Showing results for tags 'come'.

-

I believe that a former employer may have acted unfairly against me whilst I worked there and I'm intending to SAR them to see if there is any evidence of this which I can use. I do not know where the evidence may exist or in what form, whether it is in emails, phone calls (which I know to be recorded and stored) or paper records so I would like to make a SAR for every piece of information they have. I also obviously do not want to disclose the reason for my request and find that the evidence I'm looking for may miraculously disappear. I am uncertain whether it's better to make a SAR in the next couple of days (before GDPR comes in), or wait until next week when GDPR is introduced. Under the present system, AIUI I pay the statutory fee of £10 but I then have an unqualified right to request all information. However, under GDPR the statutory fee is abolished but they will be able to charge a 'reasonable fee' where the request is 'manifestly unfounded'. Is there any guidance as to what a reasonable fee might be (lower/higher/the same as the current statutory fee?), and what qualifies as a 'manifestly unfounded' request - is a general request for all data rather than a targeted request considered 'unfounded' in itself?

I believe that a former employer may have acted unfairly against me whilst I worked there and I'm intending to SAR them to see if there is any evidence of this which I can use. I do not know where the evidence may exist or in what form, whether it is in emails, phone calls (which I know to be recorded and stored) or paper records so I would like to make a SAR for every piece of information they have. I also obviously do not want to disclose the reason for my request and find that the evidence I'm looking for may miraculously disappear. I am uncertain whether it's better to make a SAR in the next couple of days (before GDPR comes in), or wait until next week when GDPR is introduced. Under the present system, AIUI I pay the statutory fee of £10 but I then have an unqualified right to request all information. However, under GDPR the statutory fee is abolished but they will be able to charge a 'reasonable fee' where the request is 'manifestly unfounded'. Is there any guidance as to what a reasonable fee might be (lower/higher/the same as the current statutory fee?), and what qualifies as a 'manifestly unfounded' request - is a general request for all data rather than a targeted request considered 'unfounded' in itself? -

Tougher laser misuse laws come into force READ MORE HERE: https://www.gov.uk/government/news/tougher-laser-misuse-laws-come-into-force

-

Hi all, I had a judgement registered against me which i paid in full within 28days. I have spoken to the court and they have confirmed it is showing as cancelled however the lady said that it can take time to filter down to credit reference agencies, does anyone know what sort of length of time this may be as it is having a significant impact on my score and i need to get a letting agency check done. Is there anything i can do to speed up process??

Hi all, I had a judgement registered against me which i paid in full within 28days. I have spoken to the court and they have confirmed it is showing as cancelled however the lady said that it can take time to filter down to credit reference agencies, does anyone know what sort of length of time this may be as it is having a significant impact on my score and i need to get a letting agency check done. Is there anything i can do to speed up process?? -

Hi All Really appreciate your help on this. I have googled and I don't think there is anything we can do, but thought I'd check here. My mother had a quote for £2700 for some building work. She Emailed the builder and he set a date to start work. She had a reply saying it was confirmed etc. They sent numerous communications. Then she had a reply from the builder on a fake Email address that looked just like his asking for £900 payment to secure the date. She checked his references etc and it all seemed okay. 2 weeks later the builder called her asking for payment to get the scaffolding started. Obviously she thought she had paid. She hadn't. The bank investigated and the fraudulent account now has no money in it so they say she has lost it and it she was at fault. I told her to ask the bank in writing how long the account was open, how many frauds occurred and when was the first one. I heard you can complain based on the bank not closing the fake account in a timely manner. Anything else you would recommend? Thanks D

-

Rent pressure zones READ MORE HERE: https://beta.gov.scot/policies/private-renting/rent-pressure-zones/ Please note this only affects 'Private Residential Tenancies' in Scotland Only Rent Pressure Zone Checker: https://www.mygov.scot/rent-pressure-zone-checker/

Rent pressure zones READ MORE HERE: https://beta.gov.scot/policies/private-renting/rent-pressure-zones/ Please note this only affects 'Private Residential Tenancies' in Scotland Only Rent Pressure Zone Checker: https://www.mygov.scot/rent-pressure-zone-checker/ -

New overdraft alerts as CMA banking rules come into force READ MORE HERE: https://www.gov.uk/government/news/new-overdraft-alerts-as-cma-banking-rules-come-into-force

-

A strain of influenza which hit Australia and affected 98,000 people, is set to come to Britain and could case our worst epidemic for fifty years. Will it or wont it.I am taking no chances how about you. The vulnerable groups include the over-65s, pregnant women, children from six to 24 months and those with long-term *illness such as *diabetes, heart disease and asthma. https://www.unilad.co.uk/health/deadly-flu-outbreak-in-uk-expected-to-kill-thousands/ Well i have not much time this morning to hang around. I am nipping off sharpish to the vets to have my Flu Injection. Adios must fly. Tawnyowl.

A strain of influenza which hit Australia and affected 98,000 people, is set to come to Britain and could case our worst epidemic for fifty years. Will it or wont it.I am taking no chances how about you. The vulnerable groups include the over-65s, pregnant women, children from six to 24 months and those with long-term *illness such as *diabetes, heart disease and asthma. https://www.unilad.co.uk/health/deadly-flu-outbreak-in-uk-expected-to-kill-thousands/ Well i have not much time this morning to hang around. I am nipping off sharpish to the vets to have my Flu Injection. Adios must fly. Tawnyowl. -

I had debt 9 year ago due to unemployment. i also have a mortgage debt because of repossession of the house in uk. My question is simple how can i avoid being swamped by the debt collectors before i find a job, settle in and be in a position to negotiate a repayment. i have a bank account in uk where registered address is overseas. i will have to change that to my current address in uk for criminal records bureau check (now called dbs check) as req for the job. i know banks share the address change with credit companies. Please advise me on best strategy. thank you

I had debt 9 year ago due to unemployment. i also have a mortgage debt because of repossession of the house in uk. My question is simple how can i avoid being swamped by the debt collectors before i find a job, settle in and be in a position to negotiate a repayment. i have a bank account in uk where registered address is overseas. i will have to change that to my current address in uk for criminal records bureau check (now called dbs check) as req for the job. i know banks share the address change with credit companies. Please advise me on best strategy. thank you -

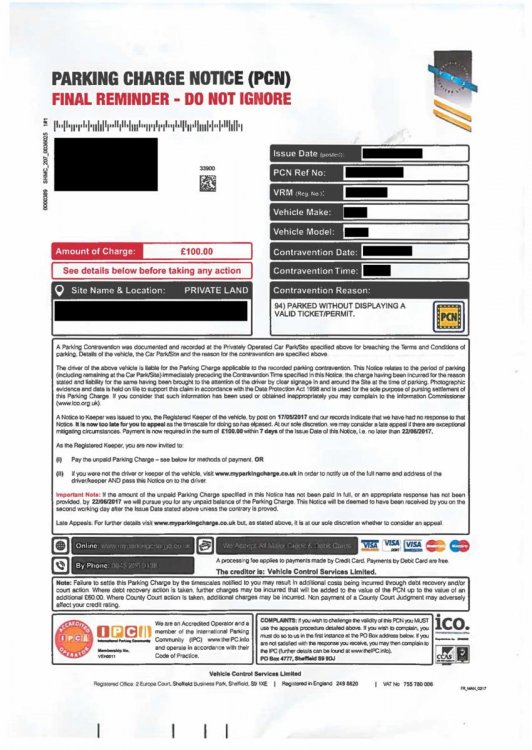

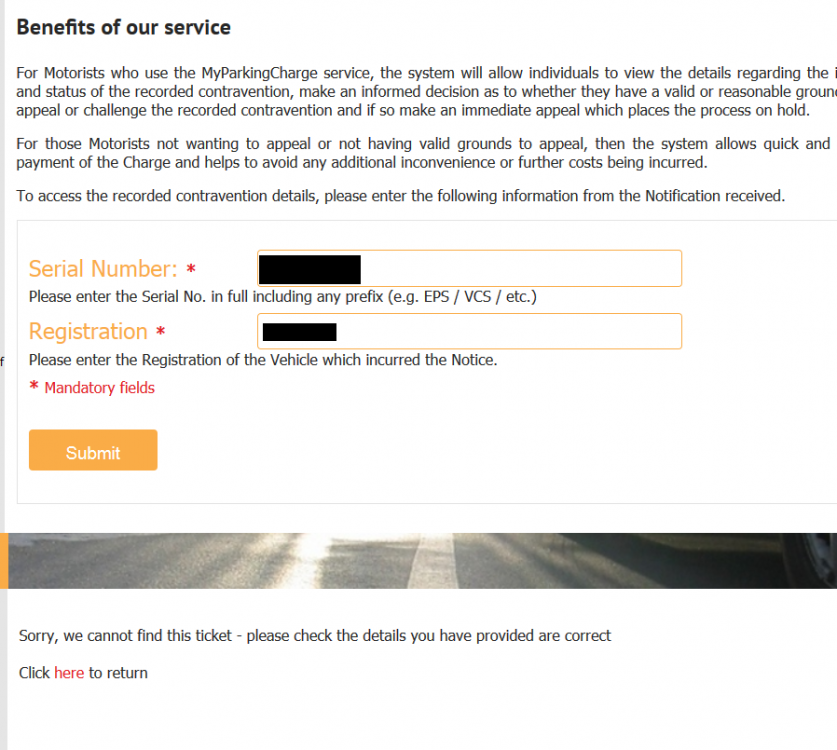

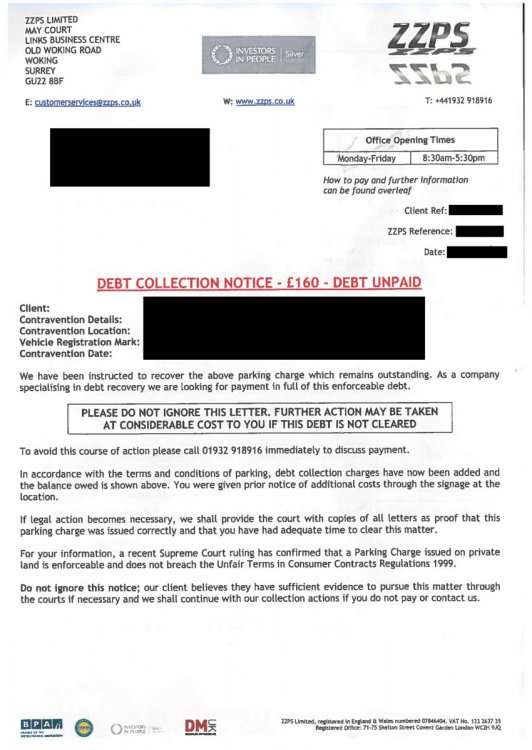

Hi all, First time here so please let me know if anything in this post should be changed. Backstory: I was in Bulgaria on business in June/July and had no knowledge of my PCN before leaving (turns out my mate moved my car out of his drive into the parking area for a couple hours where I received this PCN). Upon arriving home I find two letters, one being a final reminder sent mid June by VCS and then a debt collection notice sent by ZZPS in mid July. As I was out of the country and couldn't access my mail, I had no idea any of this was happening in my absence and had no chance to appeal the ticket in the allotted 28 days. The ticket was for £100, to be reduced to £60 if paid within two weeks and is now at £160 due to the debt collection agency add on. I haven't received any other letters regarding this claim. What I've tried: I have tried to go through the various appeals process, but when searching my ticket ref on the provided websites (namely myparkingcharge.co.uk as noted at the bottom of the VCS letter and the IPC website itself) it comes back with nothing, meaning that I couldn't have appealed it regardless. I even tried POPLA, and they can't find the ticket either. After contacting an ombudsman, they suggested to complain through the companies. VCS said that it was to go through ZZPS as they now were in charge of the debt , ZZPS replied as follows: "We must inform you that you have now passed the time frame in which an appeal can be made as appeals can only be made within 28 days of the Parking Charge Notice being issued, our client maintains that all correspondence received has been actioned accordingly and that the correct procedure has been followed. The balance of £160.00 remains payable on our systems, please refer to the back of our letter for the payment options available to you. In the absence of payment this matter will be referred to solicitors to resolve and further fees may be incurred." What do I do? If none of the appeals agencies even agree that the reference number matches any ticket, has a ticket even been issued against me? The collectors are refusing to provide evidence. I am not exactly inclined to pay this "debt" until the relevant parties prove their claim. Any advice would be appreciated as I feel like I'm about to get strong armed out of £160 Attached are the letters received, along with the website response when I search the reference. Personal info along with refs blacked out for obvious reasons.

Hi all, First time here so please let me know if anything in this post should be changed. Backstory: I was in Bulgaria on business in June/July and had no knowledge of my PCN before leaving (turns out my mate moved my car out of his drive into the parking area for a couple hours where I received this PCN). Upon arriving home I find two letters, one being a final reminder sent mid June by VCS and then a debt collection notice sent by ZZPS in mid July. As I was out of the country and couldn't access my mail, I had no idea any of this was happening in my absence and had no chance to appeal the ticket in the allotted 28 days. The ticket was for £100, to be reduced to £60 if paid within two weeks and is now at £160 due to the debt collection agency add on. I haven't received any other letters regarding this claim. What I've tried: I have tried to go through the various appeals process, but when searching my ticket ref on the provided websites (namely myparkingcharge.co.uk as noted at the bottom of the VCS letter and the IPC website itself) it comes back with nothing, meaning that I couldn't have appealed it regardless. I even tried POPLA, and they can't find the ticket either. After contacting an ombudsman, they suggested to complain through the companies. VCS said that it was to go through ZZPS as they now were in charge of the debt , ZZPS replied as follows: "We must inform you that you have now passed the time frame in which an appeal can be made as appeals can only be made within 28 days of the Parking Charge Notice being issued, our client maintains that all correspondence received has been actioned accordingly and that the correct procedure has been followed. The balance of £160.00 remains payable on our systems, please refer to the back of our letter for the payment options available to you. In the absence of payment this matter will be referred to solicitors to resolve and further fees may be incurred." What do I do? If none of the appeals agencies even agree that the reference number matches any ticket, has a ticket even been issued against me? The collectors are refusing to provide evidence. I am not exactly inclined to pay this "debt" until the relevant parties prove their claim. Any advice would be appreciated as I feel like I'm about to get strong armed out of £160 Attached are the letters received, along with the website response when I search the reference. Personal info along with refs blacked out for obvious reasons.

-

I bought 6 hard disks just over 2 years ago, 2 have failed just after the warranty, using the consumer rights act 2015 would I have a valid case for getting replaced or repaired? Is 2 years really an appropriate life expectancy for a HD?

I bought 6 hard disks just over 2 years ago, 2 have failed just after the warranty, using the consumer rights act 2015 would I have a valid case for getting replaced or repaired? Is 2 years really an appropriate life expectancy for a HD? -

Someone asked me this question and I could not answer. So as this idea grows I feel it is best to open a thread to discuss this important question. Where would the money come from. Would as Automation takes over and increased productivity happens from there somehow perhaps. Taxes. Companies, where do you think it would come from. It has to come from somewhere. Basic Income-A Great Idea Whose Time Is Coming. https://en.wikipedia.org/wiki/Basic_income

-

Hi, Just received an update to my credit file, a default registered this month for an account with a start of 2006. Its British Gas from a really old address. Since moving i have always been on the electoral role and stayed at addresses for 2-3 years. I have been at my current address for 3 years. I have not received a default notice to my current address. Does statute barred work for getting this default removed? Or maybe if i pay this old bill i can negotiate with British Gas given that I've not had a default notice through to my current address? or Something? Its been very damaging to what was a recovering credit rating ~D

Hi, Just received an update to my credit file, a default registered this month for an account with a start of 2006. Its British Gas from a really old address. Since moving i have always been on the electoral role and stayed at addresses for 2-3 years. I have been at my current address for 3 years. I have not received a default notice to my current address. Does statute barred work for getting this default removed? Or maybe if i pay this old bill i can negotiate with British Gas given that I've not had a default notice through to my current address? or Something? Its been very damaging to what was a recovering credit rating ~D -

"The national interest must come ahead of human rights" David Cameron. But is not human rights central to our national interest? Every year the British Government sell £4 billion in arms to one of the worlds worst human rights abusers, Saudi Arabia. Currently a 17 year old Saudi male faces public beheading followed by crucifixion because he has been found guilty of being involved in sedition in taking part in a human rights riot. David Cameron's Government cut a secret deal with Saudi Arabia last month to be elected onto the United Nations 'Human Rights Council'. Saudi Arabia publicly beheaded over 60 of it's own citizens last year year, flogging, up to 1000 lashes at a time, is common. Woman under penalty of imprisonment are not allowed to drive. The justification for David Cameron in turning a blind eye to these and other human rights abuses is 'We share valuable intelligence with them of people who want to harm both regimes'. As well as Saudi Arabia Britain has just completed trade deals with one of the most prolific Human Rights Abusers. That being China. An example wil be live organ donation/ harvesting from their prison population. ( Falun Gong) The response from the Chinese Government states that the prisoners agree to it. And the UK Government accepts that response What can be more harmful to our reputation on human rights when we ignore them in the name of national security that ultimately undermines our commitment to uphold human rights? No wonder the Tories are so keen to try and dump the European Convention of Human Rights as they have no respect of them. The irony in all of this is that it was a Tory who was instrumental in conceiving the ECHR That being Winston Churchil

"The national interest must come ahead of human rights" David Cameron. But is not human rights central to our national interest? Every year the British Government sell £4 billion in arms to one of the worlds worst human rights abusers, Saudi Arabia. Currently a 17 year old Saudi male faces public beheading followed by crucifixion because he has been found guilty of being involved in sedition in taking part in a human rights riot. David Cameron's Government cut a secret deal with Saudi Arabia last month to be elected onto the United Nations 'Human Rights Council'. Saudi Arabia publicly beheaded over 60 of it's own citizens last year year, flogging, up to 1000 lashes at a time, is common. Woman under penalty of imprisonment are not allowed to drive. The justification for David Cameron in turning a blind eye to these and other human rights abuses is 'We share valuable intelligence with them of people who want to harm both regimes'. As well as Saudi Arabia Britain has just completed trade deals with one of the most prolific Human Rights Abusers. That being China. An example wil be live organ donation/ harvesting from their prison population. ( Falun Gong) The response from the Chinese Government states that the prisoners agree to it. And the UK Government accepts that response What can be more harmful to our reputation on human rights when we ignore them in the name of national security that ultimately undermines our commitment to uphold human rights? No wonder the Tories are so keen to try and dump the European Convention of Human Rights as they have no respect of them. The irony in all of this is that it was a Tory who was instrumental in conceiving the ECHR That being Winston Churchil -

I moved back into my parent's house at the start of this year which was also when I registered as self-employed. I currently haven't been paying any council tax since I assume I have to let the council know I've moved in. My Dad doesn't have to pay any council tax. I have the money to pay for it but what sort of trouble can I expect to be in when I let the council know about this? Also I've so far earned around £8k this year so I think I may be able to benefit from working tax credits. Am I allowed to back date this benefit to the start of the year from when I registered as self-employed? However, I also have £10k in savings so I don't know how this will effect the benefit. Any help appreciated.

I moved back into my parent's house at the start of this year which was also when I registered as self-employed. I currently haven't been paying any council tax since I assume I have to let the council know I've moved in. My Dad doesn't have to pay any council tax. I have the money to pay for it but what sort of trouble can I expect to be in when I let the council know about this? Also I've so far earned around £8k this year so I think I may be able to benefit from working tax credits. Am I allowed to back date this benefit to the start of the year from when I registered as self-employed? However, I also have £10k in savings so I don't know how this will effect the benefit. Any help appreciated. -

Hi, I have just received a CCJ and all I got back from the courts was a letter telling me that the creditor sent the court a letter after they had received my admission and offer of monthly repayment, and that they had complained that the offer was too low. The court has now ordered that I pay a larger amount each month and that the first payment should be paid to the creditor by the 22nd of this month which is a week before I even get paid. I won't have the money by then and it's also more than I was expecting. Will the bailiffs come if I pay a week late? Or do you think the creditor will allow me to make the payment on the 29th if I explain my situation? I do feel like it is a bit unfair as they have decided that not only do I have to pay more than I offered, I also have to find it in just over a week. Any help would be much appreciated.

Hi, I have just received a CCJ and all I got back from the courts was a letter telling me that the creditor sent the court a letter after they had received my admission and offer of monthly repayment, and that they had complained that the offer was too low. The court has now ordered that I pay a larger amount each month and that the first payment should be paid to the creditor by the 22nd of this month which is a week before I even get paid. I won't have the money by then and it's also more than I was expecting. Will the bailiffs come if I pay a week late? Or do you think the creditor will allow me to make the payment on the 29th if I explain my situation? I do feel like it is a bit unfair as they have decided that not only do I have to pay more than I offered, I also have to find it in just over a week. Any help would be much appreciated. -

Forgive me if I seem a bit angry but I used to be a member here asking for advice on how to avoid a sanction from my JSA signing. I got what I thought was great advice at the time. I implemented that advice. I got sanctioned. Is there any way I can sue CAG for giving bad advice? Reading around the threads now with the "benefit" of hindsight, It seems that most site team and contributors are actually on ESA and divorced from reality and the world of work. If I'd realized this I wouldn't have followed their advice. I'm now left without money for 3 months. Thanks a lot. Do I have any recourse for suing you people? I guess if you actually knew what you were talking about then you wouldn't actually be on benefits to start with. My bad then. But you've really ****ed me over. Who can I sue for bad advice please?

Forgive me if I seem a bit angry but I used to be a member here asking for advice on how to avoid a sanction from my JSA signing. I got what I thought was great advice at the time. I implemented that advice. I got sanctioned. Is there any way I can sue CAG for giving bad advice? Reading around the threads now with the "benefit" of hindsight, It seems that most site team and contributors are actually on ESA and divorced from reality and the world of work. If I'd realized this I wouldn't have followed their advice. I'm now left without money for 3 months. Thanks a lot. Do I have any recourse for suing you people? I guess if you actually knew what you were talking about then you wouldn't actually be on benefits to start with. My bad then. But you've really ****ed me over. Who can I sue for bad advice please? -

Hi looking for a bit of advice but not sure if this is the right place. Long story short is i paid of my daughters loan of 7.5k the loan company now want to know where the money came from and are refusing to update the loan as paid on her credit file and will not close her account. She told them i paid it off but they want details of where i got the money from, now i can show them but why should i Thanks for any advice

-

Hello everyone. I am in such a stupid position that I have got myself into. I am extremely worried that it is stopping me from sleeping. To cut a long story short I have buried my head in the sand for far too long, on June 21st the Bailiffs will be coming to my house. I have been looking around and seen that it's possible for me to fill out a 'n245 form' and ask the court to stop the bailiffs coming. I have a few questions before I do. Firstly, tomorrow I plan to print off the form and send it out first class. Can the Bailiffs next week after I send this form? Should I let them know I have sent the form, or won't it be necessarily? If they turn up should I tell them then? I am extremely anxious at the idea of them turning up at my house, I am a nervous wreck. If the court do accept the application, what happens then? I am currently on Universal credits so not receiving very much money at all. I honestly won't be able to pay much every month. Do they court decide how much I should pay off of the CCJ? I'll do anything to stop bailiffs coming, but I have such an extremely small budget I don't know how to fix it. I'm very frightened and overwhelmed by the whole thing. I have also heard that the n245 form costs £50? How is that paid, I simply cannot afford to pay it in one go at the moment. I've read about a ex160 form that can apparently help with reducing that cost? Is that right. and if so do I have to send it along with the n245 form to the same place? Thank you for having such a place to come to for these questions (and I apologise for all the questions that are no doubt pretty stupid x) Yikes I have just re-read my post, I apologise for the typos.

Hello everyone. I am in such a stupid position that I have got myself into. I am extremely worried that it is stopping me from sleeping. To cut a long story short I have buried my head in the sand for far too long, on June 21st the Bailiffs will be coming to my house. I have been looking around and seen that it's possible for me to fill out a 'n245 form' and ask the court to stop the bailiffs coming. I have a few questions before I do. Firstly, tomorrow I plan to print off the form and send it out first class. Can the Bailiffs next week after I send this form? Should I let them know I have sent the form, or won't it be necessarily? If they turn up should I tell them then? I am extremely anxious at the idea of them turning up at my house, I am a nervous wreck. If the court do accept the application, what happens then? I am currently on Universal credits so not receiving very much money at all. I honestly won't be able to pay much every month. Do they court decide how much I should pay off of the CCJ? I'll do anything to stop bailiffs coming, but I have such an extremely small budget I don't know how to fix it. I'm very frightened and overwhelmed by the whole thing. I have also heard that the n245 form costs £50? How is that paid, I simply cannot afford to pay it in one go at the moment. I've read about a ex160 form that can apparently help with reducing that cost? Is that right. and if so do I have to send it along with the n245 form to the same place? Thank you for having such a place to come to for these questions (and I apologise for all the questions that are no doubt pretty stupid x) Yikes I have just re-read my post, I apologise for the typos. -

My friend is on Housing Benefit and ESA ( CONTRIBUTION BASED). He gets a small amount of Housing Benefit and is at present paying off a large overpayment at £10.89 a week from his HB. His ESA finishes in 2 weeks and he is probably going to claim carer's allowance ( cause he is going to look after his parents) and take a small job he's been offered. Now he wants to come off HB but is wondering how he does it. He only gets £15.00 per week after the overpayment is taken out and would rather stand on his own now. Trouble is he is at present being investigated because of the overpayment ( which was large) and made be prosecuted. Also he gets a occupational pension and once his ESA finishes he will pay no tax on that so his income will rise. So should he say his income will rise because of the tax, he is going to claim carers allowance and will possibly get a small job as well. Would he need to provide evidence of all this ? All he has at the moment is the letter saying the ESA is finishing. He suffers with his nerves and the investigation etc is wearing him down and he has realised that he can manage without the HB ( even if he's entitled) and would rather walk away. Can anyone help?

-

Hi All, I took out a log book loan for my sins due to personal circumstances at the time. Payments were being made unfortunately had a bout of ill health which caused me to miss 2 consecutive payments. Loan was for 12 months and made the first 4 on time before the ill health. I received a default notice after the second missed payment, the notice said that I only have 7 days to remedy the situation and pay the arrears and the charges applied. I then got a call on the 7th day to advise that as the default notice had not been remedied that the account had now been passed to repossession and that I need to pay the arrears and charges in full to stop the repo. I said that the default notice should give me 14 days to pay as the loan is under the CCA, he said that they had sent a default notice 7 days before the default notice I received and that the DN I received was a reminder. I said that I never received the first DN and not anywhere on the DN I received says that it is a reminder and that I have a further 7 days to sort out and that anyone reading the DN would assume that it is the only DN received. He said that he would look into this and come back to me, I also made a monthly payment at the same time which reduced my arrears to 1 month. Didn't hear any more until 3 days ago when I got woken up at 7am by someone wanting to repo the car, they clamped it and demanded the arrears and an additional £475.00 which is the repo fee. I had no choice but to raise the funds there and then as I use the car to ferry my 2 disabled children around. Can varooma the log book loan company pass my car for repo after only 7 days from date of default notice rather than letting me have the 14 days as they should do. Help would be much appreciated. Thanks

-

http://www.thenorthernecho.co.uk/news/local/darlington/11552200.Sanctioned_man_who_stole_to_eat_is_jailed/

http://www.thenorthernecho.co.uk/news/local/darlington/11552200.Sanctioned_man_who_stole_to_eat_is_jailed/ -

Hi all, I will try to keep this as brief but informative as possible, after suffering a nervous breakdown some 16 years ago (work related) I moved back to my home town along with my husband, the intention was to help my recovery. I was granted benefits for both myself and husband...I was on incapacity and claimed for him. After many years of various treatments and medications my mental health is wobbly at best. I am still in and out of counselling, I need my husband for support on a daily basis (as any one with mental health problems will understand) amongst all of the medication and fog that engulfed my life I somehow had a baby some 8 years ago, we are a nice little trio who get by...still on full benefits. Before my son was born I was on DLA for a few years but came off because I couldn't cope with the assessments. we have never applied for carers allowance. to be honest I don't know how my husband has stayed with me. I was called to my local office for a medical almost 12 months ago and they agreed that I was not fit to work and needed my husbands continuing support. Since then I have been contacted twice by my local job centre for help getting off benefits and back to work. I have done both interviews over the phone. Part of my condition means that I catastrophosize (yes it is a word...although probably not spelled right)This means that the slightest problem I experience is multiplied 1000 fold in my head, it inevitably takes over my life, making it difficult for me to cope with every day tasks. My next appointment is due in September I am already finding it difficult to think about anything else, my husband is willing to work, however I really don't think I could cope, sometimes |I cant leave the house let alone go to school to collect my son. I don't know what my options are but I am finding it increasingly difficult to cope. can anyone help many thanks

-

Sir Bruce Forsyth is to take part in a special routine on Sunday's Strictly Come Dancing to mark his departure as one of the show's main hosts. Yuk! Can't stand the patronising old git.

Sir Bruce Forsyth is to take part in a special routine on Sunday's Strictly Come Dancing to mark his departure as one of the show's main hosts. Yuk! Can't stand the patronising old git. -

Hi again guys, Just wanted advice on these 2 bank debts please. Nationwide and Natwest Nationwide was a overdraft for £1,300 Natwest was a overdraft for £1,700 I received today 2 letters for each debt. 1 from Red, one from Lowells. I have checked my credit files and these were on there last year but have now dropped off my report. - Last payments to both were before 2006 What should I do with the letters? Thanks in advance

Hi again guys, Just wanted advice on these 2 bank debts please. Nationwide and Natwest Nationwide was a overdraft for £1,300 Natwest was a overdraft for £1,700 I received today 2 letters for each debt. 1 from Red, one from Lowells. I have checked my credit files and these were on there last year but have now dropped off my report. - Last payments to both were before 2006 What should I do with the letters? Thanks in advance -

Hello all, I found this website a while ago and found it very interesting, i was hoping that i would never have to register and ask for advice but here i am with my (hopefully) only post Not sure if this is the right area but watched the posting video and it said this is the best place if you're not sure. I put my personal car up for sale outside my house and on eBay. On Thursday evening whist i was washing my new car a male pulled up outside my house and asked if the car was mine. I said it was and asked if he wanted to look at it. I handed him the keys and said do what you want with it and carried on washing the car. I then went back to him and said take it out on your own if you want. He asked me if i was sure and left his car. He drove off in my car on his own leaving his behind. He returned 10 minutes later and said that he would take the car. I asked him if he meant now and he replied no i will pick it up tomorrow after work and left. He left no deposit, so i took the sale with a pinch of salt. The next afternoon just as i was popping out to the Post office the male arrived. He said i'm still at work, i've just told my boss i've got to pop out to pay for a car. I will pay you now, take the keys and pick it up later. I was happy with this took the agreed £400 off him in cash, filled out the V5 with a change of owner in his name (which both of us signed) and the new keepers supplement in his name which i gave him along with the keys. As he was in a rush i did not offer to give him a receipt and he did not ask for one. As i was just on my way to the Post office before he arrived, i continued on with my day and since i was going to the Post office i thought i might as well post off the V5 whilst i was there. Which i did. When i got home a couple of hours later the car was gone. I stayed at my girlfriends last night and this was the text i woke up to this morning. Him - Hello. I'v driven the car for about 30 miles and clutch slips when warm. Sorry i'm bringing it back. Wanted a car a don't instantly need to fix. Thanks. Mat. Me - Hi Matt. I drove the car for 4400 miles and was never aware of the clutch slipping. I only stopped using the car as my daily driver on the 24th of May because I received a new van which I ordered 3 months previously. I did not sell the car with any known major problems. I gave you unlimited opportunity to inspect and drive the car on your own. I was honest and informed you of all the issues the car had. The car was sold as seen with no warranty implied or given. I can not accept the car car back as when you caught me going out yesterday I was on my way to the post office, so after you left I continued on my errand and posted off the V5 in your name. Him -The car is on your drive the keys are your house. I'll call and see you monday after work. Thanks. I returned home this morning to find the car on my drive (unlocked) all the paperwork inside and the keys through my door. When he took the car i had spent a day cleaning it inside and out. Now it looks like it has been driving through mud and had a dog sleep in it all night. When the male inspected the car i did not usher him around it in anyway and let him get on with it. I also let him take it for an unlimited test drive on his own. Sorry if i have waffled on a bit but i thought it best to get as much information down to start with.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS