flooz

-

Posts

487 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by flooz

-

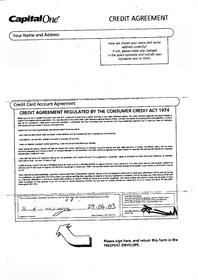

sorry, but I don't seem to be able to get it a 'sensible' size. Page 2 of letter. Accompanied with the letter and agreement is 5 pages of printed T&C's, which may or may not be the T&C's present at time of agreement. As they do not appear to form part of the actual agreement in their current form, but of course may have been in small print on the reverse of the agreement signed. Hope this is all of assistance.

-

and the letter that accompanied it, page 1

-

OK, I think I might have the hang of this now, so, this is page one of Cap One's response...

-

For some reason, I cannot get the images uploaded to photobucket,I'm trying hard to put them as attachments, but at the moment, failing miserably at that too

-

Thanks Usaname - I'm just trying to scan documents in and will post them tomorrow.

-

update: CapOne have today sent a signed credit agreement some 9 weeks after the initial SAR letter was sent; They'd initially tried to get away with providing a blank agreement, using the Section 3 (?) rule, which I followed up with a letter putting account into dispute. What's bothering me is why only now have they produced this? Is it relevant? Do I now just accept they have an enforceable agreement? Does the fact that the agreement was produced out of time have any bearing on the matter? Any further assistance is much appreciated.

-

OK. This was in the text of the letter I sent (advised on a previous thread in General Debt) As the time limit for providing the true copy has now expired, you are now in default of my request. Any account I hold with you is now in legal dispute. Whilst the account remains in dispute, you are not permitted to ask for any payment, nor am I obliged to offer any payment to you. Furthermore, whilst the dispute remains, you are not entitled to charge any interest on the account, nor make any further charges to the account. Additionally, you are not entitled to register any information on this account with any credit reference agency. So I take it, that's not right then.

-

Thanks for taking the time to respond usaname. Only thing that puzzles me then, is why in the 'account in dispute' letter does it suggest that they may not add interest and further charges? Or is there something else I don't understand?

-

-

Capital one couldn't produce a credit agreement, so sent 'scott's letter' (as advised http://www.consumeractiongroup.co.uk/forum/general-debt-issues/221505-new-rules-loans-credit.html#post2501581 here). Received telephone call from them requesting payment over telephone to bring account up to date, which we decline, and requested they correspondence with us by letter. Received today monthly statement which is now obviously incorporating late/non payment charges, as well as accruing interest. Is there any particular letter I should send? As the account is 'in dispute' aren't continuing charges supposed to be put on hold? Indeed, do I need to do anything? Or do i just let things take their course and wait for DCA letters to start arriving? Any assistance greatfully received. Many thanks.

-

quick question in order to help make a decision

flooz replied to flooz's topic in Business Bank accounts and charges

Thanks again Emandcole - you're a star. Now I'll just see if I can find a way round this maze and watch in the right area for template letters to appear ;-) -

quick question in order to help make a decision

flooz replied to flooz's topic in Business Bank accounts and charges

OK, Emandcole - i'm confused now. I've tried looking through the threads here to see any interpretation of yesterday's ruling, but haven't found anything (this site is just sooooo huge now). Any pointers as to what it means to us lemmings in the real world?? Or do we all have to be more patient?? -

quick question in order to help make a decision

flooz replied to flooz's topic in Business Bank accounts and charges

So I guess this means the banks are laughing all the way to the bank! (scuse my weird sense of humour). No point in claiming now then -

quick question in order to help make a decision

flooz replied to flooz's topic in Business Bank accounts and charges

Thanks Emandcole - I shall be scouring the news to see what happens. -

quick question in order to help make a decision

flooz replied to flooz's topic in Business Bank accounts and charges

Thanks again Emandcole, I see what you're saying now. I can't think of any charges we've sustained as a result of the bank's charges. Without doubt though, the bank charges we've been hit with of late, have undoubtedly 'pushed us over the edge' in relation to our insolvency. We thought banks were supposed to be helping and supporting small businesses through these tough times, we've found that's not the case. Oh well, back to the drawing board, lol. -

quick question in order to help make a decision

flooz replied to flooz's topic in Business Bank accounts and charges

Thanks for your response Emandcole. I think I heard something on the radio that the test case (appeal) is due this week, but I might be wrong there. Something I'm not quite sure of in your post; in the last paragraph, you mention "resultant costs you suffered as a direct result of the banks unlawful charging". Can you elaborate on that, as I'm not sure what you mean. I can't immediately think of any 'resultant costs', but I'm of the opinion that if the bank's hadn't kept charging us exhorbitant amounts, there's a chance we might not be in this position. Thank you for taking the time to answer me. -

They don't appear to; we've been informed that Mum will get the extra allowance WHEN someone moves in with her as a PERMANENT RESIDENT. The problem is, my family take turns to stay with her, as and when she needs. So there is no permanent residency of anyone in a caring role. And that is how the LA are currently viewing it.

-

Thank you, both of you. Interestingly enough, i'd done a claim for discretionary payments, and despite my showing a shortfall between income and what Mum reasonably spends on day to day living, they still send back the letter "no, we believe you've got enough money to live on". I've queried it, as I feel that they send this letter regardless of situations to try and put people off. If need be, I'll start quoting DDA etc at them as well as quoting the successful cases above. I can but hope.

-

thank you Soleman. I guess all cases differ slightly, but I think the case proves that any LA have a duty to consider extra room requirements (if necessary) of a disabled person, when it comes to calculating housing benefit (that's how I see it anyway). My mum receives HB in relation to a one bedroomed property, despite her renting a two bedroomed, due to her alzheimers she does need care, which I provide and stay with her when necessary. The LA keep quoting the Housing Regulations, stating that as a single person over 25, mum is only entitled to receive HB for a one bedroomed property. I'm trying to argue that point. It's not easy as our particular LA is very undisabled friendly. From what I've researched, the Housing Regulations are under attack from various organisations as they don't take into consideration requirements of disabled people, such as carers, unless any one carer makes it their permanent residence - which is rarely the case. I believe LA's may be forced to change their stance as a result of this.

-

thanks for that soleman - I can't get into the link, it appears to be members by subscription only. I just need the person vs person details, so I can quote it in a letter. Do you happen to know it?

-

anyone?

-

Just wondering if anyone knows. I found some information on a web site about a successful court action in the Birmingham Courts against the housing regulations and housing benefit. Essentially, it was that the housing regulations only allow for a one bedroomed property for a person over the age of 25, but it was proved to be against the DDA for some disabled persons, for example, someone who needs a full time carer, and therefore housing benefit should be awarded on the basis of a 2 bedroomed home being required. As I'm currently fighting my LA on behalf of my Mum, who has alzheimers, it would help me immensely to know what the case was, so I can quote. Does anyone know what that case was? Many thanks

-

So what are the consequences of not having a cancellation clause in the T&C's?

-

Natwest Loan and new default registered 7 years later...

flooz replied to flooz's topic in NatWest Bank

ah ha, I didn't know that. I could do with a few more 'gifts' lol. It's not a huge loan anyway, and I'm more than halfway through paying it. But at the moment, I need all the help I need. Thank you, you're a star. -

Natwest Loan and new default registered 7 years later...

flooz replied to flooz's topic in NatWest Bank

Thanks again, I can see you're on the ball today I guess I must put my 'good manners' aside, as I feel like I should respond, and just let it run it's course. I'm assuming that when I start getting DCA letters there are 'stock' letters to send, i.e. requesting they provide a credit agreement to prove their case, etc. One thing did come to mind, and it may be another bluff on their part, is if they can't provide a credit agreement from 3 years ago, would they be able to 'find' the statement that shows the transfer of funds into my current account? Would that hold up in Court? Unless, I'm one of those terribly unorganised persons that just never checks their bank account details

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS