horsemad1

-

Posts

217 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by horsemad1

-

-

-

Just an update. Ok so I decided to send a CPUTR 2008 letter by recorded delivery to Drydensfairfax, and low and behold on Monday we got a letter from them confirming they had closed the account with them and passed it back to Halifax!!!!!

-

Another question sorry - if they were to try to enforce in Court would they need to produce the original agreement because its pre-2007. Sorry have been trying to read up about CCA's and came across this remark in another thread. Why does being a pre-2007 agreement make a difference? or am I totally barking up the wrong tree?

-

Ok, but could I request that they send me the original and only the original under an s78 CCA request or is there an official letter that you know of that I could perhaps use instead?

-

Hi again theoldrouge and thank you for your reply, but if I send this letter all I will receive is the same copy of the cut & pasted together application form in post #14 as this is what Crapquest provided me with (and other DCA's as Im guessing its all that Halifax have) and that will fulfil their obligations under an s78 CCA request, they will then be able to pursue me & I'll be back to square one wont I?

-

Hi the oldrouge, Drydens first letter I received from them said "We refer to the above matter and note we have been unable to reach an arrangement with you. We have now received instructions to issue a claim against you in the county court to recover the sum outstanding. it is not too late to stop the claim being issued. Please call us on -------- or if you prefer write to us at the address below & we'll discuss an arrangement with you. if you do not contact us by 22nd Sept our instructions are to issue a claim.

Information about our Claim

Under the practice direction - Pre Action conduct we need to let you have information about the claim. You can access the Practice Direction at http://www.justice.gov.uk/courts/procedure-rules/civil/rules/pd_pre_action_conduct#DAVNA2

*The claimant will be Capquest Investments Ltd who owns the account. Their address is .........................

*The claim will be for the balance owing on the account

*We will tell the court you made an agreement with Lloyds Banking Group but failed to repay it as agreed, we will explain that your account was then sold to CapquestInvestments Ltd

*If necessary we'll show the court your credit agreement and statements to prove our claim

*You haven't told us of any dispute that you owe the balance of your account. If you dispute the claim we are willing to try to resolve the dispute without going to Court. we think the most suitable way to resolve any dispute is for us to discuss withyour representative.

*We think it is reasonable to ask you tolet us have a response by the 22/9/14. if you need longer please let us know.

*If you don't comply with the Practice Direction the Court can impose sanctions against you and this may increase your liability for costs

*You can make payments by a variety of means shown on the back of this letter

*If you want advice about this letter, you can contact a solicitor. there are also organisations that offer free advice and assistance, we have listed them on the back of this latter.

Please contact us as a matterof urgency to discuss your account".

I have contacted them and I believeI have a reasonable dispute that neither they nor Crapquest have answered. I have not received a response in wrting form them to my CPUTR 2008 request yet as to whether they have the original agreement.

I appreciate what you are saying Bazooka Boo but I want to push the fact that they nor Crapquest or any other DCA for that matter have responded to this request

-

Thanks bazooka boo but tried the 'cca received does not satisfy request & will not enter into any further correspondence " letter with cap quest & dry dens but I am worried that if I don't reply again they will initiate court action.

-

http://i392.photobucket.com/albums/pp8/julieh2/HalaifaxreconstitutedCCAfrontsid-2.jpg

http://i392.photobucket.com/albums/pp8/julieh2/ReconstitutedCCA.jpg

Also got a set of current terms & conditions.

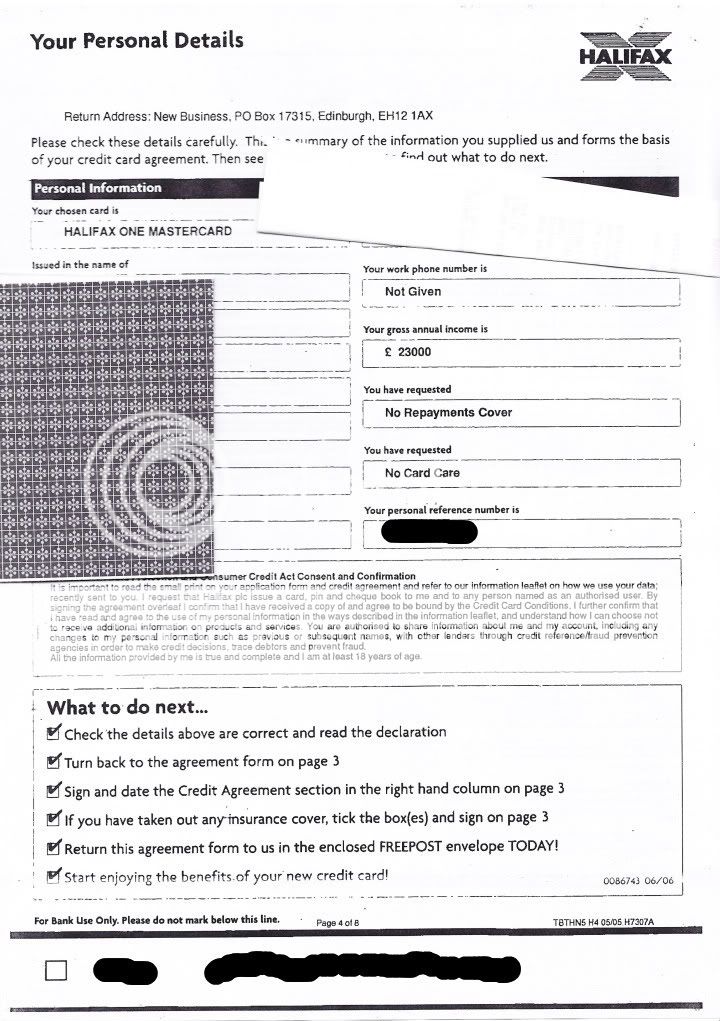

The first page says page 4 of 8 and the second states page 3 of 8, so pasted back to front to make page 4 look like that came first. have never recieved the missing 6 pages?

-

Sorry guys been offline for a while. Thanks for your replies. Crapquest are who drydens are acting on behalf of. Apparently I exhausted capquests complaints procedure after 18 months and then they passed it onto Drydens.

I wrote to drydens on the 13/9/14 basically saying acc is in dispute, should not have been passed on and that a reconstituted copy of a application form with missing prescribed terms and missing pages was not acceptable. I asked that I be allowed to view the original at their offices, I also at the same time made a formal request under CPUTR 2008 that they put in writing whether they actually do have the original.

I heard nothing back until today and got a standard response letter saying I must send the £1 fee anduntil the fee is recived they cannot action my request. Erm cheers Drydens, but you obviously don't read your mail properly, you seem to have missed the point, what about the cut & pasted together so called agreement, what about my formal request for you to put in writing whether an original agreement actually does exist for this account???!!!

Any ideas on a good response to their latest letter please?

-

If you feel that they have failed to comply with their obligations in supplying the CCA, then you could send them this, edit to suit,

Also bare in mind 'why' has it taken them this amount of time to try and reclaim money they say you owe?? Surely Shallowfax would have done it sooner rather than 5 years later??

It's been on the dca roundabout for years, been with cap quest for 18 months & after going through their complaints procedure & them saying they had satisfied my request , they passed it to fairfax.

-

Have also noticed a few more things, the first page of the re constructed application form says page 4 of 8, the reverse of this says page 3 of 8 so obviously cut & pasted together back to front, should I be demanding to see the missing 6 pages?

-

Thanks for your reply CitizenB.

Its been disputed since 2009 when payments also stopped.

Tried to negotiate a reduced payment plan as financial situation was dire but they piled interest on which was higher than the payments being made and when I requested a CCA they then sent me to their debt collectors and been on the DCA merry go round ever since.

it was sold to Capquest but also now owned by LLoyds???? Not sure if Halifax and Lloyds merged.

Yes there are interest and charges on there but no PPI. Im not sure what you mean by a credit card Proper?

Do I then reply to Drydensfairfax stating that the prescribed terms are missing and therefore they cannot enforce in court?

Ok so have started to draft a letter with a little help from another thread. Would this suffice?

"

Thank you for your letter dated 8th September 2014. This account is in dispute and has been for many years. Capquest nor halifax have been unable to supply me with true copies of the properly executed Regulated consumer credit Card Agreement in relation to the alleged Account. Unfortunately neither responses have produced any evidence that the Agreement is Enforceable.

The alleged Agreement appears to be unenforceable for the following reasons:

1. The document is an Application Form and neither carry the correct title if they are to be considered suitable as becoming Agreements once properly executed. The missing Title being 'Credit Card Agreement Regulated by The Consumer Credit Act 1974.'

2. I am entitled to receive a true copy of the Agreement and such true copies must be easily legible. The agreement is not a true copy, nor is it easily legible. Various parts of the copies are defaced and are out of sequence the first page states page 4 of 8, the back of this states page 3 of 8, quite clearly it has been cut and pasted together. Both are also hard to read due to poor quality copying. Furthermore where are the missing 6 pages???

3. The agreement must contain the prescribed terms within the four corners of the agreement, the agreement does not have the prescribed terms within the four corners in fact it does not contain any of the Prescribed terms and furthermore no where on the front is there any reference to terms and conditions being stapled on the reverse.

You should be aware that a creditor is not permitted to take ANY

action against an account whilst it remains in dispute.

The lack of a credit agreement is a very clear dispute and as such the following applies.

* You may not demand any payment on the account, nor am I obliged to offer any payment to you.

* You may not add further interest or any charges to the account.

* You may not pass the account to a third party.

* You may not register any information in respect of the account with any credit reference agency.

* You may not issue a default notice related to the account.

I reserve the right to report your actions to any such regulatory authorities as I see fit including but not limited to Trading Standards, the Office of Fair Trading, the Information Commissioners Office, The Financial Ombudsman Service and my MP .

If you have the original of my alleged agreement available I request that I be allowed to view it at your offices so I can verify it as the alleged document that I signed.

I must also remind you that any court action you may choose to take would require you to produce the original of the alleged agreement. I look foward to hearing from you within 7 days."

-

Hi this has been backwards and forwards to Capquest for about 18 months, its for a Halifax cc from 2006, my main dispute is that when I requested a CCA I was sent a copy of the application form which had only one of the prescribed terms on it. It did not show the amount of credit, credit limit or repayments, the only thing it has on it is the name and address, rate of interest and signature. They also sent the terms & conditions stapled to it on 8 separate A4 sheets.

They say this is enough and have complied with my request - is this the case? Where do I stand with the fact nearly all the prescribed terms are missing?

Now Drydensfairfax solicitors have got involved I need to respond to them asap as they are threatening court action.

Any advice as to what my response should be would be greatly appreciated.

-

Ok will do. Thanks for your help.

-

Have looked back through paperwork & no notice of assignment from egg. Should I oh down that route as a response to their recent letter?

-

Which is my worry.

Im wondering what I should do or say that will stall them for a while.

Im not convinced the statements theyve provided are real,

I know an SAR would reveal this.

What do you think my plan of attack should be then please?

I guess I need to respond to the letter theyve sent threatening Court action,

otherwise they'll think Im ignoring them ...

... Any ideas of what my response should be please?

-

Nearly £7k but with 25% off I suppose its £5.5k.

Just thought there was an issue with the enforceability of the agreement

and thats why no-one has pushed it till now.

Again, I dont know whether its scare tactics or they really will take court action.

Is it worth sending them a letter saying Im SAR -ing EGG so it may stall them?

While Im thinking about it Im not actually sure I recieved an assingment ltter form EGG

telling me its been asigned to them, might it be worth asking them for this also?

-

Thanks for reply.

Ha no it doesn't your right!!

It says they will advise their client to proceed with county court proceedings....

. It's just odd that no one has chased this in years & now all of a sudden they are on my case.

Should I ignore it then or sar egg?

Just noticed that they appear to be issuing court summons on old egg loans out of the blue on other threads,

so want to try & stall them for 7 months if poss!!

-

Ok since scanning these up have had a letter of assignment from Arrow Global

and a letter fro Wilkin Chapmans today saying they will accept 25% reduced settlement figure or Court.

As Ive only got 8 months to go before its statute barred,

what should I do ?

-

these any better?

-

Hi again been a while but

Wilkin Chapman have come back to say they are unable to provide who payment was made by,

where or how

but have provided a copy of what they say is an Egg statement showing last payment made Dec 08,

it is not on Egg letterhead.

What should be my reply please?

-

http://www.consumeractiongroup.co.uk/forum/showthread.php?399260-Feel-that-you-ve-been-treated-unfairly-by-your-Payday-loan-lender-COMPLAIN-TO-THE-FOS!!

If you believe you have been treated unfairly by the PDL then you should send a formal complaint, initially to their Head office - if they fail to resolve this to your satisfaction then you should follow the instructions in the link above to make complaint to the Financial Ombudsman.

If you have already made a complaint and they have blown you off, then they should have provided you with a final response letter - you can then make your complaint to the FOS.

Thank you citizenb I made a complaint they said I had failed to keep up a payment plan and therefore added interest. However they fa to mention that they did not tell me I owed £14 or that they were adding interest, they also failed to mention that they fabricated me reconfirming a payment plan in 2012 so that they could fail it & add moe interest and that they retook out a loan in my name in April 2013 again so they could claim missed payments & more interest. Their final response was I can pay £379 instead of £2311.79 !!! So I think I prob have a good cause to complIn to the FOS. Thanks again

-

Absolutely fuming. I very stupidly took out a loan of £150 plus £45 interest total £195 with Cash Genie on 9th January 2010. I was already in financial difficulty and missed the payment; they added interest, charges and late payment fees to the tune of £72 each month which they said they would waive after much negotiation over a payment plan starting April 10 of £5 per month.

I continued paying this until the loan was paid off in June 2012 – or so I thought. I heard nothing further from them until March 2013 and out of the blue I got an email from them stating I had missed a payment, I was a little confused by this &wrote back to them saying that I did not owe anything and would not be paying them another penny and I got a series of emails saying I had a declined payment and that they would add interest.

This prompted me to log into my online account, something I had not done since 2010 and to my astonishment they had reapplied a new loan to me in April 2013 and added interest way back to January 2010 and the balance I owed at that point was £1903.91!!!!I immediately wrote back to them stating they had illegally taken out a loan in my name, added interest to a loan that had been repaid and that I would report them to the OFT & FOS. I got an email from them stating they would investigate and then nothing until this week, an email from Carter Forbes stating I now owe £2377.91!!!!

I made a complaint and their Compliance officer broke down what I paid and what they’d charged . I set up a Standing order in 2010 so they couldn’t get my bank details, but it finished 3 months earlier than it should of because I’d miscalculated when it should finish. I owe £14 because of it.

I am in no way intimidated by these idiots but it would appear ignoring them when I assumed they had retreated with their tails between their legs just makes them add interest of £45 per month without telling me and go quiet for a while.What is the best way to tackle them and get rid of them once and for all? I am prepared to pay the £14 but nothing more. Should I offer to pay £14 as my final offer and leave it at that?

I am also prepared to get the OFT and FOS involved. Any advice on best way to proceed would be greatly appreciated.

-

No they haven't stated they can't just that they would but haven't.

Brilliant reply thank you.

I'll fire it off tomorrow & see how that go's.

In meantime I'll try & enlarge my agreement & post back up.

Thanks again

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Capquest/Drydensfairfax - Old Halifax Credit card debt threatening court action

in Halifax Bank and Bank of Scotland

Posted

Ok does this add weight to my case? I started looking back through paperwork (cos I've years of it) and came across a letter from Halifax stating that all they can provide is a copy of the application form and current t's & c's. Does this give me a stronger position in terms of them not having an original signed properly executed agreement?