Massamum

-

Posts

288 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by Massamum

-

-

-

-

-

fantastic, many thanks Vint.

-

OK, thanks very much for all your replies. Lilly, that was a very useful read, would it be possible to let me know the case law this comes from please?

No NOA from OC, only from Link (at post #15).

MBNA sold the debt on before the date of remedy in the default notice and the DN is also dodgy (post #11).

Thanks also AC, I requested a copy of the deed of assignment from Link ages ago but they are refusing point blank to let me have a copy.

I have this morning received a response from Link to my letter requesting all of the documents referred to the in CCA, they have responded by sending the same terms and conditions as MBNA sent (i.e. the latest ones). They seem incapable of understanding the simplest of requests

. What now???

. What now??? -

am bumping this. Have received more threats from Link, demanding I pay up.

-

Little bit more fun... Lloyds rejected my hardship claim on the overdraft that is made ONLY of various charges, despite the fact that we even cannot pay the mortgage (house almost on repossesion...)The worst thing that my OH's jobseeker allowance was paid into Lloyds acc. Jobcentre managed to mess things up and we haven't received any money for a quite a while and suddenly from nowhere some lousy £160 appeared in that cursed lloyds account despite the fact that we advised JC to pay everything to totally different acc. Guess what happened - I am paying fines with the money that should help me to survive...

Sorry... needed a shoulder to cry on

Preuss, so sorry to hear of your difficulties. I had a similar situation with my jobseekers allowance a while back. I wrote to DWP advising them of my new bank details but they went ahead and paid my benefits into Lloyds, Lloyds swallowed it up in charges and I had nothing to live on.

I wrote to the DWP and explained what had happened and especially that Lloyds was taking all my benefits in bank charges and pointing out that it was DWP's mistake as I'd already advised them to pay into different account and lo and behold a week or so later they re-issued me with the whole amount. Don't know if they managed to get it back off Lloyds or what happened but its definitely worth giving it a try. That is money you should be living off and god knows its little enough. Good luck.

-

good luck Sunshine, give em hell

-

hi Joemay, thanks for your message. Still unsure what to do about this. Can't work out if its best to ignore Link and MBNA or keep sending them letters reminding them of their obligations (which fall on deaf ears). Could anyone please advise on what my best course of action would be? Thank you.

-

hi Sunshine, sounds very similar to what happened to me. Interest rate hike, charging order etc and then informing me they were writing the debt off. Next thing I heard was from Link saying they'd bought the debt from MBNA. Don't want to worry you but perhaps its best to be prepared that they probably will sell the debt on.

-

fantastic on both counts. Will keep you posted of the reply I get. Thanks ever so much, most appreciated.

-

one other thing, there was a barcode at the top of each page which links the whole document together, I blanked it out as it would identify me. Does that make a difference to being within the four corners of the agreemnet?

-

cheers for that vjohn - out of curiosity, what response did you get to it? Did it get them off your back?

-

Hi Chris, what a nightmare for you. I don't know how to get them off your back permanently, I'm sure someone with more knowledge will come along soon to advise you. You have done all the right things so far, perhaps report them to the Information Commissioners Office for defaulting on the CCA request? It might be an idea to send Barclaycard a subject access request asking for copies of all statements as well.

-

Many thanks for that. Am in process of reporting them right now.

-

-

-

I have heard stories of criminal gangs from Eastern Europe hacking into lenders credit depts and deleting credit records/wiping credit peoples credit files clean, even wiping out large chunks of credit data, if true, no wonder the banks are in a mess! Guess it would only be true if you saw onerous files disappear from your credit files,mind you they might even wipe off good credit data and leave you with nothing at all on your credit file lol!

now that WOULD be worth paying for :grin:

-

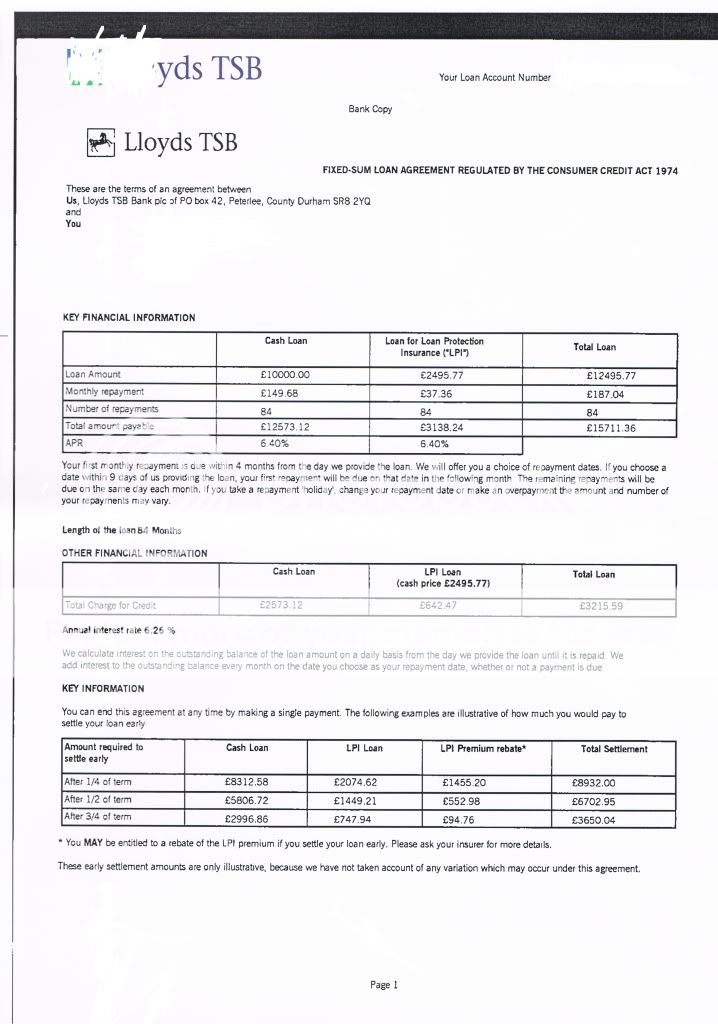

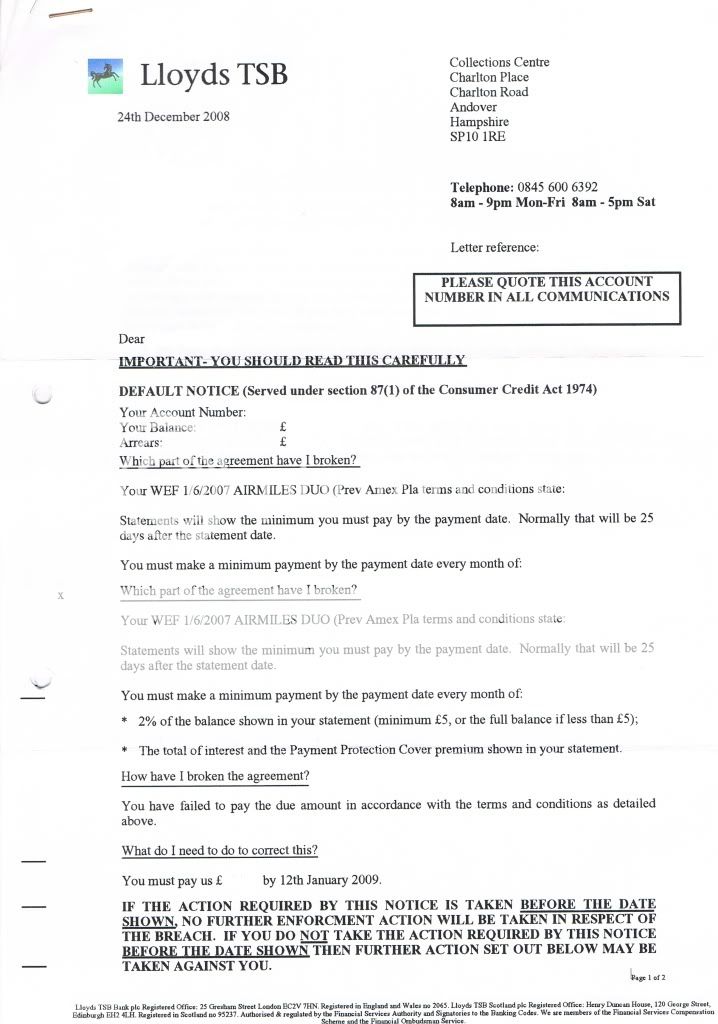

here is the default notice I received from Lloyds a few months back. It was sent on 24th Dec (merry xmas) but no idea when I received it as that was back in the days before CAG. With all the bank holidays I'm not sure they've allowed me enough time to rectify the breach anyway. Perhaps someone could have a look for me please? Thanks.

-

thanks BB, I'll do that too.

-

thanks very much for that Vint, letter is brill, will get that off asap. I received a default notice, will scan and post up as soon as I can.

-

also Lloyds have defaulted on their SAR which was sent to them early May - any advice please?

-

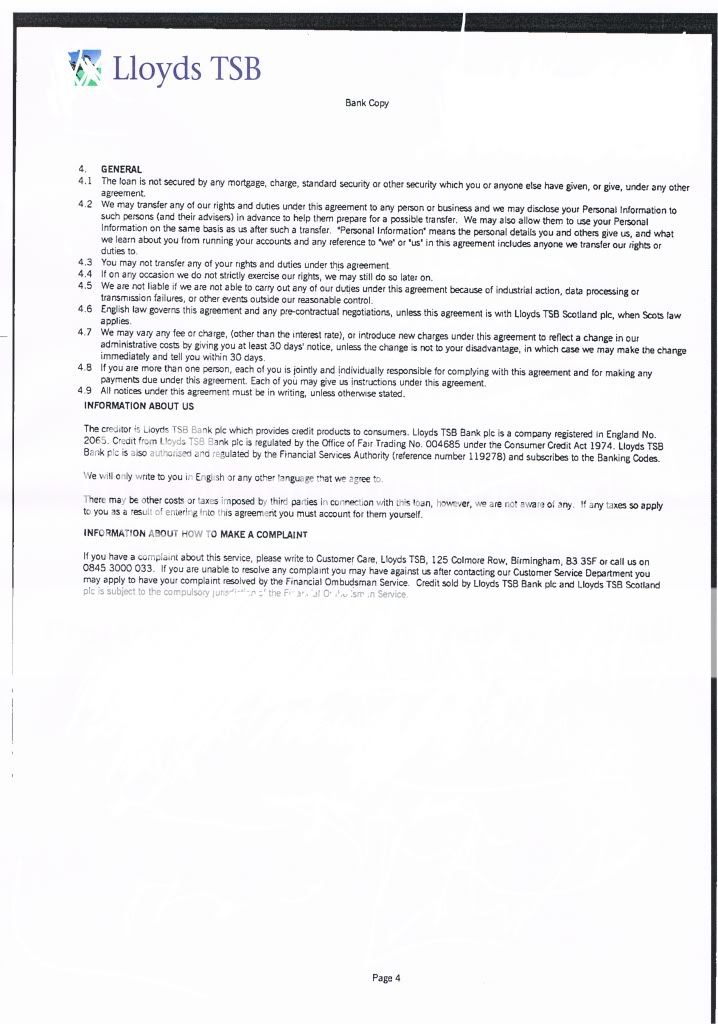

Have received a "final response" from Lloyds to my letter. They don't agree with my complaint. They say they have no obligation to supply me with the docs under s78 but because they are so wonderful they did so

. They also reckon because I've been using the account for a long time that it means I've acknowledged the debt. Oh yes, and they say the agreement contains all of the prescribed terms (even though I can't read any of it). Any ideas on what I should be doing now folks? Thanks in advance.

. They also reckon because I've been using the account for a long time that it means I've acknowledged the debt. Oh yes, and they say the agreement contains all of the prescribed terms (even though I can't read any of it). Any ideas on what I should be doing now folks? Thanks in advance. -

bump - still not sure what to do

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Enforcement Notice from Lloyds for Overdraft

in Lloyds Bank

Posted

ok, thanks for that. I've sent the SAR reminder off giving them seven days to respond.

Not sure what to do about sending the letter now, would it be best to send it off omitting the part about how much I'm reclaiming or should I wait til I get the statements back and fill out the full amount? If I wait, is there a holding letter I can send the solicitors to keep them off my back in the meantime (especially as the account isn't in dispute)?