Showing results for tags 'removal'.

-

Hope you can help. We have just moved house over the New Year. We hired a removal firm for Thursday 29 December 2016 through a bidding website. I received an e mail from the company saying they would attend after 1 p.m. on that day which I felt a bit late. On the day they came at 4.55 p.m. for a house removal! We got stuck in and starting moving and when it came to our 52 inch TV asked their advice about how to move this, they said use bubble wrap which we found and put round it and the removal men said they would use blankets and they moved the TV . When we unpacked the following evening (Friday) the TV was smashed completely. The company did advertise insurance. I telephoned early Saturday morning to be told, and received an email, that the TV was not in its box, we wrapped it ourselves, we probably broke it ourselves, and we didn't report it in 48 hours (which we did). They are saying its too small an item for insurance but this was a £600 television. Can anyone give advice please I hope I have put this on the correct forum page.

Hope you can help. We have just moved house over the New Year. We hired a removal firm for Thursday 29 December 2016 through a bidding website. I received an e mail from the company saying they would attend after 1 p.m. on that day which I felt a bit late. On the day they came at 4.55 p.m. for a house removal! We got stuck in and starting moving and when it came to our 52 inch TV asked their advice about how to move this, they said use bubble wrap which we found and put round it and the removal men said they would use blankets and they moved the TV . When we unpacked the following evening (Friday) the TV was smashed completely. The company did advertise insurance. I telephoned early Saturday morning to be told, and received an email, that the TV was not in its box, we wrapped it ourselves, we probably broke it ourselves, and we didn't report it in 48 hours (which we did). They are saying its too small an item for insurance but this was a £600 television. Can anyone give advice please I hope I have put this on the correct forum page. -

Hi Everyone, I used to have a vodafone account many years ago and something happened where i thought it had ended all paid up but it turned out i still owed some money. Once i found this out i got it paid but after looking at my credit file i see that vodafone put a default on it . although the payment shows as being missed in 2010 the default never went on until 2013 which means the file will not be removed until 2019, is there any way this can be rectified as if the default was lodged in 2010 it would be deleted from my account now. I'd like to add that this was for a fairly small amount and is causing me a real pain in obtaining credit. if anyone can help me with this it would be much appreciated, i asked vodafone online chat for the contact details for their credit department and they gave me two phone numbers. ..i rang both. one was experian and the other equifax... not who i wanted to speak to. was not impressed. please help! Terry

-

Not entirely sure if this should be in the banking forum, the benefits forum, or the debt forum, as it touches on all three. Site Team, m’dears, please move it to where you deem it best suited. Merci. My sister has a credit card debt with NatWest. Some time ago, they stopped her method of online payments which was her only way of getting money to them. Consequently the debt built up as it wasn’t being serviced. At about this time she had little or no income, eventually having to enter the benefits system. She has, I understand, been harassed by debt collectors regarding this debt. Whilst she has anxiety problems, amongst other issues, she is also the primary carer for her disabled son. Consequently, carer’s allowance and his PIP payments are made into her account. S ome of which is transferred into a savings account, her son is in need of alternative accommodation which would be more suited to his needs. The accrued sum is to pay a deposit and rent in advance whilst a housing benefit application is made. They are not currently in receipt of HB as it’s unnecessary for the current property. Without any notification, a couple of days ago, NatWest removed all the funds from her savings account and used it to pay the credit card debt. It is a four figure sum, the loss of which has been most devastating to her. A quick look through the process – it’s not my forte – and I’m assuming they are doing what is called ‘setting off’. This, apparently is something they are legally allowed to do, taking funds from one account to pay a debt on another. However, the guidelines for setting off appear to be quite clear that DWP benefits should not be taken and extreme caution must be used when dealing with financially vulnerable people. Not to mention that this is her son’s money and not hers. She has emailed NatWest to that extent, requesting the funds be returned asap. She is not in a fit state to talk to anybody on the phone and, as you may appreciate, is neither eating nor sleeping with the anxiety this has caused. Regarding the debt collectors, I’m assuming they shouldn’t be bothering vulnerable people at all. In the possible likelihood that NatWest refuse to return the funds, what would be the next sensible move?

-

I applied for a Cash Genie loan on 23/12/13. The application was accepted. The loan amount was £200, duration of credit agreement 8 days, loan ID xxxxxx8493, to be repaid in 2 simultaneous instalments of £60 (interest), and £200 on 31/12/13, total amount repayable £260. I ensured there were sufficient funds to repay the loan in full on the due date. I was therefore surprised to receive an email from Cash Genie on 27/4/14 reminding me of my "upcoming payment" for my loan ID xxxxxx4039. I checked my bank statements and discovered that payments had been taken from my debit card as follows: 30/12/13 £60 03/02/14 £60 03/03/14 £60 02/04/14 £60 Total £240 The total amount repayable under the loan agreement was £260. Cash Genie had rolled the loan over on 4 successive occasions entirely of their own volition and contrary to the terms and conditions of their own loan agreement. As the balance of the original loan agreement was £20, I repaid this on 01/05/14 and considered the subject closed. I then received an email from Cash Genie 01/08/14 containing a default sum notice for yet another loan ID xxxxxx7101 (I can only assume Cash Genie generated a new loan "agreement" every time they rolled over the loan). "The following default sums have been incurred and are now payable under the agreement referred to above: Amount Description Date £0.00 Sent Letters 01/08/2014 This Notice does not take account of default sums which we have already told you about in another default sum notice, whether or not those sums remain unpaid. The total amount of all default sums included in this Notice: £0.00." On 31/08/14 I received a second default notice via email with the exactly the same wording but the following default sums: "Amount Description Date £0.00 Sent Letters 01/08/2014 £0.00 Sent Letters 31/08/2014" This is the only correspondence I have received regarding a default notice. I am unaware therefore of any other alleged default sums. I immediately responded to these notices by paying the default sums (i.e.£0.00!). My credit record shows the following information: "Account start date: 30/05/2014 Opening balance: £260 Regular payment: £ 140 Repayment frequency: Monthly Date of default: 30/06/2014 Default balance: £260" Every line of data is complete nonsense! Furthermore, the status markers show the account being 1 month late in July 2014 (2 months after I paid it off) and in default in October 2014 (not 30/6/14 as shown above). My questions are: 1) I believe I am entitled to redress - what do I claim, and how do I calculate/ claim it? 2) Most importantly, I need this ridiculous default removed from my credit record. How? Thanks in advance!

I applied for a Cash Genie loan on 23/12/13. The application was accepted. The loan amount was £200, duration of credit agreement 8 days, loan ID xxxxxx8493, to be repaid in 2 simultaneous instalments of £60 (interest), and £200 on 31/12/13, total amount repayable £260. I ensured there were sufficient funds to repay the loan in full on the due date. I was therefore surprised to receive an email from Cash Genie on 27/4/14 reminding me of my "upcoming payment" for my loan ID xxxxxx4039. I checked my bank statements and discovered that payments had been taken from my debit card as follows: 30/12/13 £60 03/02/14 £60 03/03/14 £60 02/04/14 £60 Total £240 The total amount repayable under the loan agreement was £260. Cash Genie had rolled the loan over on 4 successive occasions entirely of their own volition and contrary to the terms and conditions of their own loan agreement. As the balance of the original loan agreement was £20, I repaid this on 01/05/14 and considered the subject closed. I then received an email from Cash Genie 01/08/14 containing a default sum notice for yet another loan ID xxxxxx7101 (I can only assume Cash Genie generated a new loan "agreement" every time they rolled over the loan). "The following default sums have been incurred and are now payable under the agreement referred to above: Amount Description Date £0.00 Sent Letters 01/08/2014 This Notice does not take account of default sums which we have already told you about in another default sum notice, whether or not those sums remain unpaid. The total amount of all default sums included in this Notice: £0.00." On 31/08/14 I received a second default notice via email with the exactly the same wording but the following default sums: "Amount Description Date £0.00 Sent Letters 01/08/2014 £0.00 Sent Letters 31/08/2014" This is the only correspondence I have received regarding a default notice. I am unaware therefore of any other alleged default sums. I immediately responded to these notices by paying the default sums (i.e.£0.00!). My credit record shows the following information: "Account start date: 30/05/2014 Opening balance: £260 Regular payment: £ 140 Repayment frequency: Monthly Date of default: 30/06/2014 Default balance: £260" Every line of data is complete nonsense! Furthermore, the status markers show the account being 1 month late in July 2014 (2 months after I paid it off) and in default in October 2014 (not 30/6/14 as shown above). My questions are: 1) I believe I am entitled to redress - what do I claim, and how do I calculate/ claim it? 2) Most importantly, I need this ridiculous default removed from my credit record. How? Thanks in advance! -

Hi there I have a fine with Staffordshire county council which has escalated to £398 and now at the stage where bailiffs are due back tomorrow (with the addition of another £110). I had an agreement which I broke. I was paying weekly but fell behind. I am guilty of burying my head in the sand. I have a few mental health issues and claim ESA at the moment. I have 4 kids and am a single mum. I sometimes get anxious about opening my mail and ignore and forget things. I know it's the wrong thing to do, but sometimes I can barely leave the house or get out of bed. Just a few years ago I was working as a full time teacher. Everything has changed since my divorce and now my life is out of control. I have called Jacobs and the council today and nothing can be done but for me to pay the full balance or he'll be back tomorrow. I offered to pay £50 today and rest in instalments, but the bailiff said the best he can do is 50% today and the rest in 10 days. I'm sitting here feeling so anxious and worried. It's my son's 9th birthday in 2 days and christmas around the corner. What a mess!! I have no idea what to do next... I know he has no right of entry and so will ignore the door tomorrow, but then the 110 will be added and so on.... there seems no way out. Any advice will be much appreciated.

Hi there I have a fine with Staffordshire county council which has escalated to £398 and now at the stage where bailiffs are due back tomorrow (with the addition of another £110). I had an agreement which I broke. I was paying weekly but fell behind. I am guilty of burying my head in the sand. I have a few mental health issues and claim ESA at the moment. I have 4 kids and am a single mum. I sometimes get anxious about opening my mail and ignore and forget things. I know it's the wrong thing to do, but sometimes I can barely leave the house or get out of bed. Just a few years ago I was working as a full time teacher. Everything has changed since my divorce and now my life is out of control. I have called Jacobs and the council today and nothing can be done but for me to pay the full balance or he'll be back tomorrow. I offered to pay £50 today and rest in instalments, but the bailiff said the best he can do is 50% today and the rest in 10 days. I'm sitting here feeling so anxious and worried. It's my son's 9th birthday in 2 days and christmas around the corner. What a mess!! I have no idea what to do next... I know he has no right of entry and so will ignore the door tomorrow, but then the 110 will be added and so on.... there seems no way out. Any advice will be much appreciated. -

Hello, my name has been put on the CUE database by OCTAGON this is for life. My crime was to use a comparison site to compare quotes, i did this about 50-60 times and the reason was to check how they arrived at their prices. I searched all types including 1- all the different vol excess about 6. 2- declared mileage about 5, 3- different types of cover about 3, 4- different addresses about 4 , 5- what date to start ins. as they differ a lot, so does the price and also a host of other type searches. To be honest i was trying to get the cheapest but also curious as to how they arrived at their prices, hence so many searches. Finally i picked Octagon and telephoned them about the online quote , they refused to insure me saying over 50 searches was far too much as in their eyes it appeared fraudulent and I was the type of person that could lie. They were especially concerned about the 4 diff family addresses I used, but I explained that my family was present and wanted to know the price diff and it was entirely innocent. I declared my correct address at the time of submitting as with all my other details, in fact it was the most expensive. They didnt want to know me and said were not insuring me and putting my name on the CUE database What i want to know is can they legally do this on a whim and can i force them to remove, are there financial repercussions to sue them. Is there somewhere that specialises in helping me? or can YOU? Many thanks....waiting and suffering PP oh ive written to them and they have closed the matter

-

question on removal of car by baliffs if it was to prove that removing a car would cause hardship on the person such as living in the country no bus service to work possible loss of employment to both husband and wife children too costly to pay for taxi could you appeal against the removal of car this is just a question it has not happened just wondering in the back of my mind

-

Hello, I home someone can help with this problem. Around December 2009, after finishing university I put some belongings in storage with Clockwork Removals in Edinburgh figuring I would have them transported once I started work again. About a year ago, I requested that they send my items over to France. Then we discovered that these items (six packing boxes) had been "misplaced" when they moved to new premises in Granton. I've been trying for a year to get my belongings returned or a refund (£65 x 12 months x 6 years = £5500 + value of belongings). Needless to say, Clockwork aren't cooperating. The first time, they asked if I could come up to their warehouse to help identify my belongings. Second time they said they had found my four chairs. Third time, they refuse to talk. It looks like I am having to go legal on this one?

-

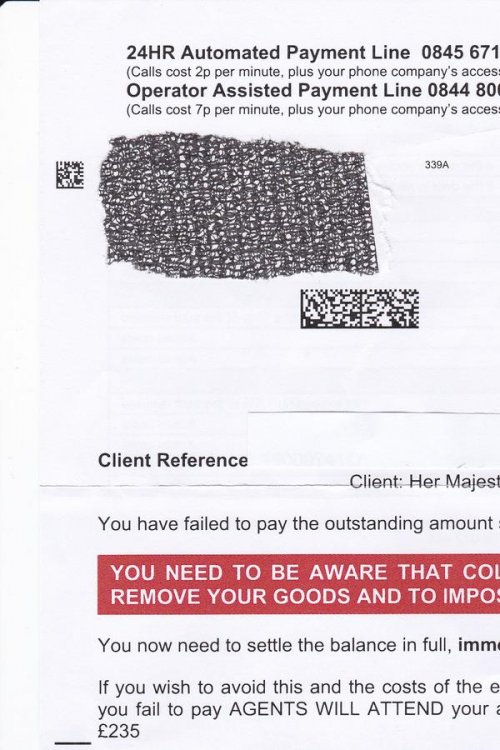

Received this letter which purports to be from Collectica collected a debt from "Her Majesty's Courts & Tribunal Service" Can this be for real? There hasn't been any court papers received concerning this matter. Somebody called without an appointment at the house. No one was in but he left his card. I have no idea who was the original creditor. I got a feeling its a try on and I would like to refer it the OFT and Financial Conduct people. Anybody got any ideas, comments welcome ?

Received this letter which purports to be from Collectica collected a debt from "Her Majesty's Courts & Tribunal Service" Can this be for real? There hasn't been any court papers received concerning this matter. Somebody called without an appointment at the house. No one was in but he left his card. I have no idea who was the original creditor. I got a feeling its a try on and I would like to refer it the OFT and Financial Conduct people. Anybody got any ideas, comments welcome ?

-

Hello, We have just had our storage and removal insurance claim denied I don't know what to do next. If I get anything wrong I'm sorry as this is my first post. Back in October we paid for a large national removal firm to come to our house, pack and export wrap all of our things and then take them to be stored in their warehouse for six months as we were moving to Eastern Europe to start a business. We took out their own removal and storage insurance covering us up to the value of £23,000 as we listed all of the items about £500 separately as per their instructions. When the time came for us to have our things delivered, we employed a second removal company to collect our things from the warehouse and deliver them to us in Eastern Europe. We also took them up on their insurance, for the same amounts as above. When our things arrived, everything looked fine at first, but as we started to unpack we saw that almost all of the boxes had been opened, then resealed and new box numbers put on with the old ones taken off. Some boxes even had two completely different numbers on, and the contents of the boxes was completely different to what was written on the packing inventory. Most of the boxes were almost empty too, but in was done in such a way that you wouldn't be able to tell until the box was open. For example, one of the boxes said that it contained my evening dresses and formal wear, it was a big box, but all it contained was our old and very worn picnic rug Our little fire safe had also been broken into, you can see where the lock has been forced and the contents are gone. We went through everything and the missing items come to just under £15,000. We informed both removal companies within four days of receiving our things. The first company who had stored the things said to fill out the insurance forms and get the information to them as soon as we could. The second company said that it was not their responsibility as everything had looked in good order when they collected it, but their broker sent us the claim forms and said to submit the claim anway. We put the claim in for the first removal company as the second removal company would not have been able to open and reseal the boxes as they did not have the branded labels with the first companys logo and details. The first removal firm said that they had sent our claim off to their brokers underwriters and that we would hear directly from them. After five weeks of not hearing anything, and of the removal company ignoring my emails and not putting me through to anyone when I called, I called the broker instead who said that they had never received our claim details. They asked me to send them directly to them, which I did. They have sent me an email saying that they are denying the claim as it is the other removal companys responsibility as the goods were in good condition when the collected them. I'm not sure what to do, it is soul destroying, these were hugely sentimental items, we are devastated. Any help or advice would be very greatly appreciated thank you. Sorry I should have added that we have now moved back to the UK as my mother became very ill and we didn't want to be far away.

Hello, We have just had our storage and removal insurance claim denied I don't know what to do next. If I get anything wrong I'm sorry as this is my first post. Back in October we paid for a large national removal firm to come to our house, pack and export wrap all of our things and then take them to be stored in their warehouse for six months as we were moving to Eastern Europe to start a business. We took out their own removal and storage insurance covering us up to the value of £23,000 as we listed all of the items about £500 separately as per their instructions. When the time came for us to have our things delivered, we employed a second removal company to collect our things from the warehouse and deliver them to us in Eastern Europe. We also took them up on their insurance, for the same amounts as above. When our things arrived, everything looked fine at first, but as we started to unpack we saw that almost all of the boxes had been opened, then resealed and new box numbers put on with the old ones taken off. Some boxes even had two completely different numbers on, and the contents of the boxes was completely different to what was written on the packing inventory. Most of the boxes were almost empty too, but in was done in such a way that you wouldn't be able to tell until the box was open. For example, one of the boxes said that it contained my evening dresses and formal wear, it was a big box, but all it contained was our old and very worn picnic rug Our little fire safe had also been broken into, you can see where the lock has been forced and the contents are gone. We went through everything and the missing items come to just under £15,000. We informed both removal companies within four days of receiving our things. The first company who had stored the things said to fill out the insurance forms and get the information to them as soon as we could. The second company said that it was not their responsibility as everything had looked in good order when they collected it, but their broker sent us the claim forms and said to submit the claim anway. We put the claim in for the first removal company as the second removal company would not have been able to open and reseal the boxes as they did not have the branded labels with the first companys logo and details. The first removal firm said that they had sent our claim off to their brokers underwriters and that we would hear directly from them. After five weeks of not hearing anything, and of the removal company ignoring my emails and not putting me through to anyone when I called, I called the broker instead who said that they had never received our claim details. They asked me to send them directly to them, which I did. They have sent me an email saying that they are denying the claim as it is the other removal companys responsibility as the goods were in good condition when the collected them. I'm not sure what to do, it is soul destroying, these were hugely sentimental items, we are devastated. Any help or advice would be very greatly appreciated thank you. Sorry I should have added that we have now moved back to the UK as my mother became very ill and we didn't want to be far away. -

Some way down the road with this already having sent letters and schedule of charges etc. Got some money knocked off twice. Sent a Letter Before Action but have not been on top of things and not followed up at 14 days. Weeks have passed. Am now going to file for court in earnest after sending a revised Letter Before Action. I'm not really happy with the way I am calculating interest in my prior documents and want to get it right and proceed with vigour. THE PROBLEM: Historic charges were applied on particular dates and did or didn't attract interest for varying amounts of time depending on how Barclaycard decided to play it i.e. A charge goes on, there is say 28 days when it does not have interest charged on it then it falls into the main balance and then charging of interest commences as if it were a purchase. When payments are made it is the first, second etc amount to be paid off and then it ceases to attract interest even if you still have a balance which was formed by purchases. THE QUESTION: Do I need to give a monkeys about the nuances of the above dates, payment thresholds etc? Is it OK to just say it attracted X numbers of months of interest which corresponded to the next time I cleared the balance? The money that paid it off would have paid off an equal amount of the "real" purchase balance if the charge had not been applied in the first place wouldn't it? ALSO: I am finding a lot of what would appear to be dead links to spreadsheets, letters etc. The ones I do find seem to be out of date for one reason or another and the forum/wiki seems to be very hard to navigate in terms of finding appropriate documents/attachments. Is there a page which has all the most up to date forms on that I am missing. I'm particularly needing a restitutional interest spreadsheet and good/recent Particulars of Claim texts. Hope someone can help. Best Regards DatumX

Some way down the road with this already having sent letters and schedule of charges etc. Got some money knocked off twice. Sent a Letter Before Action but have not been on top of things and not followed up at 14 days. Weeks have passed. Am now going to file for court in earnest after sending a revised Letter Before Action. I'm not really happy with the way I am calculating interest in my prior documents and want to get it right and proceed with vigour. THE PROBLEM: Historic charges were applied on particular dates and did or didn't attract interest for varying amounts of time depending on how Barclaycard decided to play it i.e. A charge goes on, there is say 28 days when it does not have interest charged on it then it falls into the main balance and then charging of interest commences as if it were a purchase. When payments are made it is the first, second etc amount to be paid off and then it ceases to attract interest even if you still have a balance which was formed by purchases. THE QUESTION: Do I need to give a monkeys about the nuances of the above dates, payment thresholds etc? Is it OK to just say it attracted X numbers of months of interest which corresponded to the next time I cleared the balance? The money that paid it off would have paid off an equal amount of the "real" purchase balance if the charge had not been applied in the first place wouldn't it? ALSO: I am finding a lot of what would appear to be dead links to spreadsheets, letters etc. The ones I do find seem to be out of date for one reason or another and the forum/wiki seems to be very hard to navigate in terms of finding appropriate documents/attachments. Is there a page which has all the most up to date forms on that I am missing. I'm particularly needing a restitutional interest spreadsheet and good/recent Particulars of Claim texts. Hope someone can help. Best Regards DatumX -

Hello Caggers, I have gained immensely from the advice on this forum...thanks for that everyone. I need help in removing a DN from my credit file please. The entry was made in Aug 2010 by Barclaycard for #492. I have emailed CEO using one of the sample letters on here and got a response from a lady called Judith Hayes. She has promised to send statements and records. She also mentioned that some of the charges are made up of PPI, Penalties and Interest charges. This is a cummulative total of the charges vs credit limit Credit Limit vs Balance History 2009 2010 2011 Jan -61 -232 Feb -94 -232 Mar -128 -232 Apr -163 -232 May -200 -232 Jun -226 -232 Jul -229 -232 Aug - 232 -232 Sep -232 -232 Oct -13 -232 -232 Nov 30 -232 -232 Dec -28 -232 -232 Ideas and suggestions all welcome. Thanks

Hello Caggers, I have gained immensely from the advice on this forum...thanks for that everyone. I need help in removing a DN from my credit file please. The entry was made in Aug 2010 by Barclaycard for #492. I have emailed CEO using one of the sample letters on here and got a response from a lady called Judith Hayes. She has promised to send statements and records. She also mentioned that some of the charges are made up of PPI, Penalties and Interest charges. This is a cummulative total of the charges vs credit limit Credit Limit vs Balance History 2009 2010 2011 Jan -61 -232 Feb -94 -232 Mar -128 -232 Apr -163 -232 May -200 -232 Jun -226 -232 Jul -229 -232 Aug - 232 -232 Sep -232 -232 Oct -13 -232 -232 Nov 30 -232 -232 Dec -28 -232 -232 Ideas and suggestions all welcome. Thanks -

Hi i wonder if you could help/guide me I have a charging order on my property for £10,750 from 2006, it was applied by alliance and leciester for a 10k loan I took out for my exgirlfriend (girlfriend at the time) for her parents company and they couldn't get credit they had the money in 2004 and ended up not affording it and missed payments and I couldn't afford it or get credit so it ended up a charging order as I buried me head in the sand as was only 20-21 I never knew what it was at the time, I am now trying to get a bigger mortgage before moving and this has come up blocking it How do I go about removing it before or with the house sale Many thanks

-

Hi All, I am trying to get any information possible on the removal of Settled Accounts that were in good standing from the main credit agencies. I used a well known payday loan company back in 2013 and rolled over the loan a few times and always paid early and in full. Never late and no negative info at all. However fast forward 3 years , I am trying to secure a mortgage and have been refused due to having 6 entries from a specific payday loan lender. Even though they are all settled and paid and closed they underwriters see that as there were 6 entries, that I am a risk !! I have a good credit score and this is the only negative. This is causing me to have to look through other "brokered" lenders who all want to charge fees and I am looking at a higher interest rate also. It crazy that I borrowed and paid back on time and still penalised for it. Can any one give me any advise on how I can persuade the payday lender to remove the settled accounts from my files?? As its causing me financial issues if I have to pay a higher interest rate because of them. Any help appreciated. Thanks

Hi All, I am trying to get any information possible on the removal of Settled Accounts that were in good standing from the main credit agencies. I used a well known payday loan company back in 2013 and rolled over the loan a few times and always paid early and in full. Never late and no negative info at all. However fast forward 3 years , I am trying to secure a mortgage and have been refused due to having 6 entries from a specific payday loan lender. Even though they are all settled and paid and closed they underwriters see that as there were 6 entries, that I am a risk !! I have a good credit score and this is the only negative. This is causing me to have to look through other "brokered" lenders who all want to charge fees and I am looking at a higher interest rate also. It crazy that I borrowed and paid back on time and still penalised for it. Can any one give me any advise on how I can persuade the payday lender to remove the settled accounts from my files?? As its causing me financial issues if I have to pay a higher interest rate because of them. Any help appreciated. Thanks -

Hi, My mother in law has accepted an offer on her house and all parties are ready to exchange. HOWEVER a charge on her property remains which was put in place in 1989 as security for £5000 due to her ex husband, a sort of loan agreement. This has never been repaid so the charge remains and ex husband passed away last year. This charge has now passed on to one of his sons who has signed a DS1 to have the charge removed but has not stated that he accepts the £5000 on the form. the conveyancing solicitor will not have the charge removed until they receive written confirmation from him to this effect as it is a legal undertaking by them and should he dispute the amount they are liable. The son is incredibly difficult to get hold of, has no UK bank account, lives in Spain address unknown. So, gridlock. Does anyone have any suggestions? Its very serious now as everyone awaits his signature in order to continue with the sale. Many thanks.

-

Hello Folks, I have about 4 Defaults on my credit report. A friend told me i can negotiate by offering 10% of the money owed to each of them. In turn, they will remove my name from credit agencies. Is this true? Please assist.

-

Back in 2010 I took a pdl with debitcardloans ltd - subsequently defaulted and then a ccj was issued - however the pdl has now been dissolved so i can not raise a complaint with them for not carrying out proper affordability or reference checks. I'd ideally like to get the ccj removed as otherwise its on my file till 06/2017 - is there anyway to get it removed as FOS say they can't do anything

Back in 2010 I took a pdl with debitcardloans ltd - subsequently defaulted and then a ccj was issued - however the pdl has now been dissolved so i can not raise a complaint with them for not carrying out proper affordability or reference checks. I'd ideally like to get the ccj removed as otherwise its on my file till 06/2017 - is there anyway to get it removed as FOS say they can't do anything -

Need removal of Ex from Property/mortgage deeds

HP Mum posted a topic in Mortgages and Secured Loans

Hi Am asking this on behalf of a friend: Barclays Mortgage In joint names of man (friend) and his ex partner (not married; now living with someone else). She left him and the property in 2007. He has continued to make mortgage payments (repayment & Interest / apx 8 years to run). She has made NO payments since 2007. (He has also taken care of 5 kids) He wants to get her name off the deeds and mortgage and he wants to sell. She has disappeared. How can he resolve this? He also doesn't want her to benefit from the increase in property value since 2007 !! Mostly because she left him and has contributed big fat 0 ever since.... Does anyone have any advice please ?? -

Payday Loans Default Removal

johnukccj posted a topic in PayDay loans and Short Term loans - General

After doing some reading i realise that it is futile to get defaults removed from my credit file. I am looking to get a mortgage next year, my credit file would have been clear by next year. I logged into my credit file yesterday to find two PDL defaults had appeared on my file. [ATTACH=CONFIG]59244[/ATTACH] This is obviously a pretty bad thing so i need to do all i can to remove them if at all possible. I am looking for a Full and Final Letter template to send them and couldn't see one in the document section. Can anyone help me draft one? CASHEURONETUK,LLC and PRA GROUP (UK) LIMITED Note one of the default is zero balance for some reason :S Any help would be appreciated lots. -

Hi All, I was wondering if someone could help me please as I am a bit confused as to Settled accounts and dates they are removed. I have managed to settle all my debts finally and I am trying to be realistic when I will be able to apply for a mortgage so trying to work out dates etc. There are 8 showing as Settled and 3 credit accounts as up to date and have't had any issues. Could you tell me how long a settled account stays on my file for is it 6 years? If so when is the date from? Is it Default date? of Satisfied Date? or any other I haven't thought of. Also if anyone knows, now they are settled does this increase my chance of getting credit or will be it once they are gone? I repaid them in November last year mainly, so its been almost a year Really value your thoughts, thank you.

-

I have been putting a lot of creditors off for over a year now but the defaults are really starting to hurt. I want to take on Barclays first as they sent a copy of a T&C booklet as their s78 response (as I know they do quite a lot). I also asked them under pre-litigation discovery and data protection laws to provide me with a full and exact copy of a signed agreement and they haven't bothered. I want to issue against them and had a quick look around the site to see if there are any template POCs I could use as I seen a good one around somewhere but cannot find it now. I need help with the particulars of claim. Thanks.

I have been putting a lot of creditors off for over a year now but the defaults are really starting to hurt. I want to take on Barclays first as they sent a copy of a T&C booklet as their s78 response (as I know they do quite a lot). I also asked them under pre-litigation discovery and data protection laws to provide me with a full and exact copy of a signed agreement and they haven't bothered. I want to issue against them and had a quick look around the site to see if there are any template POCs I could use as I seen a good one around somewhere but cannot find it now. I need help with the particulars of claim. Thanks. -

Hello, I have a problem with Marston Group bailiff and not sure how to approach it, any help will be much appreciated. Never dealt with a bailiff before so this is completely new to me.... Long story short: A bailiff knocked on the door at my previous address where I used to live and left a removal notice with two reference numbers. It says that the client is Borough. I'm thinking two PCNs that I didn't pay. In the last year I changed my name and address and didn't really keep on top of my debt. Now on the notice it states that I owe them nearly £600 I don't know what to do and I'm really scared to ring the bailiff... Plus the bailiff told my friend that he will visit me at work (somehow he knew where I worked) so I'm absolutely petrified! If someone could please advise me how to approach it I'd be very grateful.

Hello, I have a problem with Marston Group bailiff and not sure how to approach it, any help will be much appreciated. Never dealt with a bailiff before so this is completely new to me.... Long story short: A bailiff knocked on the door at my previous address where I used to live and left a removal notice with two reference numbers. It says that the client is Borough. I'm thinking two PCNs that I didn't pay. In the last year I changed my name and address and didn't really keep on top of my debt. Now on the notice it states that I owe them nearly £600 I don't know what to do and I'm really scared to ring the bailiff... Plus the bailiff told my friend that he will visit me at work (somehow he knew where I worked) so I'm absolutely petrified! If someone could please advise me how to approach it I'd be very grateful. -

p3t3r wrote: The Notice Of Removal Of Implied Right Of Access - this is a perfectly valid notice, - my opinion of this is backed up by the ruling from Judge Pugh which is shown earlier in this thread. The notice is akin to 'No Cold Callers' notices which are supplied by various police forces, councils etc. In relation to bailiffs, the notice is not considered to be valid. Firstly, there is no implied right of access for a bailiff since it is an explicit right. The bailiff has the right to attend the property and as such ignore the notices. IMPORTANT: Anyone relying on this notice to get rid of the bailiff is more likely to suffer financially since they are presumably under the illusion that such a notice would simply get rid of the bailiff. In this instance, the notice is absolutely useless because the bailiff does not have an implied right whatsoever, the bailiff has an explicit right - which is backed up by UK legislation which affords such right to the bailiff. Again, this is backed up by Judge Pugh. So, whilst the notices are akin to 'no cold callers' notices and apply to the vast majority of people, the notices do not apply to people who have a legal right to attend your home. The bailiff has a legal right in UK law to attend a debtors home. The reliance on such notices by individuals can lead to a dangerous scenario since the individual is under the false illusion purported by FMOTL that the notices are valid. Again, to put it simply, the notices are not valid to anyone who has a legal right to attend a home - and this includes bailiffs who are given the legal right to attend a home. Now, turning to a possibility as to how the notice is valid against bailiffs. EU law, ECHR, human rights... Lets take an example of council tax. If a debtor can not pay council tax, then their ability to pay should be assessed by a court. My opinion: If the person does not have an ability to pay, then allowances should be made by the court. In no circumstance should a liability order be granted on a person who does not have an ability to pay their council tax since as this is perverse! There is absolutely no point in instructing bailiffs to attend a debtors home and therefore significantly increase the debt by adding on bailiff fees. However, in the case of a debtor who can afford to pay but does not pay, then bailiffs should attend. IMO, bailiffs should be used as a last resort against the debtor who refuses to pay where all other possibilities have been exhausted such as deductions from benefits, salary deductions etc. There are IMO various EU laws which would help with the validity of the Notice Of Removal Of Implied Right Of Access. Firstly, the right to a fair trial. There is absolutely no fair trial in the scenario of council tax where liability orders are processed almost automatically, 'rubber stamped' by the Judges. This goes against ECHR article 6, the right to a fair trial. If the debtor has not had a right to a fair trial as defined by ECHR article 6, then the bailiff should be informed of this in conjunction with ECHR article 8, the right of respect for his home, family etc. The debtor should make their case known to the bailiff and the bailiffs client. If the bailiff does not leave the property after being informed of ECHR article 6 and article 8, then it could be argued that the bailiff is in violation of those applicable laws. This is my opinion and until someone actually tests the legality of this in a court, then it is just that, an opinion. A (BBC?) report which can be seen from one of my links in this thread from a few years ago states that the use of bailiffs should decrease since the human rights act. Unfortunately, I feel the reverse has happened in the fact that liability orders are rubber stamped and as such bailiff use has increased rather than decreased. Again,I reiterate that use of such notices are ineffective against bailiffs and other people who have a legal right under UK legislation to attend the home of a debtor. However, as Judge Pugh has outlined, the notices are valid toward those people who do not have a legal right to be at the property. Usage of such notices used in conjunction with that of various EU laws and human rights should IMHO prevent the bailiff from attending the property until such time that a FAIR TRIAL (article 6 ECHR) has occurred. The debtor should then escalate their case using ECHR and EU law in order to provide remedy. Summary: Notice of implied right of access is perfectly valid, but not valid against people (bailiffs) who have an explicit legal right to attend. However, such right should be examined under EU law since I feel that more often than not, article 6 has been violated (fair trial) which would then lead to article 8 violated. EU law / ECHR - This trumps UK law! Whilst people may have an explicit right under UK law to attend a debtors home, this is not necessarily so using EU law. Discuss.

p3t3r wrote: The Notice Of Removal Of Implied Right Of Access - this is a perfectly valid notice, - my opinion of this is backed up by the ruling from Judge Pugh which is shown earlier in this thread. The notice is akin to 'No Cold Callers' notices which are supplied by various police forces, councils etc. In relation to bailiffs, the notice is not considered to be valid. Firstly, there is no implied right of access for a bailiff since it is an explicit right. The bailiff has the right to attend the property and as such ignore the notices. IMPORTANT: Anyone relying on this notice to get rid of the bailiff is more likely to suffer financially since they are presumably under the illusion that such a notice would simply get rid of the bailiff. In this instance, the notice is absolutely useless because the bailiff does not have an implied right whatsoever, the bailiff has an explicit right - which is backed up by UK legislation which affords such right to the bailiff. Again, this is backed up by Judge Pugh. So, whilst the notices are akin to 'no cold callers' notices and apply to the vast majority of people, the notices do not apply to people who have a legal right to attend your home. The bailiff has a legal right in UK law to attend a debtors home. The reliance on such notices by individuals can lead to a dangerous scenario since the individual is under the false illusion purported by FMOTL that the notices are valid. Again, to put it simply, the notices are not valid to anyone who has a legal right to attend a home - and this includes bailiffs who are given the legal right to attend a home. Now, turning to a possibility as to how the notice is valid against bailiffs. EU law, ECHR, human rights... Lets take an example of council tax. If a debtor can not pay council tax, then their ability to pay should be assessed by a court. My opinion: If the person does not have an ability to pay, then allowances should be made by the court. In no circumstance should a liability order be granted on a person who does not have an ability to pay their council tax since as this is perverse! There is absolutely no point in instructing bailiffs to attend a debtors home and therefore significantly increase the debt by adding on bailiff fees. However, in the case of a debtor who can afford to pay but does not pay, then bailiffs should attend. IMO, bailiffs should be used as a last resort against the debtor who refuses to pay where all other possibilities have been exhausted such as deductions from benefits, salary deductions etc. There are IMO various EU laws which would help with the validity of the Notice Of Removal Of Implied Right Of Access. Firstly, the right to a fair trial. There is absolutely no fair trial in the scenario of council tax where liability orders are processed almost automatically, 'rubber stamped' by the Judges. This goes against ECHR article 6, the right to a fair trial. If the debtor has not had a right to a fair trial as defined by ECHR article 6, then the bailiff should be informed of this in conjunction with ECHR article 8, the right of respect for his home, family etc. The debtor should make their case known to the bailiff and the bailiffs client. If the bailiff does not leave the property after being informed of ECHR article 6 and article 8, then it could be argued that the bailiff is in violation of those applicable laws. This is my opinion and until someone actually tests the legality of this in a court, then it is just that, an opinion. A (BBC?) report which can be seen from one of my links in this thread from a few years ago states that the use of bailiffs should decrease since the human rights act. Unfortunately, I feel the reverse has happened in the fact that liability orders are rubber stamped and as such bailiff use has increased rather than decreased. Again,I reiterate that use of such notices are ineffective against bailiffs and other people who have a legal right under UK legislation to attend the home of a debtor. However, as Judge Pugh has outlined, the notices are valid toward those people who do not have a legal right to be at the property. Usage of such notices used in conjunction with that of various EU laws and human rights should IMHO prevent the bailiff from attending the property until such time that a FAIR TRIAL (article 6 ECHR) has occurred. The debtor should then escalate their case using ECHR and EU law in order to provide remedy. Summary: Notice of implied right of access is perfectly valid, but not valid against people (bailiffs) who have an explicit legal right to attend. However, such right should be examined under EU law since I feel that more often than not, article 6 has been violated (fair trial) which would then lead to article 8 violated. EU law / ECHR - This trumps UK law! Whilst people may have an explicit right under UK law to attend a debtors home, this is not necessarily so using EU law. Discuss. -

I've been reading Carey v HSBC with horror. I contacted [edit] solicitors. They tell me that a signed application form containing the prescribed terms and conditions was an executed agreement. This has me really worried because Arrow Global has also told me this and want cash off me pronto. The real problem is that I didn't know anything about the CCA 1974 until after Arrow had a charging order against me. When I found out about 3 years ago I stopped making payments to them. I told them why. Arrow quote Carey v HSBC and has said they want cash from me or they are going to force a sale of my house. The CAB told me to contact [edit] solicitors. I showed them the copy application form from 2000. [edit] said this was legible and as far as they were concerned it was a legally enforceable agreement as the terms and conditions seemed legible and prescribed. I've attached page 2 of the application form from 2000 containing what [edit] has said is the prescribed terms. I cannot read these terms. Wonder if anybody can. If you can read them do you think they form a legally enforceable agreement. This application form is what the original creditor sent me as part of a SAR and a CCA check. At the time I told them I couldn't read the terms and asked for a clear legible copy. I'm still waiting. Recently Arrow told me they would send me a clear legible copy but I'm still waiting. Anybody got any advice as people on this forum tell me that an application form is not an enforceable agreement but this was said before Carey v HSBC.

-

Hi there, 18 months or so ago I was going through some hard times and stupidly relied upon Payday loans to keep me afloat. Most of the loans (had around 10 in total, all with Wonga) were around 500 pounds and all were paid off before the due date. 5 years before all of this I had had some trouble with credit and unfortunately got a default from a lender meaning I was struggling to get credit anywhere else. At the time of signing up to Wonga they were running their 'Wonga will do wonders for your Credit File' campaign (http://www.dailymail.co.uk/news/article-2237712/Wonga-sorry-sending-emails-implying-loans-wonders-peoples-credit-ratings.html) and saw them as a kind of win/win for me, enhancing my credit file as well as tiding me over. Now 18 months on, having a perfect credit file (old default had dropped off and been running a credit card perfectly for the last year as well as various utilities) I am in a position to obtain a mortgage. So I've looked at my credit file and lo and behold there are 10 SETTLED Wonga accounts listed on there. Having read through the forums, from what I can gather this will not help me out at all with any sort of application. I've approached Wonga about the removal of these entries as I believe they will hinder any chance of me obtaining credit, which was totally against their advertising campaign at the time of me signing up but they have basically fobbed me off with a blanket 'We have to keep an entirely accurate CRA log'. I would like to however take this further, what would my next steps here be? Would it be a solicitors job from here on in or should I contact the CRA's directly? Any help would be greatly appreciated. Thanks!

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS