clairey

-

Posts

50 -

Joined

-

Last visited

-

I paid by debit card in both cases.

-

Hi all, I made a purchase of a dress in the sale from an online shop called Zalinah White. This is a link to the dress: Black and Cream Polka Dot Dress WIth Belt - Camilla ZALINAHWHITE.COM STYLE NOTES Step out in style with our stunning Black and Cream Polka Dot Pencil Midi Dress with V-Neck and Belt! Perfect for any occasion, this dress is now on sale for a limited time. Featuring a classic polka dot pattern in... I bought with confidence because, as you can see when you scroll down past the item description and size advice, it says in big letters 90 Days to return or exchange. Great. I bought it and it was too small. Because I liked the dress, I immediately re-ordered in a larger size and started a return. It then said I had to be "authorised". I waited two days before looking again and my order now has a 'not authorised' label for being a sales item. I realised that once I saw this, if you scroll past the 90 Days to Return picture, there's a small link for Return and Refund Policy. Click through that and read though to the 8th paragraph and there's the return restriction information on sales items. I don't feel it is reasonable at all to expect a consumer will scroll past the massive '90 Days to Return' section to the small links and click through and read 8 paragraphs to understand their policy on sales returns. They did not respond the email on this. Meanwhile, the second version of this dress I ordered arrives. It's exactly the same size as the first one. Neither dresses have size labelling on the dresses, nor do they have size labelling on the bags they were packed in. So now I have two of the same dress, both sales items. I email the company about the sizing issue on the second dress and reiterated my frustration about the website experience of the first. They are ignoring my emails. I would like to know what my rights are in this case. Neither dress is faulty per se, and I have no way to actually prove the second dress is the wrong size since there's nothing on the dress or packaging. Does anyone have any recommendations? Thanks, Claire

-

Universal Credit Application Help - Disregarded Property

clairey replied to clairey's topic in Benefits and HMRC

Thank you so much, this is what I was wondering about. That's very helpful. Thanks, Claire -

Universal Credit Application Help - Disregarded Property

clairey posted a topic in Benefits and HMRC

Hi everyone, I have a question about applying for Universal Credit. This is the first time I've ever applied for benefits and have a bit of an unusual living arrangement. I current rent the home I live in, but I also own a house (with equity) in my home town that my 71 year old mother lives in. She is over state pension credit age, which I've read in many places qualifies the property as "disregarded" or "ignored". I was just looking for some advice on the UC application form - there's nowhere that asks for details on this. You either state you have under or over £16k savings with no further questions. Do they get in touch to ask about this or do you not include it on the application because it's disregarded? I don't want to complete the application incorrectly, I know they're bogged down at the moment. Thanks in advance for any insights on the application process. Claire -

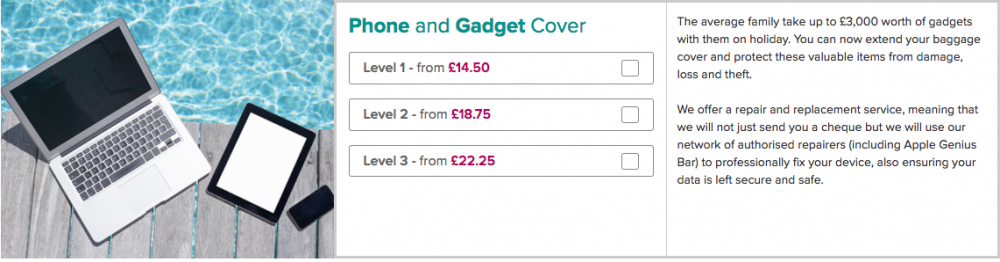

Hi there, Apologies if this is in the wrong section, but it seemed most appropriate. In October I went on holiday to India. Before I went I took out "gold" cover travel insurance with Cover For You. While I was on holiday my mobile phone was stolen from my bag. I reported it to the police, got a police report, immediately had it blocked by my phone company and did all the right things. However, on contacting the people administering the insurance, it turns out that mobile phones are not included in the insurance and that it is required to take out additional gadget insurance to cover phones. Now my phone was a brand new iPhone 7 that I'd had for 3 weeks. If it had been at all clear that it was excluded when buying my insurance, I would have taken the additional gadget insurance. But I remember going through the form application and when additional gadget insurance came up, it said this (I have recreated the insurance application and the screen is exactly as it was when I ordered): I remember thinking - I am not taking up to £3k, my baggage cover is up to £2k, so I don't need to "extend" it. And carried on. Maybe that was naive of me, maybe it was my fault for not examining it more closely, but the wording appears misleading to me. Then when I looked at the key facts, there is no information at all that gadgets are excluded from baggage allowance. In fact it states exclusion includes when: The loss, theft or damage to Valuables and electronic/other equipment occurs whilst not being carried in your hand luggage while You are travelling on Public transport or on an aircraft. This is in the personal baggage section. The reference to electronic equipment in that section again reinforced for me the idea that gadgets were covered up to the value of the personal baggage allowance. I would like to ask opinions on whether I have grounds for complaint here. I feel like I was mislead when buying the insurance and that it should be much much clearer that gadgets, including mobile phones, are excluded from personal baggage allowance and that it's essential to take out additional gadget insurance. Thanks in advance you your thoughts. [Just realised this should be in the insurance section - could an admin move it for me? Very sorry.)

-

No, not the Star Wars convention. This event hasn't happened yet. The T&Cs do not state anything about the event being subject to change in that way. Yes, there is a clause about guest cancellations and subject to work commitments, which is totally standard practice. Nothing about the event times/length/etc changing. Travel and accommodation was booked based on 4 days. Fine, the argument might be that they can fit everything into 3 days that was going to be on 4, but I don't see how that is possible. This event is always jam packed with wall to wall guests and events, every year. My question was whether it is reasonable for me to push for a refund. I'm not taking anyone to court over it. But I like to be polite when asking for a refund and make sure I'm being fair by knowing my rights and the organisers. Hence my question.

-

I'm not entirely sure this is the correct sub-forum so apologies if this needs to be moved. Quite a simple question, but one I couldn't find an answer for. I bought a ticket for a convention this month. When I purchased the ticket in November 2015 the dates of the event were Thursday - Sunday - 4 full days. The cost of tickets had increased by 43% over last year, but because they were advertising an additional 1.5 days for the event (last year it started at 1pm on Friday), this seemed a reasonable increase. SEVEN months after ticket purchase and just two months before the event, the organisers slashed the length of the event back to Friday - Sunday instead. They offered no refund and instead just gave everyone a free picture worth £5. I want to know if I'm within my rights for a refund on the ticket based on this change of T&Cs? I'm pretty angry that the cost is now so high for essentially the same event and feel I've been duped into accepting the hugely inflated cost for the event. But essentially I'd like to know if I am entitled to a refund based on the fact I won't be getting exactly what I was sold? Thanks, Claire

-

Hi, last year my neighbours constructed a monstrosity of a lean to down the side of their house with a centimetre between it and my house wall. At the time, my mother was in and spoke to them (she lives with me) and they assured her it was all fine and they'd checked permissions, etc. As we have a good relationship with them, we didn't see any reason to raise objections at that time. The lean to very narrowly (like I said, barely a centimetre) doesn't touch our property. However, if we wanted to get the wall repointed, there is zero access to it. Recently, the bad weather and excessive rain has caused significant damp down that side of the wall where we've never had it before. And when examining during a rain storm, the lean to is directing a flow of water towards that wall. I got a builder in to examine and he climbed over to have a look - his assessment was that the lean to was causing excessive water to hit that wall and cause the damp. Can you advise me of the best way to go about dealing with this? Having spoken to the neighbours, it's clear they are not interested in helping - they have just stood firm that they have a right to put it there and that's that. I called the council and they weren't very helpful, so I think the next port of call is my insurance company, but I would be interested if anyone has any knowledge of the legalities of lean tos and how the boundaries work. Thanks, Claire

-

Hi, I was wondering if anyone can help regarding whistleblowing and subsequent victimisation? I am asking on behalf of someone else. Due to the sensitive nature of the situation, I need to be a little vague, I apologise. The person complained at work about a situation that is definitely unethical and probably fraudulent. It involves vulnerable people and a high profile national organisation's name. The person was as a result bullied quite badly and the CEO made barely veiled threats about their job. About 2 weeks after the complaint, a whistleblowing policy retroactively appeared saying workers have a right to whistleblow and they support that, despite it not being the case when the person complained to management. The bullying involved being excluded from decisions/meetings relating to the persons job, being shouted at several times publically for no reasonable reason (causing the person to break down in tears) and various other nasty behaviours including being excluded from talking to anyone as the issue was being concealed and they specified that they were worried the person would talk about it. The person has now, 4-6 weeks on, been handed a reduced hours letter. This will put the person in a financial position of possibly having to reject the new hours, dismissal and possible claim. So to my question: does this sound like a constructive process to you? I feel the timing of the reduced hours is rather pointed given what has been happening recently and a desire to either force the person to resign or get a new contract in to dismiss (the person has been there 11-12 years.) And I am frustrated that this person is in tears daily about how they are being treated just for speaking out against an injustice. I am not even joking that if any of this was given to the media they would have a field day (even just the bullying, if we were to take out the other thing, would make an amazing headline given who they are and where they work). Is that too vague to even understand? I'm sorry, I guess just venting it all out helps. Thanks.

-

Hi all, I'm pretty sure that I don't have any rights in this situation, but I wanted to get your view. I rent a one bedroom flat and have been here over 4 years. I have an AST that we restarted for 12 months this February when the rent was increased. I discovered last week that my landlord has applied to redevelop the building - the planning permission was sought to basically demolish the building and rebuild brand new flats. Yesterday the public notice went up outside our building for local residents to send comments, etc. Obviously I object to this planning application as I will be evicted! There is no chance I will be able to have one of the redeveloped flats - this is in east London where we are going to go from a fairly run down set of flats on a low-ish rent, to a set of brand new premium flats that will cost a great deal more. Well, I'm sure that you've all seen the constant headlines about rents in London and redeveloped properties. My question is really about whether when granting planning permission if the council will take into account displacement of tenants? And whether we have a right to respond to the planning application as residents due to the inevitable resulting eviction? I just can't seem to find any info on this online. Basically, I don't want to lose my home or be evicted, but I realise there may be no choice in the matter. It's just so sad, the flat was in a horrible state when I moved in and I've done a lot to make it a real nice place. In fact, the LL just a month ago agreed for his handyman to come and put shelves up in the bedroom, so it feels like the worst timing. Thanks in advance for your advice. Claire

-

Their T&Cs generally don't relate to their behaviour at all. Nothing is stated about the cancellation of tickets on whim, banning people, etc, they just do that. (I looked when I had my order cancelled for sending a query.) Although they do have: Rogue Events reserves the right to refuse admission. We do not have to give evidence or a reason. You will be fully refunded for the price of your ticket within 30 days. Normal conventions will have a clause that say they will remove people that cause disturbance or refuse to comply with reasonable requests - that makes sense. But in this case, they'll just turn you away because they feel like it without any reason. An event is 3 days long, so an individual would incur significant costs for hotel, etc, if they did this. What bodies would be relevant to this kind of business? I've looked, but I can't find the appropriate place to complain. Thanks.

-

Hi there, This is a bit of an odd one, but it makes me so crazy and I don't see how it's legal for anyone to run a business like this. There is a successful convention company that organises several events a year. A typical convention will host up to 2000 people over the weekend spending a minimum of £110 each. On average, however, I'd say most people spend around £400 just on tickets and extras to the conventions. It's not cheap and people are parting with a lot of money, with some spending up to £2k on their attendance. (Again not including stuff like travel or accommodation.) This convention company is run by a one-man band and he has a serious reputation for banning people on a whim and making odd and sometimes confusing decisions based on nothing. I was banned once for saying something slightly negative about the convention online (and I have emails to prove the very lengthy time it took for me to be refunded after he banned me on a whim). Other people have the same story. recently a friend sent an email asking if her order had been processed, just to get an email saying that because she chased the order they were cancelling her order. (No joke.) Other issues are not confirming orders, not replying to queries, etc. on a more serious note, for many people that buy premium packages, when they add a last minute major guest, changing their policy to exclude those guests from the packages, or even changing it on the day, so people attend expecting they've bought one thing and arriving to be told they didn't. They don't take any form of payment other than bank transfer, not even paypal. I think everyone here knows why that would be. Clearly they're scared of chargeback. And rightly so judging by the number of complaints I've seen over the years. The reason that they are able to get away with this kind of service is that they are preying on vulnerable young fans who are desperate to meet American actors they would otherwise never get to meet and are willing to put up with almost anything to get that. Even though everyone knows that if you even look funny to this guy you could get banned. And there is an individual that also possibly has a disability discrimination case that they are investigating with a solicitor. My question is whether something like this (arbitrary bans, orders cancelled on a whim, bullying of individuals, etc) has any recourse (I can't imagine there's a legal one even if I'd like to think there was, but do we have anything like the Better Business Bureau in the States?) Be good to get people's thoughts. Thanks, Claire

-

I took out loans in 1998, 1999 & 2000 when I did my undergraduate degree. I have since been paying student loan repayments of various amounts over the years. Due to the fact that I took maximum loan amounts, I just continued paying without monitoring as I felt that this would take me a long time to pay off at the rate I was when I was first employed. (I think some of my early payments were as low as £15 p/m.) More recently I've been increasing in salary to the point of which I now pay about £200-300 p/m. So I started thinking about how long I might have left to pay this loan that takes a fair chunk every month, especially now that I'm taking out a mortgage and paying a pension and all the other deductibles of sensible adult life. When I started examining my past statements, I'm 99% convinced that a substantial number of my loan payments have not been passed onto SLC. So I am going back to 2001 when I graduated and got my first job to try and start gathering evidence of the loan payments I have made. This is a bit tricky as I don't have all my payslips from the early years and I moved around temping for a while. Nonetheless, I have a substantial amount of my old payslips and am building my info. What I'm wondering is whether anyone has any experience or stories of this happening, how easy it was to sort out and what the result was? I'd just like to know if this has happened to anyone else. Thanks, Claire

-

Hi, it's been a while, but I thought I'd update about the outcome of this. The adjudicator decided that myself and my flatmate WERE liable for some cost of this. They said that the delay in advising the LL of the mould may have caused the problem to get worse. They felt her claim was excessive and awarded her £300. They said it was unfair for her to claim the whole amount from me, and so this is split with my flatmate, so in total they awarded her £150 of my deposit. It's not too bad, but I'm still annoyed. Bear in mind I presented evidence of a precedent that the LL set for monitoring problems before reporting them. However, what seems to have been the key thing against me was that between the time we identified the problem and reporting to the LL, we had a separate conversation about something else with her. They felt we should have made her aware at that time. Hope that helps anyone having similar issues, or at least contributes to the knowledge base around this kind of thing. It's certainly made me more aware of things around the house now. Claire

-

Thanks, that's what I thought too. As you can probably see from my previous posts, there's very little 'evidence'. I believe her evidence consists of a few photos taken after I moved out, and a statement from her builder to explain the problems that occurred. She does have an insurance document that I believe she got done after I moved out that states that the property is in good decorative order and used this as an example of calling me a liar because I said that the bathroom had problems with the tiling before I moved in. This can not be used as evidence of the state of repair of the bathroom prior to the problem occurring, can it? In the whole property, the only room that was old, shabby and not updated was the bathroom - old wooden window frame in the shower, poor tiling, etc. I don't think an assessor would have said this was in good decorative order had that room been assessed then. But without any documentary photographs or a signed inventory, she can't prove either way regardless, can she? Thanks, Claire

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS