Showing results for tags 'set'.

-

Here's a good one. I send a letter of claim to the Defendant, a company, on the 5th of December 2016 which is ignored. I sent a follow up letter on the 31st of January which is ignored. I issue proceedings on the 27th of February which are deemed served on the 3rd of March. The Defendant files an acknowledgement of service saying they will file a defence within 28 days of service. They fail to file a defence. I apply for judgment on the 4th of May and judgment is issued on the 5th of May. Defendant pays judgment on the 22nd of May. Defendant writes to me on the 22nd of June saying that they want to overturn the judgment as they always intended to file a defence. Defendant says they will sue me for the judgment money unless i accept their offer of paying them back 75% of it and the entire thing is wrapped up in a Thomlinson Order. Incidentally, despite all this, the Defendant continues to do the wrongdoing I sued them for. What do people suggest I do?

Here's a good one. I send a letter of claim to the Defendant, a company, on the 5th of December 2016 which is ignored. I sent a follow up letter on the 31st of January which is ignored. I issue proceedings on the 27th of February which are deemed served on the 3rd of March. The Defendant files an acknowledgement of service saying they will file a defence within 28 days of service. They fail to file a defence. I apply for judgment on the 4th of May and judgment is issued on the 5th of May. Defendant pays judgment on the 22nd of May. Defendant writes to me on the 22nd of June saying that they want to overturn the judgment as they always intended to file a defence. Defendant says they will sue me for the judgment money unless i accept their offer of paying them back 75% of it and the entire thing is wrapped up in a Thomlinson Order. Incidentally, despite all this, the Defendant continues to do the wrongdoing I sued them for. What do people suggest I do? -

Greetings. Making a PPI claim on an old loan that was repaid in full. Wondering if I succeed, will the original creditor be allowed to use this to offset an outstanding (statute bared) debt (overdrawn current a/c and assume the original creditor still owns the debt). I noticed post #4 by dx100uk and specifically in bold: "if the original creditor still owns the debt then they can offset but not the 8% stat int part of any refund." in this thread: http://www.consumeractiongroup.co.uk...BC-credit-card I've seen on the FOS website: compensation for being deprived income etc.. http://www.financial-ombudsman.org.u...tment-loss.htm and various scenarios on PPI redress: http://www.financial-ombudsman.org.uk/publications/technical_notes/ppi/redress.html#_Where_the_consumer Does anyone have any further info or legal precedent about the 8% SI part of a PPI claim not being allowed to be used by a creditor to offset an existing debt and as such should go to the claimant ? Many thx

-

Hi - asking for my sister who is a disabled adult (mental Health). She has received a judgment by default CCJ from Home Direct, she doesn't remember receiving the court pack, nor is it something I have seen when visiting - as she usually gets me to read through things for her. Now she owes the money, no doubt about that. And up to 2016 was making regular monthly payments to a DCA when the agency changed to the current one. She has tried twice to set up the plan again, only for them to not reply, and send a standard letter again a few months later. She phoned the new DCA after receiving the default judgment notice, and they were not sympathetic at all - went through an income and expenditure with her - and included her PIP payments (and those of her daughter who has ASD) as income. They wanted a massive £800 per month, the debt is £2400. So: 1 - Can they include PIP payments as income? 2 - Would she have grounds to set aside as she says she didn't get the court paperwork (although from the sticky thread it mentions you would have to show a defence to the claim as well for that?). 3 - Would setting aside mean they would be more likely to accept a reasonable payment plan anyway? Any help is very much appreciated - thanks

Hi - asking for my sister who is a disabled adult (mental Health). She has received a judgment by default CCJ from Home Direct, she doesn't remember receiving the court pack, nor is it something I have seen when visiting - as she usually gets me to read through things for her. Now she owes the money, no doubt about that. And up to 2016 was making regular monthly payments to a DCA when the agency changed to the current one. She has tried twice to set up the plan again, only for them to not reply, and send a standard letter again a few months later. She phoned the new DCA after receiving the default judgment notice, and they were not sympathetic at all - went through an income and expenditure with her - and included her PIP payments (and those of her daughter who has ASD) as income. They wanted a massive £800 per month, the debt is £2400. So: 1 - Can they include PIP payments as income? 2 - Would she have grounds to set aside as she says she didn't get the court paperwork (although from the sticky thread it mentions you would have to show a defence to the claim as well for that?). 3 - Would setting aside mean they would be more likely to accept a reasonable payment plan anyway? Any help is very much appreciated - thanks -

My request is a simple one, I want one or two set of Blank Used Empty Original HP Cartridge for Refill Purposes. Model is 953 or 953 XL Printer Model is Officejet Pro 8715 Any one any idea of how I can source these, please let me know. It has to be Originals. Thanks all.

My request is a simple one, I want one or two set of Blank Used Empty Original HP Cartridge for Refill Purposes. Model is 953 or 953 XL Printer Model is Officejet Pro 8715 Any one any idea of how I can source these, please let me know. It has to be Originals. Thanks all. -

Good evening, I am not sure if this is the right place to be asking for advice about this but I thought I would post a thread. I recently ordered a sofa set, I paid them via online banking, the first payment was the deposit and the second payment was the remaining money due, they are clearly not what I ordered. The sofas were delivered today and it was all a farce, as I live in a flat I had to pay an extra £20 for them to carry them up to my first floor flat which I already did, I had to argue with them for sometime before they rang up the company to get it confirmed. They pretty much took all the packaging off before bringing them up and then just dumped them in my tiny hall way when they should have brought them in to my living room first and then unpacked them. Now, heres the issue, when one of the couriers brought the cushions up I thought they were the right ones but after taking the last of the packaging off from the smallest sofa it turns out the sofa does not match the picture on their website, the colors do not match etc. (See images attached). I have spoken to the manager over the phone and over email and he insists the correct sofas have been delivered and that I shouldn't have signed the delivery receipt if something was wrong and that he's willing to accept a return at my cost of £89 I shouldn't have to pay £89 if the sofas are not what I purchased, no where on their website does it say if you want to return them, it will cost £89. On the receipt it says the couriers should have unboxed them in my living room not outside, it also states no price in the box where it says how much it would cost if the items needed returning. It's states nothing on their website regarding returns as well. Where do I stand legally with this as a consumer? (I can't add pictures)

Good evening, I am not sure if this is the right place to be asking for advice about this but I thought I would post a thread. I recently ordered a sofa set, I paid them via online banking, the first payment was the deposit and the second payment was the remaining money due, they are clearly not what I ordered. The sofas were delivered today and it was all a farce, as I live in a flat I had to pay an extra £20 for them to carry them up to my first floor flat which I already did, I had to argue with them for sometime before they rang up the company to get it confirmed. They pretty much took all the packaging off before bringing them up and then just dumped them in my tiny hall way when they should have brought them in to my living room first and then unpacked them. Now, heres the issue, when one of the couriers brought the cushions up I thought they were the right ones but after taking the last of the packaging off from the smallest sofa it turns out the sofa does not match the picture on their website, the colors do not match etc. (See images attached). I have spoken to the manager over the phone and over email and he insists the correct sofas have been delivered and that I shouldn't have signed the delivery receipt if something was wrong and that he's willing to accept a return at my cost of £89 I shouldn't have to pay £89 if the sofas are not what I purchased, no where on their website does it say if you want to return them, it will cost £89. On the receipt it says the couriers should have unboxed them in my living room not outside, it also states no price in the box where it says how much it would cost if the items needed returning. It's states nothing on their website regarding returns as well. Where do I stand legally with this as a consumer? (I can't add pictures) -

I am really encouraged after reading many posts on various debts. I had a Store card with Creation and I did have an arrangement to pay but they told me it was not enough and through Drydens got a CCJ. They told me that if I were to pay the full outstanding balance that they requested no court case. Somehow I managed to find the money nearly 2k and paid them. Yet somehow I got a CCJ. I did not go to the court or had a defence. That was in 2011 and it will be SB'd in May this year. I read it somewhere if I paid the full amount I should not have had the CCJ. Is this correct? My question is that if it is possible to remove this judgement because I was told that if I were to pay in full no court case? Any advice would be greatly appreciated.

-

Hello I am new to the forum and am hoping for some advice on behalf of my brother. I am hoping for some guidance on the process for applying to the courts to have a CCJ made by default judgement '"set aside" This is a really long story going back 12 years!!! My brother was victim of a car buying [problem] which went on some years ago which resulted in him receiving a fake cheque for the sale of his car. He took this cheque (unaware it was 'rubber') to HSBC Bank who cashed the cheque credited the £10k into my brothers bank account. My brother withdrew the money and paid his debts off. Over a week later, HSBS contacted him to advise that the cheque had bounced and he now owed the bank £10K After much debate HSBC ended up calling this cash an overdraft and ultimately the debt went to debt collection. My brother ignored the debt, paid nothing against it and made no contact with the debt collection company. He cannot remember whether a default ever appeared on his credit file for this as it was 12 years ago, however, his last credit report with Experian before the CCJ appeared did not show any record of the debt. In July 2016 he updated his credit file with his new address and registered on the electoral role suddenly he began receiving letters from Robinson Way about the debt. Unfortunately he ignored the letters and eventually he was issued with a threat of legal action. He did contact the debt recovery company asking for proof of a credit agreement but this was never received. To get to the point, a CCJ has now been issued as he did not respond to the County Court notice. I am aware that there may be an option to dispute the CCJ by way of requesting it be 'set aside 'if he can prove he was not liable for the debt. I believe he may have a case due to: The original debt being 12 years old He did not make contact with the company within the last 6 years He did not receive the credit agreement he requested I am also not sure of the legality of the debt in the first place given that the debt only occurred due to the bank releasing funds on a fraudulent cheque and then asking for it back -I would have thought the security of cheques would have been the banks responsibility? I am now wondering of we can dispute this CCJ and if so where on earth do we start!? Any advise would be greatly appreciated

-

3053548.thumb.jpg.6ea05a752ac6bbf38ae4e7be9676053a.jpg) The following statement was released a few days ago by the Government. This is in response to a Daily Mail campaign earlier this year regarding individuals who have found themselves unable to get a mortgage or credit because of the existence of a judgment against them that they were unaware of (usually because all correspondence had been sent to a previous address). Depending on the outcome, this consultation could have far reaching consequences for bailiff enforcement. Currently, in relation to council tax arrears, a local authority are permitted to issue a summons to the 'last known' address. In relation to an unpaid penalty charge notice, correspondence must be addressed to the address held by DVLA at the time of the contravention.

The following statement was released a few days ago by the Government. This is in response to a Daily Mail campaign earlier this year regarding individuals who have found themselves unable to get a mortgage or credit because of the existence of a judgment against them that they were unaware of (usually because all correspondence had been sent to a previous address). Depending on the outcome, this consultation could have far reaching consequences for bailiff enforcement. Currently, in relation to council tax arrears, a local authority are permitted to issue a summons to the 'last known' address. In relation to an unpaid penalty charge notice, correspondence must be addressed to the address held by DVLA at the time of the contravention. -

Hello all Thank you for your help I received ccj court order but I didn't receive the court papers before the ccj There is no date of birth on the ccj and the second initial is wrong How do u apply for set aside There is no credit agreement and debt is over six years Is there any chance to win Do I need a defence How to do set aside Any help please The ccj issued over 2months

Hello all Thank you for your help I received ccj court order but I didn't receive the court papers before the ccj There is no date of birth on the ccj and the second initial is wrong How do u apply for set aside There is no credit agreement and debt is over six years Is there any chance to win Do I need a defence How to do set aside Any help please The ccj issued over 2months -

I applied for a flat last week, and their credit check showed that I have a CCJ against my name. Apparently, it was registered back in 2014. I am not sure if it was a deafult judgement or not, to be honest. Can I still apply for this to be set aside? If so, how do I go about it?

I applied for a flat last week, and their credit check showed that I have a CCJ against my name. Apparently, it was registered back in 2014. I am not sure if it was a deafult judgement or not, to be honest. Can I still apply for this to be set aside? If so, how do I go about it? -

It seems most debt collection agencies know when you have started making an effort to pay back debts. I have been able to agree reduced settlements or reduced monthly payments for some of my wife's debts, starting with the smallest and working upwards. It seems lenders that have made no contact in months previously are starting to threaten legal again and in one case , sending debt collectors to our house. I check our credit reports monthly through Noodle, Credit Score and also Check My File and decided to check our file also with Trust Online for any CCJs. No CCJs even on the Trust Online as at 30/08/16. My wife's latest report now shows a CCJ from 23/08/16 for a default that shes had a while. It was for a HP Car finance from Blackhorse She told them in 2014 that she's moved to husband's address and wanted to negotiate a way she could either hand car back or pay reduced amounts. I am self employed and was the sole earner. I was in hospital for quite a while after a motor accident and couldn't make payments on wife's behalf. Blackhorse decided to collect the car in the middle of the night rather than negotiate and wrote to her at my address (current address) that £480 owed. A period of two years, she has received letters from 5 debt collecting companies claiming that debt has been sold to them all at the right address. I feel the debt collectors have intentionally sent the CCJ to old address for £586 so that we will loose out knowing that it takes a month to show on credit reports. The courts claim a month has passed and said i could pay £255 to set aside but warned that the lender doesn't have to agree to a reduction of lump sum payment or monthly payments even after it's set aside. Can i get the debt company to agree to set the CCJ aside by consent so that i only have to pay £100 to the court and a full amount to them? Is there any point paying £255 + £586 for a debt of £480 that seems to have been intentionally sent elsewhere? I read also that the Court takes timing seriously, is it a disadvantage to contact the lender instead of complaining to the court first? Whatever happens , i don't want her to get a CCJ, not even a satisfied CCJ. Am i better getting it set aside and waiting for the response or is it easy to just get a judge to throw it out entirely since there's no justification for Blackhorse or any of the debt selling firms not to have my current address? If she's told the lender of her current address, lender has repossessed vehicle from the same address, lender has written to confirm debt sold at same address and five different companies have written to that address... Can i get the court to penalise their solicitor or perhaps even cancel the CCJ all together?

It seems most debt collection agencies know when you have started making an effort to pay back debts. I have been able to agree reduced settlements or reduced monthly payments for some of my wife's debts, starting with the smallest and working upwards. It seems lenders that have made no contact in months previously are starting to threaten legal again and in one case , sending debt collectors to our house. I check our credit reports monthly through Noodle, Credit Score and also Check My File and decided to check our file also with Trust Online for any CCJs. No CCJs even on the Trust Online as at 30/08/16. My wife's latest report now shows a CCJ from 23/08/16 for a default that shes had a while. It was for a HP Car finance from Blackhorse She told them in 2014 that she's moved to husband's address and wanted to negotiate a way she could either hand car back or pay reduced amounts. I am self employed and was the sole earner. I was in hospital for quite a while after a motor accident and couldn't make payments on wife's behalf. Blackhorse decided to collect the car in the middle of the night rather than negotiate and wrote to her at my address (current address) that £480 owed. A period of two years, she has received letters from 5 debt collecting companies claiming that debt has been sold to them all at the right address. I feel the debt collectors have intentionally sent the CCJ to old address for £586 so that we will loose out knowing that it takes a month to show on credit reports. The courts claim a month has passed and said i could pay £255 to set aside but warned that the lender doesn't have to agree to a reduction of lump sum payment or monthly payments even after it's set aside. Can i get the debt company to agree to set the CCJ aside by consent so that i only have to pay £100 to the court and a full amount to them? Is there any point paying £255 + £586 for a debt of £480 that seems to have been intentionally sent elsewhere? I read also that the Court takes timing seriously, is it a disadvantage to contact the lender instead of complaining to the court first? Whatever happens , i don't want her to get a CCJ, not even a satisfied CCJ. Am i better getting it set aside and waiting for the response or is it easy to just get a judge to throw it out entirely since there's no justification for Blackhorse or any of the debt selling firms not to have my current address? If she's told the lender of her current address, lender has repossessed vehicle from the same address, lender has written to confirm debt sold at same address and five different companies have written to that address... Can i get the court to penalise their solicitor or perhaps even cancel the CCJ all together? -

Greetings.. Hi, I am new to this forum .. ITS REALLY A GREAT SITE. I would like to get some advice from your great service for my claim case . I explain briefly below; I am the Claimant and a judgment was given DEFAULT in favour of me in a county court for my unpaid wages as Defendant did not come to the HEARING. As defendant did not pay me , I was about to make an application to the court for the service of Bailiff , then Court Notice arrived with the copies of judgment set aside application and a witness statement of defendant , saying as follows; '' TAKE NOTICE that the application to set aside judgement Hearing will take place on 1st November 2016. 30 Minutes has been allowed for the Hearing '' please kindly help me to answer the following; 1. Should I take my eye witness along with me to this Hearing to prove my case which I hope will help not to set judgment aside ? 2. Can I send my witness statement with my REPLY to the court for the defendantst false details? 3. Actually what will happen at this Hearing and what will the Judge ask me ? 4. What is the consent order ? I coundnt understand it fully .please give some details.. 5. How to write to Judge to make an Order to the defendant to bring some documents for the HEARING , I many times had asked for from defendant which he did not serve me yet? hope you will find some time to answer me kindly.

-

I had a card from HSBC in 2002. In 2010, I had difficulties paying so I went through the sar process, discovered that I had never signed a contract and tried to negotiate a lower settlement on this basis. In 2011 I missed a deadline to acknowledge a claim from Northampton as so received a ccj via default. I only missed the deadline by one day, spoke with the court and sent in a n244. However, the case was assigned to Uxbridge and so the n244 was lost in the system. So I sent another n244 to the new court and understood that this was in place. I have now discovered that the ccj is in place. I have contacted the court but they are saying there isn't a lot they can tell me but they can confirm there was a set aside hearing but are now telling me it should have been transferred to a court local to myself. It is a little complex for me, can anyone offer any advice please?

I had a card from HSBC in 2002. In 2010, I had difficulties paying so I went through the sar process, discovered that I had never signed a contract and tried to negotiate a lower settlement on this basis. In 2011 I missed a deadline to acknowledge a claim from Northampton as so received a ccj via default. I only missed the deadline by one day, spoke with the court and sent in a n244. However, the case was assigned to Uxbridge and so the n244 was lost in the system. So I sent another n244 to the new court and understood that this was in place. I have now discovered that the ccj is in place. I have contacted the court but they are saying there isn't a lot they can tell me but they can confirm there was a set aside hearing but are now telling me it should have been transferred to a court local to myself. It is a little complex for me, can anyone offer any advice please? -

Hi all, I live in a property rented from a housing trust under a licence rather than a tenancy agreement. When I took on the tenancy about 7 years ago I was informed that the clerk to the trustees would hold a set of keys to my home and it would be stored in a locked safe. I have recently discovered that keys have been used to enter properties owned by the trust by workers employed by them without the tenant's permission or presence. One particular maintenance worker often calls unnanounced to carry out small jobs and has been asked on numerous occasions by various tenants to make an appointment but he refuses to do so. He often works until 8pm making this awkward for people coming home from work or with children to get meals etc. This person has entered a neighbour's home without her permission. He also entered another person's home without her permission and moved personal items which I assume was to enable him to carry out a repair job. He has also questioned me because my daughter has fitted a secondary lock to her door saying he's reported her to the trust clerk as he checked that she hasn't provided a spare key. My questions are: a) has the clerk to the trustees got legal rights to hold a spare key b) does the male maintenance worker have legal rights to use this key without permission of the tenant (all mainly female living alone) c) can tenants have secondary locks fitted (leaving the original lock in place), without having to pass a key on to the clerk to the trustees as some of the tenants have been told. As you probably gather most of the tenants are females living alone and are very nervous that the male maintenance worker rocks up at any time without an appointment and seems to be able to access keys to gain entrance when the tenant isn't present. Unfortunately any complaints to the trust clerk about this man seem to fall on deaf ears and he seems to be very highly thought of by the trustees. Any legal advice welcome with pointers towards legislation to quote if possible. Thanks in anticipation.

Hi all, I live in a property rented from a housing trust under a licence rather than a tenancy agreement. When I took on the tenancy about 7 years ago I was informed that the clerk to the trustees would hold a set of keys to my home and it would be stored in a locked safe. I have recently discovered that keys have been used to enter properties owned by the trust by workers employed by them without the tenant's permission or presence. One particular maintenance worker often calls unnanounced to carry out small jobs and has been asked on numerous occasions by various tenants to make an appointment but he refuses to do so. He often works until 8pm making this awkward for people coming home from work or with children to get meals etc. This person has entered a neighbour's home without her permission. He also entered another person's home without her permission and moved personal items which I assume was to enable him to carry out a repair job. He has also questioned me because my daughter has fitted a secondary lock to her door saying he's reported her to the trust clerk as he checked that she hasn't provided a spare key. My questions are: a) has the clerk to the trustees got legal rights to hold a spare key b) does the male maintenance worker have legal rights to use this key without permission of the tenant (all mainly female living alone) c) can tenants have secondary locks fitted (leaving the original lock in place), without having to pass a key on to the clerk to the trustees as some of the tenants have been told. As you probably gather most of the tenants are females living alone and are very nervous that the male maintenance worker rocks up at any time without an appointment and seems to be able to access keys to gain entrance when the tenant isn't present. Unfortunately any complaints to the trust clerk about this man seem to fall on deaf ears and he seems to be very highly thought of by the trustees. Any legal advice welcome with pointers towards legislation to quote if possible. Thanks in anticipation. -

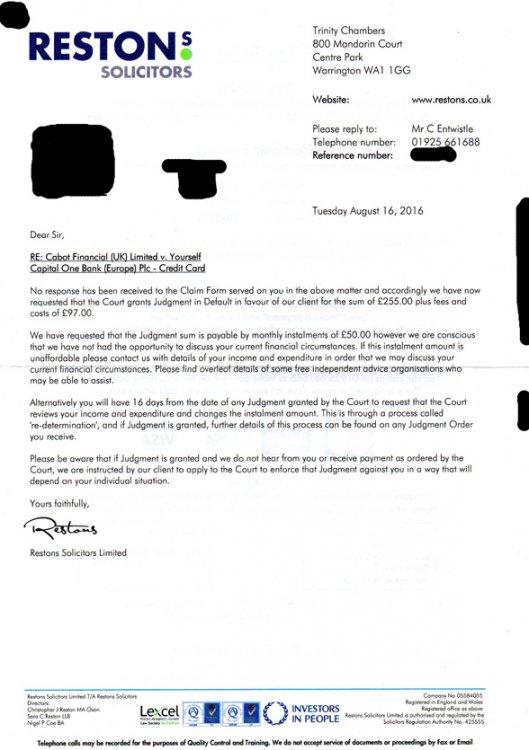

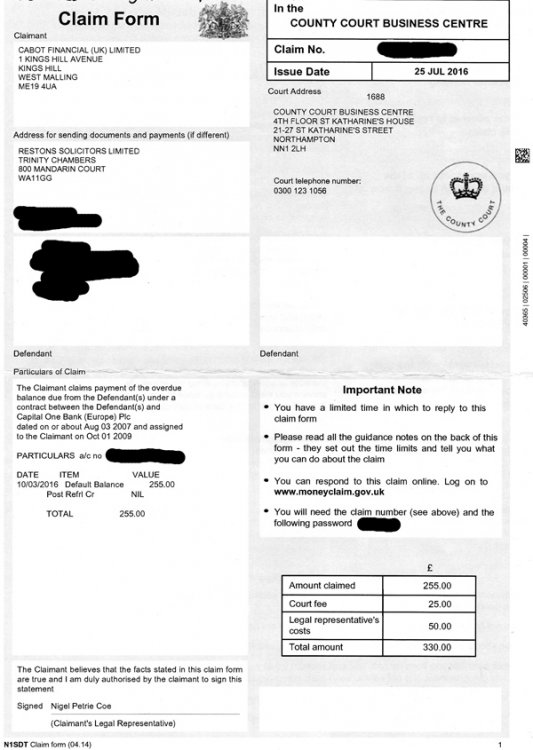

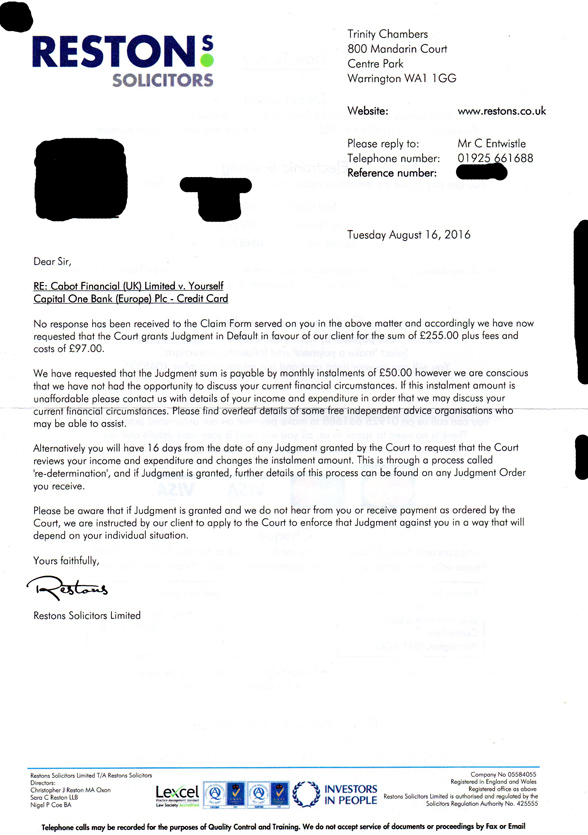

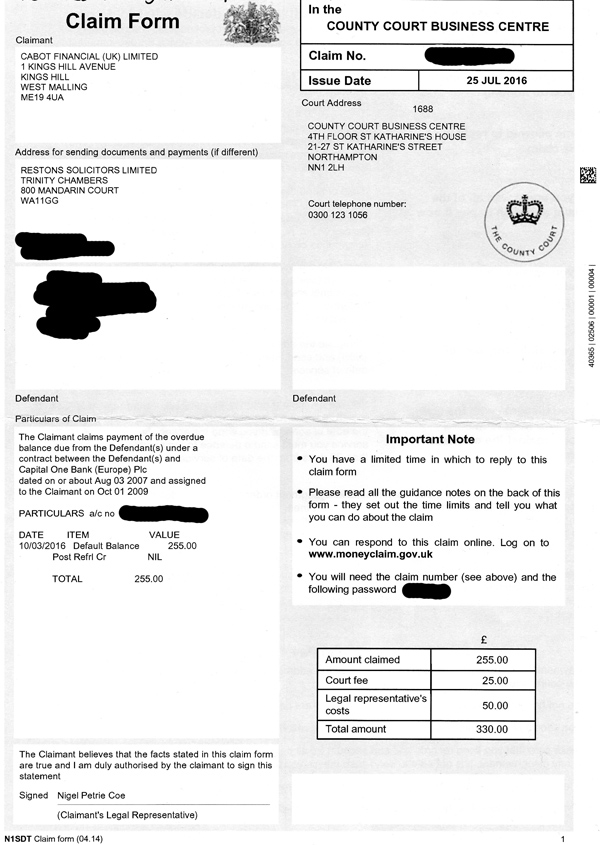

Hi there, Thanks for reading. I'm new to the forum, and hoping I may be able to find a little help with my current situation. I'm in a bit of a tangle!. Essentially I received an N1SDT CCJ claim form in the mail, too late to reply, and subsequently received a CCJ. I believe the debt to be statute barred, and intent to have it set aside if possible. I'm currently trying to claw my way out of long term unemployment by starting a small business (via the JSA/NEA scheme. I'm in the very early stages), so this is pretty awful timing. On the 18th of August I received a claim form dated 25th July. Obviously at that point it was too late to submit a seemingly simple defense, and the court ruled in favour of the claimant. I have received a 'Judgment for Claimant' notification, and correspondence from the claimant. The debt is from a capital one credit card dating back to August 2007, and was apparently 'assigned to the claimant' in Oct 2009 (this information is taken from the 'particulars of claim' section of the claim form that I received). I have no records of the debt, but have had no contact with anyone regarding the debt/account since the point were I stopped making payments (which I assume is 2007). I'm hoping that I can have this CCJ set aside, owing to the debt being statute barred. I'm currently claiming JSA, have no savings/additional income, live in my father's home, and I believe that I meet the requirements for a full remission of court fees, should I be able to go down that route. Though I'm not really sure how I go about doing that. Also I'm not entirely sure what kind of evidence I would have to supply. I have no records from the time, and assume I'll be needing them. Any advice with regards to my options at this point would be greatly appreciate. My understanding's pretty limited, and time is of the essence it seems. Thanks for any help.

Hi there, Thanks for reading. I'm new to the forum, and hoping I may be able to find a little help with my current situation. I'm in a bit of a tangle!. Essentially I received an N1SDT CCJ claim form in the mail, too late to reply, and subsequently received a CCJ. I believe the debt to be statute barred, and intent to have it set aside if possible. I'm currently trying to claw my way out of long term unemployment by starting a small business (via the JSA/NEA scheme. I'm in the very early stages), so this is pretty awful timing. On the 18th of August I received a claim form dated 25th July. Obviously at that point it was too late to submit a seemingly simple defense, and the court ruled in favour of the claimant. I have received a 'Judgment for Claimant' notification, and correspondence from the claimant. The debt is from a capital one credit card dating back to August 2007, and was apparently 'assigned to the claimant' in Oct 2009 (this information is taken from the 'particulars of claim' section of the claim form that I received). I have no records of the debt, but have had no contact with anyone regarding the debt/account since the point were I stopped making payments (which I assume is 2007). I'm hoping that I can have this CCJ set aside, owing to the debt being statute barred. I'm currently claiming JSA, have no savings/additional income, live in my father's home, and I believe that I meet the requirements for a full remission of court fees, should I be able to go down that route. Though I'm not really sure how I go about doing that. Also I'm not entirely sure what kind of evidence I would have to supply. I have no records from the time, and assume I'll be needing them. Any advice with regards to my options at this point would be greatly appreciate. My understanding's pretty limited, and time is of the essence it seems. Thanks for any help.

-

Vehicle Control Services issued a non- display of ticket 2 years ago by the evidence on an ANPR camera they then left it 14 months to start demanding money through the usual DRP/ZENITH and finally the bottom of the barrel B W Legal. They issued court proceedings when I refused to communicate with them as they had in my opinion broken data protection regulations in contacting me by telephone warning me what costs I could expect if going to court. I made the mistake of trying to fill in the court form online but on making a counter claim for intimidation the plea did not get entered so I received a court judgement in my absence. I applied to have the case set aside which I had found in my favour the judge was well in her words displeased with the conduct of B W Legal using unsolicited telephone calls to persuade people to pay up. I got a disapproval for not disclosing that I had in my possession the parking ticket, but in my defence I said that I was charged with not displaying and not non- payment. No costs were awarded to either party. I am now providing the court with the details of my case in case B W Legal wishes to continue the case or drop it (i expect they will drop it now they know I still have the ticket). The main issue I have is that they should not be issuing parking notices on the evidence of ANPR cameras only I asked for photographic evidence in the beginning but heard nothing I think they left it 14 months hoping I would not have the evidence to prove them wrong. Does anyone have an opinion on winning a case and maybe setting a legal precedent that ANPR cameras can't be used for evidence of not displaying a valid ticket without photographs for proof. This in my case shows that ANPR'S are flawed.

-

Hello I consented to a set aside I had against a company who didn't reply at all to the claim from 12/12/15. I understand that the claim will now go back to the beginning but I now need to amend my particulars. I need to know - 1 Will there be a new issue date for the claim, or does the original date of the issue of claim, 12/12/15, stand? 2 Due to the claim now going back to the beginning I need to amend my particulars as things have changed, will I have that opportunity or are my original particulars from 12/12/15 still valid? 3 If I have to apply to change my claim will I have to pay? 4 I gather that the other party can consent to my new particulars, do I need a consent order for this and draw one up and file with the court? Also paying a fee? Thanks in advance. Brenda

-

On form N244 there is a question (4) which asks "Have you attached a draft of the order you are applying for?" What is a draft order? Question 3 asks "What orders are you asking the court to make and why?" and I have written that I want the default judgement set aside and given the reasons I think it should be set aside. Does question 4 relate to this? Is it just a more in depth expansion of this or is it something completely different? I have searched on the internet and found conflicting answers to this. Some legal websites I have read say a draft order should be attached while others (e.g. NationalDebtline) say tick NO and leave it to the court to fill in. None of the websites actually explain what the draft order is though. I would greatly appreciate it if anyone can help. Thanks!

-

back in jan I received a cc claim from Cabot for a debt I had with Capital One i responded to the claim i did the income expenditure and admitted the 235 debt i owed but disputed the added solicitors fees etc .I contacted the court to see what was happening and was told the judgement had been set aside. Today nearly 6 months later I rec a letter from Mortimer clarke , which reads as follows we refer to the admission form filed in response to the claim form our client has considered your admission very carefully and is prepared to accept your part admission of 235 , from the figures provided however your total monthly income is 100 and expenditure is 100 as your expenditure is the same as your income they indicate that you may not be able to afford your proposed offer of payment of 5 pounds please confirm how you will be able to afford the propose offer in light of the above. if we do not receive a response within 14 days we are instructed to accept your offer and make an application to the court to enter judgement for the admitted amount payable by your proposed monthly installment of 5 pounds . alternatively if you confirm within 14 days that the offer is not affordable and sustainable by you we will refer this matter to our client for further instructions .if judgement is granted by the court we will write to you again with the judgement terms and ask you for further details of your financial circumstances so we can review if affordable for you any thought help advice please??

back in jan I received a cc claim from Cabot for a debt I had with Capital One i responded to the claim i did the income expenditure and admitted the 235 debt i owed but disputed the added solicitors fees etc .I contacted the court to see what was happening and was told the judgement had been set aside. Today nearly 6 months later I rec a letter from Mortimer clarke , which reads as follows we refer to the admission form filed in response to the claim form our client has considered your admission very carefully and is prepared to accept your part admission of 235 , from the figures provided however your total monthly income is 100 and expenditure is 100 as your expenditure is the same as your income they indicate that you may not be able to afford your proposed offer of payment of 5 pounds please confirm how you will be able to afford the propose offer in light of the above. if we do not receive a response within 14 days we are instructed to accept your offer and make an application to the court to enter judgement for the admitted amount payable by your proposed monthly installment of 5 pounds . alternatively if you confirm within 14 days that the offer is not affordable and sustainable by you we will refer this matter to our client for further instructions .if judgement is granted by the court we will write to you again with the judgement terms and ask you for further details of your financial circumstances so we can review if affordable for you any thought help advice please?? -

Does anyone know the bank details of Rossendales to set up the standing order, its the account number and sort code of Rossendales i need, its not clear on the website. Its because i have a bailiff coming in the morning and he said he will be taking goods. I have explained i am in terrible grief following the death of my partner, i explained i will not cope with the upset, i am in process of facing all the things i have not felt able, but i have a lot of unopened post so it wont be the only threatening letter. i need to be realistic an offer what i can. I want to set up a standing order to pay in installments the balance , first if i have proof i am repaying will it stop any seizure of goods. secondly i looked on website but cant find the account number and sort code of rossendales to set up standing order. I wondered if anyone else has managed to locate it

Does anyone know the bank details of Rossendales to set up the standing order, its the account number and sort code of Rossendales i need, its not clear on the website. Its because i have a bailiff coming in the morning and he said he will be taking goods. I have explained i am in terrible grief following the death of my partner, i explained i will not cope with the upset, i am in process of facing all the things i have not felt able, but i have a lot of unopened post so it wont be the only threatening letter. i need to be realistic an offer what i can. I want to set up a standing order to pay in installments the balance , first if i have proof i am repaying will it stop any seizure of goods. secondly i looked on website but cant find the account number and sort code of rossendales to set up standing order. I wondered if anyone else has managed to locate it -

Hi all I'm trying to get a court CCJ Judgement set aside. Essentially I am disputing the CCJ on the grounds that I had emigrated prior to the judgement being granted. 1. I disputed the debt and attempted to resolve this with the claimant. 2. Prior to emigrating from the UK I notified the claimant of my intention to emigrate and further agree settlement 3. After emigrating I confirmed I had left the country 4. They obtained a CCJ at my previous UK address 11 months after I emigrated 5. I never saw the summons 6. I discovered the CCJ 5 years later and now want it setting aside. I've completed form N244 including supporting evidence (visa stamps, new local driving licence, citizenship cert). Where do I send this and can someone confirm the costs? Also anyone been in a similar position and can offer some guidance on how they approached this? thanks Andy

-

Hi All, I've read lots of info on here but nothing that helps me for my specific case. I hope someone can throw their tuppance in! I have just found out that I have a CCJ in my name for a bill that I am not liable for. First thing I knew about it was when I checked my credit history. I am very distressed that this is on my credit history because I was hoping to get a mortgage in the next few months and this has completely messed up my credit score! The water bill at a place I now no longer live at is in arrears. I lived in the property as joint tenants with some friends from November 2013- March 2014. I moved out and they stayed on, amending the tenancy agreement and all the bills accordingly. I have loads of documents to demonstrate I moved out (council tax bill, tenancy agreements etc) the other tenants kept telling them I didn't live there but the water company refuse to change their records retrospectively. They quote a law which says we should have given 2 days notice which we did but it just wasn't recorded on their system. It's my word against theirs essentially. I had never received a summons or case judgement. Part of the money owed £85 was sent to a Debt Collection Agency and I've squared it with them. The DCA accept that I don't live there and put it on hold whilst they go back to the water company). However, I still have £600 debt in my name and this CCJ on my file. The other tenants maintain they didn't know about any of this but I can't 100% trust them on that. They said no post has come in my name but they didn't tell me my name was on the water bills they couldn't pay so I'm not convinced. However, the court document I got lists my recent address, and I assume they got this from the Electoral Roll, yet nothing turned up there either. Things I have done so far: • Scanned in Council Tax Bills and sent to water company (I've been told they won't take them into consideration). • Telephoned the water company to ask why the CCJ was issued in October 2015 in my name only. It was explained that they don't do joint claims and couldn't tell me why just that "it was policy to use the first name on the account" even though they had been dealing with the other names on the account. They told me that the other tenants had set up a payment plan which they missed a payment on, ignored the water companies calls and letters so the water company started court proceedings. • Written to the water company asking for copies of all correspondence. I plan to do a SAR/Data Protection request too. I have no idea of the exact dates, what payments have been made and when etc • Written to the court and asked for more info. I was told that the "claim pack cannot be reproduced" and they emailed me a scanned document with some basic details of the case. Not entirely sure what this document is but it lists the breakdown of costs and addresses of both parties. Anything else I should do? I know I need to get the application to Set Aside in ASAP but my partner is worried we'll lose and end up paying more money. I've explained that even if we pay it off it will still be on my history so I really need to fight it.

Hi All, I've read lots of info on here but nothing that helps me for my specific case. I hope someone can throw their tuppance in! I have just found out that I have a CCJ in my name for a bill that I am not liable for. First thing I knew about it was when I checked my credit history. I am very distressed that this is on my credit history because I was hoping to get a mortgage in the next few months and this has completely messed up my credit score! The water bill at a place I now no longer live at is in arrears. I lived in the property as joint tenants with some friends from November 2013- March 2014. I moved out and they stayed on, amending the tenancy agreement and all the bills accordingly. I have loads of documents to demonstrate I moved out (council tax bill, tenancy agreements etc) the other tenants kept telling them I didn't live there but the water company refuse to change their records retrospectively. They quote a law which says we should have given 2 days notice which we did but it just wasn't recorded on their system. It's my word against theirs essentially. I had never received a summons or case judgement. Part of the money owed £85 was sent to a Debt Collection Agency and I've squared it with them. The DCA accept that I don't live there and put it on hold whilst they go back to the water company). However, I still have £600 debt in my name and this CCJ on my file. The other tenants maintain they didn't know about any of this but I can't 100% trust them on that. They said no post has come in my name but they didn't tell me my name was on the water bills they couldn't pay so I'm not convinced. However, the court document I got lists my recent address, and I assume they got this from the Electoral Roll, yet nothing turned up there either. Things I have done so far: • Scanned in Council Tax Bills and sent to water company (I've been told they won't take them into consideration). • Telephoned the water company to ask why the CCJ was issued in October 2015 in my name only. It was explained that they don't do joint claims and couldn't tell me why just that "it was policy to use the first name on the account" even though they had been dealing with the other names on the account. They told me that the other tenants had set up a payment plan which they missed a payment on, ignored the water companies calls and letters so the water company started court proceedings. • Written to the water company asking for copies of all correspondence. I plan to do a SAR/Data Protection request too. I have no idea of the exact dates, what payments have been made and when etc • Written to the court and asked for more info. I was told that the "claim pack cannot be reproduced" and they emailed me a scanned document with some basic details of the case. Not entirely sure what this document is but it lists the breakdown of costs and addresses of both parties. Anything else I should do? I know I need to get the application to Set Aside in ASAP but my partner is worried we'll lose and end up paying more money. I've explained that even if we pay it off it will still be on my history so I really need to fight it. -

UK mobile networks look set to be forced to make it free to unlock phones at the end of customers' contracts, it was announced in The Budget. Currently, each major network offers different options to consumers who want their phone unlocked, with most charging for the privilege. Unlocking a phone allows customers to switch networks as they please. Following this week’s Budget, the government says that all mobile users should be able to have their handset unlocked at the end of their deal without paying. While it is hoping to get networks to sign up voluntarily, the government has promised to pass laws to force networks to comply if an agreement can’t be reached. http://www.uswitch.com/mobiles/news/2016/03/mobile-networks-set-to-be-forced-to-unlock-phones-for-free/?utm_campaign=insight&utm_content=160321&utm_medium=email&utm_source=uswitch&utm_term=mobiles-content-pod

UK mobile networks look set to be forced to make it free to unlock phones at the end of customers' contracts, it was announced in The Budget. Currently, each major network offers different options to consumers who want their phone unlocked, with most charging for the privilege. Unlocking a phone allows customers to switch networks as they please. Following this week’s Budget, the government says that all mobile users should be able to have their handset unlocked at the end of their deal without paying. While it is hoping to get networks to sign up voluntarily, the government has promised to pass laws to force networks to comply if an agreement can’t be reached. http://www.uswitch.com/mobiles/news/2016/03/mobile-networks-set-to-be-forced-to-unlock-phones-for-free/?utm_campaign=insight&utm_content=160321&utm_medium=email&utm_source=uswitch&utm_term=mobiles-content-pod -

Hi, I am new to this forum and new to legal terms and I am confused with what happened in court today. Someone please help me understand? Here is the story. I received an attachment of earnings order for a default judgement I knew nothing about. I enquired and found out that Lowell had applied to court a few months earlier and got the default judgement as I did not get any paperwork. Further, I had written them with CCA request but they never replied I thought that it is over and done with. I applied to local court to set aside the judgement with a witness statement and defence where I explained to court about their dirty tricks and made up evidence etc. I sent all of those documents to Lowell as well so that they could put their side of story in court. what I did not understand was that a day later, they wrote to me with a signed draft order accepting to set aside the default judgment, withdrawing their AoE order application, and paying me court fees, then asking the court for permission to reply to my defence I thought that was a trap I went to court the next day, where I thought that the case would have been heard and judge making a decision. that was not the case, and Lowell hired a local solicitor to put to court the things they said in their letter, judge said to me that was easy and struck out the judgement and AoE order, then set a date for next hearing. I am very confused have two questions; 1. Why the Lowell accepted to set aside judgement and AoE order? 2. Why the judge set another hearing to hear the case when he had already quashed the judgment? I hope someone could answer the above two question. Thanks

Hi, I am new to this forum and new to legal terms and I am confused with what happened in court today. Someone please help me understand? Here is the story. I received an attachment of earnings order for a default judgement I knew nothing about. I enquired and found out that Lowell had applied to court a few months earlier and got the default judgement as I did not get any paperwork. Further, I had written them with CCA request but they never replied I thought that it is over and done with. I applied to local court to set aside the judgement with a witness statement and defence where I explained to court about their dirty tricks and made up evidence etc. I sent all of those documents to Lowell as well so that they could put their side of story in court. what I did not understand was that a day later, they wrote to me with a signed draft order accepting to set aside the default judgment, withdrawing their AoE order application, and paying me court fees, then asking the court for permission to reply to my defence I thought that was a trap I went to court the next day, where I thought that the case would have been heard and judge making a decision. that was not the case, and Lowell hired a local solicitor to put to court the things they said in their letter, judge said to me that was easy and struck out the judgement and AoE order, then set a date for next hearing. I am very confused have two questions; 1. Why the Lowell accepted to set aside judgement and AoE order? 2. Why the judge set another hearing to hear the case when he had already quashed the judgment? I hope someone could answer the above two question. Thanks -

Hello I really need some advice. I have been given an eviction date from my mortgage lender as we are in arrears and have failed to keep to an agreement. This eviction is set for the 10th of March, we only received the notice a week and a bit ago. I have filed an N244 application to try and delay the eviction. I just don't know if it will be successful and as this hearing is set for the 8th it would be cutting it very fine. I have written in the N244 that due to my wife's medical condition we desperately need more time to find accommodation. She has an chronic back/spine condition and struggles to do normal day to day things and mobility can be an issue at times. She is also being treated for a heart issue and has to have her liver scanned at the end of March for a separate issue. We have approached the council and have been put on the list for "suitable housing" closer to our grown up Children.They need to help her when I am at work or working away. This all takes time! I have also asked if we can have time to sell the house ourselves but not sure if this will be allowed. Does anyone have experience of these hearing and if this could buy more time? I am totally lost............

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS