Don Canard

-

Posts

19 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by Don Canard

-

I have just used my bank account debit card on that noddle site mentioned above and it worked. I found that I have a good credit rating, and as dx guessed there was no sign or mention of the money that First Credit were taking from me. I have indeed been diddled good style! I've been paying them back since 2004. Isn't telling outright lies to glean money from folk illegal? First Credit have taken a good couple of thousand pounds off me relating to that, and the cheeky b****rds wanted me to pay more before I went and died on them! Good god what type of world has this become.

-

I'll try to get one by post then. Excuse me for being a bit thick regarding this but what exactly would have happened had I done it six weeks ago? How would I have benefit from that I mean? I know I've a lot to come to learn regarding these financial goings on so I'm still unclear as to how it benefits me to have the report. What am I looking for and how would having the info earlier have helped? I suppose that's what I'm driving at. I need to know this stuff so that I can tell others without telling them wrong you see.

-

i can't get one i don't have a credit card. I'll try and persuade my wife to give her details for one but she isn't keen on using cards over the internet.

-

That's a shame what just happened there, I thought we all shared a common bond? Anyway, update. I received a letter from the DCA which informs me that they are unable to provide the paperwork I requested as the original creditor have failed to supply it. Therefore they say they are are 'closing their file'. having said that they then go on to say that I still owe them the (disputed amount) of money, and at any future time should they come into possession of the CCA I requested they will reopen the case. My thoughts on this are twofold. Firstly relief of course, as other forum members suspected I now feel they were simply leaching me of cash. My second concern is the mention of re-opening the file at some future date. Even if this can't or never will happen I don't feel it is right to allow them to hold onto it. The figure they originally purchased as 'debt' owed by me is incorrect, so no matter if they did reopen the file the figure would remain incorrect and in dispute. Is there any official way I can make this clear? I simply want to make sure that whatever unsatisfied debt they consider they own is not the incorrect figure that they are bandying around. I don't want to be held accountable for a sum I don't owe either now or at any future date.

-

Hey folks, can I remind you that I'm entrusting my next moves to your advice. There is always a different point of views wherever you might find yourself, but let's not fall out over them please. I'm not worried about debt avoidance, I've been paying these people for the last seven years or more, but I don't agree with the amount they claim (they bought?) is correct. Over the years I must have paid them far more than they purchased the debt for, so I think it's time to call it quits by whatever means. Please remember that these were the folks that were pushing me to pay more - only because they were afraid that I might die before I paid them! If you need to get angry, get angry at them - not each other. Thanks, Don.

-

I can't get a credit report if I wanted one. All these 'totally free' sites still want credit card details before they will continue with the report so that's where I'm stumped. I now aim to do nothing as priorityone says, but what are they cooking up in the meantime? It appears to me that they have just given themselves eight weeks in which to answer my complaint, with no mention of the CCA request at all. A lot can be fiddled in that time, if they were using me as a cash cow then maybe they now have time to cover that up? Anyway, I'll sit tight for now until I hear from them.

-

I tried to get a CRA report online but was asked for a credit card so I wasn't able to do it. If the alleged debt didn't show on a CRA what does that mean? Am I now free of it or have the DCA done something underhand or possibly illegal? And what do you think they will be thinking of doing about it?

-

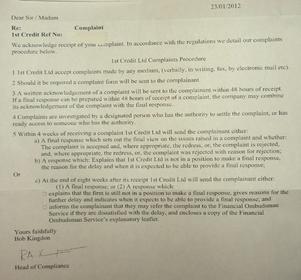

The bit about the complaint was already written into the letter in the library so I left it in, but I'm more interested as to their reaction to the main contents of the letter. Where's my CCA for example or how do they propose to move forward? This complaints procedure letter just seems to be buying them more time that anything else.

-

Hi folks, Well on the 18th of January I sent the account in dispute letter from the library as advised, and today I received my reply. Basically there is no mention whatsoever of the content of the letter regarding failing to supply a CCA, or what they intend to do about it. They only address the line at the very bottom of the account in dispute letter where it says; "You have 21 days from receiving this letter to contact me with your intentions to resolve this matter which is now a formal complaint". To this they have written back to say my complaint has been logged and will be looked into. I have posted the letter below. So what does that mean? What I wanted to know was what was their response to my disputing the debt, but they appear to have ignored that altogether.

-

Ok thanks. I saw an example 'account in dispute' letter in another thread on here somewhere I'll try and find it.

-

Hi all, just an update on how things were going regarding First Credit and the CCA request I sent them. Well first of all I used the request template from this site, sent the one pound fee as a postal order made out as advised above, and then I waited. I posted the letter to them (1st class recorded) on the 27th December, which means the 12 days plus two have now elapsed but I've had no reply. What is my position now? Do I wait a little longer for their reply or is there perhaps a follow up letter that I should hit them with? I have already cancelled the Direct debit payment as it was due to go out on the 21st, I thought they might have answered me before now.

-

Thank you. I'm learning. I have just changed my telephone number so there should be no more harassment calls from them, it's all going to be done in writing/registered post from this point on. As I see it the first major obstacle is to check whether or not First Credit have legitimacy in collecting this debt, regardless of who they have reported it to. For me that simplifies matters. They have either to prove their entitlement to continue to fleece me, or I stop paying and have no need to concern myself further with their threats. I'm not trying to reclaim any money from them, I simply don't want to pay any more to them unless it is proved to be lawful. As the figure given/sold over to them by the bank is now in dispute I just wondered where that puts them regarding their ability to proceed? Furthermore, who do I take up the disputed figures with? If the bank has sold the debt, it has sold a debt that is over and above that which it should have been, and therefore (to my way of thinking) can't be collected. Also if the bank did sell the debt several years ago, would there be any point in speaking to the bank other than to request statements to varify the error?

-

Yes I take both points, thank you. Being new at this I will do it step by step, so the CCA request will go in first (today if possible) and let's hear what they have to say. I'll then do a CRA check once I've had their reply in order to varify their actions. They have always sent me annual statements showing the amounts I have paid and indicating the amount still left to pay, so it would be very interesting to find that they had omitted to inform the CRA about this. Anyway, like I say I'll go one step at a time as it's all still a learning experience for me.

-

Exactly. My understanding is that it's not statute barred because I have been paying it off in good faith all these years, thus keeping the debt 'alive'. What a fool they have taken me for! I've read so much about people trying to use loopholes to avoid paying their debts, but that isn't what I wanted to do. I did actually owe some of the money on the card but not all of it. Out of a sense of duty, and thinking that I was doing the right thing, I have attempted to repay what I believe I owed - only to become sucked into paying an amount I didn't owe and which will take the rest of my life to pay. If as seems likely, First Credit did buy my debt, then the repayments I have made to them over the past seven years or so have more than covered their outlay by a factor of two or three. I am slowly going from incredulity to anger over this. To think that those people are living off vulnerable individuals like myself, and abusing the tendency that is in us that makes us wish to honour our debts. I don't want to break the law of course, but I'll be damned if they get another penny from me without a fight. I have got the template from this site (many thanks to whoever provided it) and it will be posted just as soon as the post office returns to work. I will keep you all informed of what happens next. Do you know I'm going to go and sit down and have a drink of something quite strong now. I find it difficult to believe such parasites exist on the back of other peoples misery. Quite unbelievable, and a very sad indictment of our society. Thank you all for your contributions and advice.

-

Thank you for those replies priorityOne. I will send a CCA request to them asap. Is there a form for CCA's on this site, or perhaps an example of what I should write? So if I'm clear on this, I now send a CCA by registered mail. I wait thirty? or so days, and if they have not complied I can then stop the direct debit and write to inform them that the account is in dispute. If they do comply and send me some sort of credit agreement within the required time limit how will I know if it is enforceable or not? As you can see I have a lot to learn, but I'm really struggling to make ends meet now, and I'm embarrassed to say that I even thought of suicide the other day. But I refuse to be pushed into an early grave by people like this, to realise they have been proffiting from my misery is awful. The man on the phone seemed angry that I would be 82 before I had paid up, he didn't appear at all concerned at all that they would be leaching from me until I am 82 though. What bastards! (sorry).

-

Yes the fees will be over six years old as this debt relates to around 2003, and I have been paying it back to First Credit every month since 2004. So I need to check my credit history? Then do I still need to get those bank statements if no debt shows, or only if one does? Does this mean I can stop the direct debit immediately? And if so what reason can I give First Credit for doing so? As I know nothing of the law I'm unsure how to reply to their legal threats and intimidating letters, which is how I ended up snared like this in the first place. Why do they refer to TSB as their 'clients' I wonder? Sorry to ask so many questions but I didn't think such things were allowed in this day and age. What you describe is akin to Piracy. Over the past few years they have taken several hundreds of pounds off me in 'repayments'. Would First Credit have simply kept that money? I thought I was paying it back to TSB via them?

-

Also I forgot to mention. First Credit regularly send me 'offers' where I can pay back half, less than half, or sometimes two thirds of the debt, and 'they will pay' the rest. I know that there is no rest to pay of course, it's just an early settlement offer. I have never been able to take them up on it as I haven't got the money, but I wondered how they can accept half the alleged debt as full settlement one day, then require all the lot on another day? Finally, on the bottom of their letter it says PAY NOW online by debit or credit card. I might be thick, but surely an invitation to pay off a credit card debt by credit card is a highly dubious suggestion to put on the bottom of their letters?

-

Thank you for the welcome those replies. Merry Christmas to you too. When I asked First Credit for a copy of the original agreement which authorises them to take this money from me they just quoted some law at me that says I couldn't have one. Then I asked for a copy of the original CCA and they say that they have contacted their client and are awaiting their response. They then went on to say; "On receipt of the copy agreement we would expect you to contact this office immediately to arrange settlement of the debt." I explained that I am in failing health, having had one kidney removed I now find the remaining one is failing. Due to the increasing cost of utility bills etc I am unable to pay them in full. I have to struggle to pay them their regular monthly payment which is only low to begin with. Am I to understand then that even though those statements are from 2002-04 I can still ask for copies by sending TSB ten pounds? Also what is reclaim? How does that work? I'm sorry to sound so unwise but I have never had to deal with people like this before. The point I wanted to make to First Credit is that if the sum claimed is incorrect then I shouldn't be paying it back until the correct sum is established, but the day after I sent the email to them they took another payment by direct debit as usual.

-

Hello all. I'd really appreciate some help in dealing with a DCA First Credit. The debt relates to a TSB credit card that I held back in 2004. I made a late payment and incurred a late payment fee which pushed me over my limit. So not only did I get a late payment fee, I got an over limit fee on top of that. I rang TSB card people to protest that this was unfair. My son had just been killed, and as a result our world was upside down, consequently I paid late and got hit for two fee's. I had paid, but under the circumstances it was just a bit later than was usual. The individual that answered my phone call told me that "The fees were my punishment (his words) for paying late." Given that I knew nothing about how these things work, naively I insisted I would withold the monthly card payment until someone dealt fairly with me. Big mistake! TSB simply added £50 a month onto to my card. £25 late payment, and a further £25 over limit, each and every month for several month. In the meantime my marriage failed and I moved into a flat. When I contacted the TSB to sort this mess out they told me that it was now in the hands of the DCA First Credit, and so I made arrangements to pay them back monthly. I have been paying monthly for seven years now, and recently received a call from someone at first credit asking me to pay more each month as they have calculated that otherwise I will be 82 years of age before the debt is repaid. What I would like to ask is this. Given that the original sum owed comprised several hundred pounds, (possibly over a thousand) of unfair charges, and I believe that such charges have since been considered excessive, is there any way I can have them removed from the debt? I have asked first credit for the actual accounting of the alleged debt so that I can see just what it is I'm being asked to repay, but all I received was a short letter telling me that they refer me to section 136 of the law of property. Can anyone tell me please what it is I should do? I have been trying to educate myself by reading some of the threads on here, such as fighting back with CPUTR etc, but it appears that a certain level of knowledge is required even to understand the posts! I'm getting really depressed about this, all I wanted was fair play, but instead I appear to have been ensnared into spending the rest of my life paying for their wages.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS