Ginger08

-

Posts

15 -

Joined

-

Last visited

-

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Hi dx, Unfortunately the FOS have refused to look at my case as they have said i have brought the case to late...... Please see attached. Complainant.Decision (1).pdf -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Thank you. -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Hi This is the email i sent in December. Hi I do apologise but I must say going by your list of varying case studies upon your website i think you are wrong. There are various examples there of let us say loans that have have recently completed, whereby resolutions have been found, they were not deemed out of time just because the policy was entered into at the start of the loan, some +10yrs earlier. What concerned me more was the DMP and thus the CMP & CML membership were only recently concluded.. The comment you have made that PayPlan sold me the two plans I've complained about in October 2007 is somewhat mute as policies were still live within the last 6yrs with regard to payments toward them , even within the last 3yrs , if fact. I would also like to mention. "letters in 2015 from Payplan should have alerted me there was an issue," is again pretty mute as I was not aware then I could complain of mis-selling, there is no evidence I can find before 2017 anywhere that CMP & CML were even reclaimable.! I would also like to point out there is a diff between CMP & CML, they state they are both membership schemes, they are NOT. I also believe the above further answers his exceptional circumstance question...there are none as I believe I don't need any as I am NOT out of time! For the reasons above I don't agree with your decision and would like to have this looked at by an ombudsman as stated in your previous email. Kind Regards. I will post the attachment shortly. here cover letter ed3.pdf

-

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Hi Just had the below sent to me from FOS. with an option to reply by the 1st of Febuary. Is it worth going back to them?? Your complaint about Totemic Limited trading as PayPlan I hope you’re well. It’s been some time since I last got in touch, so I wanted to let you know that your case is still waiting to be looked at by an ombudsman. Because I don’t think we can look at your complaint, the ombudsman will look at the information we have again and decide whether you’ve referred your complaint to us in time. Because I think the letter PayPlan sent you in 2015 should have reasonably made you aware that you had cause to complain, I thought it might be helpful to attach a copy of PayPlan’s letter for your records. I know one of the things you’re unhappy about is that when the plans were sold, you were told taking CMP and CML, would help your creditors agree to your debt management plan. So, you thought you had to have the plans for your debt management plan to be accepted. However, under the headings ‘What is Cover My Payments?’ and ‘What is Cover My Life?’, both products are described as: ‘an optional scheme that is designed by Payplan to run alongside your Debt Management Plan’. I do think this would make you aware there was a problem with the information you were given when the plans were sold, but I know you don’t agree with me on this point. However as I’ve not highlighted the point above to you before, I felt it was important I let you know all the information I’d relied on in coming to my view. If you have any other points you’d like to make, please let me know by 1 February 2021. So, we can consider all the information you want us to before an ombudsman makes a decision. However, if you have nothing else to add, then you don’t need to do anything. We’ll be in touch to let you know once the ombudsman has made a decision. Kind Regards. -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Thanks DX for the advice, I will go back to the FOS and highlight the points you have kindly made and see what they say. Kind Regards -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

So do you think it’s worth challenging the decision and asking a ombudsman to look at it?? Kind Regards. -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

TBH I can’t 100% remember but they said they did and they have the date they sent the letters so I not sure if I can challenge this, can they prove they sent the letters ?? Kind Regards -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Sorry, I’m new to the forum wasn’t sure if my original post had uploaded. -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

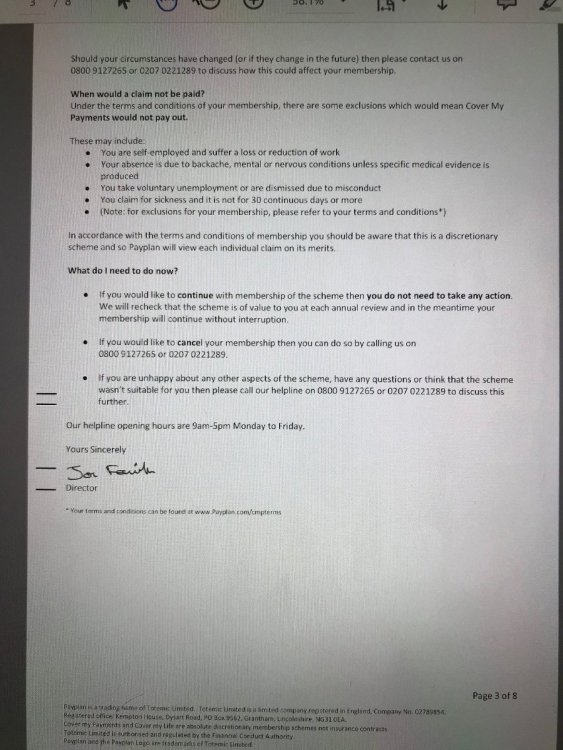

Hi I have just received the below email reply from the FOS, any advise on how to reply. Kind Regards. I’ve now looked at the information we have about this complaint. Although we deal with a wide range of complaints, there are times when we can’t help. Unfortunately, based on what I’ve seen so far, I don’t think your complaint is one we can look into. I’ve explained why below. The complaint You’re unhappy because after getting in touch with PayPlan to set up a debt management plan, they advised you to take ‘Cover My Life’ (CML) and ‘Cover My Payments’ (CMP). In the event of accident, sickness and unemployment, the CMP plan you were sold, would maintain your payments to your creditors in the event of a successful claim. In the unfortunate event of your death, the CML plan you were sold could pay up to £20,000 to your creditors. You believe the plans were mis-sold because: PayPlan told you taking the plans would help your creditor agree to your debt management plan. You had ample life insurance cover in place to cover your debt in the event of your death. You were in a salary paid job so you would have received full pay in the event of sickness. If you were made redundant, you’d have received redundancy pay because you had been with your employer for over two years. You feel that PayPlan took advantage of the situation you were in and you felt pressured to take the two plans you were sold. You’ve told me you took CMP and CML because PayPlan allowed you to believe the plans were needed for your debt management plan to be acceptable to your creditors. Why we can’t help I’m sorry to hear about the circumstances in which you’ve told us your plans were sold. However, to bring a complaint to our Service time limits apply. Our rules set out in the Financial Conduct Authority (FCA) handbook, says our Service can’t look at a complaint if it was made more than: six years after the event complained of; or (if later) three years from the date you became aware (or ought reasonably to have become aware) that you had cause for complaint. PayPlan sold you the two plans you’ve complained about in October 2007. However, you didn’t complain until February 2020. So, it’s been more than six years since the plans you’ve complained about were sold. When this happens, we can only look at your complaint if we think you’ve complained three years from the date you became aware or should reasonably have known, the plans may have been mis-sold. I’ve considered your testimony carefully. And I don’t doubt that you didn’t know there may have been an issue with the sale of the plans, until you read the media article you’ve told me about. However, the rules are quite clear that the three year time limit will also start from the point you reasonably should have known that you had cause for complaint. I can see that PayPlan wrote to you about the two plans you were sold on 6 March 2015. In the letter you were sent PayPlan advised that after conducting a review of the CMP & CML membership scheme, it discovered that over time the information it had been providing to its clients about the schemes ‘might not have always been clear. As an existing member of the two schemes, the letters you were sent explained that “PayPlan wanted to confirm you were eligible for the product, it is suitable for you and that it is providing value”. Under the headings “Who is unlikely to be suitable for the scheme?” I can see it explains that: CMP would not be suitable for “anyone who considers themselves at low risk of suffering an income shock”. CMP & CML would not be suitable for “anyone who wants the benefits of the scheme but already had an alternative product which provided sufficient protection”. The letters you received under the heading “What do I need to do now?” said that: If you would like to continue with membership of the scheme then you do not need to take any action. We will recheck that the scheme is of value to you at each annual review and in the meantime your membership will continue without interruption. If you would like to cancel your membership then you can do so by calling us on 0800 9127265 or 0207 0221289. If you are unhappy about any other aspects of the scheme, have any questions or think that the scheme wasn't suitable for you then please call our helpline on 0800 9127265 or 0207 0221289 to discuss this further. Based on the content of the letters you were sent, I think PayPlan had taken steps to notify you that there might have been a problem with the information you were given when the two plans were sold. You’ve said you had ample life cover in place and other provisions through your employer which meant you’d have been able to cover your debt. When you received these letters, I think this information about your circumstances would have been known to you. So, when PayPlan explained that the plans may not be suitable if you “…already had an alternative product which provided sufficient protection”, I think their letters reasonably raise a level of awareness that the plans you were sold may not have been suitable. I’ve thought about your comments that you were unaware that “the PPI type payments were reclaimable or could be construed as mis-selling”. I don’t doubt this. And while there’s not an expectation for any customer to know or understand what’s construed as mis-selling, I think the letters provided enough information about in what circumstances the product wouldn’t be suitable, to have understood that the plans you were sold may not have been suitable for you. I know the reason you carried on with the plans, is because you believed you needed CMP & CML in place for your creditors to accept your debt management plan. However, I can see the letters advise you to get in touch if you’d like to cancel the plan. This suggests the plans can be cancelled and you didn’t need to continue with it. I think the three-year time limit starts from March 2015, on the date PayPlan sent you the letters I’ve referred to above. I’ve said this because the letters explain in what circumstances the plans wouldn’t be suitable. I’m also satisfied that when you received the letters, you’d have known about the other provisions you had in place that could have helped with your repayments. In line with the rules, you’d have had until March 2018 to complain. Three years from the date you reasonably should have become aware that you had cause for complaint. You didn’t complain to PayPlan until February 2020. So, I don’t think you’ve raised your complaint in time. In these circumstances the rules say we can consider a complaint that’s been made outside of the time limits, if there were exceptional circumstances which prevented you from bringing your complaint. When I asked you about exceptional circumstances you said, “you were unaware the mis-selling of these products were questionable”. I understand this, but for the reasons I’ve explained above, (I think Pay Plan’s letter highlights the information members were given might not always have been clear and the plans may not have been suitable), I can’t say this prevented you from bringing your complaint sooner. I know this isn’t the answer you were hoping for, but for the reasons I’ve explained, I don’t think our Service can consider your complaint. Next steps If you decide that you don't accept what I’ve said, then please let me know by 21 December 2020. If I can’t resolve things then an ombudsman here can look at everything again and make a decision. If I don’t hear from you by that date we might not be able to look at your complaint again. -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Hi I have just received the below email reply from the FOS, any advise on how to reply. Kind Regards. I’ve now looked at the information we have about this complaint. Although we deal with a wide range of complaints, there are times when we can’t help. Unfortunately, based on what I’ve seen so far, I don’t think your complaint is one we can look into. I’ve explained why below. The complaint You’re unhappy because after getting in touch with PayPlan to set up a debt management plan, they advised you to take ‘Cover My Life’ (CML) and ‘Cover My Payments’ (CMP). In the event of accident, sickness and unemployment, the CMP plan you were sold, would maintain your payments to your creditors in the event of a successful claim. In the unfortunate event of your death, the CML plan you were sold could pay up to £20,000 to your creditors. You believe the plans were mis-sold because: PayPlan told you taking the plans would help your creditor agree to your debt management plan. You had ample life insurance cover in place to cover your debt in the event of your death. You were in a salary paid job so you would have received full pay in the event of sickness. If you were made redundant, you’d have received redundancy pay because you had been with your employer for over two years. You feel that PayPlan took advantage of the situation you were in and you felt pressured to take the two plans you were sold. You’ve told me you took CMP and CML because PayPlan allowed you to believe the plans were needed for your debt management plan to be acceptable to your creditors. Why we can’t help I’m sorry to hear about the circumstances in which you’ve told us your plans were sold. However, to bring a complaint to our Service time limits apply. Our rules set out in the Financial Conduct Authority (FCA) handbook, says our Service can’t look at a complaint if it was made more than: six years after the event complained of; or (if later) three years from the date you became aware (or ought reasonably to have become aware) that you had cause for complaint. PayPlan sold you the two plans you’ve complained about in October 2007. However, you didn’t complain until February 2020. So, it’s been more than six years since the plans you’ve complained about were sold. When this happens, we can only look at your complaint if we think you’ve complained three years from the date you became aware or should reasonably have known, the plans may have been mis-sold. I’ve considered your testimony carefully. And I don’t doubt that you didn’t know there may have been an issue with the sale of the plans, until you read the media article you’ve told me about. However, the rules are quite clear that the three year time limit will also start from the point you reasonably should have known that you had cause for complaint. I can see that PayPlan wrote to you about the two plans you were sold on 6 March 2015. In the letter you were sent PayPlan advised that after conducting a review of the CMP & CML membership scheme, it discovered that over time the information it had been providing to its clients about the schemes ‘might not have always been clear. As an existing member of the two schemes, the letters you were sent explained that “PayPlan wanted to confirm you were eligible for the product, it is suitable for you and that it is providing value”. Under the headings “Who is unlikely to be suitable for the scheme?” I can see it explains that: CMP would not be suitable for “anyone who considers themselves at low risk of suffering an income shock”. CMP & CML would not be suitable for “anyone who wants the benefits of the scheme but already had an alternative product which provided sufficient protection”. The letters you received under the heading “What do I need to do now?” said that: If you would like to continue with membership of the scheme then you do not need to take any action. We will recheck that the scheme is of value to you at each annual review and in the meantime your membership will continue without interruption. If you would like to cancel your membership then you can do so by calling us on 0800 9127265 or 0207 0221289. If you are unhappy about any other aspects of the scheme, have any questions or think that the scheme wasn't suitable for you then please call our helpline on 0800 9127265 or 0207 0221289 to discuss this further. Based on the content of the letters you were sent, I think PayPlan had taken steps to notify you that there might have been a problem with the information you were given when the two plans were sold. You’ve said you had ample life cover in place and other provisions through your employer which meant you’d have been able to cover your debt. When you received these letters, I think this information about your circumstances would have been known to you. So, when PayPlan explained that the plans may not be suitable if you “…already had an alternative product which provided sufficient protection”, I think their letters reasonably raise a level of awareness that the plans you were sold may not have been suitable. I’ve thought about your comments that you were unaware that “the PPI type payments were reclaimable or could be construed as mis-selling”. I don’t doubt this. And while there’s not an expectation for any customer to know or understand what’s construed as mis-selling, I think the letters provided enough information about in what circumstances the product wouldn’t be suitable, to have understood that the plans you were sold may not have been suitable for you. I know the reason you carried on with the plans, is because you believed you needed CMP & CML in place for your creditors to accept your debt management plan. However, I can see the letters advise you to get in touch if you’d like to cancel the plan. This suggests the plans can be cancelled and you didn’t need to continue with it. I think the three-year time limit starts from March 2015, on the date PayPlan sent you the letters I’ve referred to above. I’ve said this because the letters explain in what circumstances the plans wouldn’t be suitable. I’m also satisfied that when you received the letters, you’d have known about the other provisions you had in place that could have helped with your repayments. In line with the rules, you’d have had until March 2018 to complain. Three years from the date you reasonably should have become aware that you had cause for complaint. You didn’t complain to PayPlan until February 2020. So, I don’t think you’ve raised your complaint in time. In these circumstances the rules say we can consider a complaint that’s been made outside of the time limits, if there were exceptional circumstances which prevented you from bringing your complaint. When I asked you about exceptional circumstances you said, “you were unaware the mis-selling of these products were questionable”. I understand this, but for the reasons I’ve explained above, (I think Pay Plan’s letter highlights the information members were given might not always have been clear and the plans may not have been suitable), I can’t say this prevented you from bringing your complaint sooner. I know this isn’t the answer you were hoping for, but for the reasons I’ve explained, I don’t think our Service can consider your complaint. Next steps If you decide that you don't accept what I’ve said, then please let me know by 21 December 2020. If I can’t resolve things then an ombudsman here can look at everything again and make a decision. If I don’t hear from you by that date we might not be able to look at your complaint again. -

Payplan - Cover My Life & Cover My Payments

Ginger08 replied to Ginger08's topic in Debt Management Plan Companies

Hi DX, Thank you for your reply, FOC have mentioned a time limit of bringing a claim. I have been paying the premiums for cover my life and cover my payments since Dec 2007 when I set up the DMP until Feb 2020. Can they refuse to look at the claim because it has taken this long for me to complain. Thanks Ginger. -

Hi, I'm currently looking to reclaim my payments paid to Payplan for the cover my life and cover my payments. The F.O.S. are looking at the case now and have asked the questions below. However, PayPlan sold you CML and CMP in October 2007. And time limits apply if you want to bring a complaint to our Service. Because the sale of the products you’ve complained about took place more than six years ago, I’m concerned that you may not have referred your complaint to us in time. Because it’s been more than six years since the products you’ve complained about were sold, we can only consider your complaint in certain circumstances. To understand whether those apply here, I’d be grateful if you could help me with the following questions. When did you first realise your plan had been mis-sold? You mentioned seeing some information online, do you remember when this was and why this meant you realised you didn’t need CML and CMP for your debt management plan to be accepted. I understand that over the years PayPlan sent letters explaining the cover they’d sold may not have been suitable. Did you take any action in response to these letters? If you did can you explain what action you took. If you didn’t take any action, please explain why? Finally, can you please tell me if there were any exceptional circumstances which prevented you from referring your complaint to us sooner. How should I respond? Thanks.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS