Showing results for tags 'minicredit'.

-

I defaulted on an old minicredit loan in 2012 and the default is due to drop off in 2 months it's now with opos/kapama I have not paid anything or contacted them in nearly 3 years. ive found a few emails in my inbox about the debt, most recently a few weeks ago telling me it is now in the pre-legal stage they sent me a statement loan amount: £100 interest chsarges: £121 debt collection charges: £100 default charge 1: £25 default charge 2: £50 attempt charges: £685 i've paid £20 towards the debt according to the statement through token payments (sounds about right) but the amount owing is still over £1000 for a £100 loan i'm guessing as the default is dropping off soon this is the moment where they will try anything including a ccj to recoup some monies? especially if they dont hear anything from me. currently trying to sort all my debt problems out so.... what would you reccomend as my next course of action with this?

-

Hi there I wanted to make a complaint about loans issued to me by Minicredit back in 2012 (ish). I know they have been wound up but when I went to Opus/ Kapama they said they have no record of them? I have read on here though that they are all the same company so I am confused.com. Is there any point in going to the FOS if they claim to have no record or is this a known avoidance tactic? Also does anyone know who was the appointed Administrator for the MC wind up / dissolution as I thought I could possibly trace it through them but I am struggling to find this information online (even at companies house). Any help would be much appreciated. Thanks

-

Good afternoon. I am back under anew guise. I posted last year about a Minicredit default a £200 that ended up a £1200+ one after non payment. I hate the companies & now the default stands at £522 with Kapama & shows 5 years of non payment on my noddle file but is not present on my Experian or ClearScore files. It's on there till march 2018. Do I let it slide, I've still been getting voicemails from Opos demanding to speak to me (I blocked their numbers so that's their best way of trying to get in touch with me) for all I care they can do 1. Will that default disappear in a years time. I've a couple of other issues but that's 1 I'm looking to clear up for now. Thanks in advance Rob

-

Thanks for everything you do here – I hope you might be able to help with Opos and Kapama. Although I've read lots of threads about them, I'm struggling with some particular parts of my situation. Brief background – in 2013, lots of foolish unaffordable payday loans to pay more payday loans, including a written off Wonga. Most now dealt with, with my credit file looking like it will be clear by 2020. A few monthly payments still going, including to Opos for a MiniCredit debt purchased by Kapama - notice of assignment issued in late January 2015. The initial Minicredit loan was £450, with Kapama/Opos demanding over £1600. I've been making £20 monthly payments for 18 months, and so have nearly paid the original balance. There is no default listed for MiniCredit on my credit file. The loan is listed as an 'advance against income' with Kapama as the lender and an arrangement to pay – with over £1200 outstanding. I've come to a point where I'm reviewing my financial situation in mind of - first, a reduced income coming up because I'll be retraining in a new career - second, I want to be in a position to get a mortgage when my file is clear. That in mind, the £20 a month is no longer affordable, but as a default hasn't been recorded on that loan, I'm really concerned Opos/Kapama would register one if I stopped the arrangement now, setting back my file several (important) years. Having read through forums and taken a friend's advice, I sent them an email last week referring to the FCA ruling regarding MiniCredit's lending (link not here) but have not received a reply. The crux of that was that if the debt hadn't been transferred to Kapama by December 2014 it should be written off –*they say it was, but I have the notice of assignment – which was sent by email at the end of January 2015. The main questions I have: Can they register a default now? Should/can I stop making payments? They're currently being taken from a debit card by Opos. How should I proceed? Should I continue to complain on the grounds of that FCA ruling? Do you have any contacts at Opos/Kapama better than the general enquires address? I know there's a bit of duplication there - but as I've paid back so much of the original loan, the credit file listing and the potential relevance of MiniCredit's shutdown, I'm really not sure where I stand. Thanks in advance – I really appreciate it.

Thanks for everything you do here – I hope you might be able to help with Opos and Kapama. Although I've read lots of threads about them, I'm struggling with some particular parts of my situation. Brief background – in 2013, lots of foolish unaffordable payday loans to pay more payday loans, including a written off Wonga. Most now dealt with, with my credit file looking like it will be clear by 2020. A few monthly payments still going, including to Opos for a MiniCredit debt purchased by Kapama - notice of assignment issued in late January 2015. The initial Minicredit loan was £450, with Kapama/Opos demanding over £1600. I've been making £20 monthly payments for 18 months, and so have nearly paid the original balance. There is no default listed for MiniCredit on my credit file. The loan is listed as an 'advance against income' with Kapama as the lender and an arrangement to pay – with over £1200 outstanding. I've come to a point where I'm reviewing my financial situation in mind of - first, a reduced income coming up because I'll be retraining in a new career - second, I want to be in a position to get a mortgage when my file is clear. That in mind, the £20 a month is no longer affordable, but as a default hasn't been recorded on that loan, I'm really concerned Opos/Kapama would register one if I stopped the arrangement now, setting back my file several (important) years. Having read through forums and taken a friend's advice, I sent them an email last week referring to the FCA ruling regarding MiniCredit's lending (link not here) but have not received a reply. The crux of that was that if the debt hadn't been transferred to Kapama by December 2014 it should be written off –*they say it was, but I have the notice of assignment – which was sent by email at the end of January 2015. The main questions I have: Can they register a default now? Should/can I stop making payments? They're currently being taken from a debit card by Opos. How should I proceed? Should I continue to complain on the grounds of that FCA ruling? Do you have any contacts at Opos/Kapama better than the general enquires address? I know there's a bit of duplication there - but as I've paid back so much of the original loan, the credit file listing and the potential relevance of MiniCredit's shutdown, I'm really not sure where I stand. Thanks in advance – I really appreciate it. -

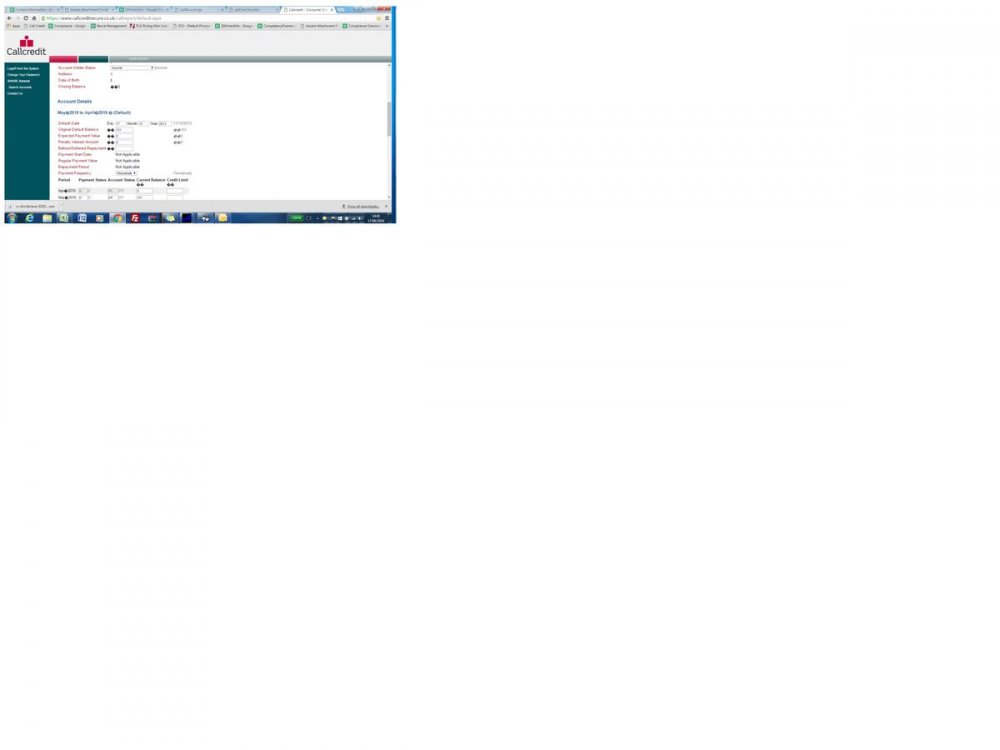

Hi All, New to the CAG and really need some experienced help with my ongoing battle with this company. I first submitted a Formal Complaint against Opos Limited in January 2016. This went to the Financial Ombudsman after I disagreed with their final response. The adjudicator advised that where Opos Limited is the debt collector and Kapama is the debt owner, he didn't think Opos Limited's collection practices were wrong, but he did advise me to send in a second complaint to Kapama about irresponsible lending. The original loan was for £100.00, and with charges etc. it ended up at £300.50. This is where things get interesting... I made a payment to Opos back on the 18th October 2014 for £149.45. When I looked at my credit report on Noddle, the 'Account Default Date' for this Minicredit loan was exactly the same I made a payment to Opos. When the adjudicator questioned them on this, apparently that date was incorrect and Minicredit defaulted me in November 2012. Please bear in mind that I actually took out the Minicredit loan in July 2013 so this definitely isn't correct! Anyway, to resolve the first complaint we agreed a settlement of £100.00 which I paid in full two days after the adjudicators decision. This was 22nd April 2016. Around the same time I sent the second complaint to Kapama for irresponsible lending. On receipt of my second complaint, Opos's Compliance Manager sent me an email on the verge of bribery saying that IF I withdrew my second complaint, she would remove the footprint of this loan from my credit file as a way of resolution. I got in touch with the adjudicator at the FOS about what they offered and he said he is personally going to call them and say it's unacceptable. Their compliance manager said she was going to update my credit file within 28 days since the settlement was received. I check on my credit report at the end of April and there is now new information... Account Default Date is 17th December 2013 with the account showing a balance of £51.45 outstanding? As you can imagine I am now fuming with this. So I phone them, and they make up some sorry excuse that they never received the settlement form (despite having an email from their compliance manager saying the account is settled). When I mentioned court they hung up on me so I emailed them with a furious message. I haven't been satisfied from the beginning that Minicredit defaulted me in the first place, so now I have opened a case with the Information Commissioners Office which they are investigating. On Wednesday 15th June 2016, I received a final response to my second complaint. This time they offered to refund around £50.00 as a gesture of goodwill and decided not to uphold my complaint. (I believe this is very weird considering they had already offered to remove the default without looking further into the complaint and have now offered a refund). They also said that they updated my credit file information through Callcredit and that this is not the same as Noddle and the information may not have shown on Noddle as it takes longer to update. I have not accepted this and again have put it in to the FOS. In response to their Final Complaint I asked a series of questions regarding the default, dates and why they have offered me the above but not upheld my complaint. They responded that they will liaise with the FOS and did not answer any of my questions. Yesterday I decided that I would pay for a subscription to Callcredit (Credit Compass) to see what my file on there shows in regards to this default seeing as this is where they say the updated the information. After looking everywhere for this account, it is NOT on there. Not in settled or outstanding. So I emailed the Compliance Manager again and said that this account is nowhere to be found and yet this is where they supposedly updated the information, and not through Noddle. She emailed me back with a screenshot of her computer with the screen showing my file details with the '£0' balance etc. (I think this could have been a big mistake for them) On that screenshot it shows Account Details 'May 2015 to April 2016'. It also looks like the boxes are available for them to amend themselves! I thought that they notified CRA's to enter personal information like that, I'm not sure if creditors are allowed to do this and are able to amend information freely themselves? What I really need some advice on is surely if Minicredit defaulted me, it would be a case of a name change on the account on my credit file back in 2013 or whatever date they supposedly defaulted me. Minicredit passed over their accounts in December 2014 and on that screenshot they're showing account details from May 2015!? I have phoned Callcredit and they asked me to send a copy of the default showing on Noddle, as well as copy of that screenshot they sent me. I have also fowarded this on to the ICO and FOS. I really apologise for the huge essay but I would like to share my story about these companies to you all. I would advise everyone that has had a default from this company to check the dates etc. If anyone can give me some advice I'd really appreciate it as I'm willing to go all the way with this. I've attached the screenshot for all of you to see. I have loads of emails for evidence and the responses so if you need to see them please let me know. I have probably missed a few things out but this is the main part of it all. Thanks

-

.thumb.jpg.bf2f59e5260173230834ce3ad8015900.jpg)

Minicredit / Kapama & Opos... Worrying Situation

fkofilee posted a topic in Debt Collection Agencies

Hi Guys Well its not often I need advice haha and this one is a right mess to deal with. Basically as some know, I ended up suffering from Identity Fraud... And im still dealing with it today. So Minicredit wrote of a Balance of £1k and determined themselves it was fraud. However OPOS purchased the account and we started to go through this whole situation of dealing with a 3rd party for a company that doesnt exist. for the 3rd time in a year and a half, I got an email as per below; So I had already told them 3 times already that the account was closed from their end, etc and that I shouldnt be hounded for this... But alas, they still do hound me. I threatened them with a C+D notice last year, and still they persist even though Minicredit confirmed the account was closed due to Fraud etc and OPOS even closed their account. Today i also recieved a statement from them, and this is a shocker; Period Covered: 25/02/2015 to 25/02/2016 Your Account Summary Loan Amount £100.00 Interest Charges £118.00 Debt Collection Charges £100.00 Default Charge 1 £25.00 Default Charge 2 £50.00 Attempt Charges £670.00 Paid £0.00 Adjusted £0.00 Outstanding Balance £1,063.00 £670 in attempt charges?!?!?!?! Anyhow the response i got back last year was to the tune of the below? Any advice on this one? Im really stuck. The original complaint was resolved but its still apparent that it hasnt and the 6 months to refer to the FOS have passed. I am also concerned because if an account is shut down due to fraud then no further balance remains, however the FCA confirmed to me that I shouldnt be getting statements for an account that doesn't exist no longer where I am not a debtor? And Breathe........... -

Hi I am being pursued by Opos for a minicredit payday loan taken out in March 2012 for £150 which was to be repaid in 25 days. Opos are claiming around £764 saying that the original amount owed was £1189 - they came on to me back in 2013 and I paid Opos a total of £400 by installments. Last payment I made was in January 2014. Opos has sent me a 'statement' showing the following: Status Debt collection Loan sum £150 Order date 07. March 2012 Interest £238.5 Due date 01. April 2012 Penalty £80 Attempt fee £640 Debt expenses £100 Total £1208.5 Balance £1189 I see that minicredit ceased trading in 2014. I have emailed Opos asking how the above charges are calculated etc. No reply as yet. What should I do? Fred

-

Hi, Ive been making payday loan complaints which started in December have so far had 3 successes and about to send some to FOS. However im confused about MiniCredit. Their website is still fully active? I know there is a statement with regards to them no longer trading at the bottom of their website with a link to the FCA, however their website still updates daily and from what i can see will let you make applications? They have links to Kapama and Opos etc. Im pretty sure that they must still be in operation but I cant find any post that confirms that they are defenitely not so wandering if anybody can point me to this please? If they are still lending in some capacity then im sure there must be lots of people who have tried but failed to contact them with regards previous lending and their ridiculous default charges! Thanks

-

Hi I have a 200 page complaint about minicredit I sent to them- but obviously no response as they have closed down What should i do- or who do i send to? no one is chasing the money

-

Hi all. A few years ago, I got myself into a mess with various payday loans and have spent the last couple of years paying them all off. Earlier this week I received an email from a company called "kapama credit" stating an account of mine had been passed onto them from Opos. The loan in question is from minicredit. A loan for £100 of which I only received £80. Due to being in the midst of my payday loan mess, this wasn't paid back.. As my head was firmly stuck in the sand, I did nothing. I was in touch with opos back in 2012 and at one point was offered the chance to pay a settlement of £150 which ended up not paying. The email i received this week states I owe over £700. In a panic, I offered them the £150 again, which they refused, stating the minimum they can accept is £392!! I then asked them for a breakdown of the account and this is their response: Principle - £59.89 Interest - £69 Attepmted payment fees - £555.50 Debt collection fee - £100 I want this sorted asap but not sure of my next steps. How much of this do I technically owe?

Hi all. A few years ago, I got myself into a mess with various payday loans and have spent the last couple of years paying them all off. Earlier this week I received an email from a company called "kapama credit" stating an account of mine had been passed onto them from Opos. The loan in question is from minicredit. A loan for £100 of which I only received £80. Due to being in the midst of my payday loan mess, this wasn't paid back.. As my head was firmly stuck in the sand, I did nothing. I was in touch with opos back in 2012 and at one point was offered the chance to pay a settlement of £150 which ended up not paying. The email i received this week states I owe over £700. In a panic, I offered them the £150 again, which they refused, stating the minimum they can accept is £392!! I then asked them for a breakdown of the account and this is their response: Principle - £59.89 Interest - £69 Attepmted payment fees - £555.50 Debt collection fee - £100 I want this sorted asap but not sure of my next steps. How much of this do I technically owe? -

Ok, I thought Minicredit had been dissolved, looking at their website now, they are back and lending??!?!? HOW

-

Can somebody help please, I'll be honest I've not really got a clue where to start to deal with this so I may as well start with my situation. I'm now 23 years old ,Back in 2012 around Christmas time I stupidly took a minicredit payday loan the usual 100 pound loan of which I only received 80. In the following weeks I lost my job as I worked for a self employed builder who due too work had too move over 3 hours away so I couldn't keep the job. I panicked and as a result took a wonga loan out as well which I have since fully settled. I managed too agree too a payment plan with wonga but always found minicredit hard too deal with. They kept adding charges, I couldn't afford too pay just those never mind the actual debt. A combination of this situation and being unable too find work made me suffer from severe depression and anxiety. After the debt reached over £800 I just buried my head in the sand and hoped it would all just go away. September 2014 i finally found solid work and became much happier but still ignored the debt. Finally now in March this year I thought it would actually be gone as I checked my credit file for minicredit it wasn't there they removed all defaults as well. I have just checked my credit file again too see I now owe £1041 too Kapama for what is the £100 minicredit loan. I searched google for help and found this forum. I would really appreciate anybody's help who has been in a similar situation or knows how I can deal with it I really don't want too feel down over debts again as this is the only thing I now owe. Sorry for the long post hard too explain over short text. Thank you

-

Hi there, Just wondered where I stand with Minicredit. My situation seems to be broadly similar to others on here, but I could do with some relevant advice here. My wife took out a loan of £100 with Minicredit in January. She was charged the FastAdvance TransmissionFee of £19.50 so only received £80.50 in her account. In February, she wrote to Minicredit and offered a monthly payment plan of £30 per month and enclosed a postal order for £30. She sent a 2nd letter in March along with another postal order for £30. On return home after posting the 2nd letter, she received a letter stating that Minicredit did not accept cheques, and could she cancel the cheque. As the postal order hadn't been returned, my wife and I have no idea what has happened to the postal order. Minicredit continued to debit our account under CPA even though we had asked the bank to cancel the CPA. These payments have since been refunded to out account. I complained in March on my wifes behalf, but Minicredit basically ignored my comments and wrote to my wife offering her payment plans. I wrote again in May and they ignored my letter, stating that the account was being passed to OPOS wih a balnce of £844. Since then, we have had nothing but harrasement by OPOS. Since the period has elapsed, I escalated the complaint to FOS, but based on the information they received from Minicredit, they 'reduced' the balance from £844 down to £382. FOS accepted this despite my comments about th postal orders and the fact that the statement sent by Minicredit was inomplete. I am getting nowhere with FOS and the postal orders still have not been applied to the account. I have also since discovered that a default has been placed on my wifes credit file in May, despite me raising complaints with them in March and May. The default is for £418 despite the loan amount being credited to my wifes account being only £80.50. Minicredit have not applied the postal orders to my wifes acccount or returned them to her. I just wondered where I go from here. I can post the transcript that Minicredit have sent to FOS if need be. Many thanks.

-

hardly any more excuses needed but another tale of woe...even the ombudsman has had enough! http://www.ombudsman-decisions.org.uk/viewPDF.aspx?FileID=63793 FYI - I've written to the FCA asking if Minicredit will be required to put funds aside to deal with any outstanding complaints with FOS (I've a current complaint with FOS about Minicredit). will keep you all posted on response although the initial feedback is all very generic, just pointing me to the Voluntary Requirement notice on the FCA website

-

I'm writing on behalf of my partner who took out a loan with Minicredit 2012/2013. After receiving all the usual threatening letters and the ridiculous charges that was added by Minicredit/OPOS, he set up a DMP with Step Change giving the outstanding balance of the debt at approx £700+. Now, having read these forums it is very clear that the charges added are unenforceable. He emailed OPOS asking for an up to date balance and a full break down of the debt. The reply.. Balance : £240.33 Principal : £100 Interest : £85.00 Penalty 1 : £25.00 Penalty 2 : £55.00 Attempt Fee : £380.00 Debt Collection Fee : £100 I believe I am correct in stating that only the principal loan, the one months interest and a single penalty fee is what is actually owed which would equal £210. He has already paid to date £58.87 through his DMP so therefore he owes £151.13 now. I have no idea where the £240.33 has come from, probably Derek falling on his calculator? Am I correct? How on earth do I go about getting OPOS to remove the unenforceable charges? An email template would be perfect.

I'm writing on behalf of my partner who took out a loan with Minicredit 2012/2013. After receiving all the usual threatening letters and the ridiculous charges that was added by Minicredit/OPOS, he set up a DMP with Step Change giving the outstanding balance of the debt at approx £700+. Now, having read these forums it is very clear that the charges added are unenforceable. He emailed OPOS asking for an up to date balance and a full break down of the debt. The reply.. Balance : £240.33 Principal : £100 Interest : £85.00 Penalty 1 : £25.00 Penalty 2 : £55.00 Attempt Fee : £380.00 Debt Collection Fee : £100 I believe I am correct in stating that only the principal loan, the one months interest and a single penalty fee is what is actually owed which would equal £210. He has already paid to date £58.87 through his DMP so therefore he owes £151.13 now. I have no idea where the £240.33 has come from, probably Derek falling on his calculator? Am I correct? How on earth do I go about getting OPOS to remove the unenforceable charges? An email template would be perfect. -

Afternoon All, I have been paying these people through Payplan for a few years now and I am coming to the end of the plan. I contacted Opos Ltd to see what the balance was and to make sure it matched the Payplan estimate. To my shock I found that I still owed over £1000 after having already paid over £500 on a £100 loan. Opos tell me that the interest and charges were added to the debt by Minicredit before Opos took over the debt. I have now emailed them giving them 7 days to clear the debt otherwise I will be taking the matter to trading standards and the FCA. I have not asked them to refund anything just to clear the balance. Is there a route through the courts I can take if nothing works ? Any help would be appreciated. BTW. I will keep you informed as to what happens as I am going after a few companies, its become a matter of principal now

-

Hello all, I'm new to the forums so please bear with me. Firstly, let me request that judgemental posts and posts advising me what "a ******" I am be kept in your head. This entire problem was cause by terrible judgement on my part. Let's say, hypothetically, I obtained a £100 loan from Minicredit by giving them false employment information. Gave them a normal monthly wage, the company's full and correct contact information, and falseified NO documents and made NO effort apart from filling in a fake wage and real company contact information. I could not pay the loan on time. I actually applied half out of curiousity, and half out of sheer desperation of not being able to eat and heat, having exhausted my assistance from the social fund. When the money was awarded to me, I spent it believing that I would pay it back when my next benefit payment went in. I was then sanctioned (the reason I dispute, but this is irrelevant) and could not pay. Anyway, to cut a long story shorter, my loan was due on October 15th 2012. I could not pay. I noticed the balance slowly (at first) increasing, so emailed Minicredit to ask they froze the interest (like Wonga did in the past, which I obtained lawfully, by the way), otherwise the part-payments I made would not actually lower the balance of my loan, not even a little bit, due to exponentially increasing interest. And charges, but I'll get to that. They of course refused. Minicredit eventually blocked my account, but continued sending me emails. You can't send a question to minicredit about a general enquiry without choosing from a drop-down list of questions. All of which end up in a (pathetic) automated reply email. If you log in (which, of course, I couldn't) you could send a custom question. I am skint (hence the reason for the stupid decision in the first place) and do not have a landline and hardly EVER top my mobile up. So I couldn't call the number on their site. This left me out of contact with them. Now, this is where I'd like to re-iterate: I know what I did was bloody stupid. But having said that, I still think the following is disgusting, as it would be the same for someone who wasn't dishonest. Initial loan: £100. They deducted a fee for "fast transfer" even though fast transfer is free, and I didn't see an option for any other kind of transfer, I definitely didn't select it manually. So I ended up with £85. Long story short by roughly Jan/Feb this year the balance had reached £1066. I cannot believe it. My irresponsible decision has left me with a debt I have absolutely no chance whatsoever of paying in a reasonable time-frame. It has been passed to Opos limited, who to be fair have a decent website and seem relatively professional. But I have some issues with them: 1. In about 3 weeks of constant emailing to [email protected] and a "Vicky Johnston", I have had about 2 maybe 3 replies. They do appear to be ignoring me. I also filed a dispute over the amount via their website's dispute form, as £1066 is surely unlawful, if not it's still quite immoral (I know, hypocritical of me, I agree). They've now sent me the "Intended action" email, threatening "Debt Recovery Service". 2. The reply I did have once from them asked me for income/expenditure. If I'm honest here, and tell them I am in receipt of only £55 local housing allowance and £71 Employment and support allowance, will they shop me for fraud? Will they report back to, or check with, Minicredit? Because Minicredit will tell them they thought I was working. I could do without being jailed for fraud. Again, I know I probably deserve it, but please believe me when I say the intention to pay was originally there. So in short: Do I give Opos the truth or will that be making a rod for my own back? I apologise for the length of this email, I am now very concerned that my stupid stupid idea has lead to me apparently facing very little option but to pay £1066 or end up in court for fraud. Please could somebody advise me on any ideas to perhaps get the amount down? Get a small repayment plan agreed? I have other debts but this is the largest and most worrying. Thanks VERY much to anyone who reads and considers replying.

-

hi, just noticed this article about minicredit http://www.google.info/forums/showthread.php?47704-Micro-Lend-Uk-Credit-Licence Was doing a bit of research as I have an FOS complaint against them for irrresponsible lending. Have got recent emails from the lovely Kristale. Has anyone got a loan from them recently? What happens my claim if they go out of business?

-

hello i checked my credit fine and saw an entry from microcredit for £500 back from 2012. I didnt not reconise the debt so i sent off the standard CCA letter with enclosed fee ect.. I got a letter back yesterday from micro credit. No signed agreement or statement as requested.. Just a load of junk advising i should go to the police if i think that someone has taken out the application in my name as it could be fraud.. bla bla bla.. anyone else received such a response?

-

Hello guys, to cut a long story short I took on a loan a month ago with minicredit or microcredit as they're also known as of £100 (wish I hadn't of now) but heres the deal. I set up a DMP with a charity called stepChange who are really helpful in helping me get through the whole process of sorting everything out so far. The thing is, a couple of my other creditors so far are all being cooperative about my current financial situation I am in except for minicredit(suprise,suprise). minicredit passed the debt onto another company called opos ltd, which i've already heard they are both the same company except with a different name. I get calls from opos, which I do not answer as I heard they are very unhelpful and threaten for you to pay up the amount with interest which is what I need help with. I rang up stepchange about this and I have emailed the new company details so that they transfer the account but they needed the outstanding balance, which I do not know how much it is to date as I only know what the balance of the loan was on minicredit account before they blocked my account I am unable to see how much interest and what not they are adding onto my balance. stepchange asked me if they had sent me any letters with the most up to date balance, I said no , they have only sent me text messages saying " dear bla bla please contact us back to talk about your account with my account number" which I gave to the charity. The only balance I could give to stepchange was £155 after being charged twice for late payment fees from minicredit. How do I find out how much my debt is with opos to date? should I write/call/email? which is the easiest method? and would it matter if I dont know the actual balance as I'm only willing to pay the £155 (that includes the interest and late payment fees) as I'm not made out of money, and ive got other creditors to pay off aswell. sorry for the long winded post but I really need help on what I should do next. ps. stepchange say that they are dealing with it so I guess i will leave it up to them now, i dont know if they will get this info for me instead of me having to chase it up, all they said to me is that if opos ring me pick it up and say that stepchange are dealing with it now and that they will send you an offer.

-

Hi, Any advice on how to proceed with my Minicredit issue would be greatly appreciated. I took out a £100 payday loan with them recently (the due date is not until the 20/7/2104). On Monday the 7th of this month i logged into my minicredit account and selected "repay early" (the due balance was £110.40) i hit the repay early button,got a pop up saying "are you sure" clicked ok and continued to the payment. My banks "verified by visa" box popped up,i entered my details and submitted the payment. The next pop i got was "payment declined insufficient funds on card" (or words very similar to that )....i knew i had more than enough in my bank to cover the paymemt. I phoned my bank (co-operative) and they confirmed that the payment to minicredit had been authorised and was pending. i then called Minicredit who said they declined to accept my early repayment due to my account details being incorrect with them...i followed the representive's request and re-entered my personal details on the minicredit site..he then assured me that the payment would then be manually processed by Minicredit and i would receive a text confirming the payment...all that has happened is that minicredit have debited a £1 from my card but so far not processed the £110.40. I have spoken to my bank and the £110.40 is now reserved for Minicredit (ie not available to me on my balance)...when i log into Minicredit i see my outstanding balance is increasing daily as the due date approaches.Anyway my fear is that they will attempt to debit my card on the 20th and then process the pending manual pending payment as well.I have had my bank place a "block" on minicredit accessing my account because as far as i am concerned i've paid them.my question is have i acted within my legal rights and should i now not get back in touch with minicredit? (my bank tell me that the only way they will be able to access my account is if i authorise a payment to them via the minicredit website). Sorry for such a long winded post but i just need to know if i have acted in the proper manner. Thanks, Gary.

-

I took out a Minicredit loan some time during 2011. It wasn't paid back and in no time at all increased from about £80 to over £800. I emailed them on numerous occasions using the info I'd gleaned from this forum and didn't receive one reply. They passed the debt on to someone else (can't remember who now) and then on to Opos. I was receiving emails from Opos for a good 18 months - 2 years asking me to contact them. Apart from the emails there was no other correspondence and no phone calls. And then quite recently it went quiet. Yesterday I received an email from a company called Allsquare and this was followed up with a message on my landline voicemail. This is a number I never even gave minicredit, so heaven knows where they've got this number from. The phone bill isn't even in my name and we're ex-directory, so I'm mystified (?) Does anyone have any experience with this company? I need to know what I'm up against as to what tactics to adopt in my approach, if any is made. I did a search on 'Allsquare' and 'Allsquare Law' in the search box on here but it throws up nothing. Just wondering if it's a new DCA on the block. A google search of their phone number 01628 200215 didn't enlighten me either. Thanks in advance.

-

Hi, Due to the demands of Christmas I stupidly took out two payday loans one with Minicredit and the other for Unclebuck. Both are due next week but there is no way I can afford to pay them back in full. I owe m.c. approx £300 and u.b. approx £200, I will offer them a reasonable repayment amount tomorrow via email. I have cancelled my debit card and instructed my bank to cancel the CPA on both. However I am terrified of the extortionate amount both of these lenders seem to add to loans if they default (reading other posts). I have learnt my lesson and just want to repay both but I expect these loans to escalate to huge amounts over time. Can anybody advise please on how to deal with these companies?? Thank you

Hi, Due to the demands of Christmas I stupidly took out two payday loans one with Minicredit and the other for Unclebuck. Both are due next week but there is no way I can afford to pay them back in full. I owe m.c. approx £300 and u.b. approx £200, I will offer them a reasonable repayment amount tomorrow via email. I have cancelled my debit card and instructed my bank to cancel the CPA on both. However I am terrified of the extortionate amount both of these lenders seem to add to loans if they default (reading other posts). I have learnt my lesson and just want to repay both but I expect these loans to escalate to huge amounts over time. Can anybody advise please on how to deal with these companies?? Thank you -

In short, I have been having very bad problems with my mental health and suicidal thoughts, my finances have spiralled out of control and I have been off of work ill. I contacted Minicredit asking for a repayment plan and they sent me nonsense about lots of fees and whatnot. I am not in the best of positions as my old wages were on there (£1300/mo instead of the now £850/mo). I took out the loan after already being signed off for work. I basically irresponsibly took out this loan because of a lack of judgement and I was already grasping at things. May I point out that upon taking this loan out I had full intention of paying back and that my sickness was prolonged longer than I expected. I have managed to work out repayment plans with all other creditors aside from Minicredit. They have asked me for bank statements and sicknotes which I have already sent them. It was due today, I basically would like to know how I can minimise the damage of this to my bank and get a secure repayment plan in which isn't going to require me to pay what I cannot afford.

In short, I have been having very bad problems with my mental health and suicidal thoughts, my finances have spiralled out of control and I have been off of work ill. I contacted Minicredit asking for a repayment plan and they sent me nonsense about lots of fees and whatnot. I am not in the best of positions as my old wages were on there (£1300/mo instead of the now £850/mo). I took out the loan after already being signed off for work. I basically irresponsibly took out this loan because of a lack of judgement and I was already grasping at things. May I point out that upon taking this loan out I had full intention of paying back and that my sickness was prolonged longer than I expected. I have managed to work out repayment plans with all other creditors aside from Minicredit. They have asked me for bank statements and sicknotes which I have already sent them. It was due today, I basically would like to know how I can minimise the damage of this to my bank and get a secure repayment plan in which isn't going to require me to pay what I cannot afford. -

Hi, Just noticed that Minicredit changed their terms and conditions and renamed the 19.50 GBP transmission fee now a drawdown fee. Makes me wonder why? So I thought it is time to reclaim this so I sent them this: "Dear Madam or Sir, I am writing in relation to loans associated to my account, for which I incurred transmission fees which I do not believe are fairly and reflecting the actual costs of fund transmissions. The loans were taken out from from 17 January 2012 to 06 July 2012 The reason I believe that these transmission fees (19.50 GBP for each transmission) are unfair and not reflecting the actual costs of fund transmissions is that these are very high and unclear. Unless you can provide proof that these transmission fees were reasonable and actually incurred, I will expect a full refund of these transmission fees (136.50 GBP), plus 8% interest on these up to 8 August 2013 (14.94 GBP), in total 151.44 GBP, plus daily interest of 8% after 8 August 2013. I look forward to your prompt response to this email. If I have not had a satisfactory response from you within eight weeks of this letter I will contact the Financial Ombudsman Service to formally investigate my complaint. Kind regards" Can't wait for their reply

Hi, Just noticed that Minicredit changed their terms and conditions and renamed the 19.50 GBP transmission fee now a drawdown fee. Makes me wonder why? So I thought it is time to reclaim this so I sent them this: "Dear Madam or Sir, I am writing in relation to loans associated to my account, for which I incurred transmission fees which I do not believe are fairly and reflecting the actual costs of fund transmissions. The loans were taken out from from 17 January 2012 to 06 July 2012 The reason I believe that these transmission fees (19.50 GBP for each transmission) are unfair and not reflecting the actual costs of fund transmissions is that these are very high and unclear. Unless you can provide proof that these transmission fees were reasonable and actually incurred, I will expect a full refund of these transmission fees (136.50 GBP), plus 8% interest on these up to 8 August 2013 (14.94 GBP), in total 151.44 GBP, plus daily interest of 8% after 8 August 2013. I look forward to your prompt response to this email. If I have not had a satisfactory response from you within eight weeks of this letter I will contact the Financial Ombudsman Service to formally investigate my complaint. Kind regards" Can't wait for their reply

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS