Still_surviving

-

Posts

332 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by Still_surviving

-

-

No - it was in 2002

Ive just been reading the T&Cs from the reconstituted original agreement, and it says under the section for PPI :

"If you want to have payment protection insurance you must confirm that you have read the details we have sent you, and you understand the main benefits and exclusions of the insurance cover"

Well this is just a load of baloney. My wife filled out the form and they sent back a countersigned copy shortly followed by the card. At no stage did they ever ask any questions about the PPI.

It is noticeable that in the current T&Cs this particular sentence has been removed.

Im certainly leaning toward fighting this one out with Cap One.

-

I was waiting until I received a final response from BC, which duly arrived today (despite the date on their letter!)

I enclose a scan of this, and have underlined a somewhat interesting sentence....no reference to 'goodwill gestures' here

http://i816.photobucket.com/albums/zz90/Still_surviving/Barclaycard/BCardLetter200910.jpg

I will now be filing at court, which I am okay with.

-

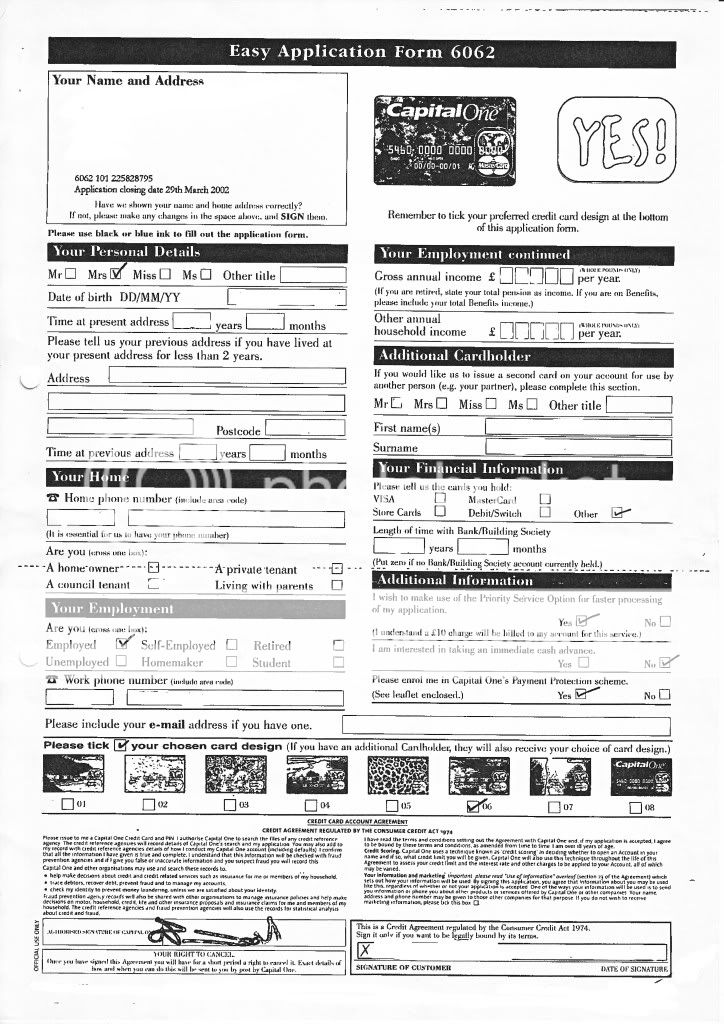

My wife recently CCAd, then subsequently SARd Cap One with a view to pursuing charges and PPI reclaims.

Responding to the CCA they sent this document as the 'signature page of her original agreement' plus 6 pages of laser printed T&Cs as her 'reconstituted original agreement'

http://i816.photobucket.com/albums/zz90/Still_surviving/Cap%20One/AppForm.jpg

This was also the only document that looked remotely like a CCA in the bundle of papers we received today for the SAR

I enclose a copy of the (somewhat stroppy) letter that they sent in response to the CCA request and could i ask the following?

(a) Is this enforceable document? I am not clued up on what they mean by 'reconstituted agreement'

(b) If it isnt, would that negate the fact she ticked the 'require PPI' box? Nothing further relating to PPI was ever sent to her...they just started taking the monthly premiums.

http://i816.photobucket.com/albums/zz90/Still_surviving/Cap%20One/Letter1a.jpg

http://i816.photobucket.com/albums/zz90/Still_surviving/Cap%20One/Letter1b.jpg

Any help would be most gratefully received

-

My girlfriend recently SARd Cap One as a start of a charges reclaim...

The only 'agreement' in those papers was actually the application form she originally completed and sent in by post, on which she had ticked the 'require payment protection insurance' box.

She never got to speak to anyone about the PPI and they never sent her any terms about it. They just sent her a card, initially with a low limit, and started taking the PPI premiums from day one.

Is she stuffed because she ticked the box? Or should they have gone through more procedures at the time?

Thanks for any help you can give

-

I wonder if anyone would be kind enough to help.....

Ive had several loans with M&S and always believed that I had never taken PPI, as I was self-employed, had told them so, and would not be covered anyway.

I was somewhat surprised therefore when I found the following CCA in my old papers

http://i816.photobucket.com/albums/zz90/Still_surviving/Marks/PPI%20Claim/MarksLoanAgreement.jpg

It clearly states on the form that I am self-employed, so am I right in saying they cannot wriggle out of it?

I eventually paid 18 installments of the 24, and a further £1515.80 which was settled from the monies of a new loan taken from them. (definitely no PPI on that one). The settlement letter I received stated that only £66.46 was rebated for early closure.

Can I politely ask how I calculate the interest part of my claim? Is it one premium taken from the start or end of the loan, or does each installment have to be done separately. Is it correct that I compound the interest using the 14.2% they charged up to the current day?

Sorry for the ramble...any help/opinion gratefully received.

-

I have a credit charges reclaim ongoing with Natwest Mastercard - we have been haggling for a while now over restitutionary interest, but we are nearly at a stage where I am minded to accept their offer.

However - we have one major stumbling block. They say any rebate will be applied to the outstanding balance of the account, I say they must send it to me, less the arrears stated on the default notice they issued.

My grounds for this are :

1. I originally applied for my CCA in October 2009. They swiftly responded, saying in essence that 'we can find no paperwork for you, however we expect you to carry on paying'. I formally placed the account in dispute upon receipt of their letter.

2. I wrote to them three times requesting a refund of unlawful charges/interest (by recorded delivery) and they completely ignored me, save to issue a default notice, followed by a termination notice.

3. I sent a 14 day LBA and it was only at this point that they acknowedged me. Since then we have exchanged letters and arrived at a stage where Im minded to accept the amount of their offer, but cannot accept their method.

I realise I may be letting my anger at being ignored for 9 months cloud my judgement, but in my eyes they repudiated the agreement (which they cannot produce) by terminating it when it was in clear written dispute. They now want to tell me how they are going to settle. In my opinion they should refund me the £1700 less £190 arrears on their DN. I would add that those 'arrears' only arose after i placed the account into dispute.

Would I be wasting my time by taking this to court if they do not back down?

Any opinion (for or against) would be welcome.

-

Yes Ive claimed compound interest in restitution, and set it all out in very neat schedules at the end of July and August showing updated interest figures.

The balance when they terminated it was just shy of £3000, the claim as last submitted was £1350, if it gets filed at court another £350 goes on for the statutory 8%

The reason Im so miffed and want the charges paid back to me and not credited to this account, is that they ignored 3 registered letters and terminated the account whilst it was in clear dispute. They cant argue it wasnt in dispute as I have their letter stating they have no CCA from before i even filed my first request for charges to be repaid.

-

Oh well....progress of sorts.

They have now responded by offering all the charges plus 8% - still not acceptable. If i give them another 14 day LBA am i being too accomodating, given that it will be the 3rd after them having ignored me for best part of 8 months.?

I am also stating that I will not accept this refund being credited to my account. Given that they terminated my account whilst ignoring my charges claim, and given that they openly stated they cannot find any CCA for me, surely I am within my rights to demand repayment to me by cheque?

I am happy to press on to court stage, I just dont want judge to think i am making unreasonable demands.

-

Sure

Unlike the other 4 credit card companies who I approached, Aqua will not budge on their claim that the £12 charges they have debited me with are unlawful.

So - as I have done with the others, I wish to issue papers against them for the fees plus compound interest in restitution at the rate they have charged me (between 29.9 and 39.9%)

I would be interested to know why you had such problems - Barclaycard (2 cards) have recently caved in and we are just now haggling over the interest rate to use in calculations.

-

I am currently locking horns with Aqua over a default charges / contractual interest claim and it appears I will have to serve papers on them.

The thing is - i know Bank of Scotland supposedly issues the card, but it says in the small print that the card is underwritten and managed by SAV Credit Ltd, and its their details who appear on the 'About Us' section of the Aqua website.

Who ultimately should i address my court claim to? I dont want to give anyone room to throw out my claim once its started.

many thanks

-

zsazsa

Any news on what happened - your court date was 3/9 wasnt it?

Just got back from hols with the other half and wondered if id find some happy smiley posts here lol

-

Ive linked below a revised claim spreadsheet Ive just prepared which differs from my original one in that it applies the cash apr% to each charge using the rate in force at the date of the charge. I realise that I am probably being overly fair to Barclaycard in that for instance the early charges are compounded entirely at 21.4% whereas the actual rate rose up to 27.9% by mid 2007.

http://i816.photobucket.com/albums/zz90/Still_surviving/Mastercard/RevisedClaim310810_0001.jpg

This has the effect of reducing my claim from £2150 to £1715, but I feel that if this goes as far as issuing proceedings, I will be seen to have acted reasonably. Besides which, if Barclays allow this to happen, the 8% statutory interest will more than offset this.

The only other thing Im considering, is whether to apply for statutory interest at the contractual rate, rather than the flat 8% if things get that far. The difference would be £420 but im wondering if that would push the judge toward believing im acting out of greed?

-

Finally! a response.....

In response to my LBA, Ive received a detailed response from BCard which included a schedule detailing how they have calculated their offer to me. This I have scanned and attached below:

http://i816.photobucket.com/albums/zz90/Still_surviving/Mastercard/MCardChargesOffer1.jpg

You will see they have offered the sum of £1036.04 against my claim of £2150 odd

Initially I was quite encouraged at the attitude they had taken, but once I scatched the surface, I realised it threw up a couple of important points for all of us claiming charges and contractual interest. Im not sure if CAGgers such as Noomill060 still read these forums, but I would welcome any input on the points made below:

1. They have removed my initial three items as being over six years old - well funnily enough, if they had responded when I first wrote in Nov.2009, they wouldnt have been out of date. I think I can deal with this point.

2. As discussed on the forums, I used the current cash advance rate when calculating my claim - 27.9%. In the back of my mind I realised that I might well have to negotiate on this, as this had fluctuated over the period of the claim, from 17.9% to 27.9%. However, it appears that while their schedule takes account of these variations, it uses the purchases rate, not the cash advance rate, and there is a consistent 3% difference on this. Am I definitely right to insist on the higher figure even allowing for variations?

3. Most interestingly (and perhaps for those with a maths head only) I cannot see that the interest they are offering is compounded, rather a flat calculation based on a monthly rate. For instance, looking at the first charge on the list of £20 from 08.07.04, they state this as being 2241 days on a purchase % of 17.9% or 1.385% per month.

Using the CI calculator suggested on this site, it throws up £40.45 in interest whereas they offer £20.41.

If we take a 30 day month, their 2241 days becomes 74.7 months. A flat rate calculation therefore becomes (£20 x 0.01385 x 74.7) = £20.69 or very close to the £20.41 they have offered. The same method seems to hold up for any of the charges taken at random off the list.

Is this just a question of them knocking up a quick excel sheet and getting the underlying principle of interest calculation wrong? Or can they come back to me and argue that this is genuinely the way that they have calculated the interest over the years?

Sorry for the long post, but I genuinely felt this would throw up some important issues for those of us claiming from Barclaycard and their spin offs.

All the best

-

LOL!

Finally, after ignoring me for nine months, they have responded and offered the princely sum of.....£51

This is the difference between the default sums charged and £12, plus 8% interest.

Oh well...at least I have an account managers name now - time for yet another letter

-

Im no expert on these matters, but I dont think a judge would object to you doing anything that results in a more accurate/fair claim.

You might also like to convey the amended schedule to crapone, but make it clear that this is your final change, and if they dont budge, you may seek statutory interest at the contractual rate.

Dont lose sight of the fact that you are looking if possible to get crapone to cave in before the court date - saves everyones time and effort.

-

LOL if you think you are thick, read my thread to see just how much of a tizz i got into trying to understand all the concepts.

-

Dont get me wrong - im not advocating you claiming the statutory interest at 25.39% - but it is something you could threaten crapone with if they dont play ball with the rest of your claim. You need to weigh up in your mind whether you think the judge might think you are overstepping the mark by doing so.

The main thing is to get crapone to realise that you are seeking restitutionary interest and that is why their defence is flawed.

-

Not sure which interest calculator you used - i used the one below, with it set to 12 compounded payments, based on a 360 day year

http://www.egalegal.com/compoundWindow.html

I think its important that you understand that you are claiming Interest in Restitution, rather than the compensatory interest they are offering.

-

Ive just read the defence documents - didnt realise they had already caved in on the default sums plus some of the CI

There is a poster called noomill060 (think thats right) who became an expert on fighting the cc companies on matters of contractual interest. In fact he would argue that the 8% statutory interest only applies where there is no stated contractual rate. In cases where there is - the 8% could / should be requested at the contractual rate. That ones a bit out of my league though.

Have you read up on the concept of 'Interest in Restitution'? It basically means crapone have taken your money (ie the default sums) and used it to earn interest at the contractual rate - be it on your card, or in lending to others. You basically want the profits they have made back. In their defence they are saying they have already compensated you for the contractual interest they have charged you....however compensatory interest is not the same as restitutionary interest. Do some googling

In essence where you have paid and cleared the charge from the account, the money was then free for them to re-lend to others at the contractual rate... get it? (took me a while)

Have a read of the early part of my thread (rest is about CCAs and such like)...the concept is discussed by people who have won cases.

http://www.consumeractiongroup.co.uk/forum/showthread.php?223521-HSM-v-Bcard-Mastercard

I will have a further read of the defence docs when im back from work.

-

Thanks - i will be interested to read how they intend to defend this. Have they made any offer to settle that includes Contractual Interest albeit at a different amount?

Happy to offer my opinion if asked...but please remember im no expert - just a soul who is going down the same path as you

-

Heya

Im in the middle of 3 claims against CC companies and Im claiming in exactly the same manner you are - ie charges + contractual interest + stat interest (once i had to issue papers)

You sound fortunate to have landed a judge who isnt in bed with the banks

Very surprised that Crapone are taking this to court, though I wouldnt be at all surprised to see them settle on the steps - after all its a very dangerous precedent to set if the judge rules in your favour formally.

They will undoubtedly tell you your contractual interest calculations are wrong, because the interest rate varied, or they didnt charge on certain sums once you had made payments. However, its very strongly my view that they need to disprove your calculations and make a sensible compromise offer based on the data they have. After all, only they have access to the calculation methods - you cannot be expected to get it spot on....you just know that an injustice has been perpetrated.

Hope this helps - will follow your thread with interest. Whens the court date?

Edit - whats the gist of the crapone defence?

-

Slick

Thank you - have found the template and will work on it today.

Having read a 100 page plus thread over the weekend on defective DNs and UR, I was surprised to see your comment, that it doesnt seem to be a major factor. I thought the whole idea of having a DN balance owing that included a lot of penalty charges included, was that it rendered the DN invalid, and meant that at best, they could only claim the arrears stated at the time.

Confused

-

Update time

No further letters from any of Barclays in house rotweillers, but I did give them one further opportunity to respond to my claim for charges & interest. Didnt even get the courtesy of reply.

Am going to file proceedings on monday morning, but seem to remember people saying MCOL wasnt the best method to use in such cases. Does anyone have a link to a good template for setting out a POC, either via MCOL or other methods?

Also - I need to get this concept of Unlawful Rescission clear in my head lol...I have previously written to BC accepting their unlawful rescission of contract, due to the DN being defective as the balance claimed contained a high level of unlawful charges and associated interest (£2300 out of £8000 total).

Am i right then in thinking that they can only claim the arrears stated on the defective DN. and also, if that is the case, what happens to the rebate of charges and interest, should i be successful? The arrears were only about £475. Are they within their rights to apply the whole rebate to the card, or do I have a claim for the rebate to be sent to me, net of the arrears? Sounds kinda unlikely lol.

-

I took my eye off the ball for a little while here, whilst trying to sort out other parts of my financial situation. I realised that I had not followed up my LBA, but I figured that as over three months had elapsed, I should give them one further opportunity to respond. Yet again they have completely ignored me - not even a 'go away your claim is wrong' type letter.

I am now going to issue proceedings, but would welcome clarification on one matter:

As they have terminated my account when over 40% of the balance shown on the DN was unlawful charges/interest, I take it I was correct to accept their Unlawful Rescission of Contract? If so, are they still within their rights to apply any refund of charges/interest directly back to the account?

Opinions would be welcomed - thank you

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

HSM v M&S Credit Card

in M&S Cards

Posted

Ive recently discovered that an old personal M&S loan of mine had PPI on it (I must have been asleep)

Seeing as ive been self-employed for 20 years (and the CCA shows me self employed) I think I have a pretty solid case for mis-selling.

Did the math last night and it appears the claim will end up around £1900 plus £1100 statutory interest if we go that far. My question is, will

M&S have to repay that to me, or will they try and lay claim to it against this imho totally unenforceable cc debt??

With Thanks