached another Bank with a view to moving our Business banking needs. They replied, 'no' and referred us to CIFAS. 12 March, whilst waiting for SAR result to CIFAS I emailed pof@barclays: Dear Sir(s) Whilst I await your response to the unfreezing of the accounts and access to my funds, I have requested a full disclousure of data held on me from Barclays Bank via a Subject Access Request submitted 8 March 2018. Could you ensure I receive the note put on the system at the local branch Manager's request, dated 15 February 2018, where I was informed the transaction was suspicious. I didn't know what that meant at the time, and it was received by the beneficiary a day or two later without issue. I would like to see what exactly was suspicious, and if it relates to the customer who paid the invoice, myself as the account holder or the beneficiary receiving the swift payment. Cifas report received 16 March: My knee jerk reaction, having skimmed over the letter was to write the following complaint and hand deliver it into my local branch: 16 March, phoned Barc fraud department, passed through security and was told they still assessing documentation I supplied. I explained I'm phoning about the Cifas marker. Call Lady explained there was a specific department for that and she would put me through. 20 mins on hold and back to customer services, I phone again and this time the young man answering explains 'that department' have now gone home and asks how he might be of help? I explain I want to know what 'False instrument(s) paid in' on the Cifas report refers to? He explains he would enquire and ring me Monday 19th March. 17 March I re-read the Cifas report carefully and realise the 4 payments of 10k must have been fraud and Barclays believe me to be involved. Email received today from POF@Barclays: BARCLAYS CLASSIFICATION: Restricted - External "Hello, Thank you for recently contacting us in regards to your remaining balance. We’ve completed your account review and are now in a position to return funds. What this means for you. Please make arrangements to visit your local branch with two forms of I.D I have left relevant notes on your account to authorise you to withdraw your funds." I believe this refers to my personal account, and have no intention of pursuing the remaining funds from the 40k payment. My response today to their email: 17th March 2018 Thank you for your earlier response. I have been told by Barclays Customer Services Fraud Team that Barclays closed my account of 3 years for 'commercial' reasons and this would not impact my ability to open Business account elsewhere. However, I applied to another High Street lender and they refused to accommodate my needs and referred me to CIFAS. I have contacted CIFAS, received a SAR response and filed a complaint with Barclays 16/03/2018, (copy attached) for accusing me of being a money launderer. I have since shown the Cifas report and Bank Statements to a friend in the Legal Profession. I have been advised Barclays are actually accusing me of allowing my account to be used for fraud and actively receiving 4 x £10,000 of stolen/fraudulently obtained money. This is absolutely not the case, and I want Barclays to clear me of any wrongdoing and update CIFAS entry immediately. Barclays, If the money was unlawfully obtained, why did you allow it to be credited to my account? Why on the same day did you allow me to send Money overseas via a Manager in Branch? Why did you not contact me at any point to raise concerns over these payments? Why did you not warn me when I enquired in Branch 15/03/2018 on the status of the Swift Transfer? I could have recalled the money at anytime in the several days it remained in my Akirix Foreign Exchange account. I could have prevented the customer from collecting the goods they purchased. Many things could have been done to prevent this unfortunate situation. On the face of it, it very much looks like Barclays failed in their duty of customer care to protect these funds from falling into the wrong hands, and are now making me, a innocent business to be the scapegoat. This is totally unacceptable. Please provide me with the crime reference number, so I can liaise with the Police and get to the bottom of this. I await a response from Barclays; I spoke to #### and #### yesterday, 16/03/2018 before getting help from my friend. #### from the Fraud Team promised to ring me Monday 19/03/2018 and explain what Giro Credits on the 13th February mean. The Branch statement shows it as Third Party Transfers, (FIP) see attached copy, yet the Statement received after Account closure reports the transfers as Giro payments. I will be awaiting his response before submitting a Second complaint, now that I am getting clarification on the actual issue to hand. Put this situation right by removing the CIFAS entry against my name. End of timeline I want Barclays to correct the Cifas entry and clear me of any wrongdoing. I had no idea the money was received via Giro payments, (whatever they are). We made clear we do not accept Cheques or Cash and only Bank Transfers are accepted for payments above £5,000. We carried out our due diligence as best we could and should not be expected to Police transactions. I've never put pen to paper to complain before and would appreciate some input from experienced members following the outcome of Barclays phone call due Monday 19th March. Thank you for reading this. I will update on Monday Lee docs1.pdf

-

Hi all I was a virgin media customer for years before someone manages to hack into my connected sipura voip modem device making it dial prem rate numbers and ran up a bill of £8000 in a matter of 3 days somehow bypassing the credit limit on my account. I have sent an email and called vm to try and sort things out to no avail Vm have made us responsible for the bill blaming the third party device and saying I shouldn't have had a third party device on the line? Somehow I think that vm are not telling me everything and that it could be someone inside vm that was the person who made the calls how was my credit limit bypassed?...

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS