Ruprecht

-

Posts

159 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by Ruprecht

-

-

On the bbc news website today:

http://www.bbc.co.uk/news/business-12622318

It says he is a "High Court Judge" but doesn't say what court he was sitting in when he made the

judgment.

Might be worth getting the decision/transcript...

-

I can't find a thread here about this news article on the bbc today, anyone here involved in the action?

-

hi mould,

most of them are not im afraid. nearly all of the are defective i.e wrong layout and dont give enough time.

also the ones like barclays have not ever produced a signed agreement.

Argos is a signed application.

2 x Shop Direct - need i say more about them

HSBC - had a letter bank from them yesterday saying they do not have a signature for a bank account to conform with DPA.

HSBC - Credit card - faulty default have written to them no reply, the CCA request they sent a bank application form, and copy of terms and conditions.

Have done sars on most of these none produced a written agreement.

hope this give you an idea

B

So you have 5 accounts that have gone south, albeit with faulty default notices and maybe unenforceable agreements?

Why do you think going to manual processing will help you in anyway?

What are you trying to achieve?

Maybe you could do a CIFAS protected registration, that should force everything to go manual:

-

You would be best just sticking to making a complaint to the ICO and seeing how they respond. A court claim will take even longer probably anyway.

The ICO complaint is free and no risk. The CRA will simply defend saying "we don't make any credit decisions"......

Don't go near a court unless you are 100% sure you know what you are doing, best case is you may waste a lot of time, worst case is they will go after you for costs! The CRAs send large law firms to defend...

If the ICO say you don't have a basis for a claim then you know it is a complete non-starter.

-

I have always used a Part 8 Claim to get companies to comply with the Data Protection Act, that is what the ICO office says too. It would cost £150 to start a claim asking the court to make an order.

Not sure if this works, takes ages to load for me:

If you are after damages too you'd have to pay extra for that part of the claim.

The only automated credit making decision process CRAs do is providing a credit score to a lender I would think, do Callcredit do that? I think Experian and Equifax do.

If nothing is inaccurate data wise they hold and you agreed the organisations reporting data on you could, I am not sure where you will get with it.

You might ask them if they provide any sort of credit scoring to lenders first....

-

You shouldn't have to file an application for a strike out. If the court hasn't received directions as requested they should have struck it out as per the order.

Maybe send the court a diary (cheeky) with your letter when requesting they strike it out.

-

If you are not happy with just gifting it and "hoping for the best" repayment wise, maybe you should keep things simple and treat it as a gamble.

Amount you are giving her/Estimated value of House x 100 = Your % share of the house

The Mould is right though, look after your family within reason. There is too much "everyone for themself" these days.

-

Worst case scenario, it'll make me feel better

Thanks for your advice. I'm going to read up on a Letter Before Action and give it to them with both barrels...

You can send them the Letter Before Action now and give them 14 days. Always have it look like you have been reasonable.

Make sure you send it Special Delivery. Recorded sometimes doesn't work out...

I think what might have happened is the only way they can have your debit card pay each month is to enter your information on some arrears payment system so it can take it. So now it looks like you are someone behind in payments making an arrangement to pay.

You need to remind them that you never entered an "arrangement to pay" were never behind with payments and always made the required minimum payment. Your account live without restriction and you feel an error has been made in the inputting it as an "arrangement to pay".

Send them a photocopy of what they are reporting to the CRA and advise them that some lenders deduce an "arrangement to pay" means the customer is struggling or behind payments.

You really need to spell it out to them. I worked for a credit card company 10 years ago and it amazed me how some of the employees managed to dress themselves in the morning. LOL!

If that doesn't work then legal action usually gets them to jump up off their seats. Advise them that once proceedings have commenced you may make an application for an injunction against them for reporting this, claim all legal costs against them and you will be sending the court file/copies of all communications with them to the Office of Fair Trading, Consumer Credit Fitness Enforcement Section.

-

equifax seem particularly bad at allowing dca's to do table 1 searches

I'm currently battling with them trying to get some that are more than 1 year old removed (they state on their webpage that all searches are removed after 1 year) yet these DCA table 1 searches never seem to be removed

You are right about Equifax. All my past problems have been about searches they have allowed without my permission, no other CRA.

I think they own Wescot, a DCA.

O2 have done a credit search on me with them last week and I have never had anything to do with O2. I think it might be some sort of marketing

search/trawl Equifax have allowed but they have recorded it as a Table 1 Credit Search.

I keep asking what information they are providing to these 3rd Parties and if the 3rd Party provided my correct DOB before they released it.

Never get a clear reponse from them.

Also, even if you subscribe to their credit report service for a monthly fee they never answer their landline and take 5 or 6 weeks to respond to an

online query which is usually some out of the country agent that gives a generic response. Dreadful service.

-

I have taken a few companies to court to force them to correct their records under the Data Protection Act. (http://www.legislation.gov.uk/ukpga/1998/29/section/14)

Before you can do that (the nuclear option) you need to give the Data Controller 40 days to correct the data. After that, if it remains wrong, I would send a Letter Before Action too giving them a further 14 days, by Special Delivery to the Data Controller of the company. The register can be searched here: http://www.ico.gov.uk/ESDWebPages/search.asp

I would ignore the credit reference agencies and focus all of your attention on Opus to get this corrected.

I know you are probably angry and want to blame the CRAs too and quiet rightly you should, they seem to accept what they are told with a pinch of salt. However, it is better to focus on the organisation providing them with the information as the CRAs are used to defending all claims and it would be a waste of time going after them and confuse you even more.

Are you 100% sure that the data is inaccurate? Is it some sort of discontinued credit card they are allowing to be paid off over time instead of in full? They might have a defence that it is accurate.

Are you wanting to apply for credit elsewhere and thinking this "arrangement to pay" will make you look like you are in some way struggling?

One thing to note though, even the court option takes ages, (over a year for me to get to a hearing!) so you might as well get your ICO complaint in straight away if they refuse to "correct" it.

-

If he is going it alone... might it be worth his(or her) while to send a CPR 31.16 letter and ask for the medical report?

This is asking for disclosure before proceedings commence and might help out costs wise.

http://www.justice.gov.uk/civil/procrules_fin/contents/parts/part31.htm

I think you seriously need proper legal advice though! Check your insurance policies for legal cover pronto as per the

previous post and don't admit anything before getting proper advice.

-

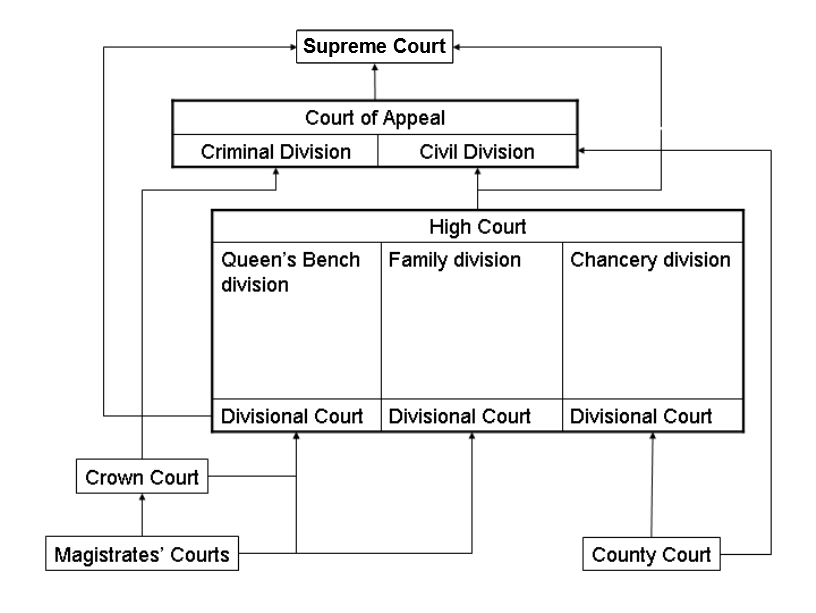

What do you want me to do copy the whole of Carey for you . heres an idea why dont you read it yourself

Are you saying there is anything wrong in your view with this Court of Appeal judgment?

Check this out:

http://upload.wikimedia.org/wikipedia/commons/0/08/English_court_system.png

Waksman is the 3rd rung down.

-

1

1

-

-

The 2nd claim could bring in all sorts of arguments against it so it wouldn't be worth them re-filing.

They'd have to explain why they claimed the previous copy was true when it wasn't etc. Unless they had the original who

would believe them the 2nd time after they told a previous "untruth".

The CCA allows them to be unbinded from providing a wrong copy under s78 doesn't it? Then again we are not just talking

about complying with s78 are we, we have litigation in progress, CPRs etc.

Nobody would re-file and open pandoras box surely?

-

Can I just check what your view on the case above would be, Peter.

Are you of the opinion that (a) the judge is wrong, and that (b) the claimant can simply go back and produce the correct agreement to get judgment in their favour? Despite no leave to appeal?

They would have to re-file a fresh claim.

The previous claim would be dead once judgment was made as they had not complied before judgment.

If they lost once and had to pay costs they might think twice re-filing against someone who wasn't a pushover.

This is what happened here isn't it? Once it was dead it was dead. Even if they complied in the meantime the

previous judgment was based when they hadn't complied.

-

I don't think anyone here is talking about unfair relationships or seeking declarations of unenforceability etc.

If they don't comply properly with the s78 it is a defence and they cannot enforce, as per this case.

You would go for the actual original agreement under CPR 31.14 anyway before even filing a defence. (Maybe get the train to their office and inspect in person too! LOL)

-

Why are we going around in circles?

If you don't satisfy a s78 request properly then you can't enforce. Simple as that.

What reason would the creditor not comply correctly with the s78 in the first place?

(Other than being lazy)

Either they have no idea what the original agreement was (so can't comply with the s78 request) because it is lost or that they know the original agreement was irredemably unenforceable so don't comply (naughty).

Nobody is saying they can't just come up with it eventually then enforce, unless it turns out to be irredemably unenforceable.

The burden of proof is on the claimant to prove it is a true copy.... e.g. How do they know it is a true copy, do they have other agreements on file from that time, etc.

It has been a long time since I seen anyone mention taking the creditor to court on here! Madness.

-

Diddy, I didnt make an actual offer back in October. I was just asking them if they could accept an offer. I asked them that i could clear the balance in instalments within few months but no response!

Ruprecht,thank you for your respond. It sounds allright to me , if i have to pay the balance within 28 days and receive no ccj. However, is there anything i need to do now? Do i have to send in the defence form? Do i need to defend myself?

And lets say i have not defended myself and court ordered me to pay the balance in full (within 28 days to avoid ccj registration), how long that would take in total together with the 28 days period?

Is there anything i should be doing right now?

Many thanks for your responses...

If you do nothing they will almost certainly apply for a "default judgment".

You get 1 month then to pay it when the judgment is issued which is usually within a day or so if they ask for default judgment on moneyclaim.

You then need to get a receipt from the person you paid confirming it was paid within the month and send it with a completed form to the court, with a fee.

This is the leaflet about it:

http://www.hmcourts-service.gov.uk/courtfinder/forms/ex320_0406.pdf

If you admit to it you might get the judgment made earlier, so if you are happy to pay it in 28 days you might be best doing nothing.

Make sure you allow time for it to be cleared funds too just in case i.e. cheque clearance.

-

You might want to read the pre-action protocols for this "stuff" so you know what you are up against.

http://www.justice.gov.uk/civil/procrules_fin/contents/protocols/prot_hou.htm

http://www.justice.gov.uk/civil/procrules_fin/contents/protocols/prot_pic.htm

-

Diddy, thank you very much for your time and effort, i really appreciate it.

Well i can offer £100 now, £100 next month and £50 in April but they havent even returned to my email which i was asking if they could accept an offer.

If i accept the debt and offer a payment, do i still get CCJ registered? I just dont want to get it. I am a student and £250 is a big amount for me and i cant really borrow from anyone as i know it will be very hard to pay them back.

What should i do?

If they get a CCJ against you then you would have to pay it within 28 days in full for it not to appear on your file. Surely you could find some employ that would pay £250 in 4 weeks to clear it?

Other than that you could always submit an embarassed defence and demand to see the agreement.... by time it got to any hearing it would be after April anyway so you could pay them (allegedly) in full anyway, before the hearing.

I can't see anymore costs being awarded on a £250 (small) claim, although your agreement with them might let them charge you more late/arrears fees. They'd would probably have to take you to court again to get them though.

Time would be better spend making some money though LOL!

-

I was slow paying my water bill due to lack of funds and it got as far as a letter dated 7/1/11 coming from the Northampton County Court Bulk Centre giving me 14 days from the date of service to pay said bill before it went to court and a CCJ would be issued. Says on the back of the letter that date of service is 5 days from letter date which means date of service is 12/1/11 and the cutoff point for payment would be 26/1/11. I'm just wondering if the 5 days are inclusive of weekends or not?

As it happens I'm sure I paid the full amount on 25th or 26th as it shows on my bank statement on the 26th. Yesterday we got a mailshot from some company offering to help with our debt due to our CCJ no XXXXXXXXXXX. This confused me and put wind up the wife as I knew I'd paid it! Phoned the water company who checked and agreed that our balance was in fact zero so we were much relieved

Then this morning we both received letters from the Bulk Centre again showing judgements have been made against us for this bill

Then this morning we both received letters from the Bulk Centre again showing judgements have been made against us for this bill  Total amount was £162 but with charges went up to £227(which I paid) and they are now asking for £249! Not sure how to pursue this now as as far as I'm concerned it was paid inside the time and the girl who took the payment said it would be automatically be stopped at the court end by the payment

Total amount was £162 but with charges went up to £227(which I paid) and they are now asking for £249! Not sure how to pursue this now as as far as I'm concerned it was paid inside the time and the girl who took the payment said it would be automatically be stopped at the court end by the payment You need to pay the full amount the judgment was for so that this will not appear on your credit file the next 6 years.

Then you can start complaining to try and get money back off the Water Company.

If you do not pay the full amount of the judgment within 28 days of the judgment your credit file will be

trashed for 6 years.

-

HI

Yes absolutely correct.

So the case here was not subject to judgement because that would be enforcement.

No reason then why the case cant be refiled.

Peter

I don't think there is anything legally stopping them. I get the feeling though that they aren't able to even reconstruct the originally agreement

because they don't know what it was anymore to even keep a straight face and say it was a true copy.

They have had plenty of time to!

-

Is there anything legally clear on what "enforcement" actually is yet under the CCA?

Is obtaining a judgment "enforcement" or enforcing the judgment e.g. sending in the bailiffs, 3rd party debt orders, garnishing wages, etc...

I remember reading one of the cases and the Judge was sort of inferring you'd have to go for injunctory relief to stop "enforcement".

Does that mean technically they can get a judgment against you without complying with a s77/78 request properly but not "enforce" it?

Leaving it up to you to try and get an injunction against them enforcing it if they tried then suddenly have them magically comply with the s77/s78 request.

It is seriously important people fully use CPR 31 the day they get the claim form and go all out to kill the claim before they even have to file a defence. Sadly Joe Public has no clue about this.

-

Hi

I have not seen the full transcript of this case but it seems that the creditor made a major mistake in not correcting the request at the orriginal hearing, if he had there would have been an enforcement

Hopefully PT will confirm this but you cannot sue someone with no cause of action then just create the cause of action in the middle of the claim.

They would have to settle that claim and re-file if they had not complied with the S77/S78 request when they commenced their claim.

It would be a clear abuse of process to commence proceedings when you infact had no cause of action, they would have to discontinue and pay costs to the defendent.

I think this is exactly the outcome of this case in this thread.

Of course this doesn't stop them from complying and re-filing. Which they might even do in this case or just go away back to their kennel tail between legs rather than risk it again with someone who knows the score!

I am pretty sure they cannot just comply with it in the middle of proceedings, confirmation PT?

-

Hi

A creditor can only access your credit file with your permission. A DCA can only look at your file in regards to a debt that you owe.

I would be writing to Equifax demanding the table 1 searches be removed and if you know the details of the DCA who looked, write to them too.

These searches do have an impact when legitimate creditors look at your file when deciding to offer credit or not

I know the searches can be derogatory and I do always get them removed (eventually).

Any credit application has the clause they can use your data to "trace debtors".

So this clause which is included in every single credit application/agreement out there might be what a DCA relies on when they do a search on say "anyone called David Smith born 01/01/75"

So I am thinking the DCA can pretty much legally look at your file if you have the same name and DOB as a debtor they seek based on the fact that when you opened any credit account you agreed that your data could be used to "trace debtors".

It seems too much of a wide power for them to have, especially as there are many William Smith's, etc born on the same day each year.

They need to add another stage when a DCA performs a search, not only do they need a name and DOB but they should be obligated to supply a "connected address" so as to rule out these unwarranted invasions of privacy of individuals with the same name sharing the same date of birth.

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

DCAs Searching Credit Files - What are their Rights?

in Credit Reference Agencies

Posted · Edited by Ruprecht

extra info

They probably do a Table 1 search to see if you are worth chasing (to see your current credit situation) ......

Then pretend it was an error....

Can the DCA do a proper credit check legally I wonder? If the account is active the creditor can check you as much as they like I believe, but once it is deado I wonder if they can continue doing that seeing as no more credit is on offer?

Edit:

I am talking about a proper credit check BTW not just debtor tracing etc.