Showing results for tags 'westcot'.

-

Hello all, apologies if this is repeating other posters, but just needed some reassurance or additional advice: I was sc@mmed via an Ebay/Paypal seller. I sold a bike to a buyer, the payment was requested as bank transfer, however the buyer suggested using PayPal and all I needed to provide was my email for him/her to deposit the money to my PayPal account. The money was deposited, the bike collected (I didn't ask for a collection receipt as it wasn't a courier I had arranged). I removed the money from my PayPal account, and thought everything was good. Two days later, PayPal indicate that the the person who deposited the money didn't receive the bike and the money will be paid back. Now I am missing a bike and my PayPal account is negative £900. I argued strongly with PayPal, explaining the details of my case, supplied the CRN, all conversations with the buyer, etc, but with absolutely no joy. I haven't had any formal communication from PayPal about paying the debt, however, this week I started receiving communications from Westcot (2per day at present). Their number is blocked and I am making a log of their calls. My question is, how do I know if PayPal have sold my debt, or have they just instructed to recover it on their behalf? If they have sold the debt, am I legally obliged to pay it back? In my eyes I don't have a debt and it was PayPal's decision to give the money back from the process of an obvious [problem]. I am quite happy to go to court as I believe PayPal are assisting and allowing fraudulent transactions to take place. It is apparent their security is flawed, and I would love to fight this, I'm just concerned that if PayPal sold the debt that they created then I am tied in to paying Westcot which clearly I don't want to do. Any advice on this would be very much appreciated. Clearly I haven't disclosed all details as its quite complex, but nonetheless I have been the victim of a this and PayPal facilitated this. Regards.

Hello all, apologies if this is repeating other posters, but just needed some reassurance or additional advice: I was sc@mmed via an Ebay/Paypal seller. I sold a bike to a buyer, the payment was requested as bank transfer, however the buyer suggested using PayPal and all I needed to provide was my email for him/her to deposit the money to my PayPal account. The money was deposited, the bike collected (I didn't ask for a collection receipt as it wasn't a courier I had arranged). I removed the money from my PayPal account, and thought everything was good. Two days later, PayPal indicate that the the person who deposited the money didn't receive the bike and the money will be paid back. Now I am missing a bike and my PayPal account is negative £900. I argued strongly with PayPal, explaining the details of my case, supplied the CRN, all conversations with the buyer, etc, but with absolutely no joy. I haven't had any formal communication from PayPal about paying the debt, however, this week I started receiving communications from Westcot (2per day at present). Their number is blocked and I am making a log of their calls. My question is, how do I know if PayPal have sold my debt, or have they just instructed to recover it on their behalf? If they have sold the debt, am I legally obliged to pay it back? In my eyes I don't have a debt and it was PayPal's decision to give the money back from the process of an obvious [problem]. I am quite happy to go to court as I believe PayPal are assisting and allowing fraudulent transactions to take place. It is apparent their security is flawed, and I would love to fight this, I'm just concerned that if PayPal sold the debt that they created then I am tied in to paying Westcot which clearly I don't want to do. Any advice on this would be very much appreciated. Clearly I haven't disclosed all details as its quite complex, but nonetheless I have been the victim of a this and PayPal facilitated this. Regards. -

Hi, I will try and explain the scenario that took place between my wife and PayPal as best I can. One morning, my wife was contacted via Facebook messenger by who she believed to be a colleague at her workplace. This was before Christmas and the colleague explained that her PayPal account had restrictions on it and asked if my wife could accept money into her PayPal account for items the colleague had sold to help with the cost of Christmas. Being the ever pleasing colleague she agreed. After the money appeared in my wife's PayPal account, she was instructed to then withdraw to her own bank account and then transfer the money to another bank account provided by the work colleague. This was all completed without any issues. She arrived at her work that morning to be told by her colleague that there was never any request to move money by her and that her Facebook account was hacked. There were two payments made in to my wife's account, both approximately £490 pounds. All money had passed through so we though it was very strange, maybe laundering, but just moved on as our own money wasn't at risk. A few days later however the second payment of £490 was declined, leaving my wife £490 down. We didn't really understand what happened but we assumed the account from which the funds were sent was either hacked as well or they were dodgy too. We contacted our bank to find out where the final destination of these funds went, and to log a case of fraud, but it was a German, online bank and they have yet to enter successfully into dialogue with our bank, so nothing is progressing. And we don't expect it to get anywhere. We now have the PayPal debt collection agency chasing her which we are not happy about. We are also not happy about the fact that no one at PayPal, the bank or any of the other fraud organisations is willing to look into the case in any more detail, despite this transpiring to be quite a common [problem]. Should we stick to our guns regarding this or will that be futile? Do Westcot and/or PayPal take these kind of things to court? Will this effect my wife's credit? I would also like to point out that all conversations that took place on Facebook etc have been recorded and ready to be shown to anyone who needs to see them.... Thanks in advance. James

-

Hi I have two ex Santander debts - £4k loan / £1400 cc which were in a Step Change DMP that ended in 2016. These debts are now being chased by Westcot. I received a letter for one of the debts on Saturday, and today Westcot have started calling me. I have not responded yet. I am aware of how aggressive Westcot are, Ive had previous dealings with them. The debts themselves are from around 2011. The letter from Westcot states they are looking for an 'affordable' payment plan. No mention of court has been stipulated yet. I really do not want to have to deal with Westcot again, as they made my life a misery last time. They have given me 10 days to respond. Would it be better to write to Santander instead? Or should I request that Westcot send me proof they can chase the debt? Many thanks in advance for any help. RJW

-

Hello, I am a new user here, writing to get advice on a Paypal Dispute of £700 This is how it went to westcot DCA (timeline); 1. It starts with me sending an iPhone to someone via Paypal. 2. I take out the money (£700) in the bank after i receive it and remove bank/card from Paypal 3. after 2 weeks he claims on PayPal that nothing has been received. 3. i didn't track hold of parcel receipts, so dispute case is LOST. 4. Paypal A/C Negative balance £700, received email from PAYPAL to pay in the amount 5. Since i have removed bank and card from paypal, they are unable to charge me. 6. I close the Paypal Account which is prob a wrong move ( it has my phone no. and address) 7. Start to receive phones from Paypal calls, which i have ignored for 2 weeks 8. Recently i received a call and letter from Westcot asking me to call back. 9. An Address verification letter received by Westcot asking to call back and tell if its Address is correct or not. They haven't mentioned the debt amount but I assume it to be much more than £700 now because of the legal expense of Westcott. I have not spoken to westcot as i read in other forums to not speak to them. I am scared as i am on a student visa here in UK and aim to work later on in the UK with work visa. Q. what do you think about Westcot taking action for £700 debt. (court or police) Q. What should i do actually do? I live in a private student accommodation (8 buildings and 1500 flats) and will change it after 3 months.. Q. Whats the worse westcot or paypal can do? Or should i just pay them back and consider my loss. Q Can it affect any future visa / gov. related track record of me? Please HELP!

-

Hi there all. I have a question regarding my account. I had a Virgin Money Account which I was paying off interest only for, for a significant time and one i had PPI on. I was paying minimum payment for some time which meant interest and charges only on it. My business failed earlier this year and I am only now coming out the other side with a salary again. The account has been sold to IDEM and noodle gives the following information. Idem Capital Securities £ 4,471 22/09/2014 Default Name nnnnn Address nnnnnnn Date of birth nnnnnnn Account type Credit Card Account number ******6888 0 Account start date 09/05/2008 Opening balance £ 4,471 Regular payment £ £ 1 Repayment frequency Monthly Date of default 28/02/2014 Default balance £ 4,471 I am now being contacted by Westcot about it daily and in letters. I would like some advice please. 1 - It seems I can still approach Virgin/MBNA about PPI and charges on this card as I believe i have a claim that may be valid. Do I contact westcot and advise them that I will be contacting them or not? 2 - What should be my next plan? I have no issue paying this debt off but i see all this stuff about CCA requests and SAR requests etc a nd I am not sure what I should do, I can ring them up and offer £200 a month not an issue. 3 - Do they have any legal right for me to disclose my financial details to them as in income and outgoings - i can see from other threads that IDEM seem to think that they are in their rights to ask lots however I don't know what westcot will want from me. Thanks in advance!

-

Hello, its been a while since i've been here. Just looking for some advice. An old Halifax debt which was being handled by DrydensFairfax Solicitors and which I have been paying at £5 a month for ever, it seems, has been passed by them to Westcott. I just wanted to know if it is reasonable to send a CCA request to them before I change where I send the payment?

Hello, its been a while since i've been here. Just looking for some advice. An old Halifax debt which was being handled by DrydensFairfax Solicitors and which I have been paying at £5 a month for ever, it seems, has been passed by them to Westcott. I just wanted to know if it is reasonable to send a CCA request to them before I change where I send the payment? -

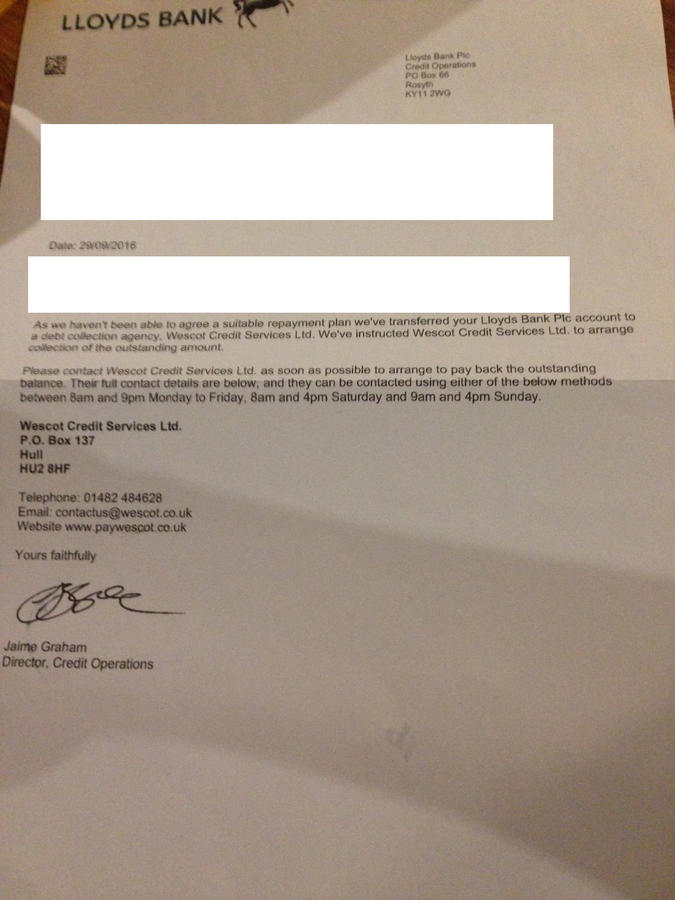

Hi, I am looking for some advice, I received the attached letter from Westcot and/or Lloyds in regards to an outstanding debt of just under £1000.00 I have in the past had a Lloyds credit card (at least over 4 years ago) and do not possess the statements or the card anymore. I do not recall leaving any outstanding debt on the card. I also received letters a few months ago from Moorcroft chasing this debt which I ignored as I thought it was fraudulent. I have not received any contact from Lloyds in regards to this debt, would they not contact me first? I am concerned this will ruin my credit rating but I am not even sure that I owe any debt… What would be the best course of action from here? Thanks

-

Debt from June 2002 £8,500 sold by Barclays to Arrow Global. I have been dealing with Capquest until Nov 2015, and paying £5 per month, when I asked for a copy of my agreement and had reply from Capquest in Feb 2016, saying account on hold whilst they request the documentation from Arrow. I heard nothing more until last week when I had a letter from Wescot asking if I was the person they referred to and to contact them. I did nothing. Then a letter today from Arrow saying that Westcot is now managing my debt and asking me to contact Wescot. Odd thing is I have always dealt via a friends address to avoid embarassment and the last two letters came to my address not my friends. What do i do?

-

RBS passing enforceable old debts to Westcot

Nomore Baloney posted a topic in Royal Bank of Scotland

My wife CCA'd the RBS regarding her credit card. They have sent back a copy of her application form (below) and a copy of a 7 page Credit Agreement. The copy of the credit agreement is unsigned (in fact there is nowhere on the agreement to sign) so I imagine if thats their best effort, the agreement is unenforcable. What do you think folks. -

Hi does anyone have any email contact details for he aqua credit card - i want to contact them about a debt I have with them and try and sort things out but they only supply a postal address or phone number on their site

-

Hi, I was hoping for a little help and advice please.. .. In 2009 I took out a Business Loan from Barclays for a business debt of £20,000. I have an signed Agreement and have been paying £230 per month ever since. I have never missed a single payment. Today I received a letter from Barclays saying that the debt had been transferred to Westcot and to contact Westcot to make arrangements to continue payments but this time direct to Westcot. I rang Barclays to see if I'd ever missed a payment and why it was going to Westcot, the lady was helpful and said I had never missed a payment but Barclays had sold a lot of accounts to Westcot.... My question is this, I know and have read about Westcot and I do not like what I have read and I don't trust them . I was happily paying off this loan and now this is tainted for me as I know where this will head... . CAN I DEMAND THAT BARCLAYS KEEP MY ACCOUNT AS I HAVE NOT DEFAULTED AND THERE SEEMS NO REASON WHY IT SHOULD HAVE GONE TO WESTCOT? Many Thanks for you time in advance. Q

-

Hello all I have been having a problem with O2 I defaulted on a phone contract . They have now passed it to Westcot. The contract was one of the newer contracts which gives you a contract for the phone and a separate agreement fro airtime . I am not denying the debt and want to pay O2 but they keep referring me to westcot. from the library I sent them the cca request and the reply have come back which I have uploaded . I just want so advice what to do next. Thanks Brian

-

Hello I'm hoping someone will be able to give me some advice. Last week I received 2 letters. The first was from BCW asking for me to verify my address and that they needed to communicate with me about a 'private matter'. I subsequently received a letter with a Barclays letter head stating that a debt (£1900) with them had been transferred to BCW and that I should now pay this in full. No breakdown of the debt was provided but an old current account number was quoted. I did hold an account with Barclays until 2004 when I switched to the Coop Bank. I moved address at the same time and so have not received any further statements or correspondence from Barclays since then. From memory I am sure that I instructed Barclays to close the account in 2004 but I don't recall if this was done by telephone or letter. I don't have copies of correspondence from this time. It's clear from other threads that I should avoid telephone contact with BCW. I need to know how they/Barclays reach the figure of £1900. It seems possible that Barclays left the account open. If that happened there may have been one or two small standing orders to charities which I forgot to cancel and which have simply accumulated over the last 10 years. What should I do now? Presumably Barclays will have to provide me with statements over the last 10 years to show me how this debt has built up. Can I ask them to let me have this bearing in mind that BCW are asking for all communication to go through them? Also, would there have been any onus on Barclays to contact me when it became clear that the account was inactive - no income going in, no cash withdrawals, just possibly 1 or 2 standing orders? And would they have been able to keep renewing the annual overdraft without my agreement? Any help on what to do would be much appreciated.

-

Hi, I was self employed but my business now makes very little with just a few hundred a month coming in. 9 months ago my wife and I sold our house (which had a joint mortgage) and bought a cheaper house in her name. We used the profit to pay off some debts but I'm still left with about £30k debt on credit cards and an unsecured loan. (which I haven't paid for about 7 months) After my wife has paid the mortgage she's left with about £600 a month for the other bills eg community charge, utilities etc so there's not much, if anything , left to pay my debts off. I'm 60 but hoping to develop a new business which may bring some money in. Also, my mother died last week and I'll receive a small inheritance of around £2000. Other than that I have no assets or car. I've included a more detailed breakdown below but any advice would be very welcome. 1 Is it really worth asking for the original credit card agreements? I've read elsewhere that they don't need to be original to recover the debts. Also, do I have to send letters to both Westcot and Barclaycard? 2. We no longer have any joint accounts. Will my wife be held responsible for my debt problems and do I have to declare her income if it goes to a ccj? 3 They've added late payment charges for the last 7 months or so. Can these be reclaimed and if so, how do I go about it? Lastly, I can't access the library though I registered a few years ago. Personal Barclaycard started in 2001 £1877 Barclaycard started in 1994 £12005 Barclaycard started in 1994 £9940 Opus started in 1996 £1067 Nationwide started in 2014 £1890 Aqua card started in 2014 £Zero Barclays overdraft £1300 Total £28k Business Barclaycard £4500 Unsure when it began as its not listed in Noddle Unsecured Business Loan Barclays £1200

Hi, I was self employed but my business now makes very little with just a few hundred a month coming in. 9 months ago my wife and I sold our house (which had a joint mortgage) and bought a cheaper house in her name. We used the profit to pay off some debts but I'm still left with about £30k debt on credit cards and an unsecured loan. (which I haven't paid for about 7 months) After my wife has paid the mortgage she's left with about £600 a month for the other bills eg community charge, utilities etc so there's not much, if anything , left to pay my debts off. I'm 60 but hoping to develop a new business which may bring some money in. Also, my mother died last week and I'll receive a small inheritance of around £2000. Other than that I have no assets or car. I've included a more detailed breakdown below but any advice would be very welcome. 1 Is it really worth asking for the original credit card agreements? I've read elsewhere that they don't need to be original to recover the debts. Also, do I have to send letters to both Westcot and Barclaycard? 2. We no longer have any joint accounts. Will my wife be held responsible for my debt problems and do I have to declare her income if it goes to a ccj? 3 They've added late payment charges for the last 7 months or so. Can these be reclaimed and if so, how do I go about it? Lastly, I can't access the library though I registered a few years ago. Personal Barclaycard started in 2001 £1877 Barclaycard started in 1994 £12005 Barclaycard started in 1994 £9940 Opus started in 1996 £1067 Nationwide started in 2014 £1890 Aqua card started in 2014 £Zero Barclays overdraft £1300 Total £28k Business Barclaycard £4500 Unsure when it began as its not listed in Noddle Unsecured Business Loan Barclays £1200 -

Hi, This is my first post but I have been looking around on here recently as have been seeking some advice. I haven't been able to find a post similar enough to mine to get an answer so I'm going to tell you about my troubles in hope someone can steer me right! I took out a Barclays Career Development Loan back in 2007. The company I took it out to train with then soon went out of business - I'm sure some of you would've heard of them. 'Connectivity IT Training' based in Docklands, London. I telephoned Barclays after I'd found out to then be told, Ok that's fine, we will take today as your course end date and you can start paying it back. How considerate of them. I made a few payments but seeing as I was on a CDL course, I obviously had no job or low pay. I stopped being able to make payments and the letters stopped coming through. Fast forward to the present day. I moved away from my Mums (I've lived at 7 addresses since then, my most recent has been just under 5 months). At the end of Dec I received a phone call from Westcot asking me if I was me. I was surprised as I have no other outstanding debt (none that would be referred to a collection agency) and as I do get a lot of junk calls I said no. The lady said she would remove my number from their system, end of. I didn't have that number when I signed for the CDL so no idea how they had gotten it. On the 2nd of Jan I received a lovely letter from them to my NEW address. Sent to my name, telling me they are attempting to contact me and that I need to confirm if it's me or not living here before the 12th of Jan or else they will assume the contact information they hold for me is correct. Now if I didn't indeed live here then I would have gotten this letter addressed for someone other than myself and not opened it just binned it and they couldn't assume that I live here etc. I have switched EVERYTHING to this address as I have moved away from the area I used to live in and it's not convenient to pick up post from my parents anymore. I did switch to other addresses I've lived at recently too and they are all previous addresses showing on my Noddle credit report. I could be on the wrong track here and thinking that this is for the Barclays CDL when it isn't however theres nothing else it can be in my opinion. Everything else is paid up to date and I've never missed a payment on anything, ever either. I am also aware that by the middle of this coming November, the loan will be 6 years with no payment or contact so will be 'Statute Barred'. The date of default displays Nov 2009. I'm guessing they are aware of this and trying to get me now before the deadline. Total outstanding is around £8600. I am not in a position to repay this as my girlfriend isn't working (on SMP as we have just had a baby and I am covering all the bills and trying to repay an old credit card which was at £8500 and now down to £5500). Is there anything I can do or anything you can suggest to me? I have no experience with Debt Collection agencies and I also don't want to have any experiences with them! Thank's a lot for reading.

Hi, This is my first post but I have been looking around on here recently as have been seeking some advice. I haven't been able to find a post similar enough to mine to get an answer so I'm going to tell you about my troubles in hope someone can steer me right! I took out a Barclays Career Development Loan back in 2007. The company I took it out to train with then soon went out of business - I'm sure some of you would've heard of them. 'Connectivity IT Training' based in Docklands, London. I telephoned Barclays after I'd found out to then be told, Ok that's fine, we will take today as your course end date and you can start paying it back. How considerate of them. I made a few payments but seeing as I was on a CDL course, I obviously had no job or low pay. I stopped being able to make payments and the letters stopped coming through. Fast forward to the present day. I moved away from my Mums (I've lived at 7 addresses since then, my most recent has been just under 5 months). At the end of Dec I received a phone call from Westcot asking me if I was me. I was surprised as I have no other outstanding debt (none that would be referred to a collection agency) and as I do get a lot of junk calls I said no. The lady said she would remove my number from their system, end of. I didn't have that number when I signed for the CDL so no idea how they had gotten it. On the 2nd of Jan I received a lovely letter from them to my NEW address. Sent to my name, telling me they are attempting to contact me and that I need to confirm if it's me or not living here before the 12th of Jan or else they will assume the contact information they hold for me is correct. Now if I didn't indeed live here then I would have gotten this letter addressed for someone other than myself and not opened it just binned it and they couldn't assume that I live here etc. I have switched EVERYTHING to this address as I have moved away from the area I used to live in and it's not convenient to pick up post from my parents anymore. I did switch to other addresses I've lived at recently too and they are all previous addresses showing on my Noddle credit report. I could be on the wrong track here and thinking that this is for the Barclays CDL when it isn't however theres nothing else it can be in my opinion. Everything else is paid up to date and I've never missed a payment on anything, ever either. I am also aware that by the middle of this coming November, the loan will be 6 years with no payment or contact so will be 'Statute Barred'. The date of default displays Nov 2009. I'm guessing they are aware of this and trying to get me now before the deadline. Total outstanding is around £8600. I am not in a position to repay this as my girlfriend isn't working (on SMP as we have just had a baby and I am covering all the bills and trying to repay an old credit card which was at £8500 and now down to £5500). Is there anything I can do or anything you can suggest to me? I have no experience with Debt Collection agencies and I also don't want to have any experiences with them! Thank's a lot for reading. -

Need some help on this one as I have done lots of searching and can not find a case that is similar to mine so would appreciate some guidance. Brief Summary: 29/04/2011 - I defaulted on a HSBC Current account overdraught with an outstanding balance of £1780.09 (which was mostly my own debt and not made up of charges/interest) 16/04/2012 - after being pursued for the debt for months (with no acknowledgement from myself) I was offered a reduced settlement figure of £1,068.05 (60% of original balance) from Westcot Credit Services LTD at which point I decided I had enough of burying my head in the sand and I coughed up and paid via their website in full. This payment is the only contact I have had with any DC at all. 29/01/2013 - I start receiving letters from MKDP/Raven/Compello demanding payment for £712.04 which just so happens to be the difference between the original balance and the reduced settlement figure. I ignore these letters because I believed they were just trying to spoof me into paying more money. As far as I am concerned I have acknowledged the debt (with Westcot) and paid in full and final settlement to close the account. The Default on my CR also changed from HSBC to MKDP a few months after this. 16/04/2014 - To my horror a Claim From from Northhampton CCBC landed on my door step the morning claiming payment of £712.04 + £55 costs. The claim form is dated 11/04/2014 I intend to dispute the whole claim on the basis that I have already settled this debt with a previous claimant and they are essentially, and wrongfully pursuing a debt that does not exist and that they have no claim to. The main issue I have is that due to a recent house move I no longer have any of the letters from Westcot or MKDP etc. In particular I can't find the original letter offering the reduced settlement offer from Westcot. I do have receipt for the payment however. I also need help in wording a suitable defence, taking into account the above as I have no idea where to start. Your help is very much appreciated.

Need some help on this one as I have done lots of searching and can not find a case that is similar to mine so would appreciate some guidance. Brief Summary: 29/04/2011 - I defaulted on a HSBC Current account overdraught with an outstanding balance of £1780.09 (which was mostly my own debt and not made up of charges/interest) 16/04/2012 - after being pursued for the debt for months (with no acknowledgement from myself) I was offered a reduced settlement figure of £1,068.05 (60% of original balance) from Westcot Credit Services LTD at which point I decided I had enough of burying my head in the sand and I coughed up and paid via their website in full. This payment is the only contact I have had with any DC at all. 29/01/2013 - I start receiving letters from MKDP/Raven/Compello demanding payment for £712.04 which just so happens to be the difference between the original balance and the reduced settlement figure. I ignore these letters because I believed they were just trying to spoof me into paying more money. As far as I am concerned I have acknowledged the debt (with Westcot) and paid in full and final settlement to close the account. The Default on my CR also changed from HSBC to MKDP a few months after this. 16/04/2014 - To my horror a Claim From from Northhampton CCBC landed on my door step the morning claiming payment of £712.04 + £55 costs. The claim form is dated 11/04/2014 I intend to dispute the whole claim on the basis that I have already settled this debt with a previous claimant and they are essentially, and wrongfully pursuing a debt that does not exist and that they have no claim to. The main issue I have is that due to a recent house move I no longer have any of the letters from Westcot or MKDP etc. In particular I can't find the original letter offering the reduced settlement offer from Westcot. I do have receipt for the payment however. I also need help in wording a suitable defence, taking into account the above as I have no idea where to start. Your help is very much appreciated. -

Hey oop. Rusty ol' me passing through, helping someone and I'm pondering on best course of action (not helped by lack of docs from the OP). C/C debt passed from OC to DCA to another DCA, then returned to 1st DCA. Last contact was in 2009 or 10. Suddenly, N1 appeared, lodged by Drysden, of course. OP has no recollection of ever getting a default notice, assignment or anything like that. I've told him to acknowledge for now while I refresh my memory, but I am dithering on where to best handle it. I am thinking: - contact Arrows with CCA request. I am 99% sure that there will not be compliant paperwork, the CC was obtained in 1996 or 7, so odds of a valid contract existing are I think highly improbable. Even if by miracle it still exists, the odds of it having all the required elements and being legible etc is just as remote, IMO. - request paper trail: default notice, assignment. The POC is very generic and vague and does not mention any date at which the notices were supposedly sent to OP, which make me suspicious, in the past, when I have been hounded, if they had followed the paper trail properly, they would say so straight away. - defence: putting claimant to strict proof of, well, pretty much everything: the amounts, assignment, etc. What annoys me is that at some point, the debt became SB then one of the DCAs managed to scare OP into starting payment anyway (he didn't know anything about these illegal tactics)... The aim is either to get the claimants to see they won't get an easy ride of it a nd that this is one defendant which won't go down quietly, a nd hopefully discontinue sooner rather than later. If that doesn't work, then make sure that them chasing after a debt which became toxic a long time ago costs them a lot of money and work by the time OP gets to court. Any opinions, advice, have I missed an obvious trick? Fire away and thank in advance.

-

Hi Guys, sorry if I'm posting this in wrong forum! I have an old business loan with £15,000 outstanding. However, the business went bust a in Dec 2012 and was Dissolved. I sent Westcot who are attempting to collect for Hoist Portfolio Holdings who bought the debt from Lloyds. I sent them request for True Signed copy etc, they responded two months later with the wrong material. I replied saying that if they couldn't supply it they were in default and had no recourse, using standard letters quoting Consumer Credit Act etc. However, they have now written back saying as it was Business Loan for which I had signed a Personal Guarantee, the Consumer Credit Act stuff doesn't apply. I have 30 days to respond with a plan for repayment or challenge further. I can scan letters if need be, any help much appreciated, as I simply don't have the money to pay them, I'm on the breadline as it is! Thanks. Urban Stealth

Hi Guys, sorry if I'm posting this in wrong forum! I have an old business loan with £15,000 outstanding. However, the business went bust a in Dec 2012 and was Dissolved. I sent Westcot who are attempting to collect for Hoist Portfolio Holdings who bought the debt from Lloyds. I sent them request for True Signed copy etc, they responded two months later with the wrong material. I replied saying that if they couldn't supply it they were in default and had no recourse, using standard letters quoting Consumer Credit Act etc. However, they have now written back saying as it was Business Loan for which I had signed a Personal Guarantee, the Consumer Credit Act stuff doesn't apply. I have 30 days to respond with a plan for repayment or challenge further. I can scan letters if need be, any help much appreciated, as I simply don't have the money to pay them, I'm on the breadline as it is! Thanks. Urban Stealth -

I'm thinking Westcot have purchased a bulk load of debt from someone as yesterday I got a lovely text from them asking me to contact them urgently (ha yeah thats going to happen) then today I got a phonecall asking me to contact them urgently (see previous response), I would like to thank them for using phone numbers that displayed they are now on barred caller list. And I know that there is no debt on my credit file (last checked yesterday after text message) Also know that my last trouble with debt was Sky TV over 9 years ago, and last ever contact with Lowells was for capital one debt which was 14 years old. Its pretty obvious that they have no address for me as there is no letters or that they dont have my landline. ohhh well better luck next time westcot

-

Hi i am hoping someone can help or at least point me in the right direction. Back in 2008-09 i went through a really difficult period, i was laid off work due to sickness and my relationship ended so with various bills an no income i found myself in a mess. I contacted all my debtors to arrange a payment plan but egg credit card weren't interested in letting me pay what i could afford, i managed to pay token amounts but then i couldn't keep up with this, they defaulted the account, then i didn't hear anything until i received a letter from Bryan Carter, they asked me to pay a chunk of the debt to stop it going to court, i wasn't in a position to do this so they sent the forms and i made an offer to pay of £20 month, being naive at this time i didn't actually realise the conseqence of what was about to happen, ie a CCJ being registered. ....so annoying as i would have asked my parents for help had i known. i have been paying £20 month since the CCJ was registered 22/7/09 until June this year, i rang BC to change the payment date an they informed me the debt was no longer with them and that i would hear from Westcot in due course. No contact until 12.9.13 with the headline 'failure to make payment' saying despite their letter of 28th August i have failed to make a payment or enter into an agreed plan, unless i contact them urgently to make a payment or to establish a regular repayment plan they will have no option but to recover the debt, this will be either: Legal action through the court and judgement obtained against me (haven't they already done this)? Refer the debt to a door stop collections agency. what i want to know is it worth me asking for a full statement of the account before it was taken to court, after reading these forums i am sure there will be charges that were applied that i could possibly claim back!? What will happen in 2 years (when the CCJ falls off credit report) i am sure unless i find myself with a windfall i will still be paying this debt, i don't have a problem paying what i owe when they are genuine charges. I also have 2 other debts that are still not resolved that are with HSBC so hoping some kind person may advise me on these also. Thank you for taking the time to read, any constructive advice is very welcome

-

Hi New member hoping for some advice I took a loan out with natwest in 2005-6 ,i lost my job 2007 , carried on paying by selling things and they wouldn't reduce payments even though they knew i was unemployed . Eventually they did after i visited the c.a.b. They set me up paying £1 per month direct but eventually natwest said that wasn't enough and passed it on to moorcroft who i was then paying £5per month to. After a while i noticed the natwest balance statement was about 600 less than the moorcroft's. I queried this with moorcroft they did nothing ,so i queried it with natwest and they said that i'd agreed when i went through the c.a.b. to pay all the account charges for when i was going overdrawn (when i first lost my job and for the 8mths or so i was still trying to pay the full loan payments) Eventually Natwest decided "as a good will gesture" to knock off around £230 of these charges. So i carried on paying moorcroft 5 per month which i couldn't really afford (at one point they put it up to £10 per month!) then in november/december last year i decided i was tired of their threatening letters and trying to get me to increase payments so stopped paying them. Shortly after this i moved house to a new address and though i haven't received any letters from natwest at this address , i have received many threatening letters from Westcot , the latest of which threatening to make doorstep visits via "credit security" (the letter is also titled "DOOR STEP COLLECTION NOTICE" and their balance shows the higher amount by around £450 than what a letter apparentley sent to from my old address from Natwest shows . I didn't notify natwest of my address change . I have not responded to either,haven't returned westcots letters or anything over last 3mths. Unsure what to do as i've been unemployed since 2007 and this financial year now have to pay £17 per month more towards council tax. Should i write to westcot and offer a couple of quid a month or write to natwest and refuse to deal with westcot? i've tried looking around on here but i'm not a good reader and struggling to find where to start. Any advice appreciated thanks Norman

-

Hi, My mother owes Lloyds TSB £4,000 for a Credit Card and £6,500 for a Bank Account. She moved to Ireland in September 2012 to retire as my father has alzheimer's disease, and it's a better quality of life over there. She has high blood pressure and suffers from stress which Lloyds TSB are aware of. I'm a student studying at University and have promised to help her deal with the constant letters to try and reduce her stress levels. The letters are being re-directed by Royal Mail from our old address to my University address. She has not informed Lloyds TSB or Westcot that she has moved abroad, as I don't want any letters being sent to her, so I'm trying to deal with them myself but have got confused about what to do next. I believe her debt issues started around 13 years ago. During May 2013, I sent Lloyds TSB an Income & Expenditure form and agree a payment of £1/month, however as I had exams during this time I completely forgot to set this up. On 26th July 2013, Lloyds TSB passed both debts over to Westcot and I have received a number of letters from them since for both debts. The first was a 'Notice of Debt Collection' and the second a 'Final Notice' threatening further action on 11th August 2013. The 'Final Notice' stated that after investigating they have confirmed that my mother still lives in the old property, however this is not true. I have not contacted Westcot as of yet. A few weeks ago, Lloyds TSB sent me some statements after speaking to them on the phone. One shows a number of payments from 07/10/2010 to 06/08/2012 of £28 per month. The other was on some paper that looked dated, with some statements dated from the year 2000. What should I do next? Thanks

Hi, My mother owes Lloyds TSB £4,000 for a Credit Card and £6,500 for a Bank Account. She moved to Ireland in September 2012 to retire as my father has alzheimer's disease, and it's a better quality of life over there. She has high blood pressure and suffers from stress which Lloyds TSB are aware of. I'm a student studying at University and have promised to help her deal with the constant letters to try and reduce her stress levels. The letters are being re-directed by Royal Mail from our old address to my University address. She has not informed Lloyds TSB or Westcot that she has moved abroad, as I don't want any letters being sent to her, so I'm trying to deal with them myself but have got confused about what to do next. I believe her debt issues started around 13 years ago. During May 2013, I sent Lloyds TSB an Income & Expenditure form and agree a payment of £1/month, however as I had exams during this time I completely forgot to set this up. On 26th July 2013, Lloyds TSB passed both debts over to Westcot and I have received a number of letters from them since for both debts. The first was a 'Notice of Debt Collection' and the second a 'Final Notice' threatening further action on 11th August 2013. The 'Final Notice' stated that after investigating they have confirmed that my mother still lives in the old property, however this is not true. I have not contacted Westcot as of yet. A few weeks ago, Lloyds TSB sent me some statements after speaking to them on the phone. One shows a number of payments from 07/10/2010 to 06/08/2012 of £28 per month. The other was on some paper that looked dated, with some statements dated from the year 2000. What should I do next? Thanks -

Hi All, Firstly thanks for this site, I have been a long time lurker ! Long story short i have some debts i am trying to get settlements on that have defaulted within last 12 months. This one, the balance was over £17K - a credit card with my bank. I asked to settle at 30%, did an I+E, and after 2 weeks the answer came back - OK. Had to pursue them to get this in writing and after 2 previous unsatisfactory versions have received this final version. Is this ok to settle on? Don't have cheques or 3rd party so planning to pay via Bank transfer. Spoke to bank and they say they have passed the debt to Westcot to collect, but they stoll own it. Told me to deal with Westcot. 1: Is this letter OK>? 2: Should I pay Wescot or the bank direct? many thanks all blotter

Hi All, Firstly thanks for this site, I have been a long time lurker ! Long story short i have some debts i am trying to get settlements on that have defaulted within last 12 months. This one, the balance was over £17K - a credit card with my bank. I asked to settle at 30%, did an I+E, and after 2 weeks the answer came back - OK. Had to pursue them to get this in writing and after 2 previous unsatisfactory versions have received this final version. Is this ok to settle on? Don't have cheques or 3rd party so planning to pay via Bank transfer. Spoke to bank and they say they have passed the debt to Westcot to collect, but they stoll own it. Told me to deal with Westcot. 1: Is this letter OK>? 2: Should I pay Wescot or the bank direct? many thanks all blotter -

at the start of the month i received a claim from from Northampton court, the particulars where as follows The claim is £xxxx being monies owing to the claimant in respect of a credit agreement between Llloyds Tsb and the defendant under account no xxxxxxxxxxxxxxx The agreement was terminated as the defendant failed to maintain the agreed terms in accordance with the pre action protocols the claimant has attempted to contact the defendant and agree and repayment plan the defendant has failed to respond or maintain a suitable agreement and the balance of £xxxx remains due and owing from the defendant to the claimant. And the claimant claims interest pursuant to section 69 of the county court act 1984 at the rate if 8% per annum from 1/11/2012 to to 05/11/2012 totaling £xxxxx and thereafter at a daily rate of 0.81 to date of judgement or sooner. on advice of a friend i sent Nelson Guest and partners a CPR 31.14 Request and a CCA request, and filed a defense as follows I, abc of this place make this statement as my defence to the claim brought by Lloyds TSB o The claimants particulars of claim are vague and fail to disclose any cause of action, they appear to be an abuse of the process in that they fail to deal with the basic rules of pleading in accordance with the CPR even allowing for the constraints of the bulk issue system o No documents supporting the claims in the particulars have been offeredand despite a CPR31.14 request to the claimant for further information none has been forth coming and as a result I cannot plead in defence to the claim o The claimant pleads that the claim is brought under a regulated creditagreement regulated by the Consumer Credit Act 1974, yet the claimant claims statutory interest which the claimants hould surely know it is not entitled to by virtue of the County Courts(Interest on Judgment Debts) Order 1991 (No. 1184 (L. 12)) in particular section 2 (3) which expressly prohibits such an award. o The defendant contends that this claim amounts to a clear abuse of the process as the claimant would know the law and is trying to bring a claim for monies which it is not entitled to and knows that this is the case o Without clarification of the claimants claim, the defendant is extremely disadvantaged and the claimants claim appears without merit o Further to that above 6 paragraphs, the defendant is unable to plead effectively or at all. The defendant is embarrassed. last week i received a letter from the court saying they had recieve my defence, and served it on the Claimant. Today I got the following from wescot... Dear abc. We acknowledge safe receipt of your letter dated the 13th August 2012 requesting the Following documents in accordance with CRP.31.14:- 1. The agreement / 2. The assignment 3. The default notice 4. The termination notice 5. Statement of Account We would firstly refer you to CPR31.14, sections (l)(a), 31.14.2 and 31.14.3, which state:- 31.14 (1) A party may inspect a document mentioned in - (a) A statement of case 31.14.2 "... Document mentioned ..." The wording in the RSC was whether a "reference is made" to the documents. The CPR Wording probably requires a specific identification of the actual document. The mere mention of a transaction which must have used a particular document is unlikely to suffice; the document itself needs to be mentioned. 31.14.3 "... A statement of case ..." "Statement of Case" includes a claim form, particulars of claim, defence, PT20 Claim...... Therefore, as inspection is limited to documents mentioned in the Statement of Case, items 2 to 5 requested falls outside that ambit, and thus the only document requested, which is mentioned in the Statement of Case is the 'Agreement'. With this in mind and the overriding objectives set out in CRP1.1 (1), I can confirm that in accordance with your request we have approached the original lender for a copy of the agreement and other documents However, have particular regards to CPR1.1(1) we will confirm at this early stage all the Documents you have requested will not be forthcoming and you should therefore take the necessary action that you believe is appropriate, as by virtue of Carey v HSBC Bank Pic [2009] your request does not actually go towards establishing a Defence. You may also wish to take Independent legal advice from a Solicitor or approach the Citizens Advice Bureau who should be able to assist you free of charge. We are able to comfirm that no documants in relation to assignment are availableas we are acting on behalf of Lloyds tsb and this account has not been assigned to wescot. It is our opinion that all the information you have requested will not be necessary to prove our Case. A Court will consider the facts and evidence and make a fair and reasonable Judgment, which in our opinion will be that the funds claimed are due and owing. You may disagree, and it Isn’t really our place to second-guess a decision that will be made by the Trial Judge following the appropriate submissions of evidence by both parties. We hope we have set out our position clearly and fairly and would once again encourage you to take independent advice. Should you have any further queries, please do not hesitate to contact our offices on 0844 8241158. We confirm our file has been placed on hold for a period of 14 days. any advice what i should do now?

at the start of the month i received a claim from from Northampton court, the particulars where as follows The claim is £xxxx being monies owing to the claimant in respect of a credit agreement between Llloyds Tsb and the defendant under account no xxxxxxxxxxxxxxx The agreement was terminated as the defendant failed to maintain the agreed terms in accordance with the pre action protocols the claimant has attempted to contact the defendant and agree and repayment plan the defendant has failed to respond or maintain a suitable agreement and the balance of £xxxx remains due and owing from the defendant to the claimant. And the claimant claims interest pursuant to section 69 of the county court act 1984 at the rate if 8% per annum from 1/11/2012 to to 05/11/2012 totaling £xxxxx and thereafter at a daily rate of 0.81 to date of judgement or sooner. on advice of a friend i sent Nelson Guest and partners a CPR 31.14 Request and a CCA request, and filed a defense as follows I, abc of this place make this statement as my defence to the claim brought by Lloyds TSB o The claimants particulars of claim are vague and fail to disclose any cause of action, they appear to be an abuse of the process in that they fail to deal with the basic rules of pleading in accordance with the CPR even allowing for the constraints of the bulk issue system o No documents supporting the claims in the particulars have been offeredand despite a CPR31.14 request to the claimant for further information none has been forth coming and as a result I cannot plead in defence to the claim o The claimant pleads that the claim is brought under a regulated creditagreement regulated by the Consumer Credit Act 1974, yet the claimant claims statutory interest which the claimants hould surely know it is not entitled to by virtue of the County Courts(Interest on Judgment Debts) Order 1991 (No. 1184 (L. 12)) in particular section 2 (3) which expressly prohibits such an award. o The defendant contends that this claim amounts to a clear abuse of the process as the claimant would know the law and is trying to bring a claim for monies which it is not entitled to and knows that this is the case o Without clarification of the claimants claim, the defendant is extremely disadvantaged and the claimants claim appears without merit o Further to that above 6 paragraphs, the defendant is unable to plead effectively or at all. The defendant is embarrassed. last week i received a letter from the court saying they had recieve my defence, and served it on the Claimant. Today I got the following from wescot... Dear abc. We acknowledge safe receipt of your letter dated the 13th August 2012 requesting the Following documents in accordance with CRP.31.14:- 1. The agreement / 2. The assignment 3. The default notice 4. The termination notice 5. Statement of Account We would firstly refer you to CPR31.14, sections (l)(a), 31.14.2 and 31.14.3, which state:- 31.14 (1) A party may inspect a document mentioned in - (a) A statement of case 31.14.2 "... Document mentioned ..." The wording in the RSC was whether a "reference is made" to the documents. The CPR Wording probably requires a specific identification of the actual document. The mere mention of a transaction which must have used a particular document is unlikely to suffice; the document itself needs to be mentioned. 31.14.3 "... A statement of case ..." "Statement of Case" includes a claim form, particulars of claim, defence, PT20 Claim...... Therefore, as inspection is limited to documents mentioned in the Statement of Case, items 2 to 5 requested falls outside that ambit, and thus the only document requested, which is mentioned in the Statement of Case is the 'Agreement'. With this in mind and the overriding objectives set out in CRP1.1 (1), I can confirm that in accordance with your request we have approached the original lender for a copy of the agreement and other documents However, have particular regards to CPR1.1(1) we will confirm at this early stage all the Documents you have requested will not be forthcoming and you should therefore take the necessary action that you believe is appropriate, as by virtue of Carey v HSBC Bank Pic [2009] your request does not actually go towards establishing a Defence. You may also wish to take Independent legal advice from a Solicitor or approach the Citizens Advice Bureau who should be able to assist you free of charge. We are able to comfirm that no documants in relation to assignment are availableas we are acting on behalf of Lloyds tsb and this account has not been assigned to wescot. It is our opinion that all the information you have requested will not be necessary to prove our Case. A Court will consider the facts and evidence and make a fair and reasonable Judgment, which in our opinion will be that the funds claimed are due and owing. You may disagree, and it Isn’t really our place to second-guess a decision that will be made by the Trial Judge following the appropriate submissions of evidence by both parties. We hope we have set out our position clearly and fairly and would once again encourage you to take independent advice. Should you have any further queries, please do not hesitate to contact our offices on 0844 8241158. We confirm our file has been placed on hold for a period of 14 days. any advice what i should do now? -

Hi all, I've been browsing this site for a while, and although you guys know your stuff I haven't been able to find a relevant solution to my issue, so I signed up and here goes.. I took a £4500 personal loan out with Santander in Oct 2011 and after losing my job in April 2012 I haven't been able to keep up with the payments, which resulted in my loan stacking up with arrears. I've recently found a new job, but by this point it was too late, (and much to my shame) I started to ignore the bank when they called with threats of bailiffs and the like. I received a letter from Santander stating that the loan was being defaulted, and at the beginning of this week I started receiving phone calls from Westcot. I haven't answered the calls or called them back (as most of you said not to) but I received a letter yesterday from Westcot saying that they were instructed to collect the debt. I can't afford the monthly payments of £250 (which is what I was expected to pay with Santander) and I'm really in a pickle over this! Any help would be much appreciated Thank you!

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS