Showing results for tags 'big'.

-

Please Help and give some advice I have over £7,000£ negative balance on my Paypal account - I can only say its my fault and I have to blame only myself but i want to pay off everything as soon as I can I had a call today from Paypal asking to pay this otherwise they will pass it to Debt collection, they gave me 7 days from today to pay as much as I can but what after ?? Did someone had simillar expeience ? What happenes after 7 days ? I asked to give me 8 weeks to pay it off but she didnt want to lissen Please advise, looks like they dont want any aggrements, I have to add that this debt its not old, week only

-

Hi - I've recently received three letters from Lowell headed 'Pre Legal Assessment' that goes on to say they are deciding whether to pass my account(s) to their legal team. Has anyone seen these before and should I do anything? I wasn't sure if I should send the Prove it letter or CCA request. They are for CCs and a store card. I have moved since the debts defaulted and they are around 5 years old. I have a scan of the letter with personal info obfuscated if anyone would like to take a look to make sure? I know the legislation for LBAs changed recently, so wasn't sure if they are allowed to send me a court claim next or it would be better to wait for an actual LBA. Thanks for any advice.

Hi - I've recently received three letters from Lowell headed 'Pre Legal Assessment' that goes on to say they are deciding whether to pass my account(s) to their legal team. Has anyone seen these before and should I do anything? I wasn't sure if I should send the Prove it letter or CCA request. They are for CCs and a store card. I have moved since the debts defaulted and they are around 5 years old. I have a scan of the letter with personal info obfuscated if anyone would like to take a look to make sure? I know the legislation for LBAs changed recently, so wasn't sure if they are allowed to send me a court claim next or it would be better to wait for an actual LBA. Thanks for any advice. -

They used to be Blemain, now are 'Together'. I am always behind with my mortgage. I am on a very low self employed income and it is erratic. So always end up having to pay three or four months arrears when they threaten me with an eviction. They have an court order due to persistent late payments. My circumstances have changed since I lived at the house...my gf who is also on the Deeds split up. She pays the mortgage, I pay the second mortgage with Together which is about £500 a month. I can never do one of those things with income and outgoings because is so erratic and I dont even live there. But I pay it every few months when I can so she doesn't lose her home, and at some point maybe we can sell it. But, because of all the charges and extra interest etc the amount I owe after paying it for about 10 years is about £10k more than I borrowed! Yet am Paying £6k a year! Total amount is about £60k and its a high interest rate because that is all I could get at the time. So virtually everything I earn bar about £100 a week pays that. And as I only get money erratically and then £2-3k every three months or so on average, I can never get in front just keep paying off the arrears and my living and some debts. So I am very depressed about it and cant see a way forward, except that one day we may be able to sell it. But there is no equity in it atm, and I am losing £6k a year really while the market is stagnant and yet actually reducing nothing its gone up over £10k. Problems started when the banks called my business o/d and loan in as then I had no way of budgeting to cope with the erratic income. I am effectively homeless, and cant even get tax credits because of my circumstances, and living between a few sets of friends and a new girlfriend. She has a tiny flat so I cant store anything there, and cant stay at all when her son is there...no room to swing a cat. All my stuff is with friends in my 'rooms' there, and I have nowhere to sit and do my books which are a few years behind and no doubt I am being chased for that too on money I haven't earned but fines for late books. I am in a total mess and cant see what to do. What can I do? Are these charges even legal? I am told they are not? I want to sort this out first as it will be one thing off my mind if I can stop them doing that. Then I have to face the HMRC and explain why I haven't done my books for several years afterwards.

They used to be Blemain, now are 'Together'. I am always behind with my mortgage. I am on a very low self employed income and it is erratic. So always end up having to pay three or four months arrears when they threaten me with an eviction. They have an court order due to persistent late payments. My circumstances have changed since I lived at the house...my gf who is also on the Deeds split up. She pays the mortgage, I pay the second mortgage with Together which is about £500 a month. I can never do one of those things with income and outgoings because is so erratic and I dont even live there. But I pay it every few months when I can so she doesn't lose her home, and at some point maybe we can sell it. But, because of all the charges and extra interest etc the amount I owe after paying it for about 10 years is about £10k more than I borrowed! Yet am Paying £6k a year! Total amount is about £60k and its a high interest rate because that is all I could get at the time. So virtually everything I earn bar about £100 a week pays that. And as I only get money erratically and then £2-3k every three months or so on average, I can never get in front just keep paying off the arrears and my living and some debts. So I am very depressed about it and cant see a way forward, except that one day we may be able to sell it. But there is no equity in it atm, and I am losing £6k a year really while the market is stagnant and yet actually reducing nothing its gone up over £10k. Problems started when the banks called my business o/d and loan in as then I had no way of budgeting to cope with the erratic income. I am effectively homeless, and cant even get tax credits because of my circumstances, and living between a few sets of friends and a new girlfriend. She has a tiny flat so I cant store anything there, and cant stay at all when her son is there...no room to swing a cat. All my stuff is with friends in my 'rooms' there, and I have nowhere to sit and do my books which are a few years behind and no doubt I am being chased for that too on money I haven't earned but fines for late books. I am in a total mess and cant see what to do. What can I do? Are these charges even legal? I am told they are not? I want to sort this out first as it will be one thing off my mind if I can stop them doing that. Then I have to face the HMRC and explain why I haven't done my books for several years afterwards. -

Had this sent to me by my disability advisor.... http://surveys.parkinsons.org.uk/s/bigbenefitssurvey/

-

Why take any dispute to the Ombudsman , is it worth the trouble? For the 3 time of trying to post this reply but worth reading:- Rights of Entry (Gas and Electricity Boards) Act 1954, The Gas Safety (Rights of Entry) Regulations 1996 In a genuine dispute there are no rights of entry(i.e magistrates warrant issued), however I would also caution health and safety matters if its a gas leak. if electricity meter dispute The Electricity Act 1989, The Utilities Act 2000 Note schedule 7 of 1989 act and schedule 5 of 2000 Act, an electric meter cannot be removed until a dispute is resolved. I did provide links to laws but the post is not going through. Hope this helps you and others. Mike

-

I am a new member and seeking for help and hope I will get a help and guidance to sort out TAX Credit rejection. I am a single mother of 2 children. In Feb 2015 my husband and I went thru separation due to our every other day arguments which was going on for past 3 years and eventually he moved out in Feb 2015 and left me no money to pay for the bills. While I was with him he used to get child tax credits and help from local council towards the house rent as he was on low wages and I was just a house wife. At time of separation my daughter was 13 yrs and son 6 yr old. Once my husband moved out he informed the local authority about the change and circumstances and because of this the council stopped paying rent. I did not know anything about the council and tax credit matters as everything was dealt by my husband. I applied for the housing & council tax benefits to my local council and child tax credits to HMRC which were all accepted. My ex asked me NOT to go thru the child support because he will buy stuff and support children which he has been but never paid me any money. I got a job in a clothing store to meet the ends and to provide for my children. Right after few weeks of separation I had been asking my ex to change his address as he does not live here. He kept telling me he doesnt have a fixed address and he lives at different places such as few days/ weeks at his friends or relatives. His letters from bank and other letters kept coming to my address after roughly many months I got fed up and I started to return his letters to senders and also threw in the bin and as usual my ex kept repeating that he will change the address soon . During the separation our relation had been up and down but I never stopped him from seeing the children as they dearly love him especially my son he took all this badly that he often cried during his sleep calling his father and also his school teachers informed me that he seem to be lost in the class. Due to the state of my children I gave him open access to my ex that he can see children whenever he wants to. In April 2016 we gave a try to get back together and allowed him to move back with me and I also informed my local council in writing. Unfortunately this did not work and I asked him to move out just after 2 weeks and once again I informed the council. Then from July 2016 my tax credits were stopped without any advance notice. On enquiring tax credit help desk told me to send my last 6 months bank statements, Pay slips, utility bills, Tenancy agreement of the property, housing & council tax benefit documents and also proof of address of my ex such as tenancy agreement. I provided all the documents except 2 and that is my own and also my ex’s tenancy agreement. My landlord has not provided me with the tenancy agreement due to being behind my rent and my ex could not provide his agreement because his landlord does not want to declare about the room renting to avoid tax. Tax credits rejected my considerations and in Nov 2016 asked me again to provide the same but recent documents and once again I did send most of them except my own agreement. My ex gave me only one tenancy agreement one of his addresses he had lived at. In total my ex lived at 5 addresses and none of them issued him tenancy agreement except one which he gave to me to send to tax credits. Recently I received a rejection letter from tax credits asking me to pay over £8K and have given me a time of one month (now less than 3 weeks) to apply for tribunal hearing. I have done nothing wrong and got in this big mess. There is no way I am able to pay that amount and don’t know what am I supposed to do. I am in great stress and tensions and one of my friend mentioned about CAG to get advice. Anyone here to advice and help to deal with this matter ? I would appreciate your help. Thanks Please see the attached letter from HMRC I have received recently. docs1.pdf

-

Hi All, Firstly, apologies if something like this has already been discussed. I have seen similar posts but I think my predicament is slightly different...it's a long story but I hope that some of you will take the time to read it and have some advice for me... So, some years ago, in my clearly very naive and gullible early 20s, I met my ex husband. We got married in 2010 when I was 23, less so because we thought it was the best thing to do, more so for 'financial reasons'. About 6 months before we got married, my ex had started to have some money problems and I noticed some unauthorised transactions on my credit card totally about £800. The transactions came under Victor Chandler and I reported them to my bank's fraud department. On learning that I had done this, my ex decided to tell me that I needed to withdraw my claim to the fraud department as it was to do with him and he could get into a lot of trouble! (He's in the RAF and works in the armoury...I believe being in debt and having gambling problems would be something that's frowned upon in his position...). He explained that he had used a online gambling site to 'transfer money' as he needed it to help his mum... the story was more elaborate and seemed to make more sense at the time.. .anyway I was young and stupid and decided to give him the benefit of the doubt and believe him. I suspected he had a gambling problem, but every time he'd spin me a story and I stupidly tried to believe him. As things progressed, I buried my head in the sand and we got married and as soon as that happened, everything went from suspicious to disaster... The guy had all my bank details, all my personal details... he memorised my bank account numbers and card numbers off by heart! He'd put on a girls voice and call up my bank pretending to be me and all sorts. He took over my accounts completely and in a bid to stop me from finding things out he'd stop me going online by tampering with the phone lines, etc. One day I found he'd taped a small piece of clear tape over the phone plug so I could check my bank online or call them! My life and my finances got to the point where I was working full time and each payday, as soon as I had been paid, literally within an hour all my available funds would be gone. My bank statements from the period which I was with him are just full of transactions of money (mostly) going out and coming in from various online gambling websites. . Despite my feelings deep down and my instincts telling me everything was wrong, I tried whatever I could to just stick it through and hoped he would change and everything would eventually go away! I mean, he went to such lengths to prove to me that things were being sorted...! By May 2013 I finally decided that I was not going to take it anymore. I wasn't going to let him continue to ruin my life and I left him. We separated in May 2013. I moved back to Hong Kong for 8 months to get away from him and stayed with my parents. During this time, my ex husband and I still had some contact as I was still having major issues with my bank and I was desperate for him to sort it out so that, even if I couldn't get any of my hard earned money back at least the black hole of debt would stop getting deeper! Eventually, he told me that a solicitor had managed to get some money back for us, but it was being paid into my account via a payday loan company. As I was out of the country and wasn't up for speaking to him much I didn't pay too much attention to this. Some money did appear in my account from a payday loan company, but the money soon disappeared again. I thought it was just the same old same old. It wasn't until some time in 2015 when I had returned to the UK and got officially divorced from him that I found out that the money that went into my account was in fact a payday loan that he had taken out in MY name. And here in my predicament lies.. .the loan was taken out online, so he used all my details and signed electronically and the money did indeed go into an account that belonged to me. The money then left my bank account going to various gambling websites, and I'm taking a wild guess that all of those accounts to all of those gambling sites were probably in my name as well. This is a debt that I don't feel I'm responsible for at all after all the punishment and the financial ruin he's left me in. In the time I was with him I lost ALL my wages plus some money my parents had gifted me in the hopes we'd settle down and have a decent deposit to put on a house. All in all, I would hazard a guess at losing somewhere between £60-70k in the time I was with him. Not to mention his own salary on top of that! But, now I think I'm stuck with this loan of around £1200. I am now being hounded by the PRA group who have bought the debt off QuickQuid and are sending me letters saying that I need to pay them. I can see on my credit record there is a default against my name under the PRA group for this unpaid debt. It's causing me a lot of stress now as I have finally settled again, with a most amazing man and we are expecting our first child together and would like to purchase our first home but my finances are making me very uneasy. In all this time, I have never contacted the police as I did what I could to try to come to a civil separation from him. I didn't want to get him in trouble as I wasn't sure if it would affect his job and whatever ill feelings I had toward him I tried to stay fair and settle things with as little trouble as possible. Seems though, that the only person suffering is me! Is it too late to take this to the police now? Have I left it too long? My ex husband, to name the things he's done.. .gambled our entire marriage, made up solicitors and created fraudulent email trails. He's taken money from me that should have gone into my bank and brought me home a 'receipt' of paying it in to my account then turned a story about how the money went into the 'wrong account'. He's taken out numerous loans in my name. Opened up accounts to gambling websites in my name. He moved into military married quarters after we were separated using a marriage certificate that was no longer valid, ran up trespass charges for a late march out and slapped me with a bill of nearly £1500! He'd steal my purse... I've never lost my purse in my entire life.. .in the 3 years we were married I managed to lose it THREE times AND every time it's miraculously turned up back on camp.. .minus the couple hundred pounds emergency cash I had in it! He cheated on me. He's even lied to me now about his current girlfriend being sexually assaulted and suffering panic attacks because of it. ..and his poor girlfriend. ..he steals money from her kids...! I apologise for all the excess info and I understand it's all a bit jumbled. I just find it extremely difficult to put what he did to me in words but felt that some background on all the things he got up to might help me get some advice... Thanks.

Hi All, Firstly, apologies if something like this has already been discussed. I have seen similar posts but I think my predicament is slightly different...it's a long story but I hope that some of you will take the time to read it and have some advice for me... So, some years ago, in my clearly very naive and gullible early 20s, I met my ex husband. We got married in 2010 when I was 23, less so because we thought it was the best thing to do, more so for 'financial reasons'. About 6 months before we got married, my ex had started to have some money problems and I noticed some unauthorised transactions on my credit card totally about £800. The transactions came under Victor Chandler and I reported them to my bank's fraud department. On learning that I had done this, my ex decided to tell me that I needed to withdraw my claim to the fraud department as it was to do with him and he could get into a lot of trouble! (He's in the RAF and works in the armoury...I believe being in debt and having gambling problems would be something that's frowned upon in his position...). He explained that he had used a online gambling site to 'transfer money' as he needed it to help his mum... the story was more elaborate and seemed to make more sense at the time.. .anyway I was young and stupid and decided to give him the benefit of the doubt and believe him. I suspected he had a gambling problem, but every time he'd spin me a story and I stupidly tried to believe him. As things progressed, I buried my head in the sand and we got married and as soon as that happened, everything went from suspicious to disaster... The guy had all my bank details, all my personal details... he memorised my bank account numbers and card numbers off by heart! He'd put on a girls voice and call up my bank pretending to be me and all sorts. He took over my accounts completely and in a bid to stop me from finding things out he'd stop me going online by tampering with the phone lines, etc. One day I found he'd taped a small piece of clear tape over the phone plug so I could check my bank online or call them! My life and my finances got to the point where I was working full time and each payday, as soon as I had been paid, literally within an hour all my available funds would be gone. My bank statements from the period which I was with him are just full of transactions of money (mostly) going out and coming in from various online gambling websites. . Despite my feelings deep down and my instincts telling me everything was wrong, I tried whatever I could to just stick it through and hoped he would change and everything would eventually go away! I mean, he went to such lengths to prove to me that things were being sorted...! By May 2013 I finally decided that I was not going to take it anymore. I wasn't going to let him continue to ruin my life and I left him. We separated in May 2013. I moved back to Hong Kong for 8 months to get away from him and stayed with my parents. During this time, my ex husband and I still had some contact as I was still having major issues with my bank and I was desperate for him to sort it out so that, even if I couldn't get any of my hard earned money back at least the black hole of debt would stop getting deeper! Eventually, he told me that a solicitor had managed to get some money back for us, but it was being paid into my account via a payday loan company. As I was out of the country and wasn't up for speaking to him much I didn't pay too much attention to this. Some money did appear in my account from a payday loan company, but the money soon disappeared again. I thought it was just the same old same old. It wasn't until some time in 2015 when I had returned to the UK and got officially divorced from him that I found out that the money that went into my account was in fact a payday loan that he had taken out in MY name. And here in my predicament lies.. .the loan was taken out online, so he used all my details and signed electronically and the money did indeed go into an account that belonged to me. The money then left my bank account going to various gambling websites, and I'm taking a wild guess that all of those accounts to all of those gambling sites were probably in my name as well. This is a debt that I don't feel I'm responsible for at all after all the punishment and the financial ruin he's left me in. In the time I was with him I lost ALL my wages plus some money my parents had gifted me in the hopes we'd settle down and have a decent deposit to put on a house. All in all, I would hazard a guess at losing somewhere between £60-70k in the time I was with him. Not to mention his own salary on top of that! But, now I think I'm stuck with this loan of around £1200. I am now being hounded by the PRA group who have bought the debt off QuickQuid and are sending me letters saying that I need to pay them. I can see on my credit record there is a default against my name under the PRA group for this unpaid debt. It's causing me a lot of stress now as I have finally settled again, with a most amazing man and we are expecting our first child together and would like to purchase our first home but my finances are making me very uneasy. In all this time, I have never contacted the police as I did what I could to try to come to a civil separation from him. I didn't want to get him in trouble as I wasn't sure if it would affect his job and whatever ill feelings I had toward him I tried to stay fair and settle things with as little trouble as possible. Seems though, that the only person suffering is me! Is it too late to take this to the police now? Have I left it too long? My ex husband, to name the things he's done.. .gambled our entire marriage, made up solicitors and created fraudulent email trails. He's taken money from me that should have gone into my bank and brought me home a 'receipt' of paying it in to my account then turned a story about how the money went into the 'wrong account'. He's taken out numerous loans in my name. Opened up accounts to gambling websites in my name. He moved into military married quarters after we were separated using a marriage certificate that was no longer valid, ran up trespass charges for a late march out and slapped me with a bill of nearly £1500! He'd steal my purse... I've never lost my purse in my entire life.. .in the 3 years we were married I managed to lose it THREE times AND every time it's miraculously turned up back on camp.. .minus the couple hundred pounds emergency cash I had in it! He cheated on me. He's even lied to me now about his current girlfriend being sexually assaulted and suffering panic attacks because of it. ..and his poor girlfriend. ..he steals money from her kids...! I apologise for all the excess info and I understand it's all a bit jumbled. I just find it extremely difficult to put what he did to me in words but felt that some background on all the things he got up to might help me get some advice... Thanks. -

As most here will know, I registered with UJ ages ago but found it utter rubbish so stopped using it. They can't mandate you to use any specific job-search site and there are far better ones I use. Got this email today from our wonderful friends at DWP.. 'Our records show that this email address (shown above) is currently registered against an active Universal Jobmatch account. It’s been a year since you accessed the account and used it to search for jobs. If you would like to keep this account please take a moment to log in. If you do nothing the account will be disabled within 4 weeks. Sincerely, Universal Jobmatch helpdesk Do not reply to this email unless you are directed to do so as we will not be able to respond. Please use the 'Contact us' facility if you have any further issues or to report this email as suspicious. We will never ask you for your password in an email. © 2013 Department for Work and Pensions (DWP)' Just confirms what we already knew; they're monitoring how often you log in to UJ. No surpises there then. What's the betting I'll get another email after my UJ account has expired?

-

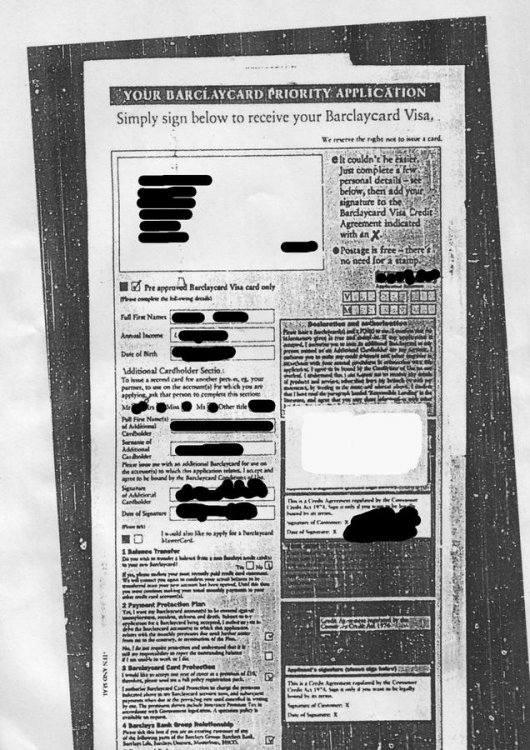

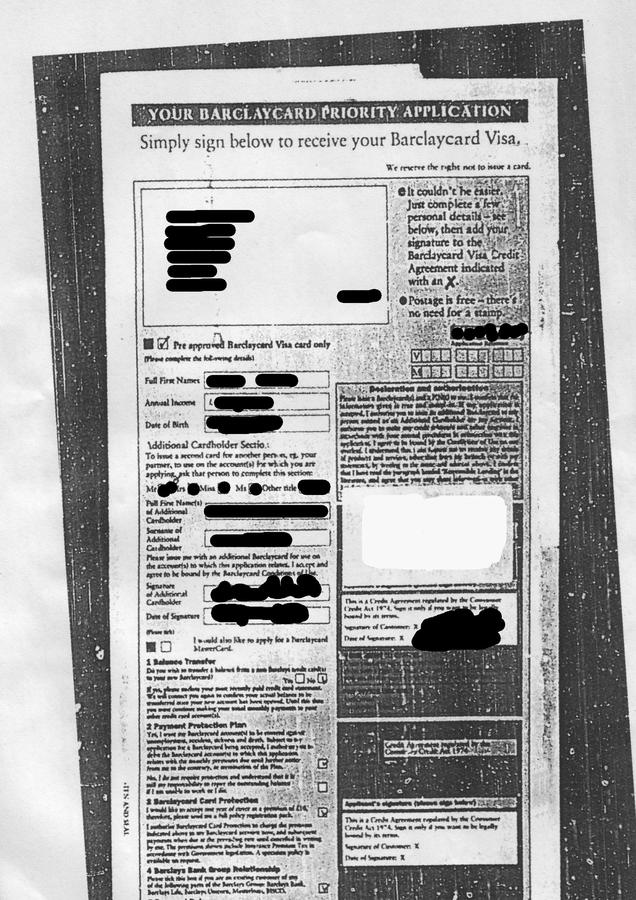

Hi all, I had no idea that with my Barclays account I had PPi. Barclays contacted me a few years ago and i got the odd thing in the post from them, it always referred to the fact that 'IF' i had ppi, tbh i really didn't think i did. The most recent form they sent me was so long! With so many questions I could not possibly remember the answers. This company contacted me and said they could see if they could do it for me and that they would do all the hard work, but then they sent me exactly the same questions, I called them and explained this is why i signed with them because i thought they were going to do all this and the guy just tried to help with the answers. Shortly after this I get a refund from Barclays for £3700 approx. AMAZING! BUT they have sent me a bill for £1400. I'm annoyed because all i needed to do was fill in the form like i did for this company and send it back to Barclays, like they asked me to a while ago, now i have to pay this company £1400, so much money, for just this form... Is there anything i can do? I have been dealing with Barclays directly for a while on this and just hit a brick wall when the form came through with lots of questions that i couldn't remember the answer to.

Hi all, I had no idea that with my Barclays account I had PPi. Barclays contacted me a few years ago and i got the odd thing in the post from them, it always referred to the fact that 'IF' i had ppi, tbh i really didn't think i did. The most recent form they sent me was so long! With so many questions I could not possibly remember the answers. This company contacted me and said they could see if they could do it for me and that they would do all the hard work, but then they sent me exactly the same questions, I called them and explained this is why i signed with them because i thought they were going to do all this and the guy just tried to help with the answers. Shortly after this I get a refund from Barclays for £3700 approx. AMAZING! BUT they have sent me a bill for £1400. I'm annoyed because all i needed to do was fill in the form like i did for this company and send it back to Barclays, like they asked me to a while ago, now i have to pay this company £1400, so much money, for just this form... Is there anything i can do? I have been dealing with Barclays directly for a while on this and just hit a brick wall when the form came through with lots of questions that i couldn't remember the answer to. -

Seriously boiling mad - I have had RAC breakdown insurance for last 4 yrs . On auto renewal direct debit . Just discovered after checking my bank online they have taken out £113 ( Last years renewal was £85 ) with no letter sent to state new premium - straight on phone to wait 20 minutes for call center . I have used their service about twice in 4yrs . Demanded a full refund for the absolute cheek of them , got offered a check in the post . ( Firstly in was a £16 refund ) Now waiting for their Complaints section to contact me for a direct transfer as it has maxed out my poor account - will not be using them again or recommending these shysters . Beware if yr on DD payments

Seriously boiling mad - I have had RAC breakdown insurance for last 4 yrs . On auto renewal direct debit . Just discovered after checking my bank online they have taken out £113 ( Last years renewal was £85 ) with no letter sent to state new premium - straight on phone to wait 20 minutes for call center . I have used their service about twice in 4yrs . Demanded a full refund for the absolute cheek of them , got offered a check in the post . ( Firstly in was a £16 refund ) Now waiting for their Complaints section to contact me for a direct transfer as it has maxed out my poor account - will not be using them again or recommending these shysters . Beware if yr on DD payments -

http://www.lbc.co.uk/eon-posts-7bn-loss-with-uk-profits-flat-126493 E.ON Posts €7bn Loss With UK Profits Flat Wednesday, 9th March 2016 09:09 The parent company of 'big six' energy firm E.ON says annual losses more than doubled to ?7bn (£5.4bn) in 2015 - with UK profits flat despite supply business earnings falling 9% to £267 The German company blamed an ?8.8bn writedown in the value of its loss-making power generation assets for the group's net loss and said that the spin-off of its oil and gas-fired power activities from its renewable energy division, completed in January, would also hurt its outlook for 2016. E.ON warned that "the course ahead will be tougher and longer than anticipated" given the changes to its business model and weak energy costs. Germany's biggest energy firms, E.ON and RWE - which owns npower in the UK - have been forced to write off billions in the value of their conventional energy assets as the German government demands a shift to cleaner sources. The cost of closing Germany's nuclear plants - a consequence of the accident at the Fukushima plant in Japan - has also pushed them into the red. Following the release of the group's financial performance, E.ON later confirmed in greater detail how its UK business did. It part-blamed a 3.5% cut to standard gas tariffs in January last year for 2015 annual supply business profits falling, alongside a competitive market. It said overall UK profits were flat on last year as more renewable energy projects, such as the Humber Gateway wind farm, came on stream in its generation arm. E.ON has not been alone in blaming fierce competition in the household supply business for hits to its profits. The market is currently the subject of a Competition and Markets Authority probe which is expected to publish its remedies on Thursday.

http://www.lbc.co.uk/eon-posts-7bn-loss-with-uk-profits-flat-126493 E.ON Posts €7bn Loss With UK Profits Flat Wednesday, 9th March 2016 09:09 The parent company of 'big six' energy firm E.ON says annual losses more than doubled to ?7bn (£5.4bn) in 2015 - with UK profits flat despite supply business earnings falling 9% to £267 The German company blamed an ?8.8bn writedown in the value of its loss-making power generation assets for the group's net loss and said that the spin-off of its oil and gas-fired power activities from its renewable energy division, completed in January, would also hurt its outlook for 2016. E.ON warned that "the course ahead will be tougher and longer than anticipated" given the changes to its business model and weak energy costs. Germany's biggest energy firms, E.ON and RWE - which owns npower in the UK - have been forced to write off billions in the value of their conventional energy assets as the German government demands a shift to cleaner sources. The cost of closing Germany's nuclear plants - a consequence of the accident at the Fukushima plant in Japan - has also pushed them into the red. Following the release of the group's financial performance, E.ON later confirmed in greater detail how its UK business did. It part-blamed a 3.5% cut to standard gas tariffs in January last year for 2015 annual supply business profits falling, alongside a competitive market. It said overall UK profits were flat on last year as more renewable energy projects, such as the Humber Gateway wind farm, came on stream in its generation arm. E.ON has not been alone in blaming fierce competition in the household supply business for hits to its profits. The market is currently the subject of a Competition and Markets Authority probe which is expected to publish its remedies on Thursday. -

Thank you to all at bridgehouse mansfield who today helped with the passing of a loved one got us in without an appointment had someone with him constantly put him on oxygen to help him breathe Thank you for how kind all your staff were simba/aslan ???? - adopted 2005 - feb 2016

-

Hi all, Here is the response from DCA from a complaint I made to them. In the letter i received from them they say that this is their "Final Response" to the complaint. And that the documents sent to me satisfy their legal obligations under the CCA 1974 etc. I have removed all personal information from it and the big white patch you can see over where a "signature" was -who knows impossible to tell due to the quality - looks like a big white sticker with some sort of bar code on it. Date on application form 1997. The t and c's are the wrong shape and size to have fitted anywhere on the application form and nowhere does it connect with the application form (ie serial number or anything else) The bits i can read, if I squint hard enough and go cross-eyed, have nothing about interest rates or penalties. And yes the scan is as bad as the original sent to me. My question is does this satisfy the request and would a court accept them? If, of course, it goes that far. Thank you in anticipation.

-

Are you ready for Wallace and Gromit's Big Bake? Wallace and Gromit need you to roll out your rolling pins, whip out your whisks and preheat your ovens to help them raise some dough for kids in hospitals and hospices from 7-13 December. The BIG Bake proudly supported by Homepride Flour, aims to get people of all ages baking to raise money for sick children in hospitals and hospices across the UK. Whether you bake cupcakes or cheesecakes, pies or pastries, brownies or bloomers, or your own unique showstopper, rise to the occasion and get registered to support this cracking fundraising event. Wallace & Gromit’s Children’s Charity will send you a FREE BIG Bake fundraising pack with all you need to take part, including posters, stickers and our very special bunting. The BIG Bake is an event for everyone; you can take part at work, at school, at home with friends and family or even within your local community! Don’t forget to enter their Cracking Baker competition to be in with a chance to win some fantastic prizes! Visit the BIG Bake website to find out more and to register for your FREE fundraising pack!!!

Are you ready for Wallace and Gromit's Big Bake? Wallace and Gromit need you to roll out your rolling pins, whip out your whisks and preheat your ovens to help them raise some dough for kids in hospitals and hospices from 7-13 December. The BIG Bake proudly supported by Homepride Flour, aims to get people of all ages baking to raise money for sick children in hospitals and hospices across the UK. Whether you bake cupcakes or cheesecakes, pies or pastries, brownies or bloomers, or your own unique showstopper, rise to the occasion and get registered to support this cracking fundraising event. Wallace & Gromit’s Children’s Charity will send you a FREE BIG Bake fundraising pack with all you need to take part, including posters, stickers and our very special bunting. The BIG Bake is an event for everyone; you can take part at work, at school, at home with friends and family or even within your local community! Don’t forget to enter their Cracking Baker competition to be in with a chance to win some fantastic prizes! Visit the BIG Bake website to find out more and to register for your FREE fundraising pack!!! -

Hi guys. Ok so I'm going to try my best to explain it all date by date below. I had some debt issues awhile ago and was put on an IVA with Payplan. November 2008, I started the IVA with PayPlan November 2013, I completed the IVA and was given the completion certificate which I have here with me 10th September 2015, I was informed by AI scheme limited (by letter) that I may have a PPI claim 21st September 2015, I received letter from Barclaycard saying my claim was sucessful and that they has sent a cheque for £3601.61 to Payplan 25th September, I called Barclaycard requesting the cheque be stopped as I haven't had any dealings with Payplan since my completion in November 2013 but was told that I had to contact Payplan. 25th September, I called Payplan but was told they are allowed to keep the money and I am only entitled to the intrest (8%). After explaining that the completion certificate says that they are only entitled to any 'pending PPI claims post closure) I was told that I am still only entitle to the 8%. The lady on the phone said "Oh we are allowed to keep it for up to 6 years after the start of your IVA" ..... However it's now been over 7 years. Her supervisor still said "You can have 8%" I did try to log on to the PayPlan site to look at any old documents but as the IVA ended in 2013 it won't let me in. Do I have a legal standing on this? I had no idea any PPI was due to be until a couple of weeks ago when AI scheme said I might have. It's been way over the 6 years since I started my IVA and I have the completion certificate to prove I finished up in Nov 2013. Any help you guys could give me would be very much appreciated. I heard about Green VS Wright in March 2015 that may be of help? Thanks.

Hi guys. Ok so I'm going to try my best to explain it all date by date below. I had some debt issues awhile ago and was put on an IVA with Payplan. November 2008, I started the IVA with PayPlan November 2013, I completed the IVA and was given the completion certificate which I have here with me 10th September 2015, I was informed by AI scheme limited (by letter) that I may have a PPI claim 21st September 2015, I received letter from Barclaycard saying my claim was sucessful and that they has sent a cheque for £3601.61 to Payplan 25th September, I called Barclaycard requesting the cheque be stopped as I haven't had any dealings with Payplan since my completion in November 2013 but was told that I had to contact Payplan. 25th September, I called Payplan but was told they are allowed to keep the money and I am only entitled to the intrest (8%). After explaining that the completion certificate says that they are only entitled to any 'pending PPI claims post closure) I was told that I am still only entitle to the 8%. The lady on the phone said "Oh we are allowed to keep it for up to 6 years after the start of your IVA" ..... However it's now been over 7 years. Her supervisor still said "You can have 8%" I did try to log on to the PayPlan site to look at any old documents but as the IVA ended in 2013 it won't let me in. Do I have a legal standing on this? I had no idea any PPI was due to be until a couple of weeks ago when AI scheme said I might have. It's been way over the 6 years since I started my IVA and I have the completion certificate to prove I finished up in Nov 2013. Any help you guys could give me would be very much appreciated. I heard about Green VS Wright in March 2015 that may be of help? Thanks. -

http://www.dailymail.co.uk/news/article-3081294/Britain-s-oldest-poppy-seller-dead-Avon-Gorge-aged-92.html This story of a 92 year old being hounded by charities, because she was kind with her money, should make people and charities think. 20 years ago, there were not so many charities around and people loyally gave to a few they had an interest in. In the last 10 years there has been an explosion in the number of charities and the amount of communications they produce. They have become businesses some of which may be more interested in making money for the people running them, than any people the charity is supposed to be supporting. I won't name the charities, but this is my experience. 1) Childrens charity - small DD payment per month. Every month a begging letter through the post with pictures of David or Sally, abused by one of their parents, with very sad pictures and story to go with it. They ask for more money to help David and Sally, so the charity can help more children. Stopped giving them money due to the constant letters. 2) Charity for the blind - After buying some raffle tickets for about £10 or £20, I kept being sent more raffle tickets every few months for the latest draw, with the expectation I would buy or sell them others. I would also receive phone calls from them begging me to take even more raffle tickets. Stopped giving them money. 3) Heart related charity - Gave a donation on behalf of a relative who died - Constant letters asking for more donations, as well as emails and phone calls. Some of the letters would have been expensive to send out, as they were large magazines Have not given to them since and they have stopped sending letters. I expect that everyone who gives to charity experiences exactly the same and I am not sure the charities obtain more money because they keep sending out begging letters. Perhaps they need to have a think about how they raise money.

http://www.dailymail.co.uk/news/article-3081294/Britain-s-oldest-poppy-seller-dead-Avon-Gorge-aged-92.html This story of a 92 year old being hounded by charities, because she was kind with her money, should make people and charities think. 20 years ago, there were not so many charities around and people loyally gave to a few they had an interest in. In the last 10 years there has been an explosion in the number of charities and the amount of communications they produce. They have become businesses some of which may be more interested in making money for the people running them, than any people the charity is supposed to be supporting. I won't name the charities, but this is my experience. 1) Childrens charity - small DD payment per month. Every month a begging letter through the post with pictures of David or Sally, abused by one of their parents, with very sad pictures and story to go with it. They ask for more money to help David and Sally, so the charity can help more children. Stopped giving them money due to the constant letters. 2) Charity for the blind - After buying some raffle tickets for about £10 or £20, I kept being sent more raffle tickets every few months for the latest draw, with the expectation I would buy or sell them others. I would also receive phone calls from them begging me to take even more raffle tickets. Stopped giving them money. 3) Heart related charity - Gave a donation on behalf of a relative who died - Constant letters asking for more donations, as well as emails and phone calls. Some of the letters would have been expensive to send out, as they were large magazines Have not given to them since and they have stopped sending letters. I expect that everyone who gives to charity experiences exactly the same and I am not sure the charities obtain more money because they keep sending out begging letters. Perhaps they need to have a think about how they raise money. -

Im going to France on Friday last Monday i tried to buy euros online. i tried 4-5 different company's to get a good rate but i could not buy through any of them because i had recently moved house and didn't pass their identity checks. One of these company's has frozen over £1500 out of my bank account since Monday and my bank nationwide are doing nothing. i don't know which company has frozen the money as it only says on the statement travel money. i ended up going to the post office to get my euros, now am left skint until this money is returned. can someone please help on this as i only have a few days till i go.

Im going to France on Friday last Monday i tried to buy euros online. i tried 4-5 different company's to get a good rate but i could not buy through any of them because i had recently moved house and didn't pass their identity checks. One of these company's has frozen over £1500 out of my bank account since Monday and my bank nationwide are doing nothing. i don't know which company has frozen the money as it only says on the statement travel money. i ended up going to the post office to get my euros, now am left skint until this money is returned. can someone please help on this as i only have a few days till i go. -

Big band leader James Last dies at 86

Conniff posted a topic in The Bear Garden – for off-topic chat

My favourite musician of all times a real gentleman. Saw many of his concerts when he visited the UK. No1 Forum -

Hello, I am in a very difficult situation with Wandsworth council over council tax. This started back last year with when I moved into a shared property with some other people and for some reason the Council tax was put under my name and the name of someone else that didn't live here. The council never sent me a bill or any correspondence until I received a summons for none payment of council tax. At this point I emailed them and explained I live in a shared house with other people and I had not received any bill and the bill should not be in my sole name. I was then informed that someone would look into this and get back to me. The next thing I heard was a Bailiff coming to my door threatening to take my stuff away or I have to pay the full amount plus over 20% of fees on top. I contacted the council again asking about any appeal or the fact that the bill is not solely mine, it took them 2 weeks to reply by email which they told me that I have had the chance to appeal and that they sent me a multiple occupancy form, which they never did. They also told me to contact the Bailiff from now on. The worse thing about this is I suffer from PSTD and extreme bouts of depression and I have recently been laid off because me taking time off because of this situation to go back on medication and into therapy. Before this I had been medication free for over a year. I feel I have been treated most unfairly and all I wanted was the chance to pay the bill in installments and for the bill not to be solely my responsibly. Is there anything I can do? as the situation seems to be getting worse no matter what I try. Thanks!

Hello, I am in a very difficult situation with Wandsworth council over council tax. This started back last year with when I moved into a shared property with some other people and for some reason the Council tax was put under my name and the name of someone else that didn't live here. The council never sent me a bill or any correspondence until I received a summons for none payment of council tax. At this point I emailed them and explained I live in a shared house with other people and I had not received any bill and the bill should not be in my sole name. I was then informed that someone would look into this and get back to me. The next thing I heard was a Bailiff coming to my door threatening to take my stuff away or I have to pay the full amount plus over 20% of fees on top. I contacted the council again asking about any appeal or the fact that the bill is not solely mine, it took them 2 weeks to reply by email which they told me that I have had the chance to appeal and that they sent me a multiple occupancy form, which they never did. They also told me to contact the Bailiff from now on. The worse thing about this is I suffer from PSTD and extreme bouts of depression and I have recently been laid off because me taking time off because of this situation to go back on medication and into therapy. Before this I had been medication free for over a year. I feel I have been treated most unfairly and all I wanted was the chance to pay the bill in installments and for the bill not to be solely my responsibly. Is there anything I can do? as the situation seems to be getting worse no matter what I try. Thanks! -

Hello all, I came back from oz 9 months ago owing substantial debt , on unsecured loans and cc. I have decided the only option for me is to ignore the emails demanding payments. There is no way I can pay back the debts. What is likely to happen in the end? I know this is a pretty random&basic msg, but I want to try and kkkeep it fairly anonymous!

-

Need some advice big time, I received a letter from the job centre earlier stating they will be taking money out of my ESA for child support, I have never herd off the CSA, my two daughters are 18 and nearly 20 although I haven't seen them for a few years through no fault of mine I used to regularly give my ex money for my children she'd never got the CSA involved and she's always worked so never got the CSA involved, naturally I thought she had got them involved this time as I have not spoke to her in a few years either, I phoned job centre plus they told me I need to speak to the CSA as it was them who told job centre plus to take money from me, I phoned CSA add some right arrogant bloke on the other end telling me my ex had not contacted them and that it doesn't matter how old my children are as I have never paid through the CSA I must pay something back, surely this is not right due to the age of my children I told him I used to pay my ex money he told me it doesn't matter because it's not on their records! Please advise if they can do this or not, He also told me it doesn't matter if my children was working full-time when I told him I would take this further and see citizens advice he put the phone down on me.

-

Hi, First time post here. I have a problem which I am hoping forum members can offer their opinions and advice on please. I run a small business which has an office based phone system. Hackers somehow accessed our office phone system one night in January. They managed to remotely make hundreds of calls, one after the other, to a premium rate number in the Solomon Islands. Each time the call connected, it cost £50. The total cost of the fraudulent calls is £3,500. BT contacted us the following morning to say it looked like our system had been hacked, due to the unusual overnight call activity to premium rate numbers. We immediately found and patched the loophole which had allowed the remote access. I then contacted our BT business account manager and asked them to place the disputed bill on hold whilst it was investigated. Subsequently, BT have written me to advise that, according to their terms and conditions, we are liable for the fraudulent calls. They have offered a payment plan, but won't reduce the bill. BT have also advised me that because the premium rate numbers are outside of the UK, they are not controlled via a UK regulatory body. They also tell me that they are under no obligation to monitor or identify fraudulent use of the network. Because the calls were made to the Solomon Islands they also advised there is no way they can recover the cost back. So, BT's view is that I have to pay the bill. They also suggested to recover the cost from the IT company which manages our network or from the Phone company which manages our phone system. Both of those companies are small business, and they say it wasn't their fault, and in any event they can't afford to pay. I should probably also add that BT agree that they accept that the phone calls have been fraudulently by criminals. I have also reported the details to Action Fraud to get my crime reference number. I've written back to BT and said asked the following question; i) As the fraud was identified straight away and BT agree it was fraud, BT wouldn't pay the company in the Solomon Islands immediately - it must go through some form of invoice process which would take some days to process. As I asked BT to not make the payment to the company in the Solomon Island when I first found out about the fraud, my logic is that, if BT don't pay the invoice to the Solomon Islands, then there is no need to pursue me for the costs. ii) Can BT then confirm they have notified the company in the Solomon Islands of the fraud? When did they notify the company? I have also asserted, if BT do go ahead and make the payment to the Solomon Islands, for a payment which they know to the fraudulent, and then the recover the cost from me, they will be benefiting from the proceeds of crime, which is definitely immoral and probably illegal. Whilst their terms and condition state that I am responsible for the fraudulent use of their network, they also have some responsibility to prevent fraudulent use of their network. They know for example from our call history, we never phone premium rate numbers, we never phone the Solomon Islands, we never phone in the middle of night, and we don't make repeated calls to the same premium rate number one after the other. Our normal call bill with BT is £200 / month by the way. BT have replied saying they are seeking a legal view. Of course their solicitor will say BT are in the right. I've replied to say, they need to be sure of their facts as if they insist on taking the payment from my account, I will raise a moneyclaim on-line, and we can let a County Court judge decide if they agree with BT's view. In my mind, the crux is whether BT make the payment to the Solomon Islands straight away, or whether they actually have an opportinity to prevent the invoice from being made straight away whist it is being investigated. If they don't make any attempt to prevent the fraud from being completed, I believe this would be unreasonable and it would help my case. Can anyone offer any suggestions or advice or how I should progress this?

Hi, First time post here. I have a problem which I am hoping forum members can offer their opinions and advice on please. I run a small business which has an office based phone system. Hackers somehow accessed our office phone system one night in January. They managed to remotely make hundreds of calls, one after the other, to a premium rate number in the Solomon Islands. Each time the call connected, it cost £50. The total cost of the fraudulent calls is £3,500. BT contacted us the following morning to say it looked like our system had been hacked, due to the unusual overnight call activity to premium rate numbers. We immediately found and patched the loophole which had allowed the remote access. I then contacted our BT business account manager and asked them to place the disputed bill on hold whilst it was investigated. Subsequently, BT have written me to advise that, according to their terms and conditions, we are liable for the fraudulent calls. They have offered a payment plan, but won't reduce the bill. BT have also advised me that because the premium rate numbers are outside of the UK, they are not controlled via a UK regulatory body. They also tell me that they are under no obligation to monitor or identify fraudulent use of the network. Because the calls were made to the Solomon Islands they also advised there is no way they can recover the cost back. So, BT's view is that I have to pay the bill. They also suggested to recover the cost from the IT company which manages our network or from the Phone company which manages our phone system. Both of those companies are small business, and they say it wasn't their fault, and in any event they can't afford to pay. I should probably also add that BT agree that they accept that the phone calls have been fraudulently by criminals. I have also reported the details to Action Fraud to get my crime reference number. I've written back to BT and said asked the following question; i) As the fraud was identified straight away and BT agree it was fraud, BT wouldn't pay the company in the Solomon Islands immediately - it must go through some form of invoice process which would take some days to process. As I asked BT to not make the payment to the company in the Solomon Island when I first found out about the fraud, my logic is that, if BT don't pay the invoice to the Solomon Islands, then there is no need to pursue me for the costs. ii) Can BT then confirm they have notified the company in the Solomon Islands of the fraud? When did they notify the company? I have also asserted, if BT do go ahead and make the payment to the Solomon Islands, for a payment which they know to the fraudulent, and then the recover the cost from me, they will be benefiting from the proceeds of crime, which is definitely immoral and probably illegal. Whilst their terms and condition state that I am responsible for the fraudulent use of their network, they also have some responsibility to prevent fraudulent use of their network. They know for example from our call history, we never phone premium rate numbers, we never phone the Solomon Islands, we never phone in the middle of night, and we don't make repeated calls to the same premium rate number one after the other. Our normal call bill with BT is £200 / month by the way. BT have replied saying they are seeking a legal view. Of course their solicitor will say BT are in the right. I've replied to say, they need to be sure of their facts as if they insist on taking the payment from my account, I will raise a moneyclaim on-line, and we can let a County Court judge decide if they agree with BT's view. In my mind, the crux is whether BT make the payment to the Solomon Islands straight away, or whether they actually have an opportinity to prevent the invoice from being made straight away whist it is being investigated. If they don't make any attempt to prevent the fraud from being completed, I believe this would be unreasonable and it would help my case. Can anyone offer any suggestions or advice or how I should progress this? -

Can anyone help on this one? We haver taken over a small business (fitness centre) this is in a larger building (a rugby club house) and is leased from them. The rent in 2008 was £10000 pa. We have half the first floor for an office, changing rooms, reception area, studio and gym, total area 350 sqm. The other half of the first floor belongs to the rugby club and has an office, reception area, changing rooms and a bar/conference centre/kitchen, total area 350 sqm Both premises were valued by the VOA in April 2014. We are valued at £16250, the other half of the first floor is valued at £7000. At first sight, this seems horribly iniquitous (as well as putting us at a major disadvantage relative to other local fitness centres) and I'm trying to work up to the formalities needed to contest this. But before I start, am I missing something obvious… is there a reason that I don't know about which will explain the discrepancy?

Can anyone help on this one? We haver taken over a small business (fitness centre) this is in a larger building (a rugby club house) and is leased from them. The rent in 2008 was £10000 pa. We have half the first floor for an office, changing rooms, reception area, studio and gym, total area 350 sqm. The other half of the first floor belongs to the rugby club and has an office, reception area, changing rooms and a bar/conference centre/kitchen, total area 350 sqm Both premises were valued by the VOA in April 2014. We are valued at £16250, the other half of the first floor is valued at £7000. At first sight, this seems horribly iniquitous (as well as putting us at a major disadvantage relative to other local fitness centres) and I'm trying to work up to the formalities needed to contest this. But before I start, am I missing something obvious… is there a reason that I don't know about which will explain the discrepancy? -

I haven't been on here for some time - thought my debt problems were behind me but If anyone can offer some advice Id appreciate it. I will try and be concise, many years ago I was very much in debt. almost 50k. I was self employed and work was up and down, I robbed peter to pay Paul (many of you will understand this) the problem got worse until I decided to do something about it. I borrowed a substantial amount of money and set about contacting all of the creditors, All of whom were really born from Lloyds Bank - I negotiation settlements around 30-40 percent of the debts. All apart from a couple, which I only entered into because of Lloyds mailing lists - eg a AA credit card (through the post) and a loan - these two totalled around 6k - and I offered to settle with them back in 2009 like I successfully did with ALL of the other debts - it was a massive undertaking, huge suffering, which led to depression and dark times - something I have had problems with for years. They refused to settle and some years later I think reared there ugly head again, and I tried to settle again, not successfully. Id had all manner of phone calls, (changed number twice) many many many red letters, eventually to cut a long story short, 1st credit picked it up, in the last few months have attempted to get a summary judgement - I attended courts and the judge refused suggesting they had not given me the opportunity to file a proper defence. the judge suggested that there would certainly be a liability on my behalf for the debt (no costs were due but will be at the next junctre) I made an offer to settle outside of court with the firms solicitor - 30 percent of the debt - they refused, I handed the letter I wrote in 2009 to settle to show the solicitor my good intention of closure. I later rang a few days later and increased the offer two more times ( I dont have this money i would have to borrow it) they still refused to accept it. I have to file a defence tomorrow in between my very busy day and I want to know the best thing to go for.

I haven't been on here for some time - thought my debt problems were behind me but If anyone can offer some advice Id appreciate it. I will try and be concise, many years ago I was very much in debt. almost 50k. I was self employed and work was up and down, I robbed peter to pay Paul (many of you will understand this) the problem got worse until I decided to do something about it. I borrowed a substantial amount of money and set about contacting all of the creditors, All of whom were really born from Lloyds Bank - I negotiation settlements around 30-40 percent of the debts. All apart from a couple, which I only entered into because of Lloyds mailing lists - eg a AA credit card (through the post) and a loan - these two totalled around 6k - and I offered to settle with them back in 2009 like I successfully did with ALL of the other debts - it was a massive undertaking, huge suffering, which led to depression and dark times - something I have had problems with for years. They refused to settle and some years later I think reared there ugly head again, and I tried to settle again, not successfully. Id had all manner of phone calls, (changed number twice) many many many red letters, eventually to cut a long story short, 1st credit picked it up, in the last few months have attempted to get a summary judgement - I attended courts and the judge refused suggesting they had not given me the opportunity to file a proper defence. the judge suggested that there would certainly be a liability on my behalf for the debt (no costs were due but will be at the next junctre) I made an offer to settle outside of court with the firms solicitor - 30 percent of the debt - they refused, I handed the letter I wrote in 2009 to settle to show the solicitor my good intention of closure. I later rang a few days later and increased the offer two more times ( I dont have this money i would have to borrow it) they still refused to accept it. I have to file a defence tomorrow in between my very busy day and I want to know the best thing to go for. -

Hi do not buy AA repair and cover warranty its a big [problem] the insurer is brc please be aware my car a 2005 Peugeot 407 broke down last Friday car was vibrating really bad as man came and said it was flywheel he towed me to local garage where they stripped gearbox they found that the flywheel dual mass had broken and seized so wasn't moving and not doing its job brc phoned and said it was not covered as its wear and tear now how can be that if its broken the flywheel has no wear on it they then stated that the clutch plate was worn down to rivets this is not the case there is thousands of miles left on all parts and if flywheel had not broken it would be still going car was not slipping at all just really bad vibration they say in there terms it is not covered for wear and tear but it doesn't say we do not cover cars over a certain age it is a big rip of so any part that fails they can say its down to wear they refuse to pay car is below average milage and fully serviced please helpa

Hi do not buy AA repair and cover warranty its a big [problem] the insurer is brc please be aware my car a 2005 Peugeot 407 broke down last Friday car was vibrating really bad as man came and said it was flywheel he towed me to local garage where they stripped gearbox they found that the flywheel dual mass had broken and seized so wasn't moving and not doing its job brc phoned and said it was not covered as its wear and tear now how can be that if its broken the flywheel has no wear on it they then stated that the clutch plate was worn down to rivets this is not the case there is thousands of miles left on all parts and if flywheel had not broken it would be still going car was not slipping at all just really bad vibration they say in there terms it is not covered for wear and tear but it doesn't say we do not cover cars over a certain age it is a big rip of so any part that fails they can say its down to wear they refuse to pay car is below average milage and fully serviced please helpa

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS