Showing results for tags 'llp'.

-

Hi, I'm wondering if someone can help me, as I've received a claim from these also for a loan of £2000 from 2006. I'm 100% certain I was mis-sold the PPI as I sent the forms off with that part unticked, which they RETURNED advising I must tick the box for it in order to complete the loan. I only heard from this IND Ltd in the middle of last month for the first time, I hadn't heard from Welcome for nearly 3 years prior to this at all! I just need to know what to do as I'm certain that the majority of the sum (nearly 3,000-odd at least) is made of interest and charges due to the PPI (I likely would have settled the original loan had the PPI not been bolted on to it!). I actually rang the FSCS number this morning to look into making a claim against Welcome for the PPI, when a woman advised me that I should contact the broker who initiated the loan - they are UCC Plc (Unsecured Credit Company Plc) - which has been in liquidation since May 2010 according to Companies House; also the number given of 0870 7773277 is no longer in service. At work at moment, so if needs be will post docs later - can anyone advise in interim what to do?

-

Hi all I received a claim form dated 20th Mar 2015 in the County Court Business Centre Northampton. The claimant Cabot and Solicitor Weightmans LLP for a Capital One Credit Card defaulted on. On the 30th March online with MCOL I filed an acknowledgement of service that I intend to defend all of this claim. With work, family and illness it has now I believe gone past the 28 days to file a defence. Is it too late to file a defence now? Having had chance to read this forum is it too late to send off the CCA and the CPR31.14 now? I really do need some advice quickly. If anybody can help it would be appreciated Thanks

Hi all I received a claim form dated 20th Mar 2015 in the County Court Business Centre Northampton. The claimant Cabot and Solicitor Weightmans LLP for a Capital One Credit Card defaulted on. On the 30th March online with MCOL I filed an acknowledgement of service that I intend to defend all of this claim. With work, family and illness it has now I believe gone past the 28 days to file a defence. Is it too late to file a defence now? Having had chance to read this forum is it too late to send off the CCA and the CPR31.14 now? I really do need some advice quickly. If anybody can help it would be appreciated Thanks -

Hi all, Hopefully someone can give a bit advice, unfortunately due to a mistake on my part i have ended up in arrears with a finance agreement through Thinksmart for a computer obtained at PCWorld. Shoosmiths who suggest that they are solicitors acting on behalf of Thinksmart although i believe they are connected have been in touch and i have communicated back via email. The debt is not huge at all but at this time of the year it can be difficult to pay back in on go. I will post the email conversation below in the hope that someone could advise how best to respond to their final email: Me to Shoosmiths: Dear Shoosmiths, With reference to the agreement number: ****** and your Ref:********* I received a letter from you stating that i am in breach of agreement and in arrears by £162.45. On checking with my bank i can see that the direct debit has indeed not been paid, i will be contacting the bank in the interim to ascertain why this has happened. I appreciate that i should have looked at correspondence from Rentsmart and that has been an error on my part thinking that it was marketing material. In order to move forward with this and with consideration that the agreement is due to end soon anyway I can offer the following as a payment plan: Friday 22nd December £60 Friday 26th January 2018 £100 Tuesday 27th February £100 This should ensure that any arrears and any due payments are finally covered. Please can i request any communication be via this email address. I look forward to your reply. Shoosmiths reply (prior to this was request to confirm address): Dear ........, Thank you for your prompt response. I must inform you that you have a further instalment falling due on 15 December 2017 in the sum of £34.15. This will increase your arrears to £196.60. My client have instructed me to terminate your account on 19 December 2017 if your arrears have not been cleared in full. I can see your proposal below shows your first payment proposed to be paid on 22 December, my client would be looking for a token payment before then to show a goodwill gesture if they were to agree not to terminate your account. I would also need a reason as to why you are not in a position to clear your arrears in full before 19 December 2017 so that I can validate the hold on termination. I look forward to receiving your response. I have formally agreed to hold your termination, I must inform you that your account is at risk of being terminated on 19 December 2017. Kind regards I'm not really in a position to make an additional payment now and my original offer was looking to include any upcoming payments, i also believe the agreement is due to end soon anyway which i need to check on, any thoughts welcome.

Hi all, Hopefully someone can give a bit advice, unfortunately due to a mistake on my part i have ended up in arrears with a finance agreement through Thinksmart for a computer obtained at PCWorld. Shoosmiths who suggest that they are solicitors acting on behalf of Thinksmart although i believe they are connected have been in touch and i have communicated back via email. The debt is not huge at all but at this time of the year it can be difficult to pay back in on go. I will post the email conversation below in the hope that someone could advise how best to respond to their final email: Me to Shoosmiths: Dear Shoosmiths, With reference to the agreement number: ****** and your Ref:********* I received a letter from you stating that i am in breach of agreement and in arrears by £162.45. On checking with my bank i can see that the direct debit has indeed not been paid, i will be contacting the bank in the interim to ascertain why this has happened. I appreciate that i should have looked at correspondence from Rentsmart and that has been an error on my part thinking that it was marketing material. In order to move forward with this and with consideration that the agreement is due to end soon anyway I can offer the following as a payment plan: Friday 22nd December £60 Friday 26th January 2018 £100 Tuesday 27th February £100 This should ensure that any arrears and any due payments are finally covered. Please can i request any communication be via this email address. I look forward to your reply. Shoosmiths reply (prior to this was request to confirm address): Dear ........, Thank you for your prompt response. I must inform you that you have a further instalment falling due on 15 December 2017 in the sum of £34.15. This will increase your arrears to £196.60. My client have instructed me to terminate your account on 19 December 2017 if your arrears have not been cleared in full. I can see your proposal below shows your first payment proposed to be paid on 22 December, my client would be looking for a token payment before then to show a goodwill gesture if they were to agree not to terminate your account. I would also need a reason as to why you are not in a position to clear your arrears in full before 19 December 2017 so that I can validate the hold on termination. I look forward to receiving your response. I have formally agreed to hold your termination, I must inform you that your account is at risk of being terminated on 19 December 2017. Kind regards I'm not really in a position to make an additional payment now and my original offer was looking to include any upcoming payments, i also believe the agreement is due to end soon anyway which i need to check on, any thoughts welcome. -

Hi guys, been dealing with Capquest via Shoosmith. Sent CCA requests to Capquest via Shoosmiths as you can see. Even though they said no further legal action would be taken I went to court to day regardless after sitting like an edjit for several hours I went an spoke to a clerk. Turns out Shoosmith changed the hearing dates on the 20th January to 29th April and I've never been informed! At the current time I have yet to receive any documentation in regards to the CCA request yet my request has been acknowledged. Why has Capquest added £186 onto this account since last month? Why is Shoosmiths still taking me to court even though they said no further action will be taken while Capquest is "investigating"? Sorry this is meant to be the 25th not 29th.... And dont know whats going on with post images, was having bother adding them.

Hi guys, been dealing with Capquest via Shoosmith. Sent CCA requests to Capquest via Shoosmiths as you can see. Even though they said no further legal action would be taken I went to court to day regardless after sitting like an edjit for several hours I went an spoke to a clerk. Turns out Shoosmith changed the hearing dates on the 20th January to 29th April and I've never been informed! At the current time I have yet to receive any documentation in regards to the CCA request yet my request has been acknowledged. Why has Capquest added £186 onto this account since last month? Why is Shoosmiths still taking me to court even though they said no further action will be taken while Capquest is "investigating"? Sorry this is meant to be the 25th not 29th.... And dont know whats going on with post images, was having bother adding them. -

Hi All, New to this forum, i have an issue with which i need help. I've tried to convey the situation as best as possible below, please let me know if more detail is required. I was in a debt management plan some years ago which had some unpaid loans. The Debt management company referred their inhouse partner (Priestly crowe) to check for PPI. Being a bit young & dumb i agreed to this and the charges. As the loans were still outstanding, the PPI which was 'claimed' was taken from the debt instead of being paid in a cash sum. I instead owe the money to Priestly Crowe. They were paid on a monthly basis the fee which i owed. Last year (October 2016) my debt management company ceased trading, i dealt with all debtors myself. I sold some belongings to have enough cash to pay everyone what was owed. However i could not get hold of Priestly Crowe. Their contact details had changed and i did not have the new correct ones. Fast forward to about February this year and i received a call from them. I asked them to send our paperwork for money owed so we could get a payment plan sorted. No post or no news. The same happened in April. On Saturday i received post from the CCBC Northampton about a CCJ that had been instructed by Priestly Crowe. I have subsequently settled the payment as i did not want any financial implications to affect my current credit score & status. Seeing how long the CCBC take to do anything, i knew i was on a short time scale to get this processed. I have questions about the process & where i stand: 1) I was told the claim pack had been sent from the court, but i have not received it. They cannot provide me with proof - only that their system shows it was sent on the 12th August. - Do i have any leg to stand to make a claim from Royal Mail? I have lost 3 weeks of time to defend my case & check the facts were all correct - debt & amount owed. Plus to now defer the case would have cost a further £255 for which i would not have been able to claim back, if i was defended correctly. 2) Priestly Crowe LLP - Regulated by the FCA. Should they/did they need to contact me prior to taking this action? Are they obliged to show the court any proof they have attempted to contact me/show i've refused payment prior to getting a CCJ? Or is simply their 'word' enough to get this processed? 3) I have asked for my history/paperwork from Priestly Crowe to check the contract, payments & the amount owed is correct. If it isn't, am i able to process a counter claim for this amount? Small claim court, CCJ . . . etc I hope i have covered all bases here and given enough information. If not, please ask away and i will reply where i can. Thanks in advance, J

-

Hello, Can you tell me how can i register as a sole trader while in the same time I'm a LTD company director and a LLP member? It seems to be a problem through the HM R&C online service or I just can't find the answer... Looking forward for all your help

Hello, Can you tell me how can i register as a sole trader while in the same time I'm a LTD company director and a LLP member? It seems to be a problem through the HM R&C online service or I just can't find the answer... Looking forward for all your help -

Name of the Claimant ? Hoist Portfolio Holding 2 LTD Date of issue 02/11/2016 Date to acknowledge =20/11/2016 Date to submit defence = 4pm Friday 02/12/2016 POC 1.This claim is for the sum of £4900 in respect of monies owing under an Agreement with the account number xxxxx pursuant to The Consumer Credit Act 1974 (CCA) The debt was legally assigned by MKDP LLP (Ex HSBC) to the Claimant and notice has been served 2.The Defendant has failed to make contractual payments under the terms of the Agreement. A default notice has been served upon the defendant pursuant to s.87(1) CCA. 3.The Claimant claims 1.The sum of £4900 2.Interests pursuant to s69 of the County Court Act 1984 at a rate of 8.00percent from the 2/11/10 to the date hereof 2188 days is the sum of £2300 3.Future interest of accruing at the daily rate of £1 4.costs What is the value of the claim?£7800 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? Pre 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? could no longer afford to maintain What was the date of your last payment? 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes In 2012 I requested my CCA, they returned to me only generic docs, with no signed application or agreement form. I will send off tomorrow for CCA and CPA? Thanks

Name of the Claimant ? Hoist Portfolio Holding 2 LTD Date of issue 02/11/2016 Date to acknowledge =20/11/2016 Date to submit defence = 4pm Friday 02/12/2016 POC 1.This claim is for the sum of £4900 in respect of monies owing under an Agreement with the account number xxxxx pursuant to The Consumer Credit Act 1974 (CCA) The debt was legally assigned by MKDP LLP (Ex HSBC) to the Claimant and notice has been served 2.The Defendant has failed to make contractual payments under the terms of the Agreement. A default notice has been served upon the defendant pursuant to s.87(1) CCA. 3.The Claimant claims 1.The sum of £4900 2.Interests pursuant to s69 of the County Court Act 1984 at a rate of 8.00percent from the 2/11/10 to the date hereof 2188 days is the sum of £2300 3.Future interest of accruing at the daily rate of £1 4.costs What is the value of the claim?£7800 Is the claim for a current account (Overdraft) or credit/loan account or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? Pre 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Yes Did you receive a Default Notice from the original creditor? Yes Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? could no longer afford to maintain What was the date of your last payment? 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Yes In 2012 I requested my CCA, they returned to me only generic docs, with no signed application or agreement form. I will send off tomorrow for CCA and CPA? Thanks -

Hi, Could you help me with a Northampton county court claim dated 13 sep 2016 which is for £935.50 + interest. I have acknowledged it online and the issue date is 13 Sep 2016. Claim History A claim was issued against you on 13/09/2016 Your acknowledgment of service was submitted on 22/09/2016 at 20:20:43 Your acknowledgment of service was received on 23/09/2016 at 08:01:36 I want to dispute the whole claim which I have told the court online as im not sure about this credit card or when it was taken out as at that time I had so many debt but im not sure which one this is. Which forms do I need to send off to the claimant and the solicitors. CCA and 31:14? Any help will be appreciated.

Hi, Could you help me with a Northampton county court claim dated 13 sep 2016 which is for £935.50 + interest. I have acknowledged it online and the issue date is 13 Sep 2016. Claim History A claim was issued against you on 13/09/2016 Your acknowledgment of service was submitted on 22/09/2016 at 20:20:43 Your acknowledgment of service was received on 23/09/2016 at 08:01:36 I want to dispute the whole claim which I have told the court online as im not sure about this credit card or when it was taken out as at that time I had so many debt but im not sure which one this is. Which forms do I need to send off to the claimant and the solicitors. CCA and 31:14? Any help will be appreciated. -

Here's my summarised situation. I'd like any advice on how I should proceed now. Took out a Credit Card with MBNA in 1999 Through their unscrupulous lending, my own stupidity & intermittent mental health issues, I ran up a debt that I couldn't pay off I started to have problems meeting my minimum monthly payments in 2010, and requested a temporary interest freeze when it got really bad (thought this was 2011, but now realise it was probably 2012... further explanation below) to help me to sort our my finances. This request was ignored. After several months I stopped paying anything and prioritised other debts. Eventually defaulted in 2012 I started to get harrassed by Aktiv Kapital Over time have now been chased by PRA, another couple of agents and back to PRA At one stage, not sure when but probably 2012/13 I requested proof of the debt being owed to Aktiv Kapital/PRA?, and didn't receive that proof. At the time I downloaded a template letter to send, but not sure where from, but it included the sentence about not admitting to the debt. Due to not receiving the proof requested I didn't enter into any communication with any of these companies again. PRA continued to harrass me. I wouldn't hear from them for months and would then be bombarded with telephone calls as well as letters. I didn't answer the phone to them or respond to their letters. Over time they have offered a discount on the debt several times In June 2016 they advised by letter that they were considering passing the case to their Scottish Solicitors I received a letter from Brodies LLP in July 2016 stating they had been instructed by PRA to pursue recovery of the debt and threatening court proceedings. I panicked! I was convinced at the time that it had actually been in 2011 that I had last communicated with the original lender and sent a Statute Barred letter. I heard nothing back and when a couple of months passed with no communication I thought I had heard the last from them. On Saturday I received a letter from Brodies again (6 months later) which included a copy of my original Credit Agreement and copies of the final few months of statements of my account with MBNA showing I made a payment in August 2012. This letter states that "To avoid this matter being passed to our Court Action Team, you are required to pay the Debt or contact us to discuss a suitable payment arrangement not later than 2 February 2017" The amount of the debt being chased is £5781.16 Are they allowed to only give 4 working days for me to contact them? Are they allowed to come back to me after 6 months of no communication? Am I entitled to request proof of ownership of the debt by PRA? Should I contact them tomorrow? I am not in a position to pay this amount. Part of me says, I borrowed the money and should accept that it eventually needs to be paid. However, if there are any loopholes I can use to my advantage then I'd like to try to use them, as for the first time in 20 years I have all my other debts under control and can't believe this has come back to haunt me. I've tried to read as much as possible on other threads, but got really confused by some of the terminology being used, so apologies if I should have been able to find my answers elsewhere.

Here's my summarised situation. I'd like any advice on how I should proceed now. Took out a Credit Card with MBNA in 1999 Through their unscrupulous lending, my own stupidity & intermittent mental health issues, I ran up a debt that I couldn't pay off I started to have problems meeting my minimum monthly payments in 2010, and requested a temporary interest freeze when it got really bad (thought this was 2011, but now realise it was probably 2012... further explanation below) to help me to sort our my finances. This request was ignored. After several months I stopped paying anything and prioritised other debts. Eventually defaulted in 2012 I started to get harrassed by Aktiv Kapital Over time have now been chased by PRA, another couple of agents and back to PRA At one stage, not sure when but probably 2012/13 I requested proof of the debt being owed to Aktiv Kapital/PRA?, and didn't receive that proof. At the time I downloaded a template letter to send, but not sure where from, but it included the sentence about not admitting to the debt. Due to not receiving the proof requested I didn't enter into any communication with any of these companies again. PRA continued to harrass me. I wouldn't hear from them for months and would then be bombarded with telephone calls as well as letters. I didn't answer the phone to them or respond to their letters. Over time they have offered a discount on the debt several times In June 2016 they advised by letter that they were considering passing the case to their Scottish Solicitors I received a letter from Brodies LLP in July 2016 stating they had been instructed by PRA to pursue recovery of the debt and threatening court proceedings. I panicked! I was convinced at the time that it had actually been in 2011 that I had last communicated with the original lender and sent a Statute Barred letter. I heard nothing back and when a couple of months passed with no communication I thought I had heard the last from them. On Saturday I received a letter from Brodies again (6 months later) which included a copy of my original Credit Agreement and copies of the final few months of statements of my account with MBNA showing I made a payment in August 2012. This letter states that "To avoid this matter being passed to our Court Action Team, you are required to pay the Debt or contact us to discuss a suitable payment arrangement not later than 2 February 2017" The amount of the debt being chased is £5781.16 Are they allowed to only give 4 working days for me to contact them? Are they allowed to come back to me after 6 months of no communication? Am I entitled to request proof of ownership of the debt by PRA? Should I contact them tomorrow? I am not in a position to pay this amount. Part of me says, I borrowed the money and should accept that it eventually needs to be paid. However, if there are any loopholes I can use to my advantage then I'd like to try to use them, as for the first time in 20 years I have all my other debts under control and can't believe this has come back to haunt me. I've tried to read as much as possible on other threads, but got really confused by some of the terminology being used, so apologies if I should have been able to find my answers elsewhere. -

I have received a claim form from Northampton CCBC as per below on Friday. I'm unsure what to do with this, the form states If you agree and are asking for time to pay then send this direct to the claimant and not the court as this may result in a judgement against you, does this mean if I make a deal with MKDP LLP then I will not get a CCJ? It's a long story of how I ended up with this debt but the short version is that in Jan 2008 I was out of work for 3 months, my overdraft facility was £1000 which was maxed. .. I had secured a new job but needed another £500 to see me through until the first payday, they refused of course.. . I moved bank accounts and didn't pay off the £1000 owing due to servicing other priority debts. I'm almost there out of my debt mountain, I have paid off everything other than the car which finishes in June and was hoping to buy a house in 12-18 months time but getting a CCJ now will end up with me getting a high rate if anything at all making it unaffordable. I think this may be more than 6 years old but have no way of proving this.. . the bank may have kept the account running for a good while as the £700 of charges must have taken a while to accrue. Do I contact them and try to make a deal? In all honesty it galls me that they have probably bought the debt for buttons and I'd like very much for them not to get a sausage, call me niave but if it was Lloyds themselves I'd offer to pay them back the grand (in bits) that I do indeed owe them but not this lot. I have seen a number of wins against them on various threads but don't know where to begin? Can anyone please help? Claimant MKDP LLP FLEMING HOUSE SEEBECK PLACE KNOWLHILL MILTON KEYNES MK5 8FR Defendant my name spelt incorrectly (does that matter?) Correct Address Particulars of claim The claimant claims the sum of 1,722.94 being monies due from the Defendant(s) to Lloyds Bank PLC under a bank account facility regulated by the Consumer Credit Act 1974 and assigned to the Claimant on 20/06/2014. The defendant(s) account number was (14 digit number... seems too long to be correct?). It was a term of the bank account that any debit balance would be repayable in full on demand. The Defendant(s) has failed to make payment as required by the demand for payment sent by Lloyds Bank PLC. The Claimant claims the sum of 1722.94 and costs. The Claimant has complied, and as far as is necessary, with the Pre-Action Conduct Practice Direction. Sorry I forgot to add that I opened the account in 1998.

-

hiya all. just got a letter from PRA group about a debt i have of roughly 2 grand. they are saying they are going to get brodies LLP scottish solicitors on to me (im in glasgow, scotland) im wondering what powers these people have - i.e. do they have any right to come to my house and seize goods? under scots law. im sure only sheriffs officers have the right to come on to my property under scots law. i know that simple debt collectors are trespassing by coming to my house just not sure where i stand with a local solicitor. thanks for any reply's! i will re - phrase that - who has the right to come on to my property? in scotland.

-

Hi Received a statement from MKDP today for a statute Barred Debt. In June last year before the statue I sent a S77/78 request along with the £1.00 Postal Order clearly stating it was for the Fee incurred and not to be used for anything else. I didnt receive anything from my request. On their statement its gone down as payment received!!! The Debt was statute from Feb 2015 I thought this wasnt allowed??? Hadituptohere

Hi Received a statement from MKDP today for a statute Barred Debt. In June last year before the statue I sent a S77/78 request along with the £1.00 Postal Order clearly stating it was for the Fee incurred and not to be used for anything else. I didnt receive anything from my request. On their statement its gone down as payment received!!! The Debt was statute from Feb 2015 I thought this wasnt allowed??? Hadituptohere -

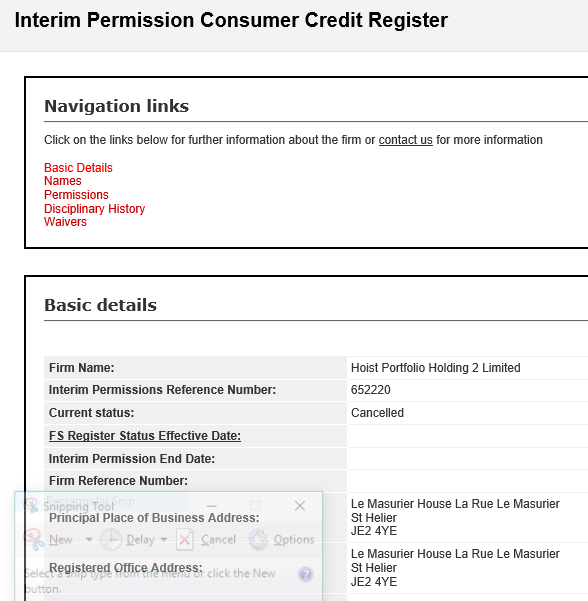

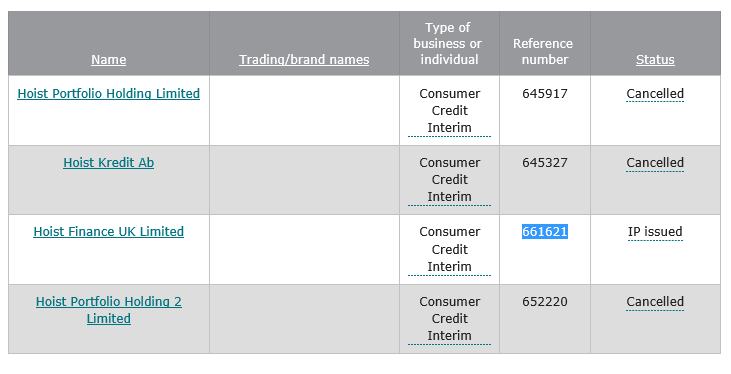

Upon checking the new FCA Public Register which is listing "Interim Permissions" in its transitional role from the OFT, I find that Hoist wildcard returns 4 results : Hoist Portfolio Holding Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Portfolio Holding 2 Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Kredit Ab (Presumably Swedish Parent Company) - IP CANCELLED Hoist Finance UK Limited - Reference Number 661621 - IP ISSUED Having received a letter from Robinson Way (As we know now owned by Hoist Finance UK Limited) they state that they have purchased an account from MKDP LLP (Compello - Hoist Director is director of Compello also). They state quite clearly and unambiguously that the alleged new beneficial owner of the account is Hoist Portfolio 2 Limited, who clearly are not registered nor authorised to engage in CC activity, and as such cannot legally instruct their associate company Robinson Way to attempt any form of recovery on their behalf. This latest threat to the consumer has all the hallmarks and modus operandi of the last bunch of cowboys who fought their corner for so long and then voluntarily surrendered their licences. I'm not mentioning names, but everyone knows whom I'm referring to. This is now the same old story, one director pulling the strings with an absolute labyrinth of companies who are nothing more than a file on a shelf and a brass plate on an accountants door, representing the fiddles of the strings. I'm making it my business to enquire with the FCA as to the status of Hoist Portfolio 2 Holding Limited just to see and hear from them directly their legal status. They would probably just BS consumers and say "oh well we're all part of the same group" blah blah blah - now where have I heard that before - sounds familiar. Would appreciate all your comments on this matter. Ive been in Court before with people as a MacKenzie Friend against the last mob who tried to collect accounts whilst unauthorised and tried to wriggle with intertwined companies. The Judge generally sees right through it.

Upon checking the new FCA Public Register which is listing "Interim Permissions" in its transitional role from the OFT, I find that Hoist wildcard returns 4 results : Hoist Portfolio Holding Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Portfolio Holding 2 Limited (Registered in Jersey C.I.) - IP CANCELLED Hoist Kredit Ab (Presumably Swedish Parent Company) - IP CANCELLED Hoist Finance UK Limited - Reference Number 661621 - IP ISSUED Having received a letter from Robinson Way (As we know now owned by Hoist Finance UK Limited) they state that they have purchased an account from MKDP LLP (Compello - Hoist Director is director of Compello also). They state quite clearly and unambiguously that the alleged new beneficial owner of the account is Hoist Portfolio 2 Limited, who clearly are not registered nor authorised to engage in CC activity, and as such cannot legally instruct their associate company Robinson Way to attempt any form of recovery on their behalf. This latest threat to the consumer has all the hallmarks and modus operandi of the last bunch of cowboys who fought their corner for so long and then voluntarily surrendered their licences. I'm not mentioning names, but everyone knows whom I'm referring to. This is now the same old story, one director pulling the strings with an absolute labyrinth of companies who are nothing more than a file on a shelf and a brass plate on an accountants door, representing the fiddles of the strings. I'm making it my business to enquire with the FCA as to the status of Hoist Portfolio 2 Holding Limited just to see and hear from them directly their legal status. They would probably just BS consumers and say "oh well we're all part of the same group" blah blah blah - now where have I heard that before - sounds familiar. Would appreciate all your comments on this matter. Ive been in Court before with people as a MacKenzie Friend against the last mob who tried to collect accounts whilst unauthorised and tried to wriggle with intertwined companies. The Judge generally sees right through it.

-

Hi all In October 2009 I defaulted on an HSBC overdraft, £700 of which was charges, the other £700 ish the actual overdraft. They didn't get in touch until last year (I had previously looked in to a DRO but HSBC wouldnt confirm the details to me as it had been passed to a DCA, my circumstances then changed and I was able to negotiate the other debts I had at the time) The account was originally opened in 2005. I sent MKDP LLP a CCA request, they took a long time to respond and finally responded saying that the account was opened 'interpersonally' (whatever that means) and therefore no agreement was necessary? I've read elsewhere on the forum that pre-April 2007 CCA agreements are required or the debt is unenforcable, can anyone confirm? I now can't afford to pay this debt having exhausted my options previously; I'm begrudged to play ball with them / HSBC when there are so many charges on there and this could have been resolved years ago if they had given me the info I needed for a DRO!

-

Hey there, I have been an avid reader of these forums for some time but never had anything of relevance to contribute until now. I have received a CC from the Northampton CCBC and below is the current status. Received a claim? Yes Issue Date: 21-5-2015 Amount approx: £528.59 Claimant: Cabot Financial UK Limited Solicitor: Weightmans LLP Original Credit: Vanquis Particulars of Claim: 1. The Defendant entered into a credit agreement described bt the original creditor as VANQUIS-CREDIT CARD and having account number XXXXXX ('The Account') 2. The Claimant, a UK limited company with company number 3757424, is the assignee and legal owner of all rights previously enjoyed by the original creditor in respect of the Account. 3. The Defendant is indebted to the Claimant in respect of the account in the sum of £528.59 4. The Claimant claims the said sum of £528.59, plus costs. Stat Barred? No I have done the following and provided a timeline as I know I am time limited by the court procedure. Time line 25/05/2015 - Received CC from Northampton CC Business Centre 25/05/2015 - Logged on to MCOL and acknowledged and disputed the claim 29/05/2015 - Wrote and sent a CCA request to Cabot requesting a copy of the original credit agreement. 01/06/2015 - Wrote and sent a CPR 31.14 request to Weightmans LLP requesting a copy of all documents they have regarding this case. 03/06/2015 - Received letter from Cabot Financial stating that they do not have the documents on file and will take approximately 40 days. 05/06/2015 - Received letter from Weightmans LLP stating they have requested the documents. So in summary; sent: Acknowledged the Claim, Sent a CCA request, Sent a CPR 31.14 request Other info: I don't have any knowledge that I can recall ever taking out a credit card with Vanquis. However I have checked my credit file. According to the records, it was started on 08/05/2007 and they are on there as a default since 31/03/2010I have attached all copies of documents I currently have. Any advice, hints tips etc... would be very much appreciated. [ATTACH=CONFIG]57941[/ATTACH][ATTACH=CONFIG]57940[/ATTACH]

Hey there, I have been an avid reader of these forums for some time but never had anything of relevance to contribute until now. I have received a CC from the Northampton CCBC and below is the current status. Received a claim? Yes Issue Date: 21-5-2015 Amount approx: £528.59 Claimant: Cabot Financial UK Limited Solicitor: Weightmans LLP Original Credit: Vanquis Particulars of Claim: 1. The Defendant entered into a credit agreement described bt the original creditor as VANQUIS-CREDIT CARD and having account number XXXXXX ('The Account') 2. The Claimant, a UK limited company with company number 3757424, is the assignee and legal owner of all rights previously enjoyed by the original creditor in respect of the Account. 3. The Defendant is indebted to the Claimant in respect of the account in the sum of £528.59 4. The Claimant claims the said sum of £528.59, plus costs. Stat Barred? No I have done the following and provided a timeline as I know I am time limited by the court procedure. Time line 25/05/2015 - Received CC from Northampton CC Business Centre 25/05/2015 - Logged on to MCOL and acknowledged and disputed the claim 29/05/2015 - Wrote and sent a CCA request to Cabot requesting a copy of the original credit agreement. 01/06/2015 - Wrote and sent a CPR 31.14 request to Weightmans LLP requesting a copy of all documents they have regarding this case. 03/06/2015 - Received letter from Cabot Financial stating that they do not have the documents on file and will take approximately 40 days. 05/06/2015 - Received letter from Weightmans LLP stating they have requested the documents. So in summary; sent: Acknowledged the Claim, Sent a CCA request, Sent a CPR 31.14 request Other info: I don't have any knowledge that I can recall ever taking out a credit card with Vanquis. However I have checked my credit file. According to the records, it was started on 08/05/2007 and they are on there as a default since 31/03/2010I have attached all copies of documents I currently have. Any advice, hints tips etc... would be very much appreciated. [ATTACH=CONFIG]57941[/ATTACH][ATTACH=CONFIG]57940[/ATTACH] -

Hello everyone sorry to bother you all I've been searching online and have come across this amazing site and fingers crossed I'm hoping someone will be able to help and advise me on how to proceed with a CCJ that I've just had put onto my credit file. The debt is for £3300 and states the judgement date was 26th January 2015 but was only added to my credit file yesterday. This debt is for a very old HSBC bank account debt that went into default on the 5th November 2009 for £3145 and now looks like MKDP LLP have purchased the debt I've heard nothing from them at all and moved into my new house in july 2014. so would not have received any court papers. I'm just looking for some legal advice on what id need to do to get this sorted it was due to come off in November this year so they got in before the 6 years and i can't afford to have this on my file as I've been trying so hard to sort my life out and it seems everything is now coming back to bite me I have also noticed a new company have applied a default to my credit file called MYJAR for £692 it looks like its for a old payday loan from txt loan from 2012-2013 again in my old address but i defaulted 2-3 years ago and its only just been put on my credit file and the default date is missing is this allowed as its showing on my file as if I've only just started missing payments ? Any help would be amazing and id be very grateful

Hello everyone sorry to bother you all I've been searching online and have come across this amazing site and fingers crossed I'm hoping someone will be able to help and advise me on how to proceed with a CCJ that I've just had put onto my credit file. The debt is for £3300 and states the judgement date was 26th January 2015 but was only added to my credit file yesterday. This debt is for a very old HSBC bank account debt that went into default on the 5th November 2009 for £3145 and now looks like MKDP LLP have purchased the debt I've heard nothing from them at all and moved into my new house in july 2014. so would not have received any court papers. I'm just looking for some legal advice on what id need to do to get this sorted it was due to come off in November this year so they got in before the 6 years and i can't afford to have this on my file as I've been trying so hard to sort my life out and it seems everything is now coming back to bite me I have also noticed a new company have applied a default to my credit file called MYJAR for £692 it looks like its for a old payday loan from txt loan from 2012-2013 again in my old address but i defaulted 2-3 years ago and its only just been put on my credit file and the default date is missing is this allowed as its showing on my file as if I've only just started missing payments ? Any help would be amazing and id be very grateful -

Desperate for help on this one, I have received a county court claim from MKDP it claims I owe them money and have broken an agreement with Barclaycard. claiming default notice served pursuant to consumer credit act 1974 The issue date was the 14th August 2014, received it on the Wednesday 20th August2014. What options do I have? I do not believe that the original documents can be produced from 2000-2001 on the account. What I believe they are trying to do is serve this as a sneaky back door to get a CCJ for the debt. Tigs.. Should of popped more info on, the debt is for 11406.91 including court costs

Desperate for help on this one, I have received a county court claim from MKDP it claims I owe them money and have broken an agreement with Barclaycard. claiming default notice served pursuant to consumer credit act 1974 The issue date was the 14th August 2014, received it on the Wednesday 20th August2014. What options do I have? I do not believe that the original documents can be produced from 2000-2001 on the account. What I believe they are trying to do is serve this as a sneaky back door to get a CCJ for the debt. Tigs.. Should of popped more info on, the debt is for 11406.91 including court costs -

Evening Folks, Apologies if this is in the wrong section, if it is could the mods kindly move it. I have arrived home today with my wife to find that my wife has kindly received in the post a CCJ obtained by Lowell(Claimant)/Bryan Carter Solicitors on 16/09/2015. Now this has come as a bit of a shock as we have received no prior correspondence from them regarding this debt or anything to state there would be any date to appear in court to deal with this. The judgment has also been obtained in my wife's maiden name, despite us being married for 3 years. I would greatly appreciate any help to urgently deal with this. Many Thanks G__M

-

Hello, I received a claim form from MKDP LLP dated 10.12.14. I have responded online intending to contest the claim. Just to give a little background of the debt as far as I recollect. I was having a temporary financial problem around 2010 and missed a payment or two. I later called barclays to make some payment. They asked if they should set up a direct debit on the account I paid for and I said no. I told them I will always make a telephone payment until my situation changes. A month later, I wanted to use the card and was told the little money I believe was in the account was gone. I found out that a company by the name Mercers had taken money off my account. I investigated this and found out that it was a company that assist Barclaycard to collect their debt. I called barclaycard and told them that my right has been violated as my account details should not have been passed to a third party which went ahead to take money out of my account without my permission. I sought compensation but they refused. I told them I would not make further payment until the issue is resolved. There were a couple of back and forth telephone conversations and I stopped hearing from them until I got this claim form from MKD LLP. I am at the moment a full time masters student at the university and have no income at the moment. I called MKDP LLP and offered to pay £1000 as a final settlement. I told them I intend to get the money the only credit card I have which has a limit of just over £1000. They refused and demanded a settlement of £1600 instead. I told them that apart from the fact that barclaycard violated my right, I do not believe I was owing that much. I have not made a formal defence and don't know how to go about it. The whole issue is overwhelming as I have exams coming up at the end of the month with loads of assignments before then. Any advice will help

-

I've just received a summary cause summons from Arrow for the sum of £4324.32 for a credit card debt I owe. This debt is not SB and won't be for a while. The summons is legit and I have to answer it. My question is this: If I took PPI out with the credit card, can I make a counterclaim, stating that the amount the pursuer is claiming is incorrect because of owed PPI and interest? If I did, any opinions/advice on how this might go? Or should I just bite the bullet and make an application for a pay over time? Thanks for any advice about this. I'm considering going for a midnight swim in the Atlantic.

I've just received a summary cause summons from Arrow for the sum of £4324.32 for a credit card debt I owe. This debt is not SB and won't be for a while. The summons is legit and I have to answer it. My question is this: If I took PPI out with the credit card, can I make a counterclaim, stating that the amount the pursuer is claiming is incorrect because of owed PPI and interest? If I did, any opinions/advice on how this might go? Or should I just bite the bullet and make an application for a pay over time? Thanks for any advice about this. I'm considering going for a midnight swim in the Atlantic. -

Hi there, New posting here. Firstly, I hope I'm in the right place for this and if not would someone please let me know? I am discussing this on behalf of my wife who has today received a court summons for a debt accrued under Vanquis Bank, now owned by Cabot Financial and they are suing via Weightmanns LLP, Liverpool. The total value of the debt (which includes their costs is just over £2900.00). Now, I recall my wife having some difficulty with Vanquis re a charge they administered to the account and there was some fallout, I don't know the exact facts and she's in such a state I can't find out. The long and short is, can anyone help / assist with this.... I know if there is a debt and it has been paid within 6 years then they have every right to go ahead and take you to court. I suppose what I am asking is there any way that we can prove they have not followed procedures, I know that she hasn't received mail from Weightmanns but has from Cabot but filed it suitably! If anyone can help we'd appreciate it. Cheers, C

Hi there, New posting here. Firstly, I hope I'm in the right place for this and if not would someone please let me know? I am discussing this on behalf of my wife who has today received a court summons for a debt accrued under Vanquis Bank, now owned by Cabot Financial and they are suing via Weightmanns LLP, Liverpool. The total value of the debt (which includes their costs is just over £2900.00). Now, I recall my wife having some difficulty with Vanquis re a charge they administered to the account and there was some fallout, I don't know the exact facts and she's in such a state I can't find out. The long and short is, can anyone help / assist with this.... I know if there is a debt and it has been paid within 6 years then they have every right to go ahead and take you to court. I suppose what I am asking is there any way that we can prove they have not followed procedures, I know that she hasn't received mail from Weightmanns but has from Cabot but filed it suitably! If anyone can help we'd appreciate it. Cheers, C -

Hi, I have just found a website for the above company which looks interesting, does anyone know anything about this company please e.g. what is their reputation like and do you know anyone who has had any dealings with them? Thank you Maybe

-

Hi, I hope that you can help me - I have read down a number of the DVLA LLP threads, but wanted some clarification if possible. Background is - purchased car mid-last year. Trader sent off the V5, but have the green slip. Tax ran out at end of October. Had letter through the door addressed to my name, but not my address - different house name (same house name as road name) from DCA stating not taxed, so LLP of £80 to pay. Subsequent search of car documents (as couldn't remember reminder coming and knew hadn't had car for 1 year) shows no V5 or reminders. Car is MOT'd and insured in my name at correct address (always has been) - details which I know DVLA have access too. Appears that is DVLA data entry error - as either entered wrong house name or if no house name on V5 from trader (didn't see it as with DVLA for cheirshed plate transfer at time of sale), then surely should have contacted previous owner for clarification as not complete details provided? I know I should have realised not had V5 etc., but I genuinely didn't. Planning to ask Postman why delivered this one to my address (different to envelope) and ask other house owners if received any DVLA letters and whether sent them back to Postman or DVLA as not at this address (would have been V5 plus a number of reminders) or just binned them. If you got this far, then thank-you and what is my best course of action?

-

Name of the Claimant ? MKDP LLP Date of issue - 11th April 2014 What is the claim for – 1."The claimant claims the sum of £xxxx.xx being monies due from the Defendant to the Claimant under a regulated agreement originally between the Defendant and HSBC Bank Plc. 2.The Defendant's account number was xxxxxxxxxxxxxxxx and was assigned to the Claimant on xx/12/2011, notice of this has been provided to the Defendant. 3.The defendant has failed to make payments in accordance with the terms of the agreement and a default notice has been served pursuant to the Consumer Credit Act 1974. The claimant claims the sum of £xxxx.xx and costs. The claimant has complied, as far as is necessary with the pre-action conduct practice direction." What is the value of the claim? £xxxx.xx (between £1300 - £1500) Has the claimant included section 69 interesticon (8%)within the total claim or is it shown separate within the Particulars but not added to the debt? Nothing specified Is the claim for a current or credit/loan account or mobile phone account? credit card account When did you enter into the original agreement before or after 2007? Before 2007 (I think) Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? No, Did you receive a Default Notice from the original creditor? Not that I recall Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not that I know of Why did you cease payments:- I lost a massive job in 2009 after a perfect credit history and found myself in a spiral out of control with various creditors wanting more than I had left. I put priority debts first! Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? No This is my first posting - I hope it makes sense I've received a CC Claim Form with the Claimant being MKDP LLP for a historical HSBC credit card debt. I've read the forums and extracted the following (see below QUESTIONS/ANSWERS) which I've completed as appropriate (changed some values etc. to protect identity). Since I was away working I missed the CC response time of 5+14, I submitted an acknowledgement of service with intent to defend a few days late and I've sent a CPR and CCA by Royal Mail (signed for) and called the court to explain my timing, interesting they said no action had been progressed and that I could do the acknowledgement on-line which I did. Have I done the right thing? Do I need to do anything else? Are MKDP likely to win and drop a CCJ on me? Thanks for your help on this - for forum is excellent. MWJ

Name of the Claimant ? MKDP LLP Date of issue - 11th April 2014 What is the claim for – 1."The claimant claims the sum of £xxxx.xx being monies due from the Defendant to the Claimant under a regulated agreement originally between the Defendant and HSBC Bank Plc. 2.The Defendant's account number was xxxxxxxxxxxxxxxx and was assigned to the Claimant on xx/12/2011, notice of this has been provided to the Defendant. 3.The defendant has failed to make payments in accordance with the terms of the agreement and a default notice has been served pursuant to the Consumer Credit Act 1974. The claimant claims the sum of £xxxx.xx and costs. The claimant has complied, as far as is necessary with the pre-action conduct practice direction." What is the value of the claim? £xxxx.xx (between £1300 - £1500) Has the claimant included section 69 interesticon (8%)within the total claim or is it shown separate within the Particulars but not added to the debt? Nothing specified Is the claim for a current or credit/loan account or mobile phone account? credit card account When did you enter into the original agreement before or after 2007? Before 2007 (I think) Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt Purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? No, Did you receive a Default Notice from the original creditor? Not that I recall Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not that I know of Why did you cease payments:- I lost a massive job in 2009 after a perfect credit history and found myself in a spiral out of control with various creditors wanting more than I had left. I put priority debts first! Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt managementicon plan? No This is my first posting - I hope it makes sense I've received a CC Claim Form with the Claimant being MKDP LLP for a historical HSBC credit card debt. I've read the forums and extracted the following (see below QUESTIONS/ANSWERS) which I've completed as appropriate (changed some values etc. to protect identity). Since I was away working I missed the CC response time of 5+14, I submitted an acknowledgement of service with intent to defend a few days late and I've sent a CPR and CCA by Royal Mail (signed for) and called the court to explain my timing, interesting they said no action had been progressed and that I could do the acknowledgement on-line which I did. Have I done the right thing? Do I need to do anything else? Are MKDP likely to win and drop a CCJ on me? Thanks for your help on this - for forum is excellent. MWJ -

Afternoon all, Hope every one is well. I have been a regular viewer of the site and have read treads relating to my issue but I have some additional questions. I am in the process of sending my defence I believe I have a few more days in which to do this. I acknowledged on the 22nd September. Name of the Claimant: MKDP LLP Date of issue: 08 Sep 2014 Date of issue XX + 19 days ( 5 day for service + 14 days to acknowledge) = XX + 14 days to submit defence = XX (33 days in total) - What is the claim for – the reason they have issued the claim? The claimant claims the sum of xxxxx being monies due from the defendant to the claimant under a regulated agreement originally between the defendant and Barclay card. The defendants account number was xxxxxxxxxxx and was assigned to the claimant on 22/6/2012, notice of this has been provided to the defendant. The defendant has failed to make payments in accordance with the terms of the agreement and a default notice has been served pursuant to the consumer credit act 1974. The claimant claims the sum of xxxx and costs. The claimant has complied as far as is necessart with the pre-action conduct practice direction. What is the value of the claim? £5k Is the claim for a current or credit/loan account or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? After Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. The Claim has been assigned by the Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? I do not recall being made aware by a notice of assignment only verbally and via chase letters. Did you receive a Default Notice from the original creditor? I do not recall receiving a default notice from the original creditor and the only default placed on my account was by the debt purchaser. Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? I have not received any statutory notice of default sums Why did you cease payments:- I was in financial difficulties, couldn’t afford minimum repayment or interest. I am pretty sure I advised Barclays the original creditor but months later claimant started chasing me for monies Was there a dispute with the original creditor that remains unresolved? not that I recall Did you communicate any financial problems to the original creditor and make any attempt to enter into a plan? I believe I advised of my financial circumstances I do not recall if an plan was offered or entered into. Additional information that may be useful or help; According to MKDP account was assigned on the 22/6/2012 they then defaulted me on 27/6/2012. Barclay Card have the account settled on 20/6/2012 Debt doesn’t appear Noddle/Credit tracker with MKDP until August Original default balance is £0 After requesting proof verbally with MKDP and months of waiting I have a suspect looking letter from Barclay Card and enclosed with this a reconstituted copy of my credit agreement, copy of terms of credit agreement varied in accordance with section 82(1). With this is a copy of the original application form signed by myself but no one else? How can they have this and not the term and conditions? And surely there have to be an authorising signature from Barclay card? Any advice would be appreciated Many thanks D

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS