mevsthem

-

Posts

186 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by mevsthem

-

-

Hi, Quick question regarding my statements. I cancelled direct debit last september and have not paid a penny since. Changed bank accounts and have letter saying d.d been cancelled. Just looking at 2 statements for Dec, Jan after termination notice and there is a payment received of £24 on each. I have not paid a penny since Sept, are they trying something underhand ? Can I find out where n how these payments have been made. I know for a fact its not from me

Thanks

-

Ok, thanks, my only concern is that they have given me 8 weeks to reply or they will consider my dispute closed.

-

Hi, In 2 minds whether to send this letter or not, think I should reply to halifax but do I let them know what evidence I have so they can be better prepared to build a case ?

-

Hi,

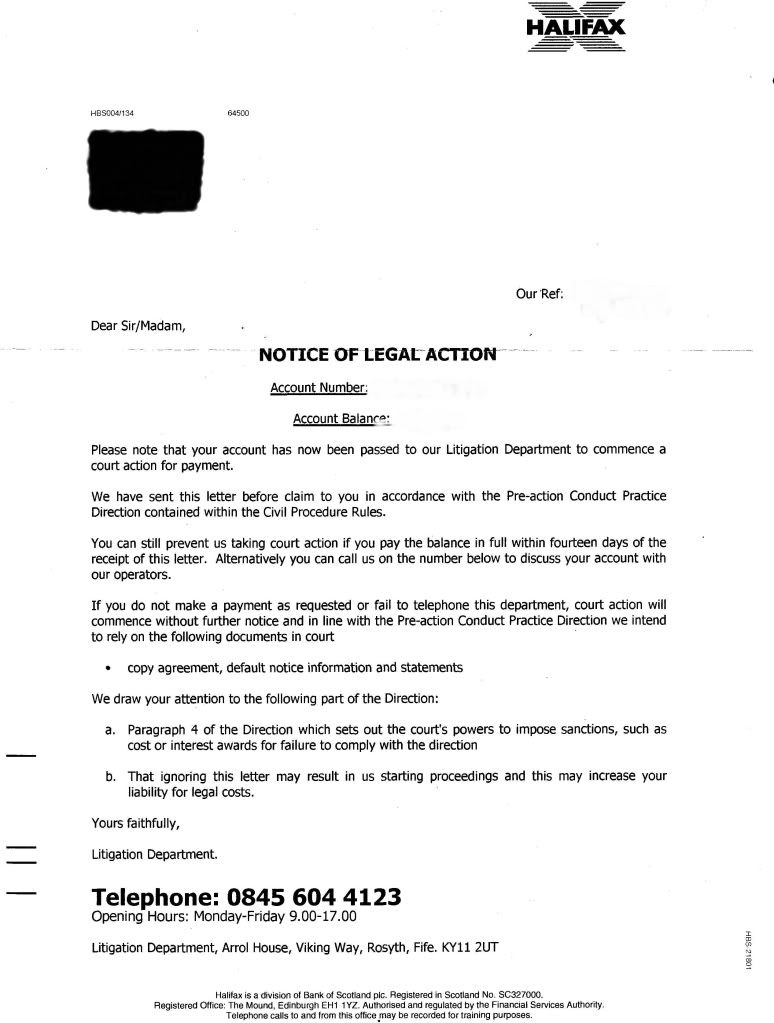

Received another Notice of Legal action, letter before claim yesterday same one as before, even though the customer relations dept have given me 8 weeks to respond to their last letter. I have written the letter below and wondered if someone would take a look and advise if it looks ok. Not very good with letters and I dont want to drop myself in it.

Dear Sir/Madam

Thank you for your correspondence dated 23/07/2010. I fail to agree that the true copy of the credit agreement you have sent me is indeed enforceable. Also there are issues regarding the default notice and termination notice you have sent to me.

Here are a few points I would like to bring to your attention.

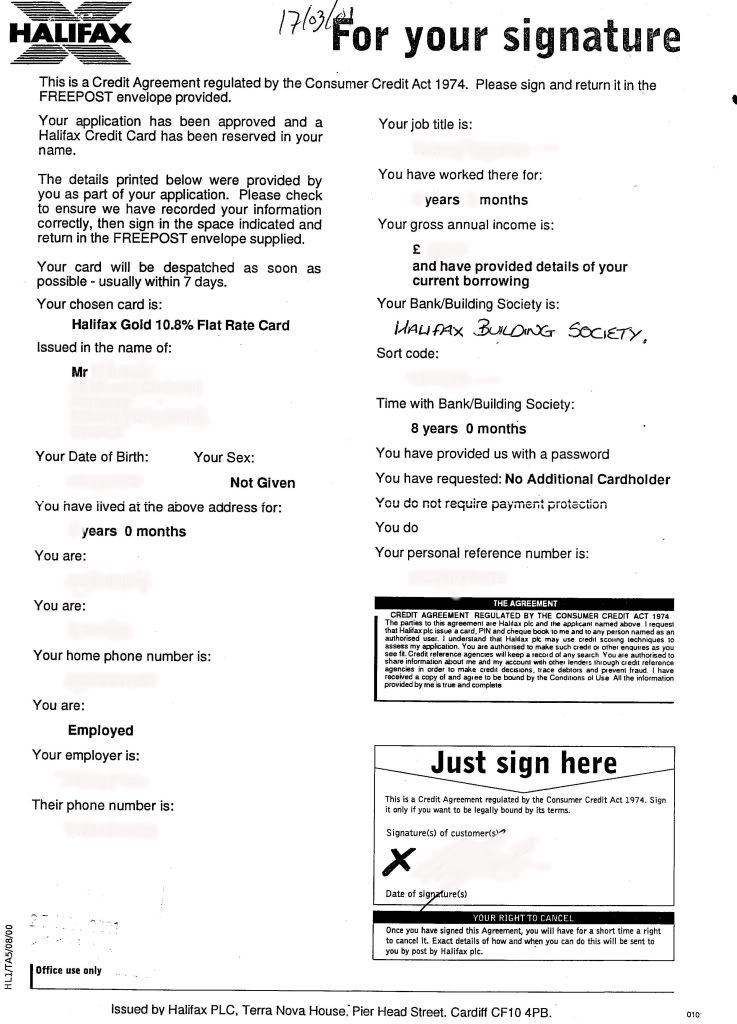

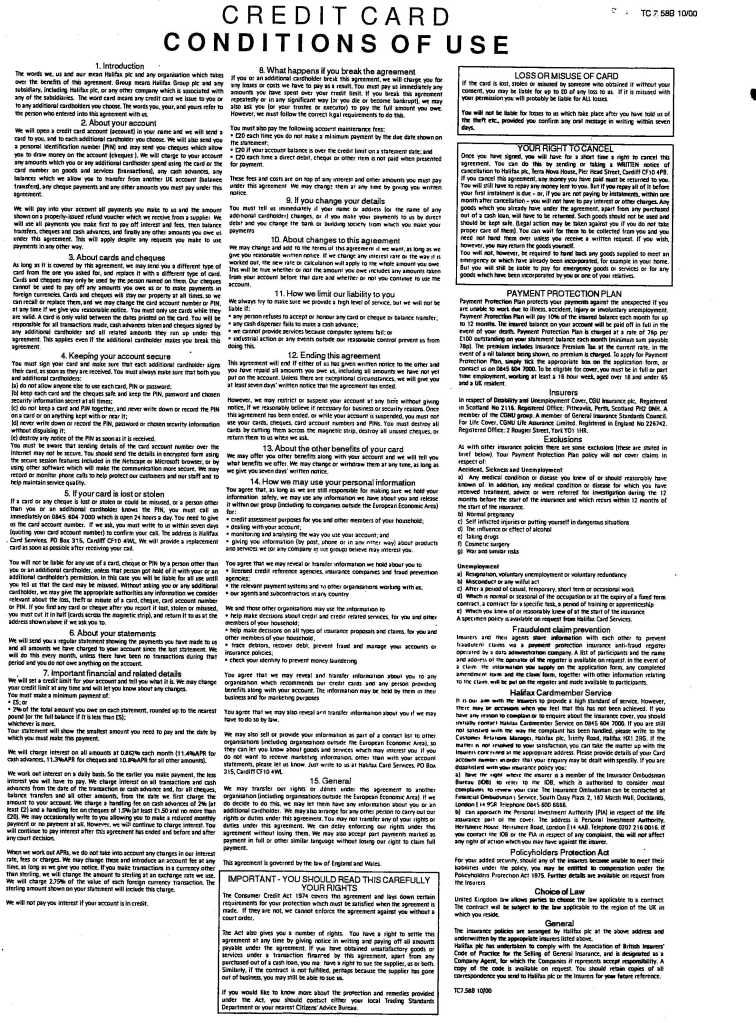

There is no reference on the first page of the agreement to the terms and conditions which are printed on the reverse. This leads me to believe this is not a true copy of said agreement. If you believe that it is a true copy then why is there two different statements regarding my right to cancel the agreement, one on the front page and one on the reverse.

The reference on the front page is marked HL1/TA5/08/00 and on the reverse it is marked TC 7.58b 10/00. This also leads me to believe they are not the same document. If they are not the same document then I am sure you are aware that the absence of these terms will render a document unenforceable in court and I also wish to point out that these terms MUST be contained within the agreement and NOT in a separate document headed terms and conditions or words to that effect.

For your information in case you are unsure. The prescribed terms referred to are contained in schedule 6 column 2 of the Consumer Credit (Agreements) Regulations 1983 (SI 1983/1553) and are inter alia: - A term stating the credit limit or the manner in which it will be determined or that there is no credit limit, A term stating the rate of any interest on the credit to be provided under the agreement and A term stating how the debtor is to discharge his obligations under the agreement to make the repayments, which may be expressed by reference to a combination of any of the following--

(a)Number of repayments;

(b)Amount of repayments;

©Frequency and timing of repayments;

(d)Dates of repayments;

(e)The manner in which any of the above may be determined; or in any other way, and any power of the creditor to vary what is payable.

Could you please explain the following points below.

There is no term stating how I am to discharge my payments to the Halifax.

The only term referring to the rate of interest to be applied is the description of the product itself Halifax Gold 10.8% Fixed Rate Card

No credit limit is stated

I would also like an explanation as to why my termination notice pre dates the point at which I can remedy the default notice, on this basis alone, my liability is no more than the arrears when the default was issued.

I have kept all correspondence between myself and the Halifax including envelopes, proof of postage and including all the letters from the various Dca's to which you have passed my details onto, which I hope you are able to substantiate with documentary evidence that conditions in paragraph 1 to 4 of Schedule 2 of the Data Protection Act are being met.

I would like to inform you that should this be brought before the court I will be relying on such evidence to file my defence.

I eagerly await your reply.

Yours Faithfully

Any advice greatly appreciated

thanks

-

Hi,

A bit of background to the situation. At the beggining of this year after loosing my job I could not afford to meet my loan payments. I telephoned not so intelligent finance and explained my situation. We agreed a reduced payment plan up until Feb 2011. I asked for this in writing and I still hold the letter.

Now this week I received a letter from the Moorcroft Muppets, stating notice of intended litigation unless I pay full outstanding balance. Can they do this when I have proof of an arrangement ?

Could someone please advise me if this reply I am about to send look ok

Dear Sir/Madam

I am some what confused regarding your letter dated 24/06/2010 regarding intended litigation. I would like you to please explain why this account has been passed to you when I have an agreement with Intelligent Finance regarding payments until 06/02/2011. These payments have been met in full and on time since 03/04/2010.

I am very displeased with your letter and will be seeking legal advice regarding this situation.

I hope this clarifies the matter and I eagerly await your response.

Many Thanks

-

Cheers Mould,

Nice paragraph, sounds like my head last night. I must be turning into one of the darn robots

regards

-

Thanks for your comforting advice. With regards to arrears could you please explain as I dont fully understand. Do you mean I am only liable for the outstanding balance when the acc terminated or the actual arrears (ie 2 months payments) on the Dn

thanks again

-

Again one of my arguments, I have not had chance to remedy the default notice in the prescribed time as they terminated 9 days beforehand

-

Hi mozz1, Thank you for your detailed response. I feel I have many arguments to throw at the halifax regarding this account. I am just worried if I try settle these arguments before court I am just aiding their defence for a claim, I think it would be better to wait for court proceedings should they occur. After reading their latest response I have 8 weeks to reply, just undecided on what response to give without giving them to much ammo so to speak. At the same time I am eagerly waiting for a response to my SAR application

-

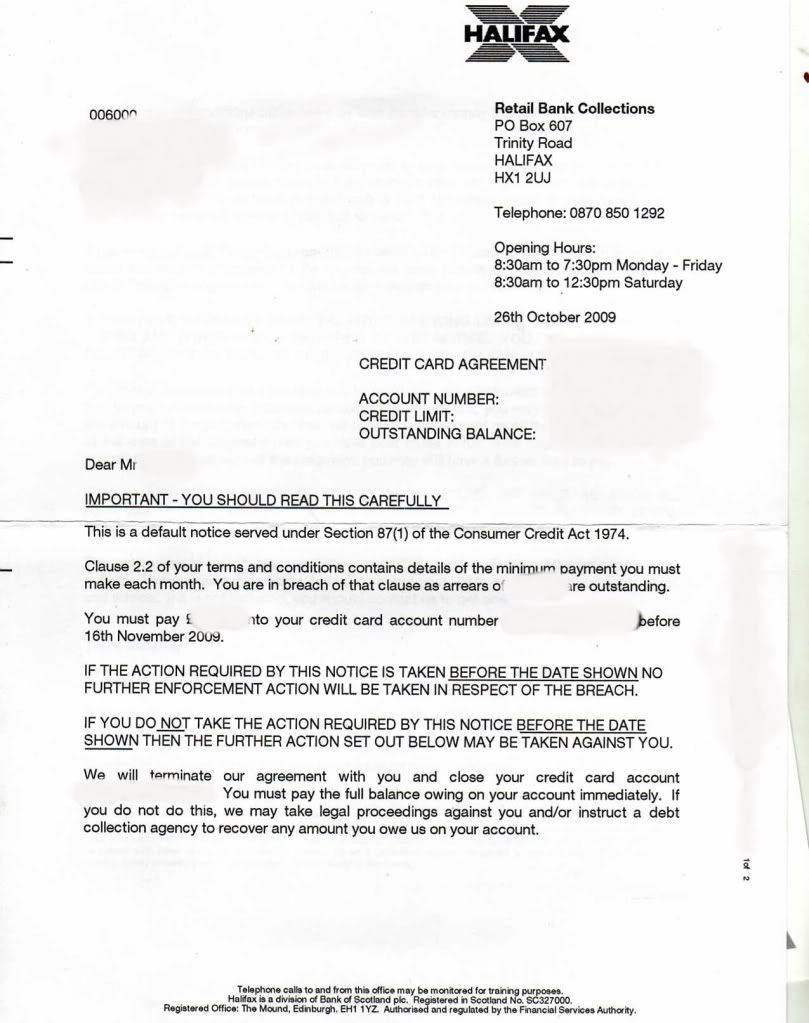

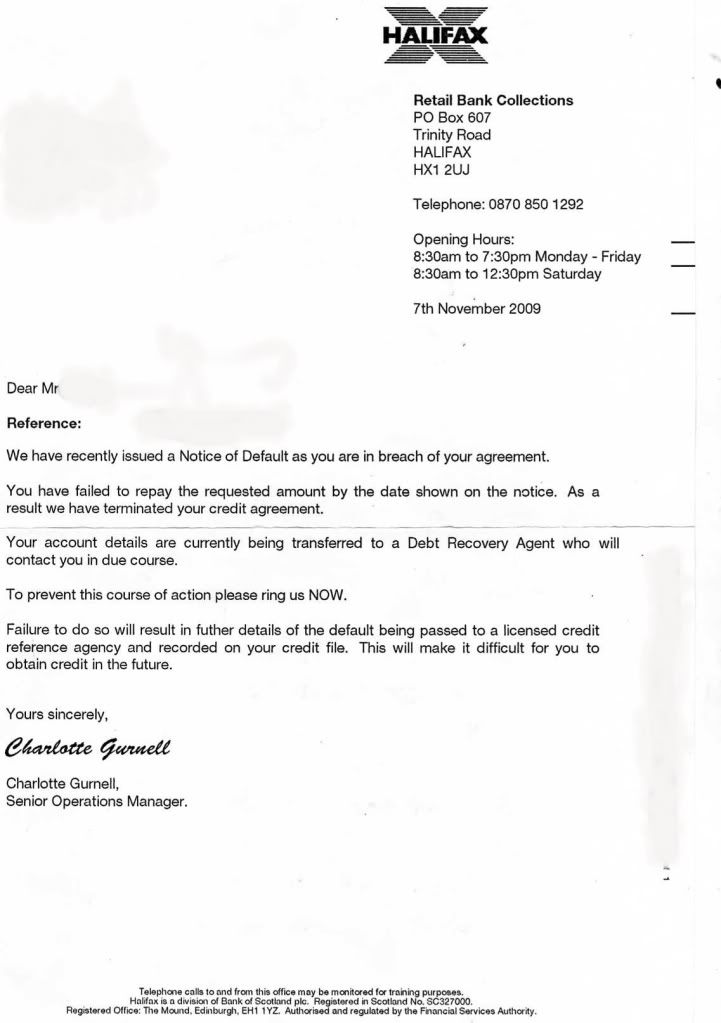

Hi here is a copy of the default notice and a letter I received very shortly after

http://i386.photobucket.com/albums/oo308/faulty500/dnotice1.jpg

http://i386.photobucket.com/albums/oo308/faulty500/dnotice2.jpg

-

Thanks for the advice, I dont want them to come back and try for more once the payment has been sent. I think I will write to them and try for full and final otherwise it looks like £10 a month for years.

Thanks again

-

Hi, Could someone please advise as to whether this offer of a full and final settlement would be acceptable or will these people try and come back forr more. A family member has agreed to settle the sum but I am unsure if its a trick or not

letter is as follows

http://i386.photobucket.com/albums/oo308/faulty500/trton.jpg

I have 14 days to pay so any advice would be greatly welcomed

thanks in advance

-

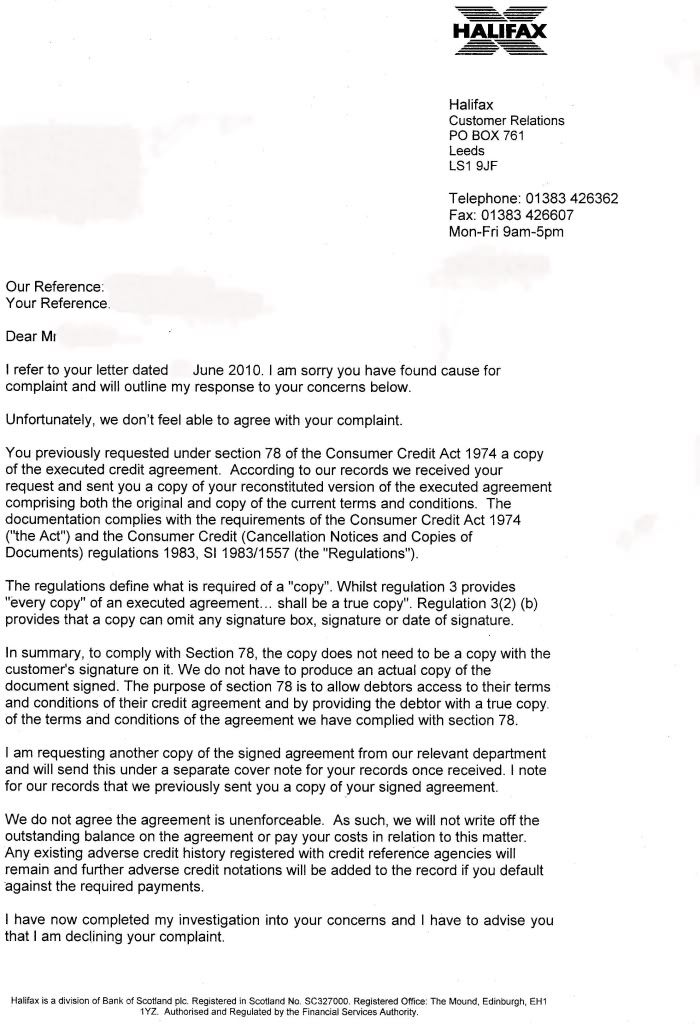

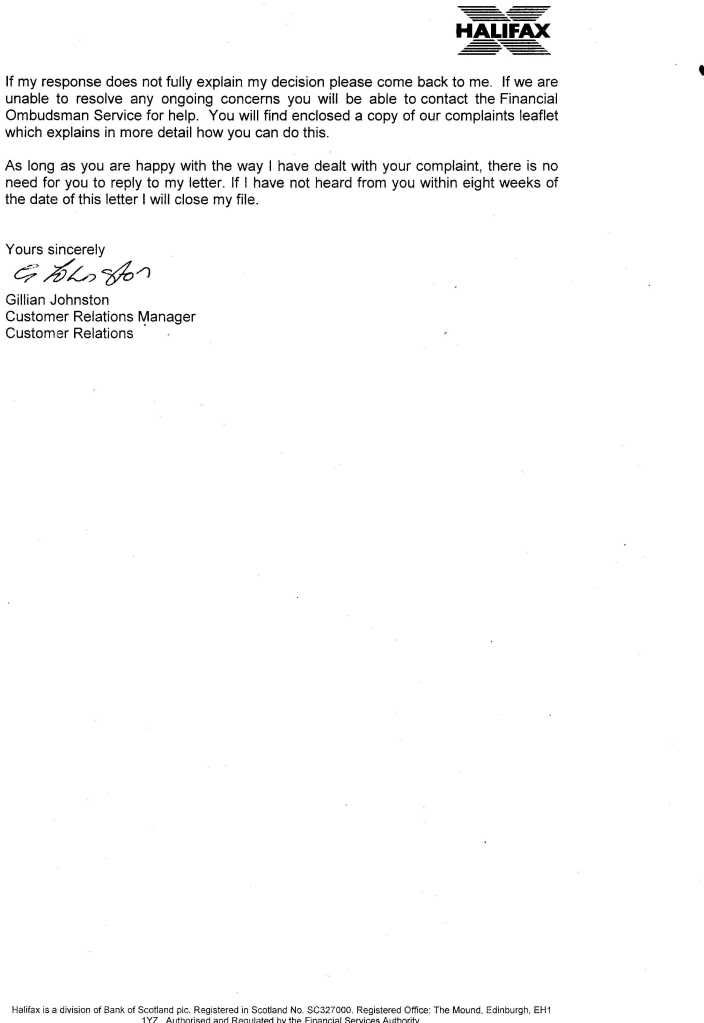

Hi, Received the following letter today along with a typed copy of new terms and old terms, feel like im going round in circles with them

http://i386.photobucket.com/albums/oo308/faulty500/halrep1.jpg

http://i386.photobucket.com/albums/oo308/faulty500/hreply2020.jpg

This is in reply to the to the above letter I sent them last week

thanks

-

Word of advice, Dont speak to them by phone get everything in writing so you have proof, and keep all letters and envelopes and write the date you received them on envelope

-

Thank you so much for the help and I will keep updating as things unfold

-

Hi would this covering letter be ok

Litigation Department

Arrol House

Viking Way

Rosyth

Fife

Ky11 2UT

Dear Sir/Madam

Ref :-

Please find copies of the correspondance between myself and the Halifax. In my opinion the account has been in dispute since the 15th june 2009 due to you not responding to my legal request to supply me a true copy of the original executed consumer credit agreement. I consider that the matter has not been resolved to my satisfaction and I still consider the matter in dispute and that any attempt of litigation will be vigorously defended.

I look forward to your response

Yours Faithfully

-

Thank you I am on it right away

-

Hi, New SAR sent this morning as one last year only gave me statements. Yes have received default notice and will scan and post up. Here is my agreement that they sent to me last year. Thanks for the help

http://i386.photobucket.com/albums/o...reement1-1.jpg

http://i386.photobucket.com/albums/o...reement2-1.jpg

Ps terms were printed on opp side of agreement and print codes do not match

-

Could someone please take a look at this letter I have received from the Halifax. The account has been in dispute since last year and I have been passed between Their DCA's for months. But today I received this letter from Halifax themselves and after reading similar posts I think I need to reply to it.

http://i386.photobucket.com/albums/oo308/faulty500/halifax1.jpg

Could anyone please advise

thanks

b

-

-

thank you im just reading it. Same app/agreement as ours too

thanks again

-

Thanks for that will try and find, Just worried myself a little when I googled pre action conduct practice direction and it came up that this is the first step to court action.

But on reading I found this paragraph which may be useful

Examples of non-compliance

4.4

The court may decide that there has been a failure of compliance by a party because, for example, that party has –

(1) not provided sufficient information to enable the other party to understand the issues;

(2) not acted within a time limit set out in a relevant pre-action protocol, or, where no specific time limit applies, within a reasonable period;

(3) unreasonably refused to consider ADR (paragraph 8 in Part III of this Practice Direction and the pre-action protocols all contain similar provisions about ADR); or

(4) without good reason, not disclosed documents requested to be disclosed.

Does paragraph 4 regard not fulfiling a cca request ?

-

Yeah CAG is a great help, Couldnt have got this far without all the help. Just thinking I might reply and offer a F&F of 50p lol might wind em up a bit. Will keep an eye on your thread and will help in any way I can

Just noticed on this latest tree conservation waste of paper it says they will rely on a copy agreement in court, does this sound like they dont have the original ?

-

I totally agree with what you are saying its just this was a strange letter thats turned up out of the blue. To be honest I wish it would go to court, then at least I know where I stand. Like you say maybe its just another empty threat as its coming up to a year since I stopped payments. Oh well only another 5 years to go

I have had statements last year saying thank you for payment when I never made one and letters saying they will accept my offer of reduced payments, what offer ? boy do I have some questions if it does go to court

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Mevsthem vs Halifax cca advice

in Halifax Bank and Bank of Scotland

Posted

Hi, just a quick update as to how things are going. Moorcroft have sent me a offer to pay 75% of balance on my classic card ( the one with just a application). The gold card i think is a few steps further towards court action. Had a letter before action from halifax, replied to it and had a reply saying that they disagree with my dispute and I have 8 weeks to reply. Then low and behold another letter before action.

I have a quick query if anyone could please advise. Going through my paperwork I have noticed payments of £24 on my statements, this has not come from me as i stopped payments in Sept last year. I think they are trying something underhand. Is there any way of me finding out where these payments are from and who has made them ?

Oh and looking at my Default notices, they have pre dated the termination notices not giving me time to rectify. Lovely Jubbly