Monty2007

-

Posts

1,341 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by Monty2007

-

-

Ask Blondie,

She got something in her head about all this maybe she can spell it out to us i hate guessing games.

I was asking you, having read your previous threads.

-

You have made me smile in this bleak situation !!

Conspiracy nothing is what it seems lol

So, what is your game?

-

I think CapQuest might have been a bit sharper on this than we would normally give them credit for.

-

...you are entitled to your opinion...

Yes I am.

-

Hi Monty

I thought I had managed to delete any reference to who the company were, but hey!

Yes I have just had a rather heated telephone conversation with them as they started my claim in july 09 and kept fobbing me off with excuses, three people have been "dealing" with my claim and all no longer work with the company anymore!

This reference I quoted is of interest as it may be significant to my claim against the company these were trying to sort out

Cas

No problem Cas. It is probably best to do it yourself, you then have control and it really is not that difficult. All the infomation, resources and help is available here on CAG!

-

Damian - I cannot understand why, having failled to ensure you sent the item tracked, you feel it is 'all Paypal's fault'. Surely you appreciate, that even if you were not the victim of fraud, if the buyer was genuine and stated he did not recieve the goods, you'd be in the same situation?

As for further action... that damage has already been done. You;re wife's credit file will probably show thew PayPal default and this will sit on her file for 6 years. So assuming it is in place, you've only another 5 years to sit it out!

I have consistently found your posts less than helpful.

-

What does this mean in laymans terms please

The non disclosure of commissions or feesA lender potentially breaches the non disclosure of commissions or fees part of the consumer credit act is when a lender: pays a commission to a third party such as a finance broker or another division of the lender in recognition of their assistance in the lender providing a credit card or loan agreement. This is because section 155 of the consumer credit act 1974 which states: “in the case of an individual desiring to obtain credit under a consumer credit agreement, any sum payable or paid by him to a credit- broker otherwise then as a fee or a commission for the credit-brokers services shall for the purposes of subsection (1) be treated as such a fee or commission if it enters, or would enter, into the total charge for credit"

They are a claims management company and you would be best advised to do it yourself. Plus that state on their site that they are not taking on any new cases and have been a bit naughty having had their license suspended. See:

----------

Dear Clients,

Great News, Kerobo's ministry of justice license suspension has been lifted.

Follow this link to verify on the MOJ's website. Following a lot of hard work alongside the Ministry of Justice we have had our license suspension lifted.

We have made an undertaking to the Ministry of Justice that we will process all existing claims to the standard that is expected of an authorised claims management company but that we will not take on any new business, so unfortunately if you have not already signed up we won't be able to help you.

-------------

Not sure about the "Great News" bit though..........

-

Many thanks to cerberusalert for the info on how to get view attachments.

I thought all docs had to be uploaded via the attach files facility, maybe this information should be on the instruction board for docs to attach to posts?:idea:

As Beachy said, your reference and name/address can be seen on this document and Amex and their sols monitor CAG.

Brachers are being very cocky here, no doubt spurned on by some recent cases.

Did you recieve a DN for these accounts?

Please also confirm that they are credit cards and not charge cards?

-

The prescribed terms for a loan and insurance must be set out separately as I indicated in a post above. One is restricted use, the other is unrestricted use and that makes it a multi agreement.

Loan

Interest

Total Charge

Signature Box

Insurance

Interest

Total Charge

Signature Box

Thanks Pinky, I see your point wrt a multi agreement.

-

Separate signature box or not the loan details have to be set out separately - they are lumped together. The prescribed term for the loan is thus wrong.

Hi Pinky, can you elaborate please? I have the same format of agreement (replace HBOS with Sainsburys Bank plc). The loan details are separate and in a box - why are the prescibed terms wrong?

-

Hi Monty,

So, my initial reading of your post is that it is indeed a carrrrrrrrrrrrrazy idea, ok no sweat. I actually don't care about the frills and spills of CCJ's and 6 years on being in the credit wilderness, so disalusioned with it all I could really care less about the fall out. Still, my point was that I would liquidate my owed £4k into some kind of mannagable FIXED sum and not this ever expanding national debt figure, that is/was the whole point of the exercise. Is there any other way to agree a fixed sum with the creditor or do they wish to play the role of Shylock ad nauseum?

Thanks for the reply, its appreciated!

Dear baba

I should also have mentioned that the bank may sell the debt to a DCA who may continue to add interest, so your plan may fail there. You should consider going onto a debt management plan and may be able to get zero or reduced interest that will allow you to pay off the capital.

I would not say that your suggestion is crazy, just that there are some alternatives that you should consider and potentially cheaper and less risky.

If it were me, and I just had that one debt then I would write to them and offer a repayment plan and request zero interest. If you don't ask......you don't get.

I would also suggest that you read the threads on Virgin Credit Cards, there may be some information that could be of use.

Good luck!

Monty

-

BOS repudiated the account when they sold it to CQ after issuing an unlawful DN.

Pinky. Why do you consider the DN to be "unlawful"?

-

A complete waste of £10 in my opinion. All a buyer buys is the details - the documentation stays on the records of the original creditor.

You may well be correct Pinky, I will update on what I get back from CQ.

-

You don't want to SAR both - all CQ will have is the name, address, agreement and amount. BOS retains all the information on the account as the original creditor. I don't know where this sending SARs to the DCA crept in.

That was my suggestion. CapQuest now own the debt so are not acting as a DCA. It would be useful to know what they have in their system, I suspect that this debt was sold as a job lot by HBOS back in December along with mine. I have been expecting CQ to litigate but they seem to be hesitating at the monent, not sure why given their mode of operation on other threads.

For £10 it is money well spent............

-

I had a kind of brainwave today! About Credit Card debt of which I have in spades. Currently I owe Virgin Credit approximately £4k and I have fallen behind in payments which has made them "irritable", poor them. Anyhoo I currently pay £130/month towards, well, nothing really, it's just thrown away in real terms it doesn't even touch the £4k it just minimises the interest on the £4k but not the core £4k itself. What a complete waste of time its proving to be, so, now the brainwave!!! Think about it in simple terms.

If I default on payments and let them take me to court I will naturally lose the case however, a judge shall find me in fault to the sum of £4k ONLY. He shall find me in default of £4k as a FIXED sum and therefore order me to pay that sum (and court costs of course) but then legally I shall only be liable for that sum and not years of interest on top of that, is this fantasy on my part or is this an actual way forward? I am sick and tired, probably like most on here, of paying interest on a sum of money that will never ever ever be paid off.

Thoughts please

PS I am a Scot living in Scotland so legal system may differ from the rest of the UK.

Well, if you follow through this scenario you will get a CCJ and if you default on that then they will enforce this through Bailiffs. It will also trach your credit record for at least 6 years.

Alternatively you may want to try to negotiate a full and final settlement.

You can always reclaim back the charges through the FOS or court action so this may bring down the total balance.

When was the card taken out? have you asked for a copy of your agreement using S78(1) of the CCA?

The law is very different in Scotland, but the same CCA and SI's are used, just the Civil Litigation process is different, also we don't have CPR in Scotland and disclosure is easier with respect to agreements and key documents.

-

1) Point 1

Subject access request i thought i send to the Bank of Scotland?

You say send it to Capquest? please clear this up i'm confused.

Pinky,

Have you got a letter which i can send that represnts what you are talking about please?

HBOS no longer own the debt, it was purchased by CapQuest, you may wish to SAR both.

-

It is not like them not to go for the jugular on an amount of money like this so they must know there is something wrong with it.

BOS repudiated the account when they sold it to CQ after issuing an unlawful DN. If you are 100% sure it was sold to CQ, to make this legally binding you HAVE to write to BOS and tell them that you accept the repudiation of agreement which occurred when they sold the agreement NO......... dated.............to CQ after issuing an unlawful DN. If you have the date when it was sold insert it.

After you have sent that letter, you can write to CQ and state that the alleged agreement is unenforceable and was repudiated by BOS when it was sold to CQ after issue of an unlawful DN. You trust that settles the matter.

Hi Pinky

I have the same DN, why do you think it is "unlawful"?

-

I have now completed and printed off the Subject access request to the Bank of Scotland and will send recorded delivery in the morning.

Capquest have not asked for any money, there reply at this stage was to inform me the debt was not statue barred in response to my limitattion act letter. They then included a form for me to fill out with my breakdown cost etc rent living gas electric etc.

But no talk of money at this stage or any other dialouge.

There letter was basic and brief but yes they have purchased the debt from the Bank of Scotland.

What do i do in the meantime should i write to them??????????????

At this point I would just send off the SAR to CrapQuest, they have just received mine so will be busy.........

I am in the same situation as yourself but with Sainsburys Bank who are jointly owned by HBOS. My agreement and DN are signed by the same people as your HBOS documents, only you agreement has charges defined whereas mine does not. You may have an angle with the PPI, and also need to check that the APR is correct.

If you can hold this off until it becomes statute barred then this would be your best course of action IMO. I would look to see if you can bring a case against them for PPI or any charges and this would remove any ability for them to bring an action and give you some time. Just a thought.........

-

Hi

Have CrapQuest bought this or just collecting?

-

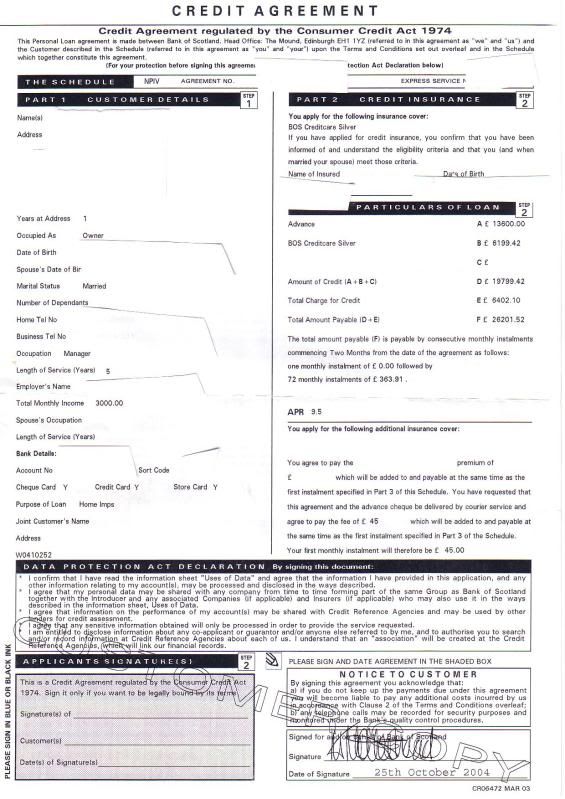

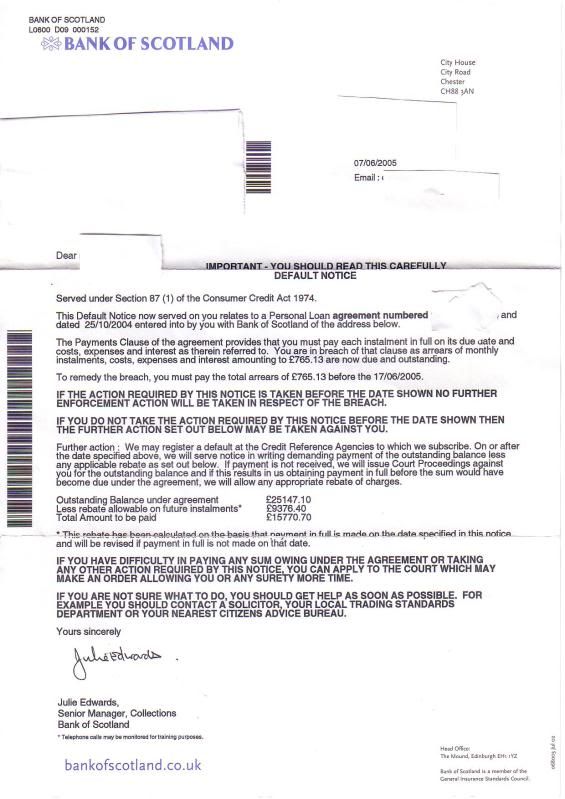

I have started a new thread as i now have the main facts,

Date of loan agreement 25th October 2004

Date of default last payment March 2005

Capquest are chasing this debt.

No acknowlegement or payments so the above dates fully apply.

As you will know the debt will be statue barred in March 2011

Here below are the links for the Customer Credit Agreement and Default notice,

CCA Link

http://i116.photobucket.com/albums/o25/kathleenbilly/CCA.jpg

Default link

http://i116.photobucket.com/albums/o25/kathleenbilly/DF.jpg

Can someone advise me as to what i should do or direct me to a letter i may be-able to send?

Thanks for any advice offered.

Do you know if your debt has also been sold to CrapQuest?

You should request all your documents under a SAR to see what they have.

Both the agreement and DN look okay to me.

-

Hi All,

Been a while since I've been on, but here's my latest question:

In 2004 I accepted a settlement figure from HFC, sent the cheque and they said they's amend all the entries on the Credit Files in my name to show it WASN'T in default and the balance had been settled. They cashed the payment, and didn't change it!

I wrote again, in 2009 and they replied saying they's made a mistake and they'd change it, and they didn't change it!

I wrote again, and sent 8 copies of their agreement letter, and a copy of the cheque, and they didn't change it!

Called them, and finally, after 5 years 9 months they've changed it!

Now the good bit, they've sent me a 3 page letter stating:

- They've made a huge error

- Its all their fault (they didn't change the records)

- They are totally to blame

- They've told ME I've been fiancially disadvantaged because of their error

- They apologised for the way the Staff spoke to me

- Apologised for not recording all the calls

Most importantly they've said "I am due compensation, but I must give evidence to support my claim"

My question is, simply what am I due?

Can I claim:

- For the sub prime mortgage I had to get because of their default notice? (perhaps the difference betweeen the standard mortgage rate of the time against what I paid, which I've worked out to the penny, to be an additional £16,000!)

- For the sub prime loan I got, again because of their default notice?

- The loss of goodstanding with banks (2 banks carried out credit searches earlier this year and said no because the default was till there)

- My pain and grief, and time?

Can anyone give me an idea of what would be reasonable to ask for, and realistically what I'd get? (I can prove the mortgage etc I've paying)

Thanks in advance, and keep up the great work!

Shearersbigtoe

Hi Shearerbigtoe

I would think you are due substantial damages for their error, see:

Richard Durkin v DSG Retail Limited and HFC Bank plc, (Judgement of Sheriff J.K. Tierney, Sheriffdom of Grampian Highland and Islands at Aberdeen (A187/04)

- They've made a huge error

-

We have recieved court summons for a debt that was owed to citi bank in 2003, (we stopped paying this debt oct 2004 and have never acknowledged debt since) this debt was then bought by capquest on 24th march 2005 and they have instructed Yuill & kyle to pursue this debt through court. I have already filed form 07 with court and have now recieved intimation of options hearing, can anyone help or give me info on lodging my defence ( debt has become prescribed by time) or if anyone has been through this could you let me know how you got on. I have spoken to a solicitor today who did not seem to have much knowledge of the law of prescription, (just told us this could cost a lot of money if we lost this case)

Hi Oli/Ida

This is an Ordinary Cause action, so yes the costs could be high if it goes to a legal debate or Proof/Proof Before Action.

Crocdoc has made some good suggestions which make sense BUT in order to help further could you please confirm the following.

1. What type of debt this is: credit card, loan, secured/unsecured?

2. What are your dates for submitting a defence, final adjustments to the Record and Options hearing?

3. What correspondance you have had with the original creditor/DCA and what payments have been made.

4. Have you an agreement?

5. Was a default notice served?

6. Has a termination notice been served?

7. Have you undertake an SAR on the original creditor?

8. Can you post up the exact details of their writ?

Please let us know any other relevant information that will help draft a defence. I have won two Ordinary Cause actions, both for credit cards and one small claims, all settled prior to legal debate.

Regards

Monty

-

1

1

-

-

Hmn but trying to contact THEM was not so easy-I remember that well-couldnt get hold of anyone and they only had one number showing for their Sunnydale offices.

Well Martin, I will have my day in court with them in mid August, I am really looking forward to it....

-

Ah ok.

Think mine was around 2004.They failed to comply with my SAR-not sending everything.

Next thing I knew they sold the account to CABOT-who are in breach of a CCA request.

Hi Martin

Now you mention it, their responde to my SAR was very poor, no statements and just a few screen prints. They did however show 3-4 calls a day to my mobile over a two month period.......

{kind=link}

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Lowell financial

in Debt Collection Agencies

Posted

Allowing DCA's to come onto this forum is a very sad day for CAG.

A totally inaccurate analogy is being drawn between allowing DCA's onto CAG with other, legitimate companies such as Vodaphone. Let's be absolutely clear that companies such as Vodaphone wish to resolve directly the complaints of their end-user customers who are you and me. For a DCA, their customers are the banks and credit card companies that sold them the debt or agreed to pay a fee for collection, by whatever means usually.

So there is no basis whasoever, for comparing a customer-focused company such as Vodaphone with a DCA.

DCA's collect on behalf of their Clients or themselves and are totally without care or scruples, many of us can vouch for that. They operate on the fringes of the law and cause misery to thousands of people on a daily basis. Many on here have been subject to abuse from DCA's and many, many more, who have not found CAG have little or no knowledge of their rights so continue to live in ignorance and fear.

By allowing DCA's to post here and essentially tout for business is not what CAG was established to do, moreover it will serve no purpose other than to allow Lowell et al to do their job with greater ease and with a captive audience.

Well done CAG management, you may as well become a DCA.

I would imagine this will push donations down even further, but then maybe Lowell et al can donate a percentage they get from this forum.