Showing results for tags 'house'.

-

Greetings All, Been a fan of the forum for several years and kudos to the site team and members for all the great resources on here. I'm hoping someone can profer some advice re an issue I'm having with the gentleman that purchased my house late November. As mentioned above completed the sale of my home late November 2016, prior to the sale the property was rented, although tenant moved out prior to completion and I am living with my partner. Problem is I indicated that fixtures and fittings were not included in the sale, i.e. beds, fridge, washing machine etc. I personally was awaiting the funds from completion to enable me move the leftover items straight to storage and shipment abroad as I am relocating.. Completion happened and I had to travel abroad immediately for a family issue and I immediately called the buyer who I had met and he told me he had collected spare keys from my estate agent and I should agree with him when I was ready to attend the property to remove my belongings. As I returned to the UK I made several call to said buyer and he ignored several calls and text and eventually agreed to grant me access on the 15th of December 2016 for proposed removal. When I arrived at the property I was given access by his builder for 5 mins but they claimed to have lost the shed keys where I also had items in. I was told to break the shed door by the builder but was hesitant to do so without new owners consent. I called said buyer as I exited the property and explained above to him and also reminded him that fittings, fridge , washing machine etc not included in the sale. Long and short of it is he has ignored and avoided my calls since that day and I have been unable to get any of my belongings. He answered my call once this week to tell me a tenant was to move in this week and he will call me re stuff in the shed but is being evasive re other stuff and trying to say I never collected them. Question please is what legal recourse I have and best suggestions in resolving this situation. I have tried to communicate with him civilly to no avail. Thank-you. Pete

-

Good afternoon, I've had a bit of an issue with Virgin Media which started out with what I assumed would be a simple and relatively easy house move / purchase in October this year (2016). N Both addresses have the same services installed, cable, telephone line - so it was intended to be a simple move out, move in - call to activate blah blah blah. First months bill came through (all the trimmings of the first bill, migration fee etc), however 23rd of October Virgin Media tried to bill me £53.69 on my old account via the old account's Direct Debit. It bounced due to my bank account being empty at the time, ! I called up the service desk and told them that I'd received a letter (to my new address might I point out) stating that the direct debit for £53.69 had bounced and that I was required to pay £53.69 immediatly. About two / three days later my old landlord had posted some bills for my old address that arrived from virgin media through my door. I checked the bill and low-and-behold it was the bill for £53.69. Whilst on the phone to the lovely lady that migrated my services service's, I had asked to be walked through the process of which one step is that they take the remaining balance from the old contract at the old address and add it onto the new contract for the new address - which I thought was ok as it meant I'll be paid up. with the above information I had received and empowered to not let this issue go any further - I rang their customer support desk and ended up being routed through VM's (Virgin Media's) Indian call center. The gentleman I spoke to was great, he looked through the issue and told me that I wasn't required to pay them a penny and that it was simply a mis-understanding or human error which could be rectified there and then. as any bewildered and incredibly happy customer does, I simply waited for him to say "Thank you for waiting Mr. Customer, I've fixed the issue on your account - your E-Billing portal should update within 24-48 hours." to which I replied with glee: "Brilliant, but am I going to receive any future letters regarding this?" to which he tells me not to worry as the issue is all sorted and that the outstanding balance had been rectified and to ignore any future correspondance. It's now the first week of November and I'm still seeing my old (what should be inactive) account on my E-Billing portal which should have been closed off by now, I decide to check it . I begin to fret slightly due to the fact that it's still reporting that I owe £53.69. I'm slightly confused, I call through to their customer service desk and once again I am routed through their indian call center. At this point I'm more upset than I was the first time I called, due to the fact that I was promised verbally that I would not have this balance any longer. I re-explain the issue and the situation, another gentleman glances over the account and comes to the same solution as the first that it was in fact human error and that he would also fix this mysterious balance of £53.69. I wait some more, the agent comes back and tells me that it's now fixed - having less faith than the last time I called I explain the situation and ask for something more promising than a verbal statement of that "it's now fixed, don't worry - you won't receive any more letters or bills" - to which he says that he can't - so I ask for a second time, "am I going to get any more letters", he responds in kind with "No Mr.Customer, you won't receive anymore letters after today" . So I leave it there. 13th of November and I get a bill for the old (not at all in-active) account stating that I owe them £53.69. At this point I'm begining to dispair due to the fact that this will have been the third call I would make to their customer service desk, in some form of attempt to rectify the issue. I end up being routed to VM's indian call center to a third gentleman to whom I end up explaining the situation to, he agress that this is a waste of time and that the previous two agents hadn't actually rectified the issue I'm told he will rectify the issue and that he'll raise a complaint relating to the human error surrounding how my move of services was handled as it appears it wasn't handled correctly. I'm then informed that he had rectified the issue and that I should hear back from the complaint within 10 working days , he then passes on a complaint reference number (which I've lost, along with the first bill that relates to this issue) and that I can ignore any further correspondance until I hear back from the complaint - so I cancel my old direct debit through my online banking portal. I wait 11 days, no written or verbal correspondance in relation to my issue at all but by this time I'd received yet another letter headed "we are sorry to hear you are leaving", reminding me that I still owe them £53.69. I once again check my E-Billing portal to find that the old account is still there and still reporting an outstanding balance of £53.69. I call to check on the status of my complaint and end up being routed to VM's call centre in Ireland. Again the lady I spoke to was fantastic, checking the issue told me that the issue was resolved so the complaint was closed and that there was no need to inform me of such. I mention that the issue has now spanned a total of 2 months, 2 bills, a letter stating that I was leaving, several phone calls and that the E-Billing portal was still reporting that I owe £53.69 . Doing her due dilligence, she decides to check the old (and rather overdue for closing) account - which resulted that she discovered that none of the three previous agents whom I had actually spoken to have done anything about and that's the reason why I "apparently" still owed money, and why my E-Billing portal was still showing that I owe £53.69. she decides to apply a "mis-applied billing correction" adjustment (a credit) to my account of £53.69, which I can see on the E-billing portal so I'm quite happy and she informs me that it will take up to 24 - 48 hours for the online portal to update. I ask if there's anyway that I could have it in writing that I would no longer receive any further correspondance from VM relating to the moneys that has been confirmed several times that I do not owe, and she says the best she can do is put it in an email. of which I'll post below: " H....! As we discussed on the phone tonight the balance on your old account of £53.69 at ADDRESS REMOVED has been cleared off now. I apologise for all this hassle you have had with this however I can no assure you that no letter will come out for this again. Kind regards Shiona Lachlan Virgin Media -------------------------------------------------------------------- Save Paper - Do you really need to print this e-mail? Visit virginmedia.com for more information, and more fun. This email and any attachments are or may be confidential and legally privileged and are sent solely for the attention of the addressee(s). Virgin Media will never ask for account or financial information via email. If you are in receipt of a suspicious email, please report to virginmedia.com/netreport If you have received this email in error, please delete it from your system: its use, disclosure or copying is unauthorised. Statements and opinions expressed in this email may not represent those of Virgin Media. Any representations or commitments in this email are subject to contract. Registered office: Media House, Bartley Wood Business Park, Hook, Hampshire, RG27 9UP Registered in England and Wales with number 2591237 " 22nd of December, I arrive home from work to find another letter from virgin media - this time it's a default notice. In a panic I ring up and get hold of a gentleman from the Irish customer service desk. Explained the issue in depth once again (plus the email that I received) and that it was starting to take the preverbial to a new level - of which he agreed, checked the account but had discovered that the previous agent from the Irish call center had actually mis-applied the "mis-applied billing correction" onto the wrong account. She in fact had credited my new account with £53.69 instead of the older account. he explains the situation and tells me that in order to actually "fix" the issue, he has to apply a credit to the old account and then debit the new account to rectify the mistake the previous agent had made - I agreed this was the best course of action and away he goes. However he sends me a screen shot of this correction, showing my account is now zeroed. He also then sends me yet another email stating the work he carried out and that I will not receive any further correspondance relating to this issue. This issue has now spanned a total of three months and I'm still in the same position as I was back in October, due to querying the outstanding balance on the E-Billing section for my old account yesterday only to discover yet another human error related issue - same issue so I'm not going to beat a dead horse any longer. Today I'm awaiting a call from a manager in the Irish call center, due to the fact this has gone on for so long and also the fact my issue has not actually been resolved in any of the last five phone calls I had made to the customer support desk over the last 3 months, including the last attempt on the 22nd of December. I'm at the point of giving up and cancelling my contract with VM not just because their E-Billing portal is an absolute joke, but because I'm currently dispairing at the fact that this has gone on for so long now and that I could be taken to court for their internal mess ups with no apprent sight of resolution. I've also been brushing up on the terms and conditions and will be demanding compensation for the stress this has put me under and the sheer amount of human error involved. If the users of this forum have any advice for me, it would be great if you can share it. You can reach me here, or by email which I think is in my profile. I'll also post updates to my situation after I've had the call with this "manager". Kindest regards,

Good afternoon, I've had a bit of an issue with Virgin Media which started out with what I assumed would be a simple and relatively easy house move / purchase in October this year (2016). N Both addresses have the same services installed, cable, telephone line - so it was intended to be a simple move out, move in - call to activate blah blah blah. First months bill came through (all the trimmings of the first bill, migration fee etc), however 23rd of October Virgin Media tried to bill me £53.69 on my old account via the old account's Direct Debit. It bounced due to my bank account being empty at the time, ! I called up the service desk and told them that I'd received a letter (to my new address might I point out) stating that the direct debit for £53.69 had bounced and that I was required to pay £53.69 immediatly. About two / three days later my old landlord had posted some bills for my old address that arrived from virgin media through my door. I checked the bill and low-and-behold it was the bill for £53.69. Whilst on the phone to the lovely lady that migrated my services service's, I had asked to be walked through the process of which one step is that they take the remaining balance from the old contract at the old address and add it onto the new contract for the new address - which I thought was ok as it meant I'll be paid up. with the above information I had received and empowered to not let this issue go any further - I rang their customer support desk and ended up being routed through VM's (Virgin Media's) Indian call center. The gentleman I spoke to was great, he looked through the issue and told me that I wasn't required to pay them a penny and that it was simply a mis-understanding or human error which could be rectified there and then. as any bewildered and incredibly happy customer does, I simply waited for him to say "Thank you for waiting Mr. Customer, I've fixed the issue on your account - your E-Billing portal should update within 24-48 hours." to which I replied with glee: "Brilliant, but am I going to receive any future letters regarding this?" to which he tells me not to worry as the issue is all sorted and that the outstanding balance had been rectified and to ignore any future correspondance. It's now the first week of November and I'm still seeing my old (what should be inactive) account on my E-Billing portal which should have been closed off by now, I decide to check it . I begin to fret slightly due to the fact that it's still reporting that I owe £53.69. I'm slightly confused, I call through to their customer service desk and once again I am routed through their indian call center. At this point I'm more upset than I was the first time I called, due to the fact that I was promised verbally that I would not have this balance any longer. I re-explain the issue and the situation, another gentleman glances over the account and comes to the same solution as the first that it was in fact human error and that he would also fix this mysterious balance of £53.69. I wait some more, the agent comes back and tells me that it's now fixed - having less faith than the last time I called I explain the situation and ask for something more promising than a verbal statement of that "it's now fixed, don't worry - you won't receive any more letters or bills" - to which he says that he can't - so I ask for a second time, "am I going to get any more letters", he responds in kind with "No Mr.Customer, you won't receive anymore letters after today" . So I leave it there. 13th of November and I get a bill for the old (not at all in-active) account stating that I owe them £53.69. At this point I'm begining to dispair due to the fact that this will have been the third call I would make to their customer service desk, in some form of attempt to rectify the issue. I end up being routed to VM's indian call center to a third gentleman to whom I end up explaining the situation to, he agress that this is a waste of time and that the previous two agents hadn't actually rectified the issue I'm told he will rectify the issue and that he'll raise a complaint relating to the human error surrounding how my move of services was handled as it appears it wasn't handled correctly. I'm then informed that he had rectified the issue and that I should hear back from the complaint within 10 working days , he then passes on a complaint reference number (which I've lost, along with the first bill that relates to this issue) and that I can ignore any further correspondance until I hear back from the complaint - so I cancel my old direct debit through my online banking portal. I wait 11 days, no written or verbal correspondance in relation to my issue at all but by this time I'd received yet another letter headed "we are sorry to hear you are leaving", reminding me that I still owe them £53.69. I once again check my E-Billing portal to find that the old account is still there and still reporting an outstanding balance of £53.69. I call to check on the status of my complaint and end up being routed to VM's call centre in Ireland. Again the lady I spoke to was fantastic, checking the issue told me that the issue was resolved so the complaint was closed and that there was no need to inform me of such. I mention that the issue has now spanned a total of 2 months, 2 bills, a letter stating that I was leaving, several phone calls and that the E-Billing portal was still reporting that I owe £53.69 . Doing her due dilligence, she decides to check the old (and rather overdue for closing) account - which resulted that she discovered that none of the three previous agents whom I had actually spoken to have done anything about and that's the reason why I "apparently" still owed money, and why my E-Billing portal was still showing that I owe £53.69. she decides to apply a "mis-applied billing correction" adjustment (a credit) to my account of £53.69, which I can see on the E-billing portal so I'm quite happy and she informs me that it will take up to 24 - 48 hours for the online portal to update. I ask if there's anyway that I could have it in writing that I would no longer receive any further correspondance from VM relating to the moneys that has been confirmed several times that I do not owe, and she says the best she can do is put it in an email. of which I'll post below: " H....! As we discussed on the phone tonight the balance on your old account of £53.69 at ADDRESS REMOVED has been cleared off now. I apologise for all this hassle you have had with this however I can no assure you that no letter will come out for this again. Kind regards Shiona Lachlan Virgin Media -------------------------------------------------------------------- Save Paper - Do you really need to print this e-mail? Visit virginmedia.com for more information, and more fun. This email and any attachments are or may be confidential and legally privileged and are sent solely for the attention of the addressee(s). Virgin Media will never ask for account or financial information via email. If you are in receipt of a suspicious email, please report to virginmedia.com/netreport If you have received this email in error, please delete it from your system: its use, disclosure or copying is unauthorised. Statements and opinions expressed in this email may not represent those of Virgin Media. Any representations or commitments in this email are subject to contract. Registered office: Media House, Bartley Wood Business Park, Hook, Hampshire, RG27 9UP Registered in England and Wales with number 2591237 " 22nd of December, I arrive home from work to find another letter from virgin media - this time it's a default notice. In a panic I ring up and get hold of a gentleman from the Irish customer service desk. Explained the issue in depth once again (plus the email that I received) and that it was starting to take the preverbial to a new level - of which he agreed, checked the account but had discovered that the previous agent from the Irish call center had actually mis-applied the "mis-applied billing correction" onto the wrong account. She in fact had credited my new account with £53.69 instead of the older account. he explains the situation and tells me that in order to actually "fix" the issue, he has to apply a credit to the old account and then debit the new account to rectify the mistake the previous agent had made - I agreed this was the best course of action and away he goes. However he sends me a screen shot of this correction, showing my account is now zeroed. He also then sends me yet another email stating the work he carried out and that I will not receive any further correspondance relating to this issue. This issue has now spanned a total of three months and I'm still in the same position as I was back in October, due to querying the outstanding balance on the E-Billing section for my old account yesterday only to discover yet another human error related issue - same issue so I'm not going to beat a dead horse any longer. Today I'm awaiting a call from a manager in the Irish call center, due to the fact this has gone on for so long and also the fact my issue has not actually been resolved in any of the last five phone calls I had made to the customer support desk over the last 3 months, including the last attempt on the 22nd of December. I'm at the point of giving up and cancelling my contract with VM not just because their E-Billing portal is an absolute joke, but because I'm currently dispairing at the fact that this has gone on for so long now and that I could be taken to court for their internal mess ups with no apprent sight of resolution. I've also been brushing up on the terms and conditions and will be demanding compensation for the stress this has put me under and the sheer amount of human error involved. If the users of this forum have any advice for me, it would be great if you can share it. You can reach me here, or by email which I think is in my profile. I'll also post updates to my situation after I've had the call with this "manager". Kindest regards, -

I have a charge order placed on my house by Bristol & Wessex Water for £1800. They recently sent me a letter stating that if I don't pay the full amount they will be taking legal action and apply for an order for sale. I then will be sent an order to vacate my property within 28 days. My house is owned outright with no mortgage and currently valued around £200K. I am living on a small private pension with no chance of paying back the debt. I went to the CAB who told me that I will end up homeless and living on the streets as there is no social housing available for single men. The Water company placed a CCJ on my credit record so it's impossible for me to borrow money to pay back the debt and keep my house. I could never understand why there were homeless people on the streets, but I do now. I will be joining them soon. What an idiot I was buying a house. If I had a council house I would have nothing to worry about and a safe roof over my head. I know a chap near here who lives in a housing association bungalow. He owes banks £73k and will not end up homeless. Comments welcome.

I have a charge order placed on my house by Bristol & Wessex Water for £1800. They recently sent me a letter stating that if I don't pay the full amount they will be taking legal action and apply for an order for sale. I then will be sent an order to vacate my property within 28 days. My house is owned outright with no mortgage and currently valued around £200K. I am living on a small private pension with no chance of paying back the debt. I went to the CAB who told me that I will end up homeless and living on the streets as there is no social housing available for single men. The Water company placed a CCJ on my credit record so it's impossible for me to borrow money to pay back the debt and keep my house. I could never understand why there were homeless people on the streets, but I do now. I will be joining them soon. What an idiot I was buying a house. If I had a council house I would have nothing to worry about and a safe roof over my head. I know a chap near here who lives in a housing association bungalow. He owes banks £73k and will not end up homeless. Comments welcome. -

Its a first post I'll be brief. One year left on mortgage. trouble with payments, only £7000 left to pay and will be paid off next year. Santander want to threaten me with litigation and take me to court. I was forced to take early retirement couple of years ago due to cancer. Any advice? going through the usual channels RE debt advice, expenditure etc cheers guys Meicimac

-

Hi, We recently moved house and new property did not have and working landline. Previous supplier was Virgin Media but that was cancelled by the previous occupier's family. When I looked to transfer from my current home the website said I would have to pay a new connection charge for engineer etc. As BT couldn't provide the service I arranged for Sky to provide phone line and Broadband as part of my existing TV package, BT however want to charge £169.75 early termination of contract fee and a separate charge of £31 for "cessation of broadband." My question is simple, are they entitled to make these charges as I moved house to a residence that did nnot have a supply.. Surely the contract was broken. Any advice would be gratefully received how to avoid these charges Thank You Trojan

Hi, We recently moved house and new property did not have and working landline. Previous supplier was Virgin Media but that was cancelled by the previous occupier's family. When I looked to transfer from my current home the website said I would have to pay a new connection charge for engineer etc. As BT couldn't provide the service I arranged for Sky to provide phone line and Broadband as part of my existing TV package, BT however want to charge £169.75 early termination of contract fee and a separate charge of £31 for "cessation of broadband." My question is simple, are they entitled to make these charges as I moved house to a residence that did nnot have a supply.. Surely the contract was broken. Any advice would be gratefully received how to avoid these charges Thank You Trojan -

Hi, long time since I have been on so hope I have put this in the correct place. I am taking two large loans from a friend and family, to clear some business issues, both of which need to be secured on my property. Lawyers are asking ridiculous sums for agreements and posting the charges. A full legal charge appears to be too complicated and time consuming for my needs so I am proposing equitable charges which should suffice. My question is, what forms do I need to submit to the land registry and can this be backed by a simple loan agreement between lender and borrower? Would there be templates on the site for loan agreement and charge as I cannot seem to find them myself? The loan agreement I can find online if necessary, it is the charge details that I do not have. Many thanks for any input. r

Hi, long time since I have been on so hope I have put this in the correct place. I am taking two large loans from a friend and family, to clear some business issues, both of which need to be secured on my property. Lawyers are asking ridiculous sums for agreements and posting the charges. A full legal charge appears to be too complicated and time consuming for my needs so I am proposing equitable charges which should suffice. My question is, what forms do I need to submit to the land registry and can this be backed by a simple loan agreement between lender and borrower? Would there be templates on the site for loan agreement and charge as I cannot seem to find them myself? The loan agreement I can find online if necessary, it is the charge details that I do not have. Many thanks for any input. r -

A first post, so hello. My home was repossessed six months ago and the estate agent’s website shows a notice saying Mortgagees in possession are now in receipt of an offer for the sum of £240,000 for [property]. Anyone wishing to place an offer on the property should contact [Estate agent’s details] before exchange of contracts or within the next 7 days whichever is sooner. This replaced a previous notice, first seen on 29 September 2016, specifying 28 days instead of the current ‘7 days’. What does this notice mean? Does it actually mean that a sale is proceeding but contracts haven’t yet been exchanged? The house isn’t advertised ‘Sold subject to contract’. I think this notice is meaningless as it doesn’t say when ‘the next 7 days’ runs from, it’s just an advertising gimmick. Isn’t the mortgage lender supposed to pay some attention to the defaulting mortgagor’s interests, and accept a reasonable offer? The asking price for the property is £250,000 so the offer, if it exists which I doubt, of £240,000 should be accepted. The outstanding loan is £65,000 and of course there will be costs for anything they think they can pile on. The agents refused to speak to me when I phoned to ask if a sale was proceeding. I’m housed by the Council and they can’t find out either. What are my legal rights in this situation? I made an appointment to see a solicitor in my local town but after going into their office and actually speaking to the man, I got the very definite impression that this new client (who also needs other services like a Will and executors of my estate as I don’t have family, and will pay for work done), wasn’t the kind of client they want. Any help would be very much appreciated. TIA. Ginger Mog

-

I don't know if this is the correct place to post. I have a linked detached house and it isn't in the best of repair. We had very high winds last week and some of the concrete pointing fell out (the wood on the fascias has rotted) onto my neighbours drive, luckily her car wasn't there but she has said if her car had have been damaged she would sue me. Can she do that? I haven't the money for new fascia but have had a roofer round to make it safe. I just wanted to know for future reference. Also my fence was blown down nearly so it is leaning but not blown over. She has told me I need to get it fixed immediately as she cannot weed her garden . Again does anyone know where I stand legally. Thanks for any help you can give me.

I don't know if this is the correct place to post. I have a linked detached house and it isn't in the best of repair. We had very high winds last week and some of the concrete pointing fell out (the wood on the fascias has rotted) onto my neighbours drive, luckily her car wasn't there but she has said if her car had have been damaged she would sue me. Can she do that? I haven't the money for new fascia but have had a roofer round to make it safe. I just wanted to know for future reference. Also my fence was blown down nearly so it is leaning but not blown over. She has told me I need to get it fixed immediately as she cannot weed her garden . Again does anyone know where I stand legally. Thanks for any help you can give me. -

There is a tree on the side of a path runs past my house that is overgrown to the point it is coming into contact with the side of my house, the roof and is also hitting the windows of my property. I have contacted the council about this previously in 2011 when it was dealt with by way of a crown reduction, however 4 years later and its bigger than so i again reported it last summer and was advised that it would be cut back in 6/8 weeks. However 16 months have passed since my local borough council made that promise and despite several calls and emails nothing has been done about it and today i received an email from my local county council telling me that they were going to do nothing more about it. Would appreciate any advice, if there is anything i've left out that i should have included please let me know and i'll update. Thanks

There is a tree on the side of a path runs past my house that is overgrown to the point it is coming into contact with the side of my house, the roof and is also hitting the windows of my property. I have contacted the council about this previously in 2011 when it was dealt with by way of a crown reduction, however 4 years later and its bigger than so i again reported it last summer and was advised that it would be cut back in 6/8 weeks. However 16 months have passed since my local borough council made that promise and despite several calls and emails nothing has been done about it and today i received an email from my local county council telling me that they were going to do nothing more about it. Would appreciate any advice, if there is anything i've left out that i should have included please let me know and i'll update. Thanks -

I sold my mothers house in January this year. The buyer is now suing me for misrepresentation. Immediately prior to completion, the buyer noticed that there was a fault with the heating. I offered to have it repaired but this was refused and the buyer demanded £2000 off the purchase price which I declined on the basis that the buyer had refused my offer to have it fixed. I have now received court claim papers. When i signed the property information form the heating was Ok and i stated this on the form. The heating was later turned off for the summer. As the purchase took almost a year, I was asked later to confirm that the information form remained current and I confirmed this as I was not aware of any changes. There is no doubt that at completion there was a fault with the heating though when it stopped working is not known. It was working when I signed the form but by completion it had stopped. the buyer did not undertake any surveys. I have tried to negotiate and I have offered £1000 in settlement without admitting liability, but this has been refused. I attach the particulars of claim and my proposed response and I would welcome any comments. Thank you. response to claim form.pdf Particulars of Claim.pdf

-

I would welcome some suggestions from Forum Members please as to what I should with regards to a landlord who is taking her time in restoring central heating in the house which I am renting. I have been without heating now for a week. Prior to this, the boiler had broken down a number of times and the landlord was told by two of the engineers that the boiler was obsolete and needed replacing. I have been in touch with the LL and made the point that the situation is becoming untenable, but all I got back was that she is dealing with the matter. I would be grateful for some suggestions about what options are available to me so that I can use some leverage to get the LL to act and act urgently? I hope members can help. Many thanks in advance. Mack

I would welcome some suggestions from Forum Members please as to what I should with regards to a landlord who is taking her time in restoring central heating in the house which I am renting. I have been without heating now for a week. Prior to this, the boiler had broken down a number of times and the landlord was told by two of the engineers that the boiler was obsolete and needed replacing. I have been in touch with the LL and made the point that the situation is becoming untenable, but all I got back was that she is dealing with the matter. I would be grateful for some suggestions about what options are available to me so that I can use some leverage to get the LL to act and act urgently? I hope members can help. Many thanks in advance. Mack -

Open House London is the capital's largest annual festival of architecture and design, taking place on 17 & 18 September 2016. Open House London is a truly citywide celebration of the buildings, places and spaces where we live and work. It provides a unique opportunity to see, explore and learn about Londonʼs amazing architecture and design over one weekend. With more than 750 buildings opening their doors this year, Open House Londonʼs selection will include beautifully designed residences, innovative infrastructure projects and prestigious civic buildings, alongside a programme of neighbourhood walks, engineering and landscape tours, cycle rides and expertsʼ talks – all for free. http://www.openhouselondon.org.uk/

Open House London is the capital's largest annual festival of architecture and design, taking place on 17 & 18 September 2016. Open House London is a truly citywide celebration of the buildings, places and spaces where we live and work. It provides a unique opportunity to see, explore and learn about Londonʼs amazing architecture and design over one weekend. With more than 750 buildings opening their doors this year, Open House Londonʼs selection will include beautifully designed residences, innovative infrastructure projects and prestigious civic buildings, alongside a programme of neighbourhood walks, engineering and landscape tours, cycle rides and expertsʼ talks – all for free. http://www.openhouselondon.org.uk/ -

I have recently moved and my bank said BH rejected payment. I called first thing Monday morning to pay them and sort out address. Staff where just rude and said i had to pay £15 charge I cannot afford this and told them i want to pay what they didnt take sat. They are now asking for this weeks payment early too !!

I have recently moved and my bank said BH rejected payment. I called first thing Monday morning to pay them and sort out address. Staff where just rude and said i had to pay £15 charge I cannot afford this and told them i want to pay what they didnt take sat. They are now asking for this weeks payment early too !! -

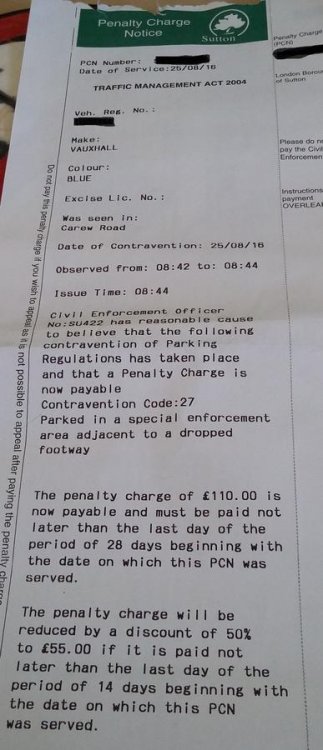

I received the following PCN outside my house and want to appeal as my car was not blocking the dropped part of the footway. I was in a hurry when I left yesteray morning so I didn't take a picture of the side of the car from the road which would have clearly shown it was not blocking it. heres the PCN And now a couple of the enforcement pics - note there is none showing the side of the car from the drivers side as this would clearly show no blocking In the bottom pic you can see the other enforcement officer in the background smiling - not very professional! Now my pic showing with the car and then without so you can see the full kerb. If you look at the amazon box you can follow the line to see my car is not blocking it. I need help with wording the appeal. You unfortunately cannot see my house on google streetmap. I have an 8 month old and suffer with sciatica and have my own private space at the back of the house. I only use the front when i am on my own as it is less to walk to get her out of the car. Needless to say i dont think i really need to use any of this as i have not committed any offence. Yes if i was over the stones in the road or blocking the dropped kerb then I would pay up. they got me once before on this further down the road in another car so i really am cautious about parking on the road .

I received the following PCN outside my house and want to appeal as my car was not blocking the dropped part of the footway. I was in a hurry when I left yesteray morning so I didn't take a picture of the side of the car from the road which would have clearly shown it was not blocking it. heres the PCN And now a couple of the enforcement pics - note there is none showing the side of the car from the drivers side as this would clearly show no blocking In the bottom pic you can see the other enforcement officer in the background smiling - not very professional! Now my pic showing with the car and then without so you can see the full kerb. If you look at the amazon box you can follow the line to see my car is not blocking it. I need help with wording the appeal. You unfortunately cannot see my house on google streetmap. I have an 8 month old and suffer with sciatica and have my own private space at the back of the house. I only use the front when i am on my own as it is less to walk to get her out of the car. Needless to say i dont think i really need to use any of this as i have not committed any offence. Yes if i was over the stones in the road or blocking the dropped kerb then I would pay up. they got me once before on this further down the road in another car so i really am cautious about parking on the road .

-

Hi there, Just wondering if anyone can help. We moved into our previous house in 2011. We paid a management company each year for the communal service charge as instructed. Not an issue. However, when we were in the process of selling in 2015, our solicitor found that the accounts for the previous four years had not been completed and filed by the management company. We were advised that our buyers wanted to hold a retainer of £200 in case of an underpayment, which we agreed to. Just before we exchanged contracts, the management company emailed to advise that for the first year (2011-2012), we had actually OVERPAID them by £144.45. Following this, we emailed them the following: ----------------------------------------------- From: ***** Sent: 08 June 2015 18:08 To: ***** Subject: Ref ****** Good afternoon ****, I have received communication from you regarding a credit to my account for the period 06/07/2011 - 30/06/2012 to the value of £144.45. As the charges for each year are paid in advance, I would not like this credit applied to any future bill, instead I would like to receive the amount direct to myself in form of a cheque or bank transfer, due to the fact that I have sold the above property and will be moving at the end of this month. Please can you confirm that this will be actioned as per my request, and the same applied to any further credits that may be due for any charges up until 30th June 2015. I look forward to hearing from you. I can be contacted via this email or on the mobile number below. Regards ****** ------------------------------------------------------ The management company then replied with the following stating that once ALL years accounts were finalised, they would return any overpayments to us: On Tuesday, 16 June 2015, *********** wrote: Good Morning Thank you for your email I note your below instruction however at this stage the credit it unable to be returned to yourself. Any overall credits can of course be returned to yourself following the production of all outstanding accounts. Kind regards **********- MIRPM AssocRICS Acting Branch Manager, Estate Management ------------------------------------------------- We have since been advised by our solicitor that the overpayments are for the following amounts: 2011-2012 - £144.45 2012-2013 - £185.41 2013-2014 - £110.83 2014-2015 - £83.80 Total overpaid - £524.49 However, the management company have gone against what they have agreed to and credited the accounts, meaning the buyers have now had this money and they are refusing to refund us. Our solicitor has not been overly helpful and the management company have now said they won't speak to us as we are no longer the owners of the house. What rights do we have? Are we able to fight this in small claims? Any know how would be good. Thanks in advance.

Hi there, Just wondering if anyone can help. We moved into our previous house in 2011. We paid a management company each year for the communal service charge as instructed. Not an issue. However, when we were in the process of selling in 2015, our solicitor found that the accounts for the previous four years had not been completed and filed by the management company. We were advised that our buyers wanted to hold a retainer of £200 in case of an underpayment, which we agreed to. Just before we exchanged contracts, the management company emailed to advise that for the first year (2011-2012), we had actually OVERPAID them by £144.45. Following this, we emailed them the following: ----------------------------------------------- From: ***** Sent: 08 June 2015 18:08 To: ***** Subject: Ref ****** Good afternoon ****, I have received communication from you regarding a credit to my account for the period 06/07/2011 - 30/06/2012 to the value of £144.45. As the charges for each year are paid in advance, I would not like this credit applied to any future bill, instead I would like to receive the amount direct to myself in form of a cheque or bank transfer, due to the fact that I have sold the above property and will be moving at the end of this month. Please can you confirm that this will be actioned as per my request, and the same applied to any further credits that may be due for any charges up until 30th June 2015. I look forward to hearing from you. I can be contacted via this email or on the mobile number below. Regards ****** ------------------------------------------------------ The management company then replied with the following stating that once ALL years accounts were finalised, they would return any overpayments to us: On Tuesday, 16 June 2015, *********** wrote: Good Morning Thank you for your email I note your below instruction however at this stage the credit it unable to be returned to yourself. Any overall credits can of course be returned to yourself following the production of all outstanding accounts. Kind regards **********- MIRPM AssocRICS Acting Branch Manager, Estate Management ------------------------------------------------- We have since been advised by our solicitor that the overpayments are for the following amounts: 2011-2012 - £144.45 2012-2013 - £185.41 2013-2014 - £110.83 2014-2015 - £83.80 Total overpaid - £524.49 However, the management company have gone against what they have agreed to and credited the accounts, meaning the buyers have now had this money and they are refusing to refund us. Our solicitor has not been overly helpful and the management company have now said they won't speak to us as we are no longer the owners of the house. What rights do we have? Are we able to fight this in small claims? Any know how would be good. Thanks in advance. -

Hi, I have two or three charges on my home as a result of unsecured (credit card) debt from about 10 years ago. These charges do not appear on my credit report as they are over 6 years old. However, if I try to sell my home, can the creditors (who are all debt purchasing companies and who all bought the debtor account for pennies on the pound and then turned it into a secured charge through a CCJ) impose the charge and block the sale of the property unless I pay them the full sum of the old debt? I'd really like to know where I stand on this , as I have my mum's care home bills to pay as well as my own living expenses. Thanks.

-

There is this bunch of local kids around the ages of 6-7 years, definitely not more than 8 years playing very very noisy football right next to our house. All sorts of swearwords flying around between themselves as they play and they kicking the football into big metal garage doors (they use that as the goal). It is a huge bang at every 'goal' (every minute) and they do this for about 2 hours on most evenings from 7pm till 9pm and on weekends in good weather also on bank holidays and any other school holiday times when they go on for even 5 or 6 hours. It is insane! The position of our house is on a corner where 2 streets meet and these metal garage doors are located at the end of our garden. The houses of other residents located past these garage doors and I guess that is enough distance for them not having to 'enjoy' the racket these boys make. As far as I'm aware kids of that age are not even supposed to be let out from home without adult supervision. Been in touch with police on the 101 phone number. First time 3 months ago they were very helpful, they asked a lot of details and came out in 1 hour to deal with the kids. The boys obviously tried to do a runner but I think the police did manage to speak to 1 or 2 of them.... The kids started coming here again a few weeks ago and now their numbers are growing (last night 6 of them) and in line with that the number of loud bangs we have to suffer grows too as well as the general kids' shouting noise. They play on the road and there are garage doors on either side of the road so they just kicking the football around right on the road and kicking it into these metal doors on either side. This is a quiet residential area with not much traffic - moreover there is a park 5 minutes from here! The football obviously often lands in our garden (at least 3 times a week) and they just climb up our fence from the street, sometimes by pulling to the fence an object they find nearby as people do flytip on this particular street corner and the kids just come into our garden to look for their football. The football also goes into other people's sheds that is next to these garages and those only got wooden doors with a padlock locking it down but with large enough gaps under and above. These belong to residents in other streets nearby. The kids do climb in there too to retrieve the ball and been causing more than a little damage to the some of these shed doors. Last night I got home from work at 8pm only to find that 1 of these boys is ramaging around in our garden whilst the other boy is sitting on the top of our fence giving him directions which way to look for the football. I've obviously told them off as this is not the first time nor the second. I've then called the police on 101 again. I got an answer from the officer that 'what exactly do you expect from the police to do about little boys playing football?' So not so helpful this time.... Tried to explain the case of trespassing and how much of a nuisance they are but the officer just shrugged me off and hung up. Have contacted my local council 3 months ago with this issue but they said it's not in their authority to act (I asked if they could put up here a No Ball Play Area sign) because it is a normal residential area and not a council housing. I know that reading this might sound like I'm just some grumpy, old hag who just doesn't like kids but that is totally not the case at all. In fact for a few weeks after the police talked to them, the kids only came here 1-2 times a week and did not kick the ball into the metal doors and that was absolutely fine. Just wondering that if this is not the council's authority to deal with and neither does the police care then where shall we turn to change the current situation? Social services....? By the way we did talk to these boys a lot before on a friendly way to convince them that it's not safe to play football on the road like this and please don't kick the metal doors with the ball but obviously they don't give a flying monkeys....They claim but it might as well just be a lie that their parents don't allow them to play football in the park because they don't think it's safe.... Park only 5mins walk from here!!!

There is this bunch of local kids around the ages of 6-7 years, definitely not more than 8 years playing very very noisy football right next to our house. All sorts of swearwords flying around between themselves as they play and they kicking the football into big metal garage doors (they use that as the goal). It is a huge bang at every 'goal' (every minute) and they do this for about 2 hours on most evenings from 7pm till 9pm and on weekends in good weather also on bank holidays and any other school holiday times when they go on for even 5 or 6 hours. It is insane! The position of our house is on a corner where 2 streets meet and these metal garage doors are located at the end of our garden. The houses of other residents located past these garage doors and I guess that is enough distance for them not having to 'enjoy' the racket these boys make. As far as I'm aware kids of that age are not even supposed to be let out from home without adult supervision. Been in touch with police on the 101 phone number. First time 3 months ago they were very helpful, they asked a lot of details and came out in 1 hour to deal with the kids. The boys obviously tried to do a runner but I think the police did manage to speak to 1 or 2 of them.... The kids started coming here again a few weeks ago and now their numbers are growing (last night 6 of them) and in line with that the number of loud bangs we have to suffer grows too as well as the general kids' shouting noise. They play on the road and there are garage doors on either side of the road so they just kicking the football around right on the road and kicking it into these metal doors on either side. This is a quiet residential area with not much traffic - moreover there is a park 5 minutes from here! The football obviously often lands in our garden (at least 3 times a week) and they just climb up our fence from the street, sometimes by pulling to the fence an object they find nearby as people do flytip on this particular street corner and the kids just come into our garden to look for their football. The football also goes into other people's sheds that is next to these garages and those only got wooden doors with a padlock locking it down but with large enough gaps under and above. These belong to residents in other streets nearby. The kids do climb in there too to retrieve the ball and been causing more than a little damage to the some of these shed doors. Last night I got home from work at 8pm only to find that 1 of these boys is ramaging around in our garden whilst the other boy is sitting on the top of our fence giving him directions which way to look for the football. I've obviously told them off as this is not the first time nor the second. I've then called the police on 101 again. I got an answer from the officer that 'what exactly do you expect from the police to do about little boys playing football?' So not so helpful this time.... Tried to explain the case of trespassing and how much of a nuisance they are but the officer just shrugged me off and hung up. Have contacted my local council 3 months ago with this issue but they said it's not in their authority to act (I asked if they could put up here a No Ball Play Area sign) because it is a normal residential area and not a council housing. I know that reading this might sound like I'm just some grumpy, old hag who just doesn't like kids but that is totally not the case at all. In fact for a few weeks after the police talked to them, the kids only came here 1-2 times a week and did not kick the ball into the metal doors and that was absolutely fine. Just wondering that if this is not the council's authority to deal with and neither does the police care then where shall we turn to change the current situation? Social services....? By the way we did talk to these boys a lot before on a friendly way to convince them that it's not safe to play football on the road like this and please don't kick the metal doors with the ball but obviously they don't give a flying monkeys....They claim but it might as well just be a lie that their parents don't allow them to play football in the park because they don't think it's safe.... Park only 5mins walk from here!!! -

Hello, I am not familiar with the current legislation regarding payday loans so advice on a letter structure would be appreciated. Background: A few years ago now I was a compulsive gambler and borrowed from any lender that would give me the cash . I managed to rack up £50k's of debt and at the time didn't have a secure job. Two years ago after a lot of hard work on myself, help from family and a years worth of councelling, I have not gambled, I've got a permanent job paying a decentish wage , I've paid off nearly all my debts. one of those who I hadn't yet paid was from a company named wageday advance for£650. They have since I ignored their threatening letters passed it onto Moorcroft who wrote me a lovely letter saying they will come to visit me at my house in the near future for a chat about it. firstly I have absolutely no desire at all to chat to them about it in my house. Is there a template to say I do not want them to come to my house? Secondly. They mention a reduced offer as settlement, but didn't say an amount. Now, I have been on a quest to be debt free since I stopped gambling, and paid back the main people. But I guess I left the payday loans to last simply because I do have quite an angst against them - they do prey on the vulnerable soley for profit and to the severe detriment of the borroweer. Don't get me wrong, I take full responsibility for my debts and what I did and have paid some VERY heavy prices - however, lending at whatever it was 3000%+ without doing any checks to someone who is essentially not well is in my mind criminal! However, my mind doesn't really come into play here, it's what the law says that counts. Is there any legislation about responsible lending that these companies should have adhered too? Can you even fight them on these grounds? What would be a reasonable lump sum final offer for a £650 debt? If I did just want to get rid of it? Thank you so much for reading.

Hello, I am not familiar with the current legislation regarding payday loans so advice on a letter structure would be appreciated. Background: A few years ago now I was a compulsive gambler and borrowed from any lender that would give me the cash . I managed to rack up £50k's of debt and at the time didn't have a secure job. Two years ago after a lot of hard work on myself, help from family and a years worth of councelling, I have not gambled, I've got a permanent job paying a decentish wage , I've paid off nearly all my debts. one of those who I hadn't yet paid was from a company named wageday advance for£650. They have since I ignored their threatening letters passed it onto Moorcroft who wrote me a lovely letter saying they will come to visit me at my house in the near future for a chat about it. firstly I have absolutely no desire at all to chat to them about it in my house. Is there a template to say I do not want them to come to my house? Secondly. They mention a reduced offer as settlement, but didn't say an amount. Now, I have been on a quest to be debt free since I stopped gambling, and paid back the main people. But I guess I left the payday loans to last simply because I do have quite an angst against them - they do prey on the vulnerable soley for profit and to the severe detriment of the borroweer. Don't get me wrong, I take full responsibility for my debts and what I did and have paid some VERY heavy prices - however, lending at whatever it was 3000%+ without doing any checks to someone who is essentially not well is in my mind criminal! However, my mind doesn't really come into play here, it's what the law says that counts. Is there any legislation about responsible lending that these companies should have adhered too? Can you even fight them on these grounds? What would be a reasonable lump sum final offer for a £650 debt? If I did just want to get rid of it? Thank you so much for reading. -

Hi I am having some issues with Virgin Media and would appreciate some advice. I took out a contract with VM in February of this year when we moved house into rented property. It was an 18 month contract for phone and broadband only. Then in July we were given the opportunity to purchase a property on a government scheme in a new housing development which we did. I had hoped to transfer the contract over but VM said they couldn't supply me in the new property so I would have to cancel the contract but they would charge me £240 for the pleasure of doing that (the remaining months on the contract) I felt this was unfair as they can't supply me and I would have taken the service with me. I also have heard they turned down the option to install cables to the estate which would have allowed them to supply me. I cancelled the contract, cancelled my direct debit and wrote to their complaints department. To which I got a letter addressed to my new address informing me they only agree to supply the property at start of contract not the person therefore I have to pay up. I still don't think this right and refused to pay. I sent the equipment back. Then I didn't hear anything from then for a month. Yesterday I get a call from debt collection company saying they are chasing the outstanding fee. I am told the VM have written to me a number times but turns out these letters went to my old address as that's all they have on record. That isn't the case as they have written to me in current property. They also have my email address they could have written to me at but didn't. Generally I am fed up with VM and won't be going back even if they can supply me in the future. I would like some advice on where to complain to next, on what grounds and if I have a case. I was thinking that they can only charge me to cover their losses not a loss of income. The term in the T&CS sounds like a penalty clause which isn't enforceable in court. Mike

-

Hi, would appreciate advice/comments on my situation. I have lived in the USA for over 3 years and have no plans to return to the UK (except for holidays). I own a house in the UK that has mostly been rented out but this year I have attempted to sell it - 5 months ago I accepted an offer and its been a long an protracted sale but I thought it was going to finally complete but have now been told that my buyer has been refused insurance due to the properties flooding history (last flooded in 2007!). Now I am faced with the very real possibility that I stand no chance of selling the house - yes I could rent it again, but will surely be faced with the same issues in the future and I thoroughly dislike renting long distance. There is a little equity in the property but that is meaningless with no prospect of selling it. What would happen if I just walked away from it, considering I do not live there and have no intention of returning permanently? Thanks.

Hi, would appreciate advice/comments on my situation. I have lived in the USA for over 3 years and have no plans to return to the UK (except for holidays). I own a house in the UK that has mostly been rented out but this year I have attempted to sell it - 5 months ago I accepted an offer and its been a long an protracted sale but I thought it was going to finally complete but have now been told that my buyer has been refused insurance due to the properties flooding history (last flooded in 2007!). Now I am faced with the very real possibility that I stand no chance of selling the house - yes I could rent it again, but will surely be faced with the same issues in the future and I thoroughly dislike renting long distance. There is a little equity in the property but that is meaningless with no prospect of selling it. What would happen if I just walked away from it, considering I do not live there and have no intention of returning permanently? Thanks. -

Big stink in the US house http://edition.cnn.com/2016/06/02/politics/paul-ryan-endorses-donald-trump/ Steven Hawking says its 'really bad man' http://www.newyorker.com/humor/borowitz-report/stephen-hawking-angers-trump-supporters-with-baffling-array-of-long-words

Big stink in the US house http://edition.cnn.com/2016/06/02/politics/paul-ryan-endorses-donald-trump/ Steven Hawking says its 'really bad man' http://www.newyorker.com/humor/borowitz-report/stephen-hawking-angers-trump-supporters-with-baffling-array-of-long-words -

Hi all, a bit more than a month ago I received a 2 year old PCN from southwark that I had completely forgotten about. I noticed the letter had no house/door number. It looked like one of the neighbours put it on the envelope in pencil and then delivered. I ignored it as I believe I don't think that it is enforcable without having officially delivered and having my full address on it? As far as I am concerned it could be someone else on the street. The post lady however knows ofcourse that it must be me and keeps dropping them with my other mail. I have received a CC a few weeks ago and finally yesterday the OFR. The first 2 letters I opened, but the OFR I have not opened. Am I right in thinking that writing undeliverable - no house number on the envelope and returning it will get me out of this, or at least they realise they cannot chance it any longer and have to enquire with the DVLA to get my full details? I don't even have the vehicle anymore, which is probably why they cannot get the details and just rely on a vague memory from a previous PCN? Any insights into address field legalities would be much appreciated as I cannot seem to find anything online about it.

Hi all, a bit more than a month ago I received a 2 year old PCN from southwark that I had completely forgotten about. I noticed the letter had no house/door number. It looked like one of the neighbours put it on the envelope in pencil and then delivered. I ignored it as I believe I don't think that it is enforcable without having officially delivered and having my full address on it? As far as I am concerned it could be someone else on the street. The post lady however knows ofcourse that it must be me and keeps dropping them with my other mail. I have received a CC a few weeks ago and finally yesterday the OFR. The first 2 letters I opened, but the OFR I have not opened. Am I right in thinking that writing undeliverable - no house number on the envelope and returning it will get me out of this, or at least they realise they cannot chance it any longer and have to enquire with the DVLA to get my full details? I don't even have the vehicle anymore, which is probably why they cannot get the details and just rely on a vague memory from a previous PCN? Any insights into address field legalities would be much appreciated as I cannot seem to find anything online about it. -

H i everyone and apologies if this is in the wrong section. Around June 2014 I completed an application to construct a single storey extension of (4.5 metres), extended the kitchen and making a shower room downstairs. The property also had a conservatory at the back but I was not sure if that was part of the original property so decided to complete the necessary forms and mentioned that the extension will start from the end of the kitchen and not from the end of the conservatory. Once everything was approved I had a building inspector come down to my property and it was he who advised that according to the house plans the conservatory is part of the original property so you can start the extension from the end of the conservatory. The extension has been completed, however not signed of by the building inspector as the shower room is not completed. Last week I had a letter from the planning enforcement officer and he said that your extension is 6.5 metre but we only allowed you to extend by 4.5 metre. I tried explaining that it was the building inspector that confirmed it was part of the original build. He wasn't having any of it and sent me a picture of the conservatory from 2014, which I guess was taken from the building inspector that came down. He said the colour of the bricks don't match so it's not part of the building. The building inspector that first visited us has left the council. He has given 2 options: either knock the building down by 2 metres or pay £385 for planning application but i think they are just trying to make money. I would really appreciate if someone can advise on what I should do

-

Hi all, I rent a house. My landlady has some issue with Npower an an outstanding amount. There was a letter, which I opened at her request, from last month saying they were going to have a hearing on a date now passed (but not when the letter was sent) to gain a warrant of entry to enter your home. I went out today and when I came back there was a gas pre-pay meter installed (outside) and a letter on the table inside. all the windows were closed and the doors were locked. I think they must have picked the lock on the front door. Is this legal? is there anything I can do about it? I am currently on ESA because of serious back issues, and receive housing benefit. as I say it was my landlady's debt, but I am renting the house. thanks in advance

Hi all, I rent a house. My landlady has some issue with Npower an an outstanding amount. There was a letter, which I opened at her request, from last month saying they were going to have a hearing on a date now passed (but not when the letter was sent) to gain a warrant of entry to enter your home. I went out today and when I came back there was a gas pre-pay meter installed (outside) and a letter on the table inside. all the windows were closed and the doors were locked. I think they must have picked the lock on the front door. Is this legal? is there anything I can do about it? I am currently on ESA because of serious back issues, and receive housing benefit. as I say it was my landlady's debt, but I am renting the house. thanks in advance -

.thumb.jpg.19cf2e6e72a613e714b8262daf620cf2.jpg) Im in Scotland. I have sold my house, the sale date is Fri 29th Apr. I asked my solicitor how soon i will get my money. They told me 5 working days. The money needs to clear blah blah, I can get it in 3 working days if the other solicitor agrees to use a different type of payment, which of course involves a fee. Does this sound normal. I desperately need this money to go and find myself accommodation. Im shocked why it takes so long. Can you guys advise please.

Im in Scotland. I have sold my house, the sale date is Fri 29th Apr. I asked my solicitor how soon i will get my money. They told me 5 working days. The money needs to clear blah blah, I can get it in 3 working days if the other solicitor agrees to use a different type of payment, which of course involves a fee. Does this sound normal. I desperately need this money to go and find myself accommodation. Im shocked why it takes so long. Can you guys advise please.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS