Showing results for tags 'cra'.

-

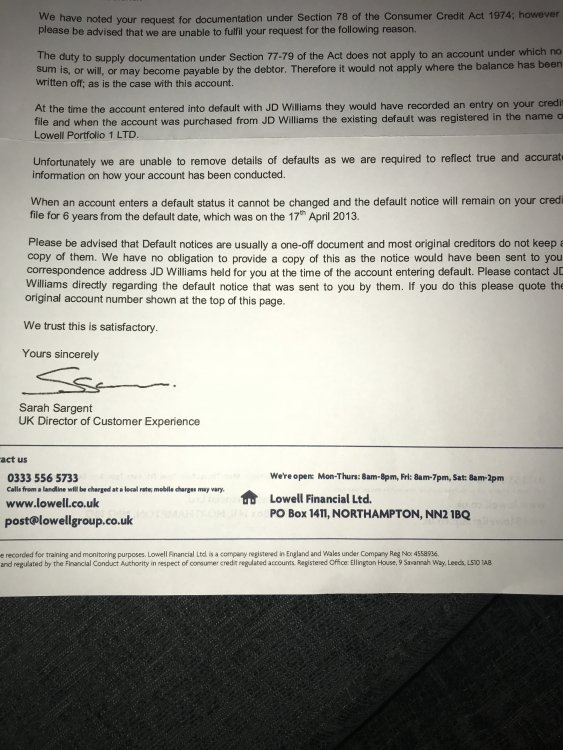

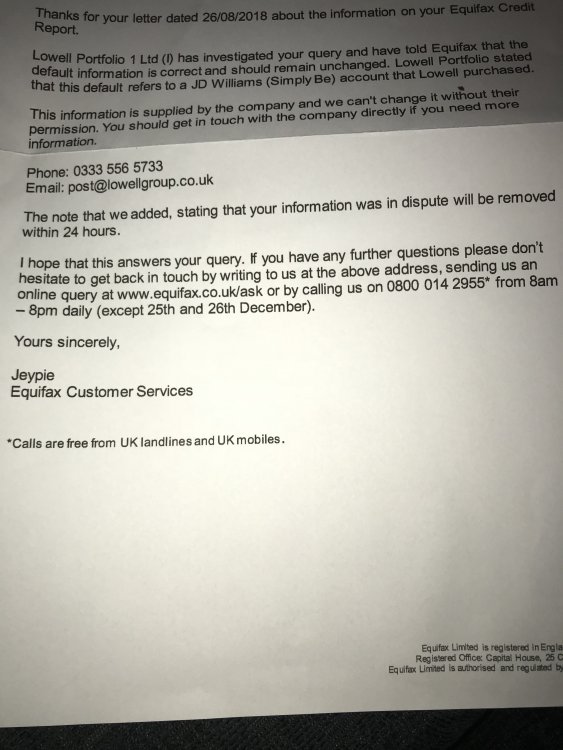

I also obtained this from them regarding a JD Williams account. It does not makes sense. Debt written off. No copy of contract, can't remove default as information was correct at the time but they can't send or have copies of nothing..? letter below including the reply from Exuifax, which tells me that the dca can't leave a default if it buys the debt? so something really wrong here.

I also obtained this from them regarding a JD Williams account. It does not makes sense. Debt written off. No copy of contract, can't remove default as information was correct at the time but they can't send or have copies of nothing..? letter below including the reply from Exuifax, which tells me that the dca can't leave a default if it buys the debt? so something really wrong here.

-

Hello I SAR'd VODAFONE for a debt that is on my credit file that i believe is not mine. I asked for SAR but they are asking for proof of my ID and address etc. I have only ever lived at one address, i told them that the credit file and the information they have put on the CRA's is the same as the address they are sending the SAR, but now the time has elapsed for them sending this to me. I don't want to send them any ID as I know they don't have my ID and won't send me any contract or nothing. There also sent it to a DCA, and I SAR'd them, they said its taking longer than expected, outwit the time limit and said will get back to me in a month or so - probably because they don't have any information from vodafone cos the contract and debt is not mine. Can anyone help me out?

-

This seemed like the best forum for this question, mods please move it if it should be somewhere else. Fraudsters obtained access to a friend of mine's online bank accounts and stole a lot of money. They did it by first stealing her mobile phone number. They submitted a fake PAC request to my friend's mobile phone provider and managed to convince them they were her. They then moved my friends mobile number to a different mobile provider, then managed to gain access to the online bank accounts and reset passwords. The bank sent verification codes to my friend's mobile number to check the requests were genuine but of course the mobile number was by that time under the control of the fraudsters. What I've learnt from all that is that PAC theft is a real weak link in online banking security unless mobile phone companies are as rigorour in ID verification for PAC requests as banks are. I don't think phone companies are. that's just background. After much time in meetings at the bank etc the bank has refunded all the money stolen without any quibbling and the phone company has apologised and offered (a small amount of) compensation and has closed down the stolen number. My friend now has a brand new number and as added security has had her account with mobile phone co restricted to say that no PAC code can be issued unless she goes in person to one of their stores with appropriate ID. I've advised her that she ought to check with the three Credit Reference Agencies to make sure the fraudsters didn't try to set up any fake accounts in her name during the time they were in control of her phone number. To find out what credit searches have been done on her will it be sufficient to just to get the statutory report from the three CRAs? eg this one from Experian https://www.experian.co.uk/consumer/statutory-report.html She doesn't particularly want to pay for wider access to her CRA information - she isn't interested in knowing her credit score for example - if the statutory report will tell her what she needs. (They used to cost £2 didn't they? I see Experian's is free now under GDPR) She's also changed her passwords on her email and every online site she uses. Anything else she should be doing? I've told her the fraudsters probably harvested a lot of the information they used from what she's posted on social media so to be very careful about that.

-

Hi Has anyone successfully had erroneous data removed from CRAs that was put there by Laredoute? I have a close family member who had previous credit with them many many years ago. She noticed about a year ago that Laredoute had updated her credit file with payment arrangements which she ceased many years ago.. then it was showing as being paid successfully, then again changed back to indicating missed payments. Will a CPR 31.14 help in this situation, though I doubt they will hold any data with the debt being so old, but thats only a guess. Any advice will be much appreciate regarding how to get the negative marks removed from CRAs. Thanks in advance WS

Hi Has anyone successfully had erroneous data removed from CRAs that was put there by Laredoute? I have a close family member who had previous credit with them many many years ago. She noticed about a year ago that Laredoute had updated her credit file with payment arrangements which she ceased many years ago.. then it was showing as being paid successfully, then again changed back to indicating missed payments. Will a CPR 31.14 help in this situation, though I doubt they will hold any data with the debt being so old, but thats only a guess. Any advice will be much appreciate regarding how to get the negative marks removed from CRAs. Thanks in advance WS -

This may have been covered so apologies however my wife had a debt with QuickQuid in 2010, there hasn’t been communication with them since and don't recall having DCA's involved we’ve seen the debt now appear on her Noodle credit file with an account start date of 2010 (when she took out the advance and wasn't able to make any repayments) but a default date of 2015 – i assume they’ve done this just before the debt is Barred so we’re screwed until 2021. Can they do this or is this unlawful? Some help would be appreciated. I've heard that a default can only be registered with a DCA within 6-months of the payments stopping - according to the ICO. Not sure if this is right.

-

I recently won against PRAC financial in a claim they made against me for a disputed PDL. (The dispute is still awaiting FO decision). Exact reasons the judge quoted were no evidence of assignment of the debt to PRAC and no evidence of a Default letter sent. Also their default was in the wrong company name. My other thread regarding the claim... https://www.consumeractiongroup.co.uk/forum/showthread.php?484274-PRAC-BW-claimform-old-PaydayUK-PDL-Debt-***Claim-Dismissed*** Today I had an email about a change to my credit report. Turns out the change is PRAC reporting a missed payment. Considering I won the claim what do I need to do to them. I assume writing to them stating the judge ruled no default/assignment so they have no right to either use my data, make changes to my credit record or in any way deal with me. Then demand they remove all entries? Any tips/examples floating around that will guide me?

I recently won against PRAC financial in a claim they made against me for a disputed PDL. (The dispute is still awaiting FO decision). Exact reasons the judge quoted were no evidence of assignment of the debt to PRAC and no evidence of a Default letter sent. Also their default was in the wrong company name. My other thread regarding the claim... https://www.consumeractiongroup.co.uk/forum/showthread.php?484274-PRAC-BW-claimform-old-PaydayUK-PDL-Debt-***Claim-Dismissed*** Today I had an email about a change to my credit report. Turns out the change is PRAC reporting a missed payment. Considering I won the claim what do I need to do to them. I assume writing to them stating the judge ruled no default/assignment so they have no right to either use my data, make changes to my credit record or in any way deal with me. Then demand they remove all entries? Any tips/examples floating around that will guide me? -

I bought a £500 graphics card from CCL 15 months ago, it broke, CCL said it has 3 year warranty, but after 12 months you return it to Gigabyte directly. I created an RMA with Gigabyte, they gave 3 options, Pay £15 for a company to deal with the return (at the time I thought this was just to collect the card from me and return it to Gigabyte, as I assumed Gigabyte would pay for the return), Send the card yourself or deliver it in person. I chose option to send it myself as I thought £15 was a lot for a 1 way delivery. I posted the card at the post office, £15.26, grrrr, hindsight! I got an email from Gigabyte telling me the card is repaired, I should arrange collection and let them know the details. At this point I thought, hang on a minute, you want me to pay for return!!! So I sent this email. They replied with this. So, where do I stand now? Who is liable for the return costs? CCL or Gigabyte?

I bought a £500 graphics card from CCL 15 months ago, it broke, CCL said it has 3 year warranty, but after 12 months you return it to Gigabyte directly. I created an RMA with Gigabyte, they gave 3 options, Pay £15 for a company to deal with the return (at the time I thought this was just to collect the card from me and return it to Gigabyte, as I assumed Gigabyte would pay for the return), Send the card yourself or deliver it in person. I chose option to send it myself as I thought £15 was a lot for a 1 way delivery. I posted the card at the post office, £15.26, grrrr, hindsight! I got an email from Gigabyte telling me the card is repaired, I should arrange collection and let them know the details. At this point I thought, hang on a minute, you want me to pay for return!!! So I sent this email. They replied with this. So, where do I stand now? Who is liable for the return costs? CCL or Gigabyte? -

I'm pretty sure this can be done using the law / courts if necessary - my problem is that I don't know what laws to cite and I don't have the funds to go and see a specialist solicitor.... The story in brief: I had a credit card with MBNA. MBNA (improperly [i believe]) assigned the debt to IDEM in 2012. IDEM and I fell out in 2013 - I stopped paying. We went through the tos and fros of asking them to provide paperwork. They couldn't - they defaulted the debt in December 2013 and (improperly [i believe]) assigned the debt on to Arrow Global at the end of 2015. Arrow Global appointed Shoosmiths solicitors to pester me ... cutting a lot of crap out, I asked for sight of the (last) DEED of assignment citing the Pelias Construction case and Lord Denning's words about an alleged debtor having proof that the person demanding payment has the right to do so and that any payment on his (the debtor's) part would extricate himself from being in debt... About a month ago, they (Shoosmiths) wrote back to me to tell me that they cannot provide any documentation at this point and will be discontinuing all collection activity forthwith. I have since called Shoosmiths to ask whether their client is going to remove the default notice from my CRA file as they know they can't enforce the debt (don't have the paperwork). Cutting to the quick I was told that they believe I owe them the money but just can't prove it and as a result they feel they "have the right to protect other lenders from me".... Clearly leaving default notices littered over my CRA file is very unfair. I feel like I am facing the consequences (at least in part) and treated as though guilty. Arrow Global are not a court - nor are Shoosmiths. If they cannot or will not proceed to court as I have been threatened so often where the question of who owes what to whom could have been addressed and properly adjudicated, HOW DO I GO ABOUT INSISTING THEY REMOVE THE DEFAULT NOTICE? What law(s) can I cite in any letter demanding this be removed / suppressed until proof does come to hand and / or who do I write to in their place and / or how do I get a court order for its removal and if I set about taking them to court, does the onus of "proof" then fall back on me? Any help would be appreciated. FWIW I know that this will have to fall off the end anyway in a couple of years or so - but in the meanwhile, we'd like to move house and having this mark there is preventing us from being able to effectively transfer our mortgage.

-

I bought a Denon AV receiver about 7 months ago from an online retailer. I now need to return it for a replacement power supply as it is making a humming noise. The retailer tells me I need to purchase packaging, arrange a courier and they will contribute £10 for carriage. This is a large and expensive item so packaging it safely will be a big job and I am not sure that £10 will cover carriage and insurance. They tell me repair could take up to 4 weeks which is very inconvenient as this is a critical part of our media system and used daily. I realise being without films and music isn't the end of the world but on the other hand I am annoyed that such an expensive item has failed so soon and is causing this inconvenience. I see The Consumer Rights Act says: What constitutes "significant inconvenience" and should a large item be expected to be returned with all costs, including packaging refunded?

I bought a Denon AV receiver about 7 months ago from an online retailer. I now need to return it for a replacement power supply as it is making a humming noise. The retailer tells me I need to purchase packaging, arrange a courier and they will contribute £10 for carriage. This is a large and expensive item so packaging it safely will be a big job and I am not sure that £10 will cover carriage and insurance. They tell me repair could take up to 4 weeks which is very inconvenient as this is a critical part of our media system and used daily. I realise being without films and music isn't the end of the world but on the other hand I am annoyed that such an expensive item has failed so soon and is causing this inconvenience. I see The Consumer Rights Act says: What constitutes "significant inconvenience" and should a large item be expected to be returned with all costs, including packaging refunded? -

I regularly check my credit report with Equifax, Noddle and Clearscore. I moved house over seven months ago and transferred all my bank account details to my new address. I am on the electoral register at my new address and I removed myself from the register at my old address. I did this months ago so all should be fine. However, my Equifax credit report still shows me living at my old address and says I am not on the electoral register at all. My Noddle credit report shows my old and new address but also says I'm not on the register at either address. I have written to all three CRA's telling them of my new address. They replied saying they can't change my address until I am on the electoral register at my new address. What on earth are these CRA idiots up to? Given a name and address I can easily and quickly find out if a person is on the register at that address, so why can't the CRA's? When I moved I changed over my energy, telephone, internet, water, driving licence, amateur radio licence, and council tax accounts to my new address. However according to the CRA's I don't live at my new address. I am therefore of the impression that CRA credit reports aren't worth the paper they are written on. Incorrect information is worth less than no information.

-

I have just checked my credit file today - having not checked it for months as ive not needed to and found a default in july 2016 placed on there by Mototmile Finance!! I was shocked. After some investigative work I now know it was a cash genie loan from 2012, which defaulted in 2012!! There is no mention of cash genie on my credit report at all. There used to be but it was removed last year, i'm not sure why but might have been when they went into liquidation?? So i thought that was the matter over......and now Motormile have put a fresh default on there?? I know they are currently carrying out a redress (discovered after some research online) but how do i know if this will qualify and the default be removed?? Or should I write to them and go about this some other way?? Legally they cant add on a 2016 dated default surely?? I am livid to say the least. We are about to look into mortgages as first time buyers and have painstaking saved up a deposit and this could now cause major problems obtaining one....or basically we will get flat out no's.

-

Hi not sure if this the right forum (please move on if incorrectly placed) but I would like some advise. I had a loan with Northern Rock and I asked to reduce my payment on the loan as I was struggling to make the payments. The loan went via the government to Marlin financial who contacted me and I agreed to increase the payment amount. (I was now in a better situation and this suited me to pay the loan of quicker). A few months before the final payment was due I had another letter informing me that the loan had now been passed onto Cabot financial and I did not need to do anything as the DD would just continue. I made the last few payments and thought that was that but; When I checked my credit score I found that the loan was not marked as being settled and it was also showing an arrangement in place for the last three years plus. I have contact Cabot about this and the have sorted out the loan showing as settled but think that it should show as having an agreement in place. I would like some advise as I did not sign anything with Northern Rock just a phone conversation about reduced payments and I have never entered into any sort of agreements with either Marlin or Cabots. This has greatly affected my credit score and if it possible to get it removed I would like to. So I suppose the question is can it be removed and is it right to report a payment agreement when I entered into no agreement with either Marlin or Cabot, and I never signed anything for Northern Rock.

Hi not sure if this the right forum (please move on if incorrectly placed) but I would like some advise. I had a loan with Northern Rock and I asked to reduce my payment on the loan as I was struggling to make the payments. The loan went via the government to Marlin financial who contacted me and I agreed to increase the payment amount. (I was now in a better situation and this suited me to pay the loan of quicker). A few months before the final payment was due I had another letter informing me that the loan had now been passed onto Cabot financial and I did not need to do anything as the DD would just continue. I made the last few payments and thought that was that but; When I checked my credit score I found that the loan was not marked as being settled and it was also showing an arrangement in place for the last three years plus. I have contact Cabot about this and the have sorted out the loan showing as settled but think that it should show as having an agreement in place. I would like some advise as I did not sign anything with Northern Rock just a phone conversation about reduced payments and I have never entered into any sort of agreements with either Marlin or Cabots. This has greatly affected my credit score and if it possible to get it removed I would like to. So I suppose the question is can it be removed and is it right to report a payment agreement when I entered into no agreement with either Marlin or Cabot, and I never signed anything for Northern Rock. -

Hi, I moved into a new house in July 2014 which had BG as the gas and electricity supplier. At the beginning of Sept I changed supply to another company. Shortly afterwards I received my final bill which for July and August amounted to £308 for gas and £90 for Electricity. they wanted £400 for 2 months supply in a new build house. I queried this and they stated the meter readings were correct and somebody had been to our property and manually read the meters. long story cut short, they weren't telling the truth after 7 months of wrangling and speaking to 2x DCA, taking my complaint to Centrica and providing a photo of my meter in February (which was still way below there supposed read) they agreed there was a mistake. All good final bill adjusted to £120 for both + £60 compensation and still ended up with a £35.17 refund! Finally the end of the matter or so I thought... In mid April I contacted the bank to take out a loan for £12k. Over the phone they provisionally approved me based on their internal scoring system but declined me based on my credit score. I queried this and was advised to take a copy of my credit report to the branch. I printed off my Experian credit report and met with the adviser to go through the finer details they couldn't see anything array and eventually agreed to lend the money by turning it into a joint application and at a high interest rate (18.9%!). last night I checked my free credit report with Noddle and saw 4 months missed payment on both of my old BG accounts. whilst I was disputing the final bill with them they logged missed payments on both accounts until I settled in April. So two questions I have: 1) Will BG remove these based on the fact they upheld my complaint? 2) Can I pursue BG with regards to the higher interest rate on the loan? as without the missed payment showing I would have had a lower interest rate. Any help will be really appreciated Thanks,

-

Hi all! This could hopefully be an easy one Car needs repair, just over 30 days since purchase, garage are agreeing but I want to retain my one shot repair option. How do I word an email reply to ensure I retain my right to reject and ask for refund or reduction if not repaired properly, pleeeease? Basically they offer a three month warranty but I want it done as a statutory repair and not a contractual one. Cheers NGE

-

this could be a very stupid questions but I notice on my CRA files some loans/debts show as settled whilst others show as satisfied. Which is better? I ask as I have an aqua card debt I need to pay and want to request a full and final settlement figure but part of my request is also asking that the debt be shown as nothing else owing on it.

this could be a very stupid questions but I notice on my CRA files some loans/debts show as settled whilst others show as satisfied. Which is better? I ask as I have an aqua card debt I need to pay and want to request a full and final settlement figure but part of my request is also asking that the debt be shown as nothing else owing on it. -

I had an account with Wonga that was taken out in April 2011. I received an email from Wonga in Feb 2015 just over a year ago stating that i no longer owe any money to Wonga or to PRA(UK) ltd and that my credit file would be updated to reflect this. My issue is this. I believe i have 2 defaults in relation to Wonga on my credit file. 1 for £1145.00 from Wonga the other £1192.00 from PRA UK Ltd. They have different default dates however I'm sure they must be the same account as i cannot recall any other debts to that value at that time. I have contacted both companies but haven't received any feedback as yet. Question 1- Could they be the same accounts with different default dates and values? albeit similar. Question 2- Does the Wonga buyback remove the default or just update the balance the zero? Thanks in advance.

-

what exactly does digital media of content mean? suppose someone asks for something that I email to them, is that digital content? supposing I order a psychic or tarot reading on line (whether people agree to such things or not) and I get it, read it and later it turns out to not be true. ..is that digital content if the site says for entertainment purposes only. if I order racing tips from a tipster online, he emails them to me and they don't win ...is that digital content? any insight to this would be a great help:???:

what exactly does digital media of content mean? suppose someone asks for something that I email to them, is that digital content? supposing I order a psychic or tarot reading on line (whether people agree to such things or not) and I get it, read it and later it turns out to not be true. ..is that digital content if the site says for entertainment purposes only. if I order racing tips from a tipster online, he emails them to me and they don't win ...is that digital content? any insight to this would be a great help:???: -

Not sure if this goes under CRA or Data Protection, please move if required. I am working on an EU complaint with some others about what to me seems a breach of the data protection act or at least article 8 of the human right act regarding privacy rights. I have obtained company documents from a CRA (meant for their clients) that offer customers the opportunity to join what I will call a "club", when they join they agree to provide the data on their customers including monthly payments and an update of their address. In return they get some free access (depending on how much info they share) to CRA system. CRA then use that data to update alerts to debt collectors, information brokers and other clients. My initial concern about this was about PURPOSE, the monthly payments are NOT credit payments, but for a broadband service (with 4 million customers), they even provide this customer information if the client prepays a year upfront. If the purpose of the CRA is about CREDIT then it seems entirely WRONG to pass on this information. If it was an energy company I would have a problem if the client were paying on presentation of the bill but tolerate it if the client added an outstanding bill to a monthly payment system which is in effect credit. My next concern was that the broadband company provided no meaningful way for the customer to opt out of having their data shared, the only reference in the terms provided at the point of sale was that a customer may have an address check. There is a page on their website that says they share your data with CRA, it is very much a take it or leave it comment saying we do this for your own good. If this is taken to it's logical conclusion McDonalds could share that you bought a burger, Petrol stations could share your purchasing location and so on. I think we all should have a reasonable expectation of privacy that when trading with a company as a private individual. I had a chat with a lowly member of staff at the ICO and they suggested that the CRA's are given carte blanche by the ICO and that we have to "account for ourselves", my response was that we do IF we decide to participate in taking credit but not if we do not take credit. They suggested that I might want to complain to the EU commissioners or I could complain to them first but they have a history of not going near CRA's. SHOULD WE BE ENTITLED TO OPT OUT OF THE CREDIT REFERENCE SYSTEM OR AT LEAST CONTROL WHAT IS SHARED? It would seem that Article 8 of the Human Rights Act thinks we should! It talks about a PRIVATE LIFE... The concept of a right to a private life encompasses the importance of personal dignity and AUTONOMY and the interaction a person has with others, both in private or in public. The right to personal autonomy and physical and psychological integrity, respect for private and confidential information, particularly the storing and sharing of such information Respect for privacy when one has a reasonable expectation of privacy and the right to control the dissemination of information about one’s private life. It seems to me there is no autonomy (self-government) afforded to the consumer with regard to the storing and sharing of their information by these credit reference agencies. Especially for those that do not even take credit. I think WHO I TRADE WITH and HOW MUCH I PAY it is a very private thing, especially if I am not given a MEANINGFUL way to opt out and to me that means a tick box where I say “NO YOU MAY NOT SHARE MY DATA WITH ANYONE WITHOUT MY EXPRESS WRITTEN PER OCCASION PERMISSION.” I think this "club" should be totally illegal, it amounts to a data swap. It seems to me that the ICO themselves by not enforcing this are in Breach of Article 8 as well as both the company providing the information and the CRA sharing the information. I would be very grateful for comment from the members of this forum and any advice they may wish to provide.

-

Hi, I've just noticed on my newly issued credit report that two debts, which were settled years ago, have mysteriously appeared. One belonging to BT, which I believe I addressed here for 200 odd and the other to Cabot Financial who insist that I have a debt with O2. (£900 odd?! no explanation as to what its for) The BT debt isn't an issue, that expired as of 9 hours 11 mins ago as per stutter barring O2 deny having a debt with me,Cabot tell me I do, neither of which will entertain sending me a letter to the effect... Also in the past I've sent them various letters: Oct 2011: Letter requesting invoices and full and final breakdown of the nature of the debt Nov 2011: (No Response) Chase up letter referring to the previous Dec 2011: (No Response) Final chase up letter stating that "if I don't hear from you within 30 days, I'll deem this matter as closed and resolved" (no response to date) I've contacted the CRA, they won't entertain the fact that I've gone though all these steps, Cabot are just a bunch of morons on the telephone as they won't discuss the matter and will only accept "a credit card or debit card number" and sound stay anything else. I'm literally grasping at strafers here as I really can't be bothered to go to court... Would the FCA be able to assist in this matter (and is that the right course of action?) Hope you can help Cheers, A

-

Hi there, friend of mine has been dealing with cabot for a CC, she has ignored them for some time recently been receiving letters regarding going to court from their solicitors stating the amount court costs would be, she is not worried about that as she knows it will be statues barred very soon but she has just checked her file on Clear score and the amount has been increased by the amount of court costs described in their last letter. Can they do this, add the costs on to her cra file before it's even been to court? Many thanks.

Hi there, friend of mine has been dealing with cabot for a CC, she has ignored them for some time recently been receiving letters regarding going to court from their solicitors stating the amount court costs would be, she is not worried about that as she knows it will be statues barred very soon but she has just checked her file on Clear score and the amount has been increased by the amount of court costs described in their last letter. Can they do this, add the costs on to her cra file before it's even been to court? Many thanks. -

Here is my best attempt at summarising my dealings with Peachy: Date Borrowed Repaid Interest/charges 20/12/13 0200.00 02/01/14 0227.00 0027.00 03/01/14 0500.00 03/02/14 0645.00 0145.00 0500.00 03/03/14 0630.00 0130.00 04/03/14 0500.00 30/04/14 0677.00 0177.00 01/05/14 0250.00 29/05/14 0075.00(rollover) 0075.00 27/06/14 0327.50 0077.50 27/06/14 0500.00 25/07/14 0193.74 0141.00 29/08/14 0156.48 0089.05 26/09/14 0157.76 0060.82 31/10/14 0177.07 0056.69 27/11/14 0044.88(rollover) 0044.88 23/12/14 0047.25 (rollover) 0047.25 30/01/15 Final payment due: £162.51 principal + £61.75 interest + £5.00 fees = £229.26 Repayment failed Total borrowed: 2450.00 Principle repaid: 2287.49 Interest + fees repaid: 1071.19 TOTAL REPAID: 3358.68 Principle outstanding: 0162.51 Amount claimed: 0996.09 Interest @ 8% (08/06/16): 0158.98 Total claim: 1155.07 Not surprisingly I have a late payment marker on my credit file, and have received twice-weekly text/email threats of a default marker for the last 18 months (together with "borrow more money!" emails every couple of days). SAR was sent on 5/5/16 with £10 postal order, deadline is 16/6/16. I have received no communication from Peachy other than threats/marketing, until yesterday, an email stating "We are pleased to inform you that we have successfully collected your loan payment" of - you guessed it - £10. They've used the SAR fee on my outstanding balance. Looking for guidance on how to proceed. I think I have enough information without the SAR to go ahead and complain/claim, but I'd also like to make a complaint regarding their handling of DPA requests - can anyone advise? Thanks in advance.

Here is my best attempt at summarising my dealings with Peachy: Date Borrowed Repaid Interest/charges 20/12/13 0200.00 02/01/14 0227.00 0027.00 03/01/14 0500.00 03/02/14 0645.00 0145.00 0500.00 03/03/14 0630.00 0130.00 04/03/14 0500.00 30/04/14 0677.00 0177.00 01/05/14 0250.00 29/05/14 0075.00(rollover) 0075.00 27/06/14 0327.50 0077.50 27/06/14 0500.00 25/07/14 0193.74 0141.00 29/08/14 0156.48 0089.05 26/09/14 0157.76 0060.82 31/10/14 0177.07 0056.69 27/11/14 0044.88(rollover) 0044.88 23/12/14 0047.25 (rollover) 0047.25 30/01/15 Final payment due: £162.51 principal + £61.75 interest + £5.00 fees = £229.26 Repayment failed Total borrowed: 2450.00 Principle repaid: 2287.49 Interest + fees repaid: 1071.19 TOTAL REPAID: 3358.68 Principle outstanding: 0162.51 Amount claimed: 0996.09 Interest @ 8% (08/06/16): 0158.98 Total claim: 1155.07 Not surprisingly I have a late payment marker on my credit file, and have received twice-weekly text/email threats of a default marker for the last 18 months (together with "borrow more money!" emails every couple of days). SAR was sent on 5/5/16 with £10 postal order, deadline is 16/6/16. I have received no communication from Peachy other than threats/marketing, until yesterday, an email stating "We are pleased to inform you that we have successfully collected your loan payment" of - you guessed it - £10. They've used the SAR fee on my outstanding balance. Looking for guidance on how to proceed. I think I have enough information without the SAR to go ahead and complain/claim, but I'd also like to make a complaint regarding their handling of DPA requests - can anyone advise? Thanks in advance. -

@thameswater Non Customer CRA Default

CookieRocks posted a topic in Utilities - Gas, Electricity, Water

Hi, hoping for some advice. Last month, whilst checking my Elearscore/ Equifax credit file, Thames Water have added and defaulted an account onto my credit file. It's added on my previous address. I never had an account with Thames Water. I've not lived at the address for over 8 years. They've added the account in 2016 but backdated it to 2014. Default amount is over £1000+. From my formal complaint, they first said they got my details from me. They then said they got my details from a letter they opened which was from a solicitor which was addressed to me and dated around 2014 [it can only be a DCA solicitor letter. All mail was in a shared common hall as it was three storey flats]. They then also say that my details are still at the address on the Electoral Roll data. Obviously I dispute it all. They refuse to remove it, saying I have to prove that I wasn't living there, but I don't think I should have to. I think they need to prove that I was living there, they refuse to, I'm not sure they can, but it's just going back and forth now. Obviously this is affecting my credit rating and credit worthiness. What should I do? Thanks in advance. CookieRocks -

Hi, I just wanted to check this out, in 2009 I was unfortunate enough to be given a CCJ by Suzuki Finance Limited for a car loan that I couldn't repay which was through Black Horse Finance. I made a payment arrangement and am still paying off the CCJ (which I will be doing until I die as they repayment amount is only £10 per month). I have paid the CCJ every month without fail and it reached 6 years old earlier this year and was removed from my Noddle account. However, even though I have never missed a payment the entry is also showing in "other accounts" on my credit report and I noticed that last month the default date has been changed to 12/7/12. Can someone advise me if Black Horse or Suzuki Finance (whoever has done this) are allowed to do this please? I have reported the matter to Noddle as default date incorrect and I'm waiting to hear from them. Thank you Maybe

Hi, I just wanted to check this out, in 2009 I was unfortunate enough to be given a CCJ by Suzuki Finance Limited for a car loan that I couldn't repay which was through Black Horse Finance. I made a payment arrangement and am still paying off the CCJ (which I will be doing until I die as they repayment amount is only £10 per month). I have paid the CCJ every month without fail and it reached 6 years old earlier this year and was removed from my Noddle account. However, even though I have never missed a payment the entry is also showing in "other accounts" on my credit report and I noticed that last month the default date has been changed to 12/7/12. Can someone advise me if Black Horse or Suzuki Finance (whoever has done this) are allowed to do this please? I have reported the matter to Noddle as default date incorrect and I'm waiting to hear from them. Thank you Maybe -

Lending Stream Hi there, in March 2011 I took out a loan with lending stream (amongst others), which I didn’t pay back, Due to a gambling addiction (addiction fixed now:-)) All of my accounts at the time fell into arrears and therefore default, which I deserved But upon checking my credit file, all of my other accounts show a default date of around may-sept 2011, yet lending stream show there’s as Nov 2012 With the 6 year rule I was happy to wait till sept 2017, but lending streams is a more than a year later, I thought It was a reporting mistake so I called them, and they confirmed the same date Surely it should have defaulted within 3 months to 180 days like the rest, I’ve heard of lending stream being weird how they report things to the CCA’s Can I challenge this? I.e. you should have defaulted me sooner

Lending Stream Hi there, in March 2011 I took out a loan with lending stream (amongst others), which I didn’t pay back, Due to a gambling addiction (addiction fixed now:-)) All of my accounts at the time fell into arrears and therefore default, which I deserved But upon checking my credit file, all of my other accounts show a default date of around may-sept 2011, yet lending stream show there’s as Nov 2012 With the 6 year rule I was happy to wait till sept 2017, but lending streams is a more than a year later, I thought It was a reporting mistake so I called them, and they confirmed the same date Surely it should have defaulted within 3 months to 180 days like the rest, I’ve heard of lending stream being weird how they report things to the CCA’s Can I challenge this? I.e. you should have defaulted me sooner -

Ok a quick scan on his forum says I'm not alone but here's my story - just wondering what the best set of steps is, i.e. complain to NPOWER even though I'm not a current customer, raise it with the regulator, or other options. I was with NPOWER until December 2014. I paid my bills on a monthly direct debit budget scheme. When I switched suppliers I very kindly received a cheque from NPOWER for the balance on my account and thought that was that. Of course I then got bills, lots and lots of bills with lots and lots of amounts. It took them, in my opinion far to long to switch me as well. I contacted them and asked how I could owe them anything when they'd just sent me a refund, asked them to send me definitive bills with readings etc. In the end I gave up and heard nothing. in August I suddenly got a series of communications. At the beginning of August I got 2 bills, one for gas and one for electric, 16.19 and 4.37. Then on the 12th of August I got a reminder for the gas, at £293.98 and one for the electric at 129.97 (remember I haven't been using them for about 8 months now!). These were quickly followed by those very special telemessage things that are supposed to scare you on the 26th and 27th August. Now here's where they really excelled themselves because on the 28 August I got a threatogram from Collections Direct for the gas, 293.98 (at least the amounts were now consistent) but one day later, on the 29th August I got a letter from NPOWER advising me they'd made a mess of it all and were writing off any outstanding balance. And all went quiet. Now I'd have to be honest and say I could not have told anybody whether I did or didn't owe them any money. The number of bills I got showing different amounts - including a refund - had me completely lost. Now today I receive reminders again, pay in 7 days etc etc. So I want this gone once and for all. I've not been a customer for over 15 months. So do I complain to them in the first instance or should I just take this straight up the food chain?

Ok a quick scan on his forum says I'm not alone but here's my story - just wondering what the best set of steps is, i.e. complain to NPOWER even though I'm not a current customer, raise it with the regulator, or other options. I was with NPOWER until December 2014. I paid my bills on a monthly direct debit budget scheme. When I switched suppliers I very kindly received a cheque from NPOWER for the balance on my account and thought that was that. Of course I then got bills, lots and lots of bills with lots and lots of amounts. It took them, in my opinion far to long to switch me as well. I contacted them and asked how I could owe them anything when they'd just sent me a refund, asked them to send me definitive bills with readings etc. In the end I gave up and heard nothing. in August I suddenly got a series of communications. At the beginning of August I got 2 bills, one for gas and one for electric, 16.19 and 4.37. Then on the 12th of August I got a reminder for the gas, at £293.98 and one for the electric at 129.97 (remember I haven't been using them for about 8 months now!). These were quickly followed by those very special telemessage things that are supposed to scare you on the 26th and 27th August. Now here's where they really excelled themselves because on the 28 August I got a threatogram from Collections Direct for the gas, 293.98 (at least the amounts were now consistent) but one day later, on the 29th August I got a letter from NPOWER advising me they'd made a mess of it all and were writing off any outstanding balance. And all went quiet. Now I'd have to be honest and say I could not have told anybody whether I did or didn't owe them any money. The number of bills I got showing different amounts - including a refund - had me completely lost. Now today I receive reminders again, pay in 7 days etc etc. So I want this gone once and for all. I've not been a customer for over 15 months. So do I complain to them in the first instance or should I just take this straight up the food chain?

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS