Showing results for tags 'reply'.

-

Good evening all, I've done a bit of research trying to close accounts which led me to requesting CCA's to Cabot. I sent two for two different accounts which they took off Halifax (1 x CC & 1 x Current Acc Overdraft). I posted the following to them: Dear Sir/Madam Account No: With reference to the above agreement, I require you to supply the following documentation before I will correspond with you further on this matter. 1. You must supply me with a true copy of the alleged agreement you refer to. This is my right under your obligation to supply a copy of the agreement, under the legislation contained within s.78 (1) Consumer Credit Act 1974. 2. A full statement of account. 3. A signed true copy of the deed of assignment of the above referenced agreement that you allege exists. 4. A copy of any other documents referred to in the agreement. I understand that under the Consumer Credit Act 1974 (sections 77-79) , I am entitled to receive a copy of any credit agreement and a statement of account when I request it. I enclose a payment of £1 which is the fee payable under the Consumer Credit Act 1974. I understand a copy of any credit agreement along with a statement of account should be supplied within 12 working days. I understand that, under the Consumer Credit Act 1974, creditors are unable to enforce an agreement if they fail to comply with the request for a copy of the agreement and statement of account. A speedy response would be appreciated to resolve the matter amicably. I look forward to hearing from you soon. Yours faithfully THE LETTERS WERE RECEIVED ON 17TH/18TH JULY AND TODAY I RECEIVED THE FOLLOWING LETTERS: Thank you for your CCA request etc etc... We currently do not have this information on file. However I have requested the relevant details, which include a copy of the credit agreement, statement of account and relevant terms and conditions from the original lender. You have requested a copy of the Deed of Assignment. Please be advised that the DOA is a confidential document between Cabot and the original lender. It does not contain any personal details relating to you or your account and is not available for disclosure. We sent you a Notice of Assignment for your account to your address, which is sufficient to confirm our ownership of this account. Only the courts can request this... Blah blah blah. A couple of things here... I asked for a true copy, they are referring to simply a copy. If they do obtain a copy, is this enforceable? Also is it acceptable what they are saying about disclosing the DOA to me? I don't ever recall being sent a Notice of Assignment, if I did, is this sufficient to confirm ownership and enforceable? I have been currently paying towards what they are claiming, on a monthly basis via DMP. The next payment is due in a couple of days. Should I continue paying or is it advisable to stop until they wholly action my request? Thanks in advance and any help/advice/feedback is much appreciated! I'm looking to get a mortgage by the end of the year so I can get my son into the school I/he wants. Many thanks.

Good evening all, I've done a bit of research trying to close accounts which led me to requesting CCA's to Cabot. I sent two for two different accounts which they took off Halifax (1 x CC & 1 x Current Acc Overdraft). I posted the following to them: Dear Sir/Madam Account No: With reference to the above agreement, I require you to supply the following documentation before I will correspond with you further on this matter. 1. You must supply me with a true copy of the alleged agreement you refer to. This is my right under your obligation to supply a copy of the agreement, under the legislation contained within s.78 (1) Consumer Credit Act 1974. 2. A full statement of account. 3. A signed true copy of the deed of assignment of the above referenced agreement that you allege exists. 4. A copy of any other documents referred to in the agreement. I understand that under the Consumer Credit Act 1974 (sections 77-79) , I am entitled to receive a copy of any credit agreement and a statement of account when I request it. I enclose a payment of £1 which is the fee payable under the Consumer Credit Act 1974. I understand a copy of any credit agreement along with a statement of account should be supplied within 12 working days. I understand that, under the Consumer Credit Act 1974, creditors are unable to enforce an agreement if they fail to comply with the request for a copy of the agreement and statement of account. A speedy response would be appreciated to resolve the matter amicably. I look forward to hearing from you soon. Yours faithfully THE LETTERS WERE RECEIVED ON 17TH/18TH JULY AND TODAY I RECEIVED THE FOLLOWING LETTERS: Thank you for your CCA request etc etc... We currently do not have this information on file. However I have requested the relevant details, which include a copy of the credit agreement, statement of account and relevant terms and conditions from the original lender. You have requested a copy of the Deed of Assignment. Please be advised that the DOA is a confidential document between Cabot and the original lender. It does not contain any personal details relating to you or your account and is not available for disclosure. We sent you a Notice of Assignment for your account to your address, which is sufficient to confirm our ownership of this account. Only the courts can request this... Blah blah blah. A couple of things here... I asked for a true copy, they are referring to simply a copy. If they do obtain a copy, is this enforceable? Also is it acceptable what they are saying about disclosing the DOA to me? I don't ever recall being sent a Notice of Assignment, if I did, is this sufficient to confirm ownership and enforceable? I have been currently paying towards what they are claiming, on a monthly basis via DMP. The next payment is due in a couple of days. Should I continue paying or is it advisable to stop until they wholly action my request? Thanks in advance and any help/advice/feedback is much appreciated! I'm looking to get a mortgage by the end of the year so I can get my son into the school I/he wants. Many thanks. -

Hi all, Today my wife received rather thick envelope containing letters from Lowell and BW Legal, containg a reply form, which after looking about online seems like a new thing (pre action Protocol?). My wife hasnt heard anything about this debt in a very long time, plus we moved home last year so that possibly hasnt helped matters. The debt is for Vanquis Bank (Credit Card) and was defaulted on 31/10/2012 - no payments have been made since before this date and its approaching being statute barred. Whats the best way to proceed WITHOUT acknowledging the debt? Do I tick boxes D to dispute the debt and tick box I and ask for more information? If so what information? Should I also sent a normal CCA letter with the reply form? Do I now just deal with BW Legal seen as all this has come from them as Lowel say it has been sent BW Legal? Many thanks Martyn

Hi all, Today my wife received rather thick envelope containing letters from Lowell and BW Legal, containg a reply form, which after looking about online seems like a new thing (pre action Protocol?). My wife hasnt heard anything about this debt in a very long time, plus we moved home last year so that possibly hasnt helped matters. The debt is for Vanquis Bank (Credit Card) and was defaulted on 31/10/2012 - no payments have been made since before this date and its approaching being statute barred. Whats the best way to proceed WITHOUT acknowledging the debt? Do I tick boxes D to dispute the debt and tick box I and ask for more information? If so what information? Should I also sent a normal CCA letter with the reply form? Do I now just deal with BW Legal seen as all this has come from them as Lowel say it has been sent BW Legal? Many thanks Martyn -

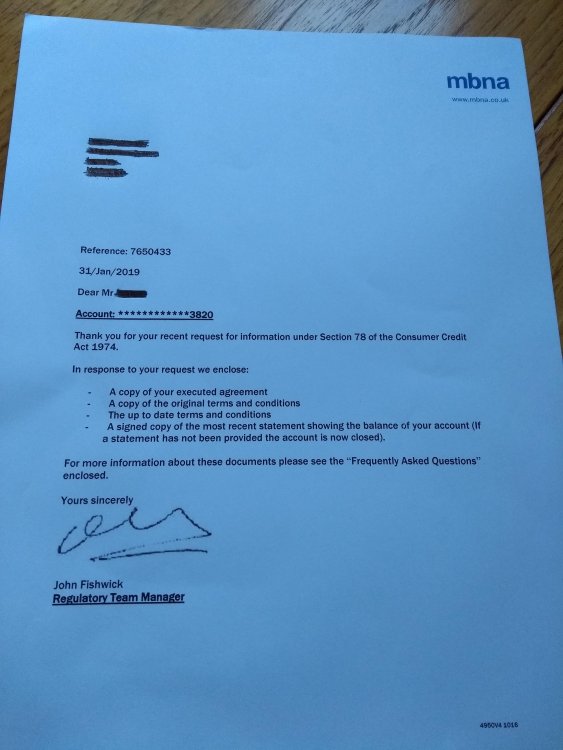

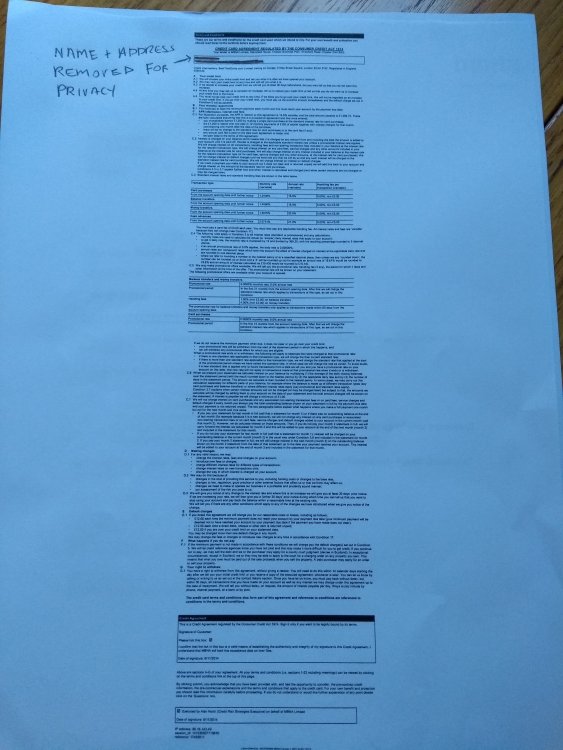

Had the following back from MBNA in response to a CCA request. 2 sets of T&C's, one current, and one supposedly from the time they card was taken out (not sure how I'd actually verify that) A summary statement showing current balance And a "copy executed agreement" Have uploaded the covering letter and the redacted "copy executed agreement". Basically, is this valid? This card was taken out in late 2014, and from what I've read it seems like it probably is a valid an enforceable response to my request, but would like to be sure before taking next step (MBNA bluntly rejected a recent full and final offer of around 60% of balance, claiming they never accept such offers. I should also mention that the debt is still with MBNA and no payments have been made for 3 months now. Current balance is a around £10.5k. Borrowing from family and selling a few things I reckon I could raise £8k tops. It doesn't seem like MBNA would accept this as a full and final, and all the while the interest mounts up.

-

Good evening...... I had the pleasure of a member of Resolve Calls team visit my home this evening with regard to an old debt of an unsecured loan taken out with Northern Rock in 2004 - last paid via debt management in 2014. Cabot took up this debt in 2015, I sent them a CCA request in Jan 16 but from memory only received a standard response. I have two questions i could really do with some advice on 1) Should I write to Cabot reminding them of the outstanding CCA request or resend the request? From memory i think they sent a generic response effectively saying they were 'looking for it' . I know i should have kept this info, however the original signed agreement was definitely never provided. 2) Is there a letter or anything I can communicate to prevent these people just turning up at my door? They wrote to me months ago informing me of Resolve Calls involvement but i assumed it was fairly generic. The guy was very polite and non-threatening, I gave him no more info than he could find from the electoral roll, his objective seemed to be to get me to call his office on my doorstep at 7.30pm in the dark. At this point i politely told him that wouldn't be happening so he gave me a card with details on to call. I work away fairly often and do not want these people turning up when my partner and young son are at home alone. Thanks in advance for any advice

Good evening...... I had the pleasure of a member of Resolve Calls team visit my home this evening with regard to an old debt of an unsecured loan taken out with Northern Rock in 2004 - last paid via debt management in 2014. Cabot took up this debt in 2015, I sent them a CCA request in Jan 16 but from memory only received a standard response. I have two questions i could really do with some advice on 1) Should I write to Cabot reminding them of the outstanding CCA request or resend the request? From memory i think they sent a generic response effectively saying they were 'looking for it' . I know i should have kept this info, however the original signed agreement was definitely never provided. 2) Is there a letter or anything I can communicate to prevent these people just turning up at my door? They wrote to me months ago informing me of Resolve Calls involvement but i assumed it was fairly generic. The guy was very polite and non-threatening, I gave him no more info than he could find from the electoral roll, his objective seemed to be to get me to call his office on my doorstep at 7.30pm in the dark. At this point i politely told him that wouldn't be happening so he gave me a card with details on to call. I work away fairly often and do not want these people turning up when my partner and young son are at home alone. Thanks in advance for any advice -

I personally know somebody who got a mortgage with an IVA so I know its possible as that's more frowned upon. I appreciate I won't get as good a deal having a DMP to my name though. Been in DMP for about 5 years. So defaults will be gone within 2 years. Cabot (was Halifax) £2300 Cabot (was Halifax)£3250 CashEuroNet (aka Quick Quid) £770 Instant Cash Loans (aka Payday uk)£305 Link (was Co-op) £5700 Moorcroft (aka Home Retail Group) £132 Nationwide (as is) £4200 Although one of these does not even appear on any of my credit reports.

-

Cabot purchased a debt, the original debt was either m&s credit card or tesco credit card,i think. I have ignored all letters. I suspect its almost (if not) statute barred by now. (need to dig out files to check this) I now have received a letter before claim and reply form, from Cabots solicitors, mortimer cooke. Not sure whether to reply, is it bonafide? a scare tactic, or will no response get me a ccj? Any guidance will be very appreciated.

-

i have just had a letter back saying my credit card around 2001-4 is outside of banks retention period so they cannot provide the data i asked for for my sar. so i assume the ppi complaint i sent will also be declined.... shocking.... they are of course lying through their back teeth any suggestions of how i should respond???

-

Hi there all. I have a question regarding my account. I had a Virgin Money Account which I was paying off interest only for, for a significant time and one i had PPI on. I was paying minimum payment for some time which meant interest and charges only on it. My business failed earlier this year and I am only now coming out the other side with a salary again. The account has been sold to IDEM and noodle gives the following information. Idem Capital Securities £ 4,471 22/09/2014 Default Name nnnnn Address nnnnnnn Date of birth nnnnnnn Account type Credit Card Account number ******6888 0 Account start date 09/05/2008 Opening balance £ 4,471 Regular payment £ £ 1 Repayment frequency Monthly Date of default 28/02/2014 Default balance £ 4,471 I am now being contacted by Westcot about it daily and in letters. I would like some advice please. 1 - It seems I can still approach Virgin/MBNA about PPI and charges on this card as I believe i have a claim that may be valid. Do I contact westcot and advise them that I will be contacting them or not? 2 - What should be my next plan? I have no issue paying this debt off but i see all this stuff about CCA requests and SAR requests etc a nd I am not sure what I should do, I can ring them up and offer £200 a month not an issue. 3 - Do they have any legal right for me to disclose my financial details to them as in income and outgoings - i can see from other threads that IDEM seem to think that they are in their rights to ask lots however I don't know what westcot will want from me. Thanks in advance!

-

Evening, I am seeking some thoughts from more learned individuals. I received a Claim Form end of Dec 2017 for an old WF debt and subsequently entered my defence on MCOL. This was on the 5 January. Since then I have received nothing further to my formal requests for additional information surrounding claim aside from two chaser letters from Cabot's solicitors detailing their 'client wish to settle out of court' and then '14 days to negotiate settlement otherwise instructions from Cabot to lift stay'. Called the court today and was advised that Cabot / their solicitors had attempted to amend the particulars of the claims on the 11 February but this was denied as they did not pay the fee. Their last letter to me dated 5 March is as above on the 14 days. I'm tempted to actually have the claim struck out as the claim remains stayed open ended. Has this happened to anyone before ? Thanks

Evening, I am seeking some thoughts from more learned individuals. I received a Claim Form end of Dec 2017 for an old WF debt and subsequently entered my defence on MCOL. This was on the 5 January. Since then I have received nothing further to my formal requests for additional information surrounding claim aside from two chaser letters from Cabot's solicitors detailing their 'client wish to settle out of court' and then '14 days to negotiate settlement otherwise instructions from Cabot to lift stay'. Called the court today and was advised that Cabot / their solicitors had attempted to amend the particulars of the claims on the 11 February but this was denied as they did not pay the fee. Their last letter to me dated 5 March is as above on the 14 days. I'm tempted to actually have the claim struck out as the claim remains stayed open ended. Has this happened to anyone before ? Thanks -

Hi. Wondered if someone could help with my ET please. I am doing this alone so any help would be very much appreciated. My complaint is quite long so Ill just keep the headlines. In reality I was made redundant due to a breakdown in work relationships. My notice of dismissal and paperwork shows I was dismissed because of redundancy. My role was still in existance and therefore my argument is that I could not have been made "redundant". I was given redundancy pay. I submitted my ET claim for unfair dissmissal. The organisation sent a load of gumpf back. Most of which doesn't seem relevent and I think is designed to confuse but they have put: "The reason for dismassal was redundancy which is a potebtially fair reason under section 98(2) of the employment rights act 1996. Without prejudice and as alternative to the above the claimant was dismissed for "some other substantial reason" which is potentially fair reason under section 98 (1)(b) of the employment rights act 1996". Can I just check that I have understood this please? Part 2 states they can dismiss me for: A. capability, B. conduct, C. redundancy or D. because of law/regulations And Part 1b says they can dismiss me for any of these reasons or for any other "substantial" reason. They stated they have dismissed me for 2c (redundancy). All my paperwork says 2c. They can't now say it was for another reason as per part1b can they? Surely then it would not have been redundancy and they would have put "dismissal due to break down in relationships" or sonething to that effect on my paperwork? I'm getting myself worked up that I'm missing something. As an aside, I may have to start using "without prejudice and as alternative to the above" as an argument! Also - they are not abiding by deadlines. We were meant to have exchanged our document list by last Thursday and I still haven't received theirs. Is there much I can do about that? Thank you.

Hi. Wondered if someone could help with my ET please. I am doing this alone so any help would be very much appreciated. My complaint is quite long so Ill just keep the headlines. In reality I was made redundant due to a breakdown in work relationships. My notice of dismissal and paperwork shows I was dismissed because of redundancy. My role was still in existance and therefore my argument is that I could not have been made "redundant". I was given redundancy pay. I submitted my ET claim for unfair dissmissal. The organisation sent a load of gumpf back. Most of which doesn't seem relevent and I think is designed to confuse but they have put: "The reason for dismassal was redundancy which is a potebtially fair reason under section 98(2) of the employment rights act 1996. Without prejudice and as alternative to the above the claimant was dismissed for "some other substantial reason" which is potentially fair reason under section 98 (1)(b) of the employment rights act 1996". Can I just check that I have understood this please? Part 2 states they can dismiss me for: A. capability, B. conduct, C. redundancy or D. because of law/regulations And Part 1b says they can dismiss me for any of these reasons or for any other "substantial" reason. They stated they have dismissed me for 2c (redundancy). All my paperwork says 2c. They can't now say it was for another reason as per part1b can they? Surely then it would not have been redundancy and they would have put "dismissal due to break down in relationships" or sonething to that effect on my paperwork? I'm getting myself worked up that I'm missing something. As an aside, I may have to start using "without prejudice and as alternative to the above" as an argument! Also - they are not abiding by deadlines. We were meant to have exchanged our document list by last Thursday and I still haven't received theirs. Is there much I can do about that? Thank you. -

I have response from Cabot to my CCA request. This is for Barclays loan (36K) which they bought in 2010. they do not have information on file and have requested said documents from original lender. they acknowledge the 12 day time limit but state they hope to comply with my request in 40 days, if the unlikely event that cannot obtain the information after 40 days, they will write again. original loan was 42K - do i sit tight and see if they produce documents or go for a silly F&F to clear up the matter on the basis they may take something now, in the event they do find the documents it may cost me a lot more in the long run ?

-

I send CCA to all my debtors, I have reply from Westcot advising that they are not the creditor but collecting on behalf of Cabot and that i need to either resend to them with postal order made payable to Cabot for forwarding or send direct to Cabot. 2 questions 1. shall I send direct to Cabot or go via Westcot 2. I read on other persons post a reply that said Cabot do NOT collect enforceable debt, I would really appreciate confirmation of this, as Cabot are collecting the largest debt i have, Barclays Loan, still awaiting a response to CCA for this one, although Cabot already replied to another debt advising they will no longer pursue chasing payment. thanks

-

This is what I received back from cca the dca, I hope ive included what I should img003[22].pdf

-

Barclaycard response below: I will only post the important bits We refer to your request for documentation under Section 78 of CCA 1974, we need to advise you that , regrettably, we are currently unable to fulfill your request. As such, we are not currently able to enforce our agreement with you and the agreement will remain unenforceable until such time as we are able to fulfill your request. what this means for you whilst discussions continue, we know that we're not able to enforce our agreement with you, but our rights continue to exist under the agreement. your balance is £3,731 and you will need to continue payments, blah blah blah. it is important to note that, where debt has accrued on your account, we will, where required, report to credit ref agencies, demand payment blah blah blah. they acknowledge delay in responding and accept that they are therefore prevented from enforcing our agreement they di however very kindly enclose a copy of short form cancellation and historic terms and conditions - why would I want those, lol next action - IGNORE and see this as a winner ??

-

Further to a cca request to Lowell, see my other post (do not know how to link posts) I have received the following: Dear Mr ******* your request for further information we refer to your recent request for further information regarding this account further to our letter dated 20th October 2017, please fine enclosed your returned fee of £1 in regards to your request for information under the consumer credit act 1974. at top of letter - its shows OC which was M&S store card it quotes the original account number and Lowell reference number and a BALANCE of £0 (was around 3K) I have no other letter, so not sure what they are referring to when they say 'further to our letter dated 20th Oct" It looks like a winner to me but shall i contact to see if there is another letter that i have not received, am thinking they may have sold it and that is why they show 0 balance thanks

-

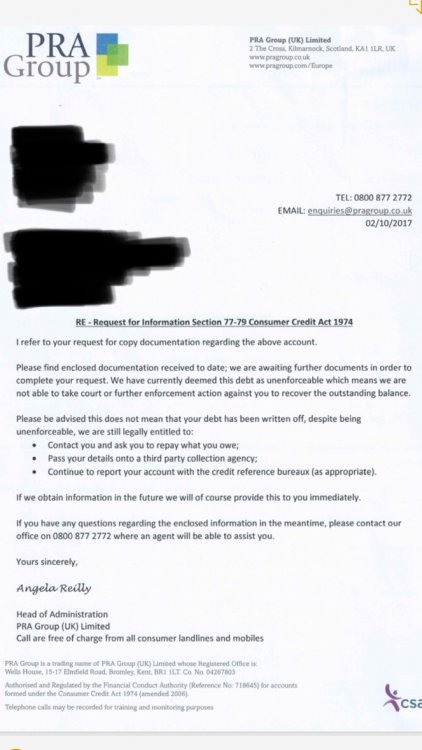

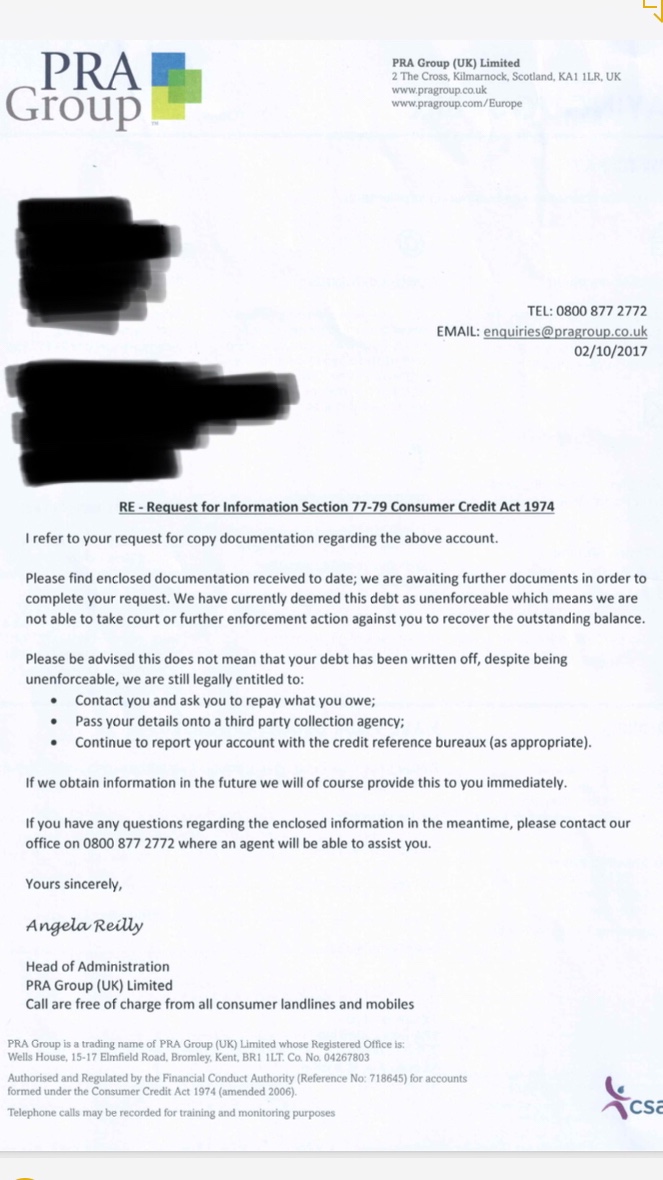

Hi there, My wife and I have unfortunately gotten ourselves into around £20,000 of debt. I recently wrote to the agencies sending out letters using the template to ask for the signed credit agreement. We have received this back from PRA GROUP. Could someone possibly give us some advice on what we need to do next Thank you Here

-

Hello, I rented a studio over 4 years ago through a London Agent; standard AST. The Agent secured my deposit (over £1000) with TDS. After one year my LL decided she did not need the agent anymore and offered to rent the flat directly to me. This, according to her, saved her some money to proceed with the needed repairs. I have been renewing contract (no changes in there) for the consecutive 3 years since then. Due to her numerous failures to carry out repairs (leaks, mold, poor insulation, lack of heating - literally she removed electric heaters from the walls to make the flat look bigger, fuse box issues - lights tripping out the box on a daily basis, boiler issues, shower power issues plus criminals next door, with their drug-related behaviour 24/7), I had enough and decided to move out, ending the contract in 2017. I gave her 2 months notice, but according to the contract I did not have to. She was extremely unhappy with my decision. On the same day she gave my private phone number to an Estate Agent; without permission&behind my back. They informed me that my LL decided to sell the flat and they would need immediate access to take pictures and show the property to potential buyers. I was speechless. I looked at my contract only to find out that she was in breach. The contract states that if the LL intends to sell the property, the tenant must be informed in writing 2 months prior the notice of intention to sell. Anyway, for the 2 months I have been harassed by my LL and Estate Agent so much, I had to take sick leaves as I was not able to perform my duties at work (she had known that I work nights only). On the day of my move she broke into the property (the police were called by my neighbours) and changed the locks. It's been over one month now and she does not reply to my requests for the return of my tenancy deposit. To cut the story short, when the new AST was up in 2016, she delayed it until the next month. She claimed that because of her delays in paperwork my deposit was protected for the time being as periodic, but she would protect it in full once the contract was signed. In 2016 I did not receive any reminder from TDS that the fixed term was ending and that action was required so that protection of the deposit continues ( this is what they say when asked about clarifying whether a LL complies with their rules). In the middle of my 2016-2017 tenancy I checked TDS (I had no reference number, nothing regarding the full AST deposit protection scheme from her). The only way I could check my deposit was by inputting the start date of the tenancy and full name on their website. The TDS could not find my deposit. I asked my LL about it and she said, blushing and stammering, that the deposit was in her account. I was at my wit's end so I tried to find my deposit with a reference number on periodic one. It turned out it's been periodic. My contract for the year 2016-2017 was not periodic. The previous deposit protection was fully registered and says: Tenancy start xx/xx 2015. Expected to end on or after xx/xx/2016. Can anyone advise how I pursue TDS and my LL about this? All advice/experience with LLs and TDS much appreciated. Thank you

Hello, I rented a studio over 4 years ago through a London Agent; standard AST. The Agent secured my deposit (over £1000) with TDS. After one year my LL decided she did not need the agent anymore and offered to rent the flat directly to me. This, according to her, saved her some money to proceed with the needed repairs. I have been renewing contract (no changes in there) for the consecutive 3 years since then. Due to her numerous failures to carry out repairs (leaks, mold, poor insulation, lack of heating - literally she removed electric heaters from the walls to make the flat look bigger, fuse box issues - lights tripping out the box on a daily basis, boiler issues, shower power issues plus criminals next door, with their drug-related behaviour 24/7), I had enough and decided to move out, ending the contract in 2017. I gave her 2 months notice, but according to the contract I did not have to. She was extremely unhappy with my decision. On the same day she gave my private phone number to an Estate Agent; without permission&behind my back. They informed me that my LL decided to sell the flat and they would need immediate access to take pictures and show the property to potential buyers. I was speechless. I looked at my contract only to find out that she was in breach. The contract states that if the LL intends to sell the property, the tenant must be informed in writing 2 months prior the notice of intention to sell. Anyway, for the 2 months I have been harassed by my LL and Estate Agent so much, I had to take sick leaves as I was not able to perform my duties at work (she had known that I work nights only). On the day of my move she broke into the property (the police were called by my neighbours) and changed the locks. It's been over one month now and she does not reply to my requests for the return of my tenancy deposit. To cut the story short, when the new AST was up in 2016, she delayed it until the next month. She claimed that because of her delays in paperwork my deposit was protected for the time being as periodic, but she would protect it in full once the contract was signed. In 2016 I did not receive any reminder from TDS that the fixed term was ending and that action was required so that protection of the deposit continues ( this is what they say when asked about clarifying whether a LL complies with their rules). In the middle of my 2016-2017 tenancy I checked TDS (I had no reference number, nothing regarding the full AST deposit protection scheme from her). The only way I could check my deposit was by inputting the start date of the tenancy and full name on their website. The TDS could not find my deposit. I asked my LL about it and she said, blushing and stammering, that the deposit was in her account. I was at my wit's end so I tried to find my deposit with a reference number on periodic one. It turned out it's been periodic. My contract for the year 2016-2017 was not periodic. The previous deposit protection was fully registered and says: Tenancy start xx/xx 2015. Expected to end on or after xx/xx/2016. Can anyone advise how I pursue TDS and my LL about this? All advice/experience with LLs and TDS much appreciated. Thank you -

As attached are my docs from Creation creation33.pdf

As attached are my docs from Creation creation33.pdf -

I took out a Unsecured Personal Loan with Halifax online in December 2011. I was NEVER asked questions like, can you afford the payments, are you employed/unemployed, and I certainly was not asked about my income. This have got so bad I am currently on an IVA - Halifax increased the IVA from 5 years to 6 years forcing me to pay for longer. I am now wondering if bankruptcy is the best option. Do I have a claim that Halifax lent to me irresponsibly without going through my finances first?

I took out a Unsecured Personal Loan with Halifax online in December 2011. I was NEVER asked questions like, can you afford the payments, are you employed/unemployed, and I certainly was not asked about my income. This have got so bad I am currently on an IVA - Halifax increased the IVA from 5 years to 6 years forcing me to pay for longer. I am now wondering if bankruptcy is the best option. Do I have a claim that Halifax lent to me irresponsibly without going through my finances first? -

Hi, After two notices from Indigo Park Solutions I have now received a letter from Wright Hassall Solicitors for failing to pay the Penalty Notice, and requiring me to make payment of £196. The letter states that failure to make payment in full or contact them to discuss repayment 'may result in us recommending to the Car Park Operator that the matter be enforced through criminal court proceedings. Such proceedings would require your attendance at a Magistrates Court.' Should I ignore this letter or reply, and if I need to reply what should I reply with? This is the first time Iv'e ever had to deal with anything like this!

Hi, After two notices from Indigo Park Solutions I have now received a letter from Wright Hassall Solicitors for failing to pay the Penalty Notice, and requiring me to make payment of £196. The letter states that failure to make payment in full or contact them to discuss repayment 'may result in us recommending to the Car Park Operator that the matter be enforced through criminal court proceedings. Such proceedings would require your attendance at a Magistrates Court.' Should I ignore this letter or reply, and if I need to reply what should I reply with? This is the first time Iv'e ever had to deal with anything like this! -

Received this in the post today Along with my original CCA letter. Any advice? I dont know what details they have as I have moved a number of times since then. If it was a credit card I would have thought capquest would have the details Just double checked on my Noodle account. It is listed in my closed accounts (if it is that one) and is shown as settled in Dec 2010 with no missed payments. Edit: it cant be that one on the account as my card limit was £1000 and have been paying £6.52 for years and my outstanding balance is shown as £1211.14 and the account is settled properly. Edit 2: Is it worth doing a SAR with CapQuest to see what they have on file and amounts?

-

Have received allocation of hearing and instructions to supply witness statements and documents to court by certain date. I am the claimant. I am trying to reply to the initial defence to the claim which is an absolute mess with disjointed emails. Ridiculous statements and allegations, referring to me that I have 'dementia' am also delusional, and paranoid" and asks the judge to take these abusive comments into consideration as I 'clearly don't know what time of day it is, never mind the truth'. The defendant has supplied a document which she refers to as an email sent to her In fact it is a 'chopped down' private message sent to someone else. The only way she can get access to this message is by either hacking my account or getting it from the person to whom it was sent. Reading more carefully her reason for supplying this is she now states that she sent it to the police in response to my allegation of theft of my property to which the case relates. I can actually see that she did as there is a police email address above. Now I have the full message, and it clearly is from me to someone else via a messaging system, not an email to her, and it is now obvious why she 'chopped' the message as the full message 'shoots her in the foot' so to speak. She has also denied, several times that events took place, highlighted for the judge in bold, and yet I have documented proof that these events took place as she admitted the same on paper. I am not sure how to respond to these issues in my witness statement. Should I bring them directly to the attention of the judge or just refer to them in my statement? How is the judge likely to view her deliberate deception, particularly sending a document that was never sent to her that she then sent to the police claiming it was from me to her, but she thenalso tampered with it? How is the judge likely to respond to her abusive comments that I have Dementia, am delusional and paranoid and that people with dementia cannot remember anything. Any comments would be helpful, thanks.

-

Hi For a while Arrow and now Drysden Fairfax have been irritating me with a Capital One CC account which was defaulted on. Taken out in 2001. Last payment approx 3 years ago. In May, I CCA'd them, eventually received the attached document. They say they've sent a Recon, quoting a high court decision in 2009. This document is all they sent, despite their letter saying that they have also sent a copy of the terms & conditions. Does not sending the accompanying t&c's mean it's failed CCA reply? More importantly, is the attached CCA enforceable? It's termed as an Application Certficate? Prescribed terms? (I'm not too clever on this aspect) Thoughts and advice appreciated. CR cap one recon cca.pdf

-

Hi everyone I sent some CCA a few months ago, some had copies some didnt. Moorgate have 2 of my credit cards and they couldnt find the CCA ...until now. It was an MBNA credit card i took out Theyve sent me a copy of my original agreement in 2003, its signed so i guess im still owing this one? As long as its a proper, signed copy i still owe it correct? thanks

-

We further requested recording / true copy of a particular transcript of telephone conversation giving date and exact time from a Loan Broker. Previously received some sort of print / scratchpad notes of conversation with SAR but important part of dialogue seems to have been omitted. Now my OH was told it was being recorded and she said that the person at the brokers was talking to her and typing up notes at same time. They have now refused our further request and stated that they are not obliged to provide any other format / CD or telephone call transcriptions. Can someone kindly confirm if this is correct ? Thank-you

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS