Showing results for tags 'fraudulent'.

-

I had a CC with RBS in the 2000s. I requested copies of the alleged agreement several times but to no avail. Last contact with RBS was in 2010 but confirmed to a DCA in 2014 that I had made several attempts to request copies of any such agreement and confirmed that no such evidence had been provided and for them to stop contacting me which they did. Then recently I receive a letter from another DCA stating the usual crap. I informed them any alleged debt is Stat Barred but they have written back stating it isnt stat barred. They allege the letter in 2014 was an acknowledgement of the debt but I have a copy and it certainly wasn't an acknowledgement of the debt merely confirmation that requests for alleged docs had been made. Anyone else had similar

-

Hello all, Recently I became a victim of fraud and I have been trying to reach out to all the right people in order to correct this. I purchased a brand new, still sealed mobile phone from what looked like a reputable seller on eBay. They had been on eBay for quite a few years selling all sorts of items with great feedback and not negatives. I received the mobile phone after paying using my CC and used it for 6 months as there were no issues until February this year. It had turned out the original owner had put the mobile phone on the global blacklist as I believe they're the only person (except the police) that can do this. I tried to get in contact with the seller and it had seemed they had deactivated their eBay account, which was strange since they had been a long term user of eBay. I'm reaching out to the eBay community for advice on this situation please. I have actioned the following so far: - My CC company won't issue a refund due to a third party handling the transaction (PayPal). There is a Consumer Credit Act 1974 (yes, this is a problem in this day and age) that apparently stops banks from issuing refunds. - eBay have said they wouldn't help and I needed to go to the payment handled. - PayPal have said they wouldn't help being it's outside their 180 day limit. I have sent the CEO a letter with all the evidence screenshotted. - I wrote a letter to the supplier of the mobile phone and report the fraudulent activity but I received a very unprofessional letter with no name or signature back. I am looking to send this to their CEO and ask if this is acceptable. - I logged a case with Action Fraud who tried to pass it to the National Fraud Agency and got told they literally don't have the time to check this case. - I am currently trying to work with the Financial Ombudsman Service to push my CC company into getting my money back. Short of me running about and trying to get either my mobile phone working (off the blacklist and the IMEI number moved to my account) or getting my money back, I am running out of ideas. I could try legal advice but if anyone has any kind of appropriate and helpful advice, I would be grateful. Kind regards, Mark

-

Hi, some weeks ago a letter from Eon reached my address addressed to a person who does not live there and liver lived there in the last 5 years, and wasn't the person who lived here before we moved in. Thank you for switching to EON, please send us your meter reading so we can complete the switch. Thinking nothing of it, I binned the letter. After that more letters from eon arrived, addressed to the occupier. Most I binned some I opened. They seemed very genuine, in the line of You won 1 million pounds please send us your personal details and some money so we can complete the transaction. More recently they were actual bills, reminding me to send my meter reading to my supplier which is not EON. It didn't work online. I tried it by phone and it didn't work. I called them on there service phone and the lady accepted my meter reading. A week later and I still didn't get a bill. Checked online and my meter reading wasn't there. Now I sent an e-mail to my supplier who confirmed that EON had falsely grabbed my account and switched it to them. (They still had all the data like meter point number and meter serial number because they were the supplier years ago before we switched to the new supplier). I checked the old bills, and the previous account number was different to the account number used for the new bills. I called EON and was put on hold most of the time for more than 10 minutes. Once I talked to someone, but I remember only because I didn't input the account number as asked. As soon as I gave him the account number I was put on hold. A mail from my current supplier confirmed they are working on the issue to solve it and it can take 6 months. Now letters from EON contain the bill for some time (£37), a threat of debt collectors, and threats of court orders, magistrates, warrants, etc. I'm afraid one morning a whole terror group of the police will smash in windows and doors, killing my orchid, only to have a look at my meter. When I checked the Internet, I found this practice of threatening The Occupier by utility companies is going on at least since 2004. Is there any party or MP or court or judge willing to put a stop to this fraudulent behaviour? Put the CEO and her whole board of directors into prison and throw away the key, something along this line. We had a similar issue with British Gas. After moving in to a new property, someone knocked, asked for the meter reading, and a week later I got a letter from British gas congratulating me to switch to them. Somehow I got the matter resolved in a very short time, probably involving trading standards, or calling BG and pulling the guy through the phone line. Can't remember. But this seems to me endemic considering all the links found here and other forums, and the Internet at large. Another question: If I go to court to stop the harassment by EON, how much would I need to pay to a lawyer?

Hi, some weeks ago a letter from Eon reached my address addressed to a person who does not live there and liver lived there in the last 5 years, and wasn't the person who lived here before we moved in. Thank you for switching to EON, please send us your meter reading so we can complete the switch. Thinking nothing of it, I binned the letter. After that more letters from eon arrived, addressed to the occupier. Most I binned some I opened. They seemed very genuine, in the line of You won 1 million pounds please send us your personal details and some money so we can complete the transaction. More recently they were actual bills, reminding me to send my meter reading to my supplier which is not EON. It didn't work online. I tried it by phone and it didn't work. I called them on there service phone and the lady accepted my meter reading. A week later and I still didn't get a bill. Checked online and my meter reading wasn't there. Now I sent an e-mail to my supplier who confirmed that EON had falsely grabbed my account and switched it to them. (They still had all the data like meter point number and meter serial number because they were the supplier years ago before we switched to the new supplier). I checked the old bills, and the previous account number was different to the account number used for the new bills. I called EON and was put on hold most of the time for more than 10 minutes. Once I talked to someone, but I remember only because I didn't input the account number as asked. As soon as I gave him the account number I was put on hold. A mail from my current supplier confirmed they are working on the issue to solve it and it can take 6 months. Now letters from EON contain the bill for some time (£37), a threat of debt collectors, and threats of court orders, magistrates, warrants, etc. I'm afraid one morning a whole terror group of the police will smash in windows and doors, killing my orchid, only to have a look at my meter. When I checked the Internet, I found this practice of threatening The Occupier by utility companies is going on at least since 2004. Is there any party or MP or court or judge willing to put a stop to this fraudulent behaviour? Put the CEO and her whole board of directors into prison and throw away the key, something along this line. We had a similar issue with British Gas. After moving in to a new property, someone knocked, asked for the meter reading, and a week later I got a letter from British gas congratulating me to switch to them. Somehow I got the matter resolved in a very short time, probably involving trading standards, or calling BG and pulling the guy through the phone line. Can't remember. But this seems to me endemic considering all the links found here and other forums, and the Internet at large. Another question: If I go to court to stop the harassment by EON, how much would I need to pay to a lawyer? -

Hi everyone I would really appreciate some advice on how to handle the following: My father, who is severely physically disabled and vulnerable, recently got a debt collection letter from Lowell alleging a £400 debt to three for a smartphone contract that was taken out over the phone. My father is computer illiterate and never took out this contract. It was likely taken out by his ex partner and carer in 2015. I have written to three with a subject access request but all they have provided me with is copies of bills. They say they do not have any recordings of phone conversations from the time the contract was entered into. I need to know from them: - What steps were taken to establish the identity of the person taking out the contract and protect my father from fraud? - What bank account details are associated with this account or was the account opened without any bank account details? - What date was the account opened? - Who signed for the delivery of the device and where was the device delivered? They have not yet provided me with any information. How can I go about proving that this debt is not my fathers? Is the onus on Lowell to prove this debt is his if we go to court? Can they prove this debt with only bills as evidence? My dad is very vulnerable and on a fixed income with lots of additional costs as he is currently moving into supported housing and has very complex health needs. He can not afford to pay this bill which is not his. Advice very much appreciated. Thank you Em

Hi everyone I would really appreciate some advice on how to handle the following: My father, who is severely physically disabled and vulnerable, recently got a debt collection letter from Lowell alleging a £400 debt to three for a smartphone contract that was taken out over the phone. My father is computer illiterate and never took out this contract. It was likely taken out by his ex partner and carer in 2015. I have written to three with a subject access request but all they have provided me with is copies of bills. They say they do not have any recordings of phone conversations from the time the contract was entered into. I need to know from them: - What steps were taken to establish the identity of the person taking out the contract and protect my father from fraud? - What bank account details are associated with this account or was the account opened without any bank account details? - What date was the account opened? - Who signed for the delivery of the device and where was the device delivered? They have not yet provided me with any information. How can I go about proving that this debt is not my fathers? Is the onus on Lowell to prove this debt is his if we go to court? Can they prove this debt with only bills as evidence? My dad is very vulnerable and on a fixed income with lots of additional costs as he is currently moving into supported housing and has very complex health needs. He can not afford to pay this bill which is not his. Advice very much appreciated. Thank you Em -

A few days ago I completed a few transaction over LocalBitcoins.com to a buyer named Muumbis (currently blocked) who seemed to be a trusted user, had good feedback and 2 months of multiple transactions. The buyer sent me the funds through a PayPal transfer, and then I proceeded to send/release the bitcoins to his account once the money hit my account. These transactions were very profitable to me, amounting to about 40% of profit over the then exchange price of bitcoin. Only after 6 PayPal transactions amounting to a total of around £11000, I noticed that the person’s details included in the PayPal account used to forward all these payments differed greatly from the personal information of this LocalBitcoins.com user. For comparison sake, the owner of the PayPal account is a Canadian, while this person seems to be based in Netherlands (Proxy, likely) and has a verified phone number from Kenya, as well as, beginning of a different gender. As of now PayPal as yet to contact me about any irregularities in these transactions and I made sure I transferred all my PayPal balance to my savings account. However I’m confident I got [problem]med and it’s just a matter of time until these payments are flagged as unauthorized transactions and the owner of the PayPal account files a chargeback against me leaving me empty of bitcoins and about 5000£ of negative PayPal balance, which I have no means to payback as I’m student and I already have some debt going. Summary, I sold some bitcoins at 40-50% in profit to a guy who used a hijacked PayPal account to pay me. It’s just a matter of time until the victim of the hijacked account files a PayPal unauthorised transaction/ chargeback against me. PayPal then reverses the transaction and the [problem]mer gets the bitcoins while I’m left to pay around 5000£ of debt due to the profit margin. I’m divested by this, as I’m a victim too just like the affect PayPal account owner, plus I have no means to payback if these transactions are found to be unauthorized. Perhaps, in the end, all I could do is payback the some of the money to the victim excluding the profit/debt margin that was employed in this [problem]. God, I can’t believe a fell for it, I’m aware of this sort of thing yet due to my own stupidity or being a student with no income I just went for it….Never felt so dumb. I know I’m making assumptions on what if…however, I just need to a little guidance on what to do next or who to turn to, basically a course of action to reduce all the possible damage. Thank you all

-

Hello, I'd be very grateful for any advice on how I resolve the following: - I noticed a card payment for 143.66 to Lending Stream going through my account. Realised it was fraudulent and got my card stopped etc - later that day I checked my account more thoroughly and saw that another exact same debit had gone out the month before, but I'd not noticed it - I called lending stream who confirmed they have no account in my name, or at my address and agrees the charges were fraudulent - I have now called multiple times and emailed many more but I've had no further response from them. Where do I go from here? I'd be grateful for any advice. I'm more annoyed that they feel they can just ignore the fact they've allowed two fraudulent charges against my card. Thank you

Hello, I'd be very grateful for any advice on how I resolve the following: - I noticed a card payment for 143.66 to Lending Stream going through my account. Realised it was fraudulent and got my card stopped etc - later that day I checked my account more thoroughly and saw that another exact same debit had gone out the month before, but I'd not noticed it - I called lending stream who confirmed they have no account in my name, or at my address and agrees the charges were fraudulent - I have now called multiple times and emailed many more but I've had no further response from them. Where do I go from here? I'd be grateful for any advice. I'm more annoyed that they feel they can just ignore the fact they've allowed two fraudulent charges against my card. Thank you -

Hi there I recently took up Sky on an offer regarding SkyQ. This included a main 1TB box and a smaller mini box. In short: In the initial call making me the offer (retentions team) there was no mention of a fee for multi-room services. I raised a complaint about this to which I requested the call to be listened to. I was told subsequently that the call was listened to and the monthly fee was mentioned. I then made a SAR and got a copy of the call recording and system log notes. The call contains no mention of the multi-room fee. So in short I've been lied to and have proof. Is this fraudulent - I think it is? ("deception intended to result in financial gain") If this is fraudulent, should I report this as a crime? Mr P

-

Long story short. Returned from holiday in Florence in early July booked thru Booking .com to find an unauthorized debit (around £170) on our HSBC statement in favour of Best Western Hotel. Transaction date was prior to our departure from the UK, and we stayed at a B&B, not a hotel. CrCards cancelled & replaced to forestall further unauthorized debits. Immediately queried debit with bank, who magnanimously credited the charge, and will send us a form to complete. Never arrived. Two further enquiries at our local branch, and we were told we'd get it eventually. Nope, never did. Complained to both BWH and Booking.com - twice. No response from BWH, and Booking.com were next to useless. All they did was query the charge with our B&B (Locanda di Mosconi), who had absolutely nothing to do with the unauthorized debit. Now received a letter from HSBC saying that their investigations turned up zip, and the debit will now be re-imposed, along with charges, interest, etc. 'Phoned to complain, and advised to ignore letter, as it was sent prior to completion of their enquiries! Also assured that form will be sent this time. Hmm....... Sorry, but I just don't believe them. Sod's law stipulates that our a/c will be debited in around 2 weeks regardless of what we have been told, then a right royal battle to get it back again. Now seriously considering closing the a/c to forestall re-imposition of the fraudulent charge, which I thought was their baby. If we do that, can they still legitimately pursue us for the fraud? Any advice appreciated, & apologies for the length of the short version.

-

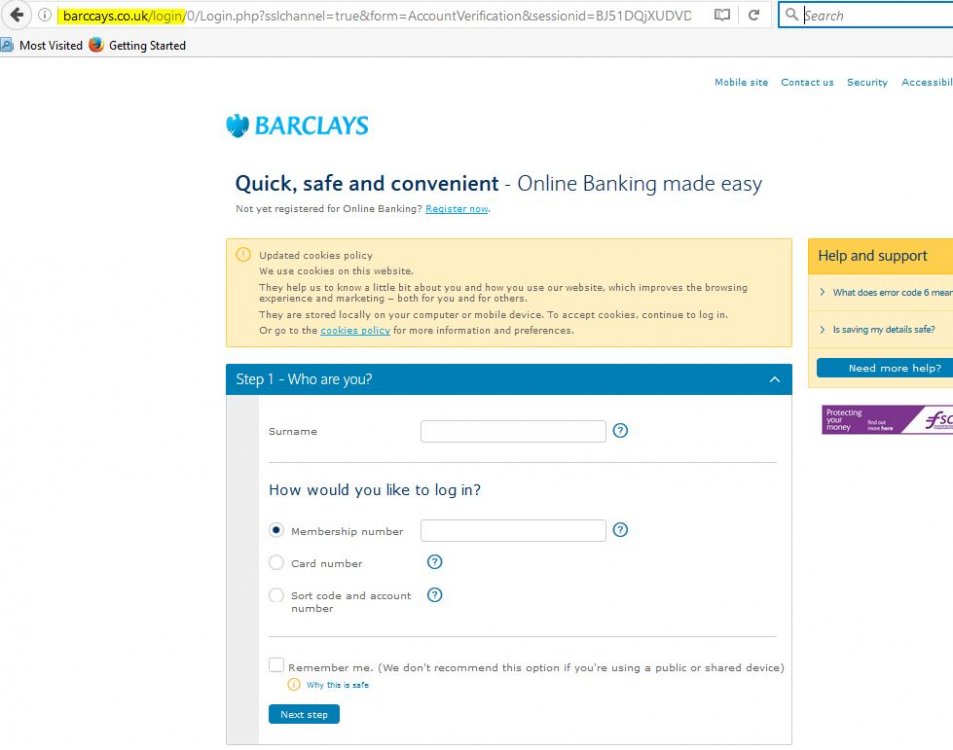

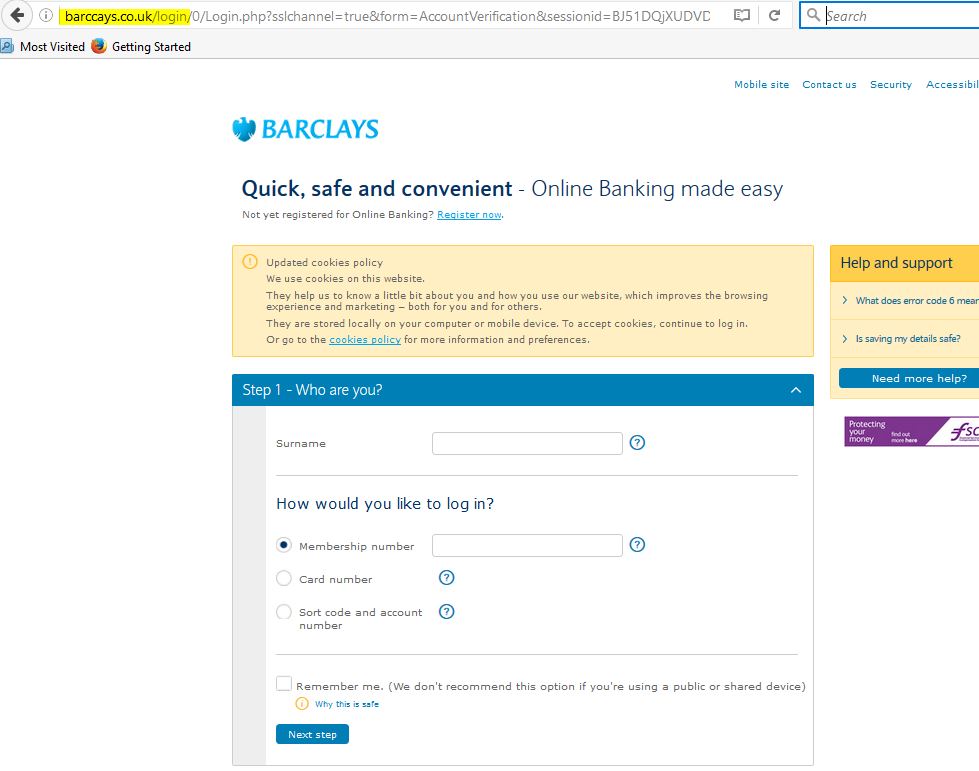

Be careful when Googling for Barclays. If you click on it, it looks, at first glance, like Barclays. But it is actually Barccays It's a sca mmers site, where you are asked to submit all your usual on-line banking details. Your account would be emptied before you were any the wiser. Always double check the address bar before entering any details

-

A dear friend is trying to fight legal action from this catalogue company via Lowell's even though she never opened the account and goods were delivered to a different address. She informed the catalogue company approximately two years ago when she first received a letter about the account. After that she heard nothing til a couple of months ago with a letter from Lowell's. Being inexperienced and knowing this was not her account she rang them and explained the account was fraudulent. She also rang the catalogue company but they couldn't give her any information! She has acknowledged the court papers and entered a defence that though the account is in herr name, she didn't receive the goods and they were not delivered to her address. But Lowell's just sent her a letter saying they would reduce the amount! How does she get evidence when the catalogue company say they have no information on what was ordered and where it was delivered? Why is this happening when she informed them about the fraud years ago. Its been assigned to her local court but she needs to be able to get evidence?

A dear friend is trying to fight legal action from this catalogue company via Lowell's even though she never opened the account and goods were delivered to a different address. She informed the catalogue company approximately two years ago when she first received a letter about the account. After that she heard nothing til a couple of months ago with a letter from Lowell's. Being inexperienced and knowing this was not her account she rang them and explained the account was fraudulent. She also rang the catalogue company but they couldn't give her any information! She has acknowledged the court papers and entered a defence that though the account is in herr name, she didn't receive the goods and they were not delivered to her address. But Lowell's just sent her a letter saying they would reduce the amount! How does she get evidence when the catalogue company say they have no information on what was ordered and where it was delivered? Why is this happening when she informed them about the fraud years ago. Its been assigned to her local court but she needs to be able to get evidence? -

Hi all, Back in Nov 2015 i bought an Audi A5 Sports Convertible, 2012 reg, for £16,600 from a massive London based car dealer. In June this year I've decided to sell it as they worry of it devaluing in time was too much for me so i wasn't really able to enjoy the car anymore. I've tried taking it back to the same dealer but they were only able to offer me £13,000 after a quick check (this amount being subject to a thorough investigation). The guy told me the car is in a really good condition and i should have no problem selling it privately for about £14,500. So after advertising it for over a month i was lucky enough to get an offer of £15,000 but, just before paying the deposit, the potential buyer called the garage to verify the service history and was informed it's fake. As i still had a copy of the original advertisement from when i bought the car together with the six invoices, all from the same garage where presumably the services have been carried out (no service book, just invoices), I've contacted consumer rights and they advised me to get in touch with the company that financed the vehicle for me. In the meantime i got confirmation in writing from the garage that they've never serviced my vehicle so i've sent everything to the finance company who opened a dispute with the car dealer and said they will contact me in 5 working days. I am now waiting for them to get back to me but in the meantime i keep wondering what will i be entitled to?! i really don't want the car (I would have never bought it if i knew it has no service history) but i have used it in the past 7 months and added 4000 miles to its usage. i am worried they will only offer me what they did before (£13,000) but if it was as advertised by them (with 6 genuine services) I could have sold it for £15,000 privately, without a service history it's near enough impossible to sell a car of this value. Consumer rights wanted to report it to trading standards as it's a criminal offence but I've asked them to hold back for now as i feel it's my bargaining tool, I've mentioned this to the finance company and said i would like to try and resolve this matter peacefully first before getting the media and trading standards involved... Any ideas as to where i stand in terms of compensation? Many thanks, Anca

Hi all, Back in Nov 2015 i bought an Audi A5 Sports Convertible, 2012 reg, for £16,600 from a massive London based car dealer. In June this year I've decided to sell it as they worry of it devaluing in time was too much for me so i wasn't really able to enjoy the car anymore. I've tried taking it back to the same dealer but they were only able to offer me £13,000 after a quick check (this amount being subject to a thorough investigation). The guy told me the car is in a really good condition and i should have no problem selling it privately for about £14,500. So after advertising it for over a month i was lucky enough to get an offer of £15,000 but, just before paying the deposit, the potential buyer called the garage to verify the service history and was informed it's fake. As i still had a copy of the original advertisement from when i bought the car together with the six invoices, all from the same garage where presumably the services have been carried out (no service book, just invoices), I've contacted consumer rights and they advised me to get in touch with the company that financed the vehicle for me. In the meantime i got confirmation in writing from the garage that they've never serviced my vehicle so i've sent everything to the finance company who opened a dispute with the car dealer and said they will contact me in 5 working days. I am now waiting for them to get back to me but in the meantime i keep wondering what will i be entitled to?! i really don't want the car (I would have never bought it if i knew it has no service history) but i have used it in the past 7 months and added 4000 miles to its usage. i am worried they will only offer me what they did before (£13,000) but if it was as advertised by them (with 6 genuine services) I could have sold it for £15,000 privately, without a service history it's near enough impossible to sell a car of this value. Consumer rights wanted to report it to trading standards as it's a criminal offence but I've asked them to hold back for now as i feel it's my bargaining tool, I've mentioned this to the finance company and said i would like to try and resolve this matter peacefully first before getting the media and trading standards involved... Any ideas as to where i stand in terms of compensation? Many thanks, Anca -

Hi guys, This is a long read, I know, but I believe that not only have I purchased a car with a fraudulent MOT, I have also uncovered a rather large fraud involving a very well known scrap collection company. I bought a 52 plate (2002) Ford Mondeo on eBay on 10th July. The car was advertised as having 12 months MOT and it was stated that the car passed with zero advisories on the 6th July and that it had been 'fastidiously maintained'. I checked it's MOT online and it showed that it had indeed passed with no advisories. This obviously gave me the confidence to bid on the vehicle without test driving, which in hindsight was very stupid! (Lesson well and truly learned) I collected the vehicle on the 11th and on the drive home there was considerable knocking sounds coming from the rear of the car so I took it straight to my local garage to have it looked at. The mechanic who looked at the car stated that it was physically impossible for this car to have passed an MOT just 5 days previous, let alone passed it with no advisories. He said there were a number of dangerous faults and he advised me not to drive the vehicle home. He told me I could leave the car there for a few days and said that I should contact the DVSA to complain about the MOT carried out on the 6th July. I filled in the necessary form and the DVSA inspected the vehicle yesterday (22nd). The inspector phoned me to inform me that he had discovered a very long list of failures which included 5 dangerous faults. He immediately, and understandably, issued the vehicle with a Prohibition Notice and told me in no uncertain terms that not only had the vehicle been incorrectly passed on the 6th but that he believed the tester who passed it hadn't even seen the car before issuing the pass certificate. Thing is now, the car has cost me £450 so far (not a lot to many people but it is to me) and I'm left with a vehicle with a scrap value of £65! Now here is where it gets interesting. I've looked into scrapping the car and I've been shopping around for the best prices when I found a site called Car Take Back. They arrange for a local company to collect your vehicle for you and it is supposedly taken away and recycled. That's what their website says, anyway. But the company they list as being my local collection agent just so happens to operate from the same unit under the same owner with the same telephone number as the company I purchased the Mondeo from on eBay. Could it be that he is collecting scrap cars from members of the public via Car Take Back, sticking fraudulent MOT certificates on them and then listing them under his other company name on eBay? Almost all of the cars he lists have 12 months MOT with no advisories, which is very suspicious. If this is the case then this obviously needs to be stopped. The chap from DVSA must have done his research, too, as he also mentioned that the company I purchased the vehicle from also collects scrap for Car Take Back. He never came out and said it but he's obviously thinking along the same lines as me. He has assured me that in addition to the company that wrongly passed the vehicle, he will also be fully investigating the company that I bought the car from. Whilst I welcome that and hope justice is done, I'm still out of pocket. So, for those of you that have stuck with me this far; what do you think is the best avenue for me getting my money back? I have today written to the previous owner listed on the logbook explaining what has happened and asking them to confirm whether they did scrap the car via Car Take Back. But, I am unsure of my next steps. Trading Standards? Contact the seller with all of the evidence I have so far and ask him to refund me? Last time I spoke to him he denied any knowledge of the MOT and said it was nothing to do with his company. Contact the MOT station that issued the MOT and ask them to bring the car up to MOT standard? Wait for the DVSA to finish then pursue the seller with whatever evidence they uncover? I'd really appreciate any advice or help from someone that might have been through this before and might be able to advise the best route to getting my money back.

-

I have been a member of Amazon UK since 2003 and have rarely used the seller feedback option on the UK site. I was appalled to learn that I have apparently left pages & pages of 5 star feedback for sellers. This, on a quick perusal yesterday, goes back to 2009 but I suspect it goes back further. I assume Amazon do this to instil consumer confidence in the sellers listed on their marketplace which seem to be around the 95-99% rate on average. I have not left this 5 star feedback so I contacted Amazon 3 times in the last two days but they have not responded which is unusual. Since I have not posted this feedback I have addressed the matter to Trading Standards & CMA but I am never sure how effective they are. I am appalled to be treated dishonestly and basically used in this way. I note that Amazon have started taking legal action against people who fraudulently leave feedback on items they sell. Can anyone stop them from using customers this way? This is not the first time Amazon's business practices have been highlighted but I suspect this particular problem is rife on their sites across the world. As soon as my last items appear, I shall be ceasing trading with this company. Has anyone else noted this and if so, what is the best way to address this and let others know what is happening? Many thanks

-

Hi there, I'm having some problems to get the balance of my deposit back, this is £290. I have sent 3 emails to my former landlord and he said that I'm his lodger, I don't have any right and they are not willing to give me anything back. The problem is I'm not his lodger, he didn't live in the property. The landlord is a business of 2 Spanish guys (agency) taking advantage of other foreigners in London. They rent properties through letting agencies and they sublet every inch in the house to people. We were living in London 8 people in a house with one bathroom. As far as I know the owner of the house doesn't know what is happening in her house, but my landlord doesn't want to give me her details nor the letting agency details neither. The agency who rented me the house keeps partly the deposits of other tenants saying that the walls need to be repainted or things like that. My former flatmates had the same problem as me. In my case, they are charging me for a mould which grew in the bedroom due poor insulation, for the cleaning of that mould and for the curtains (which are dirty because of the mould and they were so high I couldn't remove them to wash them up). They are charging me for the walls (were dirty before I moved there, but they didn't do a check-out to the previous tenant and they are charging me for it) and for one night I did not sleep there. This agency are making fraudulent contracts. My contract says "Licence to occupy" and it says "This agreement is not intended to confer exclusive possession upon the licensee, nor it is intended to create the relationship of landlord and tenant between the parties. The Licensee shall not be entitled to an assured tenancy or a statutory periodic tenancy under the Housing Act 1988 or to any other statutory secure of tenure now or upon the determination of the Licence. The Licensee accepts that this Licence does not confer any statutory protection and/or rights that would otherwise be applicable to an assured tenancy or a statutory periodic tenancy under the Housing Act 1988". I contacted Shelter and they said that the agreement is not legal as I was a tenant, not a lodger, as the landlord is an agency and they do not share the property with us. A legal advisor in Shelter told me that I can go to court and make a claim because the agency didn't protect my deposit despite the agreement says. Does anybody know what can I do in this case? This agency does not want to talk to me nor to reply my emails. They took my money unfairly and they are doing the same to other foreigners as people leave the property and they do not know how to claim their money back. So they keep doing the same over and over again. They are taking advantage mainly of Spaniards who come to the UK without knowing how the system works. Is there any way I can report them? If so, where? I don't mind the money, but I want to stop them to do the same to other people. Many thanks.

Hi there, I'm having some problems to get the balance of my deposit back, this is £290. I have sent 3 emails to my former landlord and he said that I'm his lodger, I don't have any right and they are not willing to give me anything back. The problem is I'm not his lodger, he didn't live in the property. The landlord is a business of 2 Spanish guys (agency) taking advantage of other foreigners in London. They rent properties through letting agencies and they sublet every inch in the house to people. We were living in London 8 people in a house with one bathroom. As far as I know the owner of the house doesn't know what is happening in her house, but my landlord doesn't want to give me her details nor the letting agency details neither. The agency who rented me the house keeps partly the deposits of other tenants saying that the walls need to be repainted or things like that. My former flatmates had the same problem as me. In my case, they are charging me for a mould which grew in the bedroom due poor insulation, for the cleaning of that mould and for the curtains (which are dirty because of the mould and they were so high I couldn't remove them to wash them up). They are charging me for the walls (were dirty before I moved there, but they didn't do a check-out to the previous tenant and they are charging me for it) and for one night I did not sleep there. This agency are making fraudulent contracts. My contract says "Licence to occupy" and it says "This agreement is not intended to confer exclusive possession upon the licensee, nor it is intended to create the relationship of landlord and tenant between the parties. The Licensee shall not be entitled to an assured tenancy or a statutory periodic tenancy under the Housing Act 1988 or to any other statutory secure of tenure now or upon the determination of the Licence. The Licensee accepts that this Licence does not confer any statutory protection and/or rights that would otherwise be applicable to an assured tenancy or a statutory periodic tenancy under the Housing Act 1988". I contacted Shelter and they said that the agreement is not legal as I was a tenant, not a lodger, as the landlord is an agency and they do not share the property with us. A legal advisor in Shelter told me that I can go to court and make a claim because the agency didn't protect my deposit despite the agreement says. Does anybody know what can I do in this case? This agency does not want to talk to me nor to reply my emails. They took my money unfairly and they are doing the same to other foreigners as people leave the property and they do not know how to claim their money back. So they keep doing the same over and over again. They are taking advantage mainly of Spaniards who come to the UK without knowing how the system works. Is there any way I can report them? If so, where? I don't mind the money, but I want to stop them to do the same to other people. Many thanks. -

I have a friend who was contacted by his insurance company due to a claim that he was in an accident and wrote off someone's car. My friend was not in an accident and so following investigation his insurance company rejected the claim. I've seen the photos of both cars, my friends car has not been in an accident, and the other car is an old banger with a bumper literally falling off. It might be worth mentioning the party making the accusation consist of three men who all have suffered from whiplash. Now it appears that the fraudulent party are now going after my friend directly, he got the following corespondence from his insurance company: My friend is obviously terrified having never been involved in legal proceedings other than buying a house. Can anyone layout what he can expect? I've told him he's got nothing to worry about as this false claim has been thrown out by the insurance company and you can't prove something that never happened. Practically can he refuse to cooperate as it is a waste of time? Is he obliged to do anything? Is it time to get a solicitor or will the insurance company assist as they are involved? Thanks for any advice. Any questions I'll relay and get back to you.

-

Scenario: Ex wife left house in July this year. I remained in marital property (in joint names although I have always paid the mortgage and all bills). Divorced in November 15. She had already changed her name back to her pre-married name prior to moving out. She didn't turn up for Financial Order hearing at court - this has been adjourned until March16. I received post addressed to her former married name and as it was from a phone Company I was suspicious and opened it. 2 letters - one a Bank DD mandate confirmation and the second a Phone Bill for a new phone and two year calling plan - all made out in her ex name and at an address she doesn't live at. Whilst she still may have a legal claim against the house - I believe this to be fraudulent activity - any advice/comments would be welcome before I throw more money at my costly Solicitor. NB. Phone has not been delivered to this address - so she obviously sorted that one out with them or collected it. Also - shes no longer on electoral roll at this address so don't understand how shes managed to do it?

-

Hi, Some advice please. I was involved in a very minor shunt over the weekend, there was no damage to either vehicle but I exchanged numbers with the other driver. I took pictures of both cars as well. I've had a phone call today from the other driver asking for my insurance company details and informing me that he has neck pain. My vehicle was stationery at the time and the other vehicle rolled back into my car. I'm very concerned as I think this is a fraudulent claim but even more of a concern is that I had a claim earlier in the year where my car was written off. If I tell my insurance company of this incident I probably wont be able to afford my renewal, regardless of whether it was my fault or not. Also my understanding is that the other driver goes to his insurance company and makes the claim who will then automatically contact my insurers. Any guidance would be appreciated.

-

Greetings, I do not know if I am posting this in the right forum, but I'm wanting help with something Barclays has done to me: I posted the following question to Barclays customer service department (all the following quotes are simply repostings of our interaction): Me: "Greetings, I am requesting that Barclay card does not increase my credit line, and does not do any hard credit checks whatsoever on my account. Can you please add a note that this customer does not wish to have any credit checks accomplished?" Barclay's Response: "Dear _customer's name_: Thank you for contacting us regarding your Barclaycard Arrival Plus World Elite MasterCard. We can certainly address your concern regarding the FICO® score on your account. When you view your FICO® Score through this program, you are not impacting your credit score in any way. Credit inquiries classified as "Hard inquiries" (like when you apply for credit) may affect your credit score. "Soft inquiries" do not impact your credit score and are initiated for the purpose of pre-approved credit offers, and by existing creditors to monitor risk. The FICO® program is simply sharing the information obtained through soft inquiries. Therefore, it does not affect your credit score. Further, please be advised that we receive updated information from TransUnion once every 10 weeks, or whenever there are certain changes to your credit file (new account openings, new inquiries for credit, etc.). Whenever that updated information affects your FICO® Score, we will send you an email alert letting you know that your FICO® Score has changed. For more information regarding your FICO® score, you can access the Terms of Use through the 'Your FICO® Score' tab, located in the 'Tools' section of the website. We hope you find this information helpful. If you have any other questions and concerns, please reply to this message. Sincerely, Customer Care" My response: "Greetings, thank you for responding. This is not what I asked. Notice that I asked you not to do any HARD credit inquiries on our account. I don't care if the FICO score is updated, I care that you don't do any HARD inquiries on our account. In other words, last year you did a HARD inquiry on our account to increase our credit limit, which we did not ask for. I do NOT want that done again. Does that make sense? I can explain further if you'd like." Barclay's response: "Dear _customer name_ : Thank you for contacting us regarding your Barclaycard Arrival Plus World Elite MasterCard. We can certainly address your concern regarding the hard inquiry on your account. We will need to pull and evaluate your Credit Bureau Report. Please keep in mind that we are only doing a hard pull in order to process your credit limit increase request. We hope you find this information helpful. If you have any other questions and concerns, please reply to this message. Sincerely, Customer Care" My response: "Wow! What part of DO NOT PULL A HARD CREDIT REPORT are you not understanding? I thought I had been really really clear, but I guess not. Is there a way that you might send this request to someone who understands English for me? I'd really really appreciate it. Again, I want to try to be as clear as I possibly can. I do NOT want you to pull ANY hard credit reports from me. I do NOT want an increase in credit with you. I do NOT want another hard credit report pulled. Again, would it be possible for you to forward this request to someone who understand English? I'm not being rude, I just really don't understand why you can't understand my request . It seems really straight forward. DO NOT PULL A HARD CREDIT REPORT, and DO NOT GIVE ME AN INCREASE IN CREDIT. If you're having difficulty with this, please tell me what your first language is and I will see if I can translate it so that it is understandable. Please respond back that you will NOT pull a hard credit report ever again. Thank you." One week later, I found out that they had pulled a hard credit report on me. Is there anything that can be done about this? It seems very blatant disregard for the customer's request.

-

Nobody ever told it it was fraudulent

sirbob10 posted a topic in Vehicle retailers and manufacturers

Hi I'm desperate for some advice. Since 2010 my dad has took the finance out for me due to bad credit history. We've had 3 VW, 2 Toyotas and now a Honda. Toyota have financed the last 2 cars and the Honda we have now. We've always been upfront with the dealer. the 2 Toyotas came from the same dealer and we told them that I couldn't get finance so they asked if someone else could and my dad agreed and when we went for the Honda I to,d them as well and they also suggested I get someone so I did and my dad agreed again. Today I've found out it's illegal. I was talking to Toyota Finance due to a issue with the Honda and mentioned my dad had the finance and I drove the car and it was registered in my hisbands name and kept at our address. She said Toyota don't allow this..I told her the 2 dealers have never said a thing about it not being allowed. I've told my dad and he's shocked and said if it was fraud he'd never have agreed to finance the cars. What is likely to happen. We are looking to sell the car anyway but I'm worried they think my dad has committed fraud. It was the dealer who suggested it. Why would they do this if it was fraud. -

Between 1st-7th April a number of payments were taken from my debit card, to a company I have never heard of. I contacted barclays who put me through to the fraud team, who said I could open a dispute. I had to wait for forms, and as soon as they recieved them I would get a refund. When the forms arrived I took them into my local branch and asked them to fax them for me, so that they couldn't get 'lost' or anything. I then contacted the fraud department and was told that now I had to wait 10 working days for a refund. 3 days after that I recieved a letter stating it would now be TWENTY working days before I got a refund. I called the bank back and was told it would be 10 and the letter was wrong. 10 working days came and went so I called again, to be told it would be a further 10 working days as I had been informed it would be twenty, not ten (!) At this point I was fairly ****ed off tbh. I contacted the FOS who informed me that I should have received an instant refund when reporting the fraud. They also told me however that I had to follow the banks internal complaints procedure before I could put in a complaint with the FOS. So I put in a complaint. I was then contacted by someone who told me that it would be a 2 more days but for the incorrect information I had been given..he would credit my account with fifty quid as a 'goodwill gesture'. 2 days went, then I recieved another letter telling me my case had been passed to the 'complex investigations team' and would take ANOTHER 20 working days. I was foaming by this point. Called them back and they said to ignore that letter as it was wrong (again). I asked how long this 'investigation' was going to take, and now the timescale didn't exist at all. I was told it 'usually' takes 20 working days but could take much longer. I tried to register another complaint about again being given wrong info by many different staff members, but I was told that as I had accepted a 'goodwill gesture' payment nothing could be done! I hung up the phone in a rage at this point. Probably not the most mature thing to do but I really feel its taking the mick. When I calmed down a bit, a few days later I called again. And was told a letter had been sent to me I received the letter the next say stating that my complaint would not be upheld as fraud investigations take time and not every one is the same, and also stating that they are following FCA rules by withholding my refund for nearly 6 weeks. I was then taken into hospital so I have not contacted them again, nor have they sent me any letters or given me a refund. What can I do now? The barclays complaints department will not even entertain my complaint,. so I can't get a 'final response' letter which is what the FOS said they needed. I am out a large amount of money (to me) and barclays appears to be enjoying messing me around. Its really true when they say bad things come in 3s..had problems with brighthouse, fraud on my bank, and a hospital stay all within a few months of each other

-

Hello kind people! Long story short, it sounds unreal but I assure you it certainly is true. In 2007 I took a loan from a high street bank I originally applied for 7k. Then decided to round the amount up to 10k, which they happily agreed to do and the money was in my account the same day. However, the next day the bank paid another 10k into my account (!) I went to the bank branch where I took the loan from and they simply said it was a mistake and removed the extra 10k. Recently I have received a letter from debt collectors asking for that virtual 10k which I have never applied for and never taken. It turns out that the bank still had that virtual 10k on my account as a loan! Now the debt collectors backed off after I asked them to get that mess sorted with the bank and apparently they're awaiting the bank's response. My question is what will be the reasonable compensation for messing my credit score with a virtual 10k debt and all the hassle they have caused me for years? Should I take this to small claims court or any other court? To me this is a full on fraud as the bank blatantly refused to remove this virtual 10k although there has never been a loan agreement on that and asked me to pay the virtual loan which I have never asked for. The 10k has been withdrawn back from my account within an hour after I reported their mistake back in 2007 but the amount has been still held on my record All help will be greatly appreciated. Lots of love Littlebitlost

-

Hi, First time post here. I have a problem which I am hoping forum members can offer their opinions and advice on please. I run a small business which has an office based phone system. Hackers somehow accessed our office phone system one night in January. They managed to remotely make hundreds of calls, one after the other, to a premium rate number in the Solomon Islands. Each time the call connected, it cost £50. The total cost of the fraudulent calls is £3,500. BT contacted us the following morning to say it looked like our system had been hacked, due to the unusual overnight call activity to premium rate numbers. We immediately found and patched the loophole which had allowed the remote access. I then contacted our BT business account manager and asked them to place the disputed bill on hold whilst it was investigated. Subsequently, BT have written me to advise that, according to their terms and conditions, we are liable for the fraudulent calls. They have offered a payment plan, but won't reduce the bill. BT have also advised me that because the premium rate numbers are outside of the UK, they are not controlled via a UK regulatory body. They also tell me that they are under no obligation to monitor or identify fraudulent use of the network. Because the calls were made to the Solomon Islands they also advised there is no way they can recover the cost back. So, BT's view is that I have to pay the bill. They also suggested to recover the cost from the IT company which manages our network or from the Phone company which manages our phone system. Both of those companies are small business, and they say it wasn't their fault, and in any event they can't afford to pay. I should probably also add that BT agree that they accept that the phone calls have been fraudulently by criminals. I have also reported the details to Action Fraud to get my crime reference number. I've written back to BT and said asked the following question; i) As the fraud was identified straight away and BT agree it was fraud, BT wouldn't pay the company in the Solomon Islands immediately - it must go through some form of invoice process which would take some days to process. As I asked BT to not make the payment to the company in the Solomon Island when I first found out about the fraud, my logic is that, if BT don't pay the invoice to the Solomon Islands, then there is no need to pursue me for the costs. ii) Can BT then confirm they have notified the company in the Solomon Islands of the fraud? When did they notify the company? I have also asserted, if BT do go ahead and make the payment to the Solomon Islands, for a payment which they know to the fraudulent, and then the recover the cost from me, they will be benefiting from the proceeds of crime, which is definitely immoral and probably illegal. Whilst their terms and condition state that I am responsible for the fraudulent use of their network, they also have some responsibility to prevent fraudulent use of their network. They know for example from our call history, we never phone premium rate numbers, we never phone the Solomon Islands, we never phone in the middle of night, and we don't make repeated calls to the same premium rate number one after the other. Our normal call bill with BT is £200 / month by the way. BT have replied saying they are seeking a legal view. Of course their solicitor will say BT are in the right. I've replied to say, they need to be sure of their facts as if they insist on taking the payment from my account, I will raise a moneyclaim on-line, and we can let a County Court judge decide if they agree with BT's view. In my mind, the crux is whether BT make the payment to the Solomon Islands straight away, or whether they actually have an opportinity to prevent the invoice from being made straight away whist it is being investigated. If they don't make any attempt to prevent the fraud from being completed, I believe this would be unreasonable and it would help my case. Can anyone offer any suggestions or advice or how I should progress this?

Hi, First time post here. I have a problem which I am hoping forum members can offer their opinions and advice on please. I run a small business which has an office based phone system. Hackers somehow accessed our office phone system one night in January. They managed to remotely make hundreds of calls, one after the other, to a premium rate number in the Solomon Islands. Each time the call connected, it cost £50. The total cost of the fraudulent calls is £3,500. BT contacted us the following morning to say it looked like our system had been hacked, due to the unusual overnight call activity to premium rate numbers. We immediately found and patched the loophole which had allowed the remote access. I then contacted our BT business account manager and asked them to place the disputed bill on hold whilst it was investigated. Subsequently, BT have written me to advise that, according to their terms and conditions, we are liable for the fraudulent calls. They have offered a payment plan, but won't reduce the bill. BT have also advised me that because the premium rate numbers are outside of the UK, they are not controlled via a UK regulatory body. They also tell me that they are under no obligation to monitor or identify fraudulent use of the network. Because the calls were made to the Solomon Islands they also advised there is no way they can recover the cost back. So, BT's view is that I have to pay the bill. They also suggested to recover the cost from the IT company which manages our network or from the Phone company which manages our phone system. Both of those companies are small business, and they say it wasn't their fault, and in any event they can't afford to pay. I should probably also add that BT agree that they accept that the phone calls have been fraudulently by criminals. I have also reported the details to Action Fraud to get my crime reference number. I've written back to BT and said asked the following question; i) As the fraud was identified straight away and BT agree it was fraud, BT wouldn't pay the company in the Solomon Islands immediately - it must go through some form of invoice process which would take some days to process. As I asked BT to not make the payment to the company in the Solomon Island when I first found out about the fraud, my logic is that, if BT don't pay the invoice to the Solomon Islands, then there is no need to pursue me for the costs. ii) Can BT then confirm they have notified the company in the Solomon Islands of the fraud? When did they notify the company? I have also asserted, if BT do go ahead and make the payment to the Solomon Islands, for a payment which they know to the fraudulent, and then the recover the cost from me, they will be benefiting from the proceeds of crime, which is definitely immoral and probably illegal. Whilst their terms and condition state that I am responsible for the fraudulent use of their network, they also have some responsibility to prevent fraudulent use of their network. They know for example from our call history, we never phone premium rate numbers, we never phone the Solomon Islands, we never phone in the middle of night, and we don't make repeated calls to the same premium rate number one after the other. Our normal call bill with BT is £200 / month by the way. BT have replied saying they are seeking a legal view. Of course their solicitor will say BT are in the right. I've replied to say, they need to be sure of their facts as if they insist on taking the payment from my account, I will raise a moneyclaim on-line, and we can let a County Court judge decide if they agree with BT's view. In my mind, the crux is whether BT make the payment to the Solomon Islands straight away, or whether they actually have an opportinity to prevent the invoice from being made straight away whist it is being investigated. If they don't make any attempt to prevent the fraud from being completed, I believe this would be unreasonable and it would help my case. Can anyone offer any suggestions or advice or how I should progress this? -

Hello CAG! You know, there are times when we all have to deal with 'not so good' customer service but in the end matters end up being resolved with some persistence. However with Vodafone customer support I've never felt soo helpless. I have followed their process to the letter, and thus so far it has got me nowhere. I need a Vodafone rep to action on this and get it sorted. Background: June 2012 - I sign up to Vodafone as a new customer, 24 month contract (Iphone 4). June 2014 - Contract ends, I do not change anything. October 2014 - I decide to DOWNGRADE to a sim 30 day contract plan (£11.ono) as this suits my needs and I don't want to upgrade. My plan is changed as requested, no long term contract. - See Attachment #1 [ATTACH=CONFIG]55754[/ATTACH] Everything WAS GOOD - until... Mid January 2015 a fraudulent upgrade order is placed on my account. I have a 'full-fat' version of my issue in a thread with attachments over at the Vodafone eForum... which sadly has got me NOWHERE. ## I'll need to PM the rep the forum link as I can't post the link on here ## Monday 12th Jan 2015 Text message received on my mobile thanking me for the upgrade. What upgrade? I try to login into the online portal to make sure all is well. I can't login, I'm able to reset my account, seems someone changed the username (email address), added an extra character. Price plan still shows 1mth Sim only, £11.50 ... so I think nothing of it, perhaps a glitch. Wednesday 14th Jan 2015 - 10pm DPD email received confirming that my Vodafone package is to sent out tomorrow. What the hell? - even worse... it has my name on the package and an address based in Birmingham... I do NOT have any connection with that address, nor do I live in Birmingham! I try logging into the online portal, once again my username has been changed. I managed to get access back, and now my bill has bumped up to £48.50!!... from what I can see it's a two year contract on an iphone 6! What the fraudster didn't know, was that I received the DPD delivery email, therefore I was able to change the delivery day to one FULL week later so that he/she would not get it tomorrow. Once delivery had been changed, I spoke to Vodafone web support, called lost/stolen dept on the phone and even filled in a online 'Fraud Claim' form on their site to cover all bases! Thursday 15th Jan 2015 - 8.30am Call the Vodafone Lost/Stolen dept for an update, they confirm DPD has got the package and is returning it back to Vodaphone... SUCCESS! - See Attachment #2 They also mentioned the fraudulent order was placed via the web portal. Finally I am told the non-contact Fraud team will need 7-10 days to investigate before my account is returned back to normal. [ATTACH=CONFIG]55755[/ATTACH] Thursday 15th January 2015 - 7:00pm I receive an automated email from Vodafone in the evening confirming my new 'fraudulent' plan - I know at this point I need to wait 7-10 days for the fraud team to do their thing and put everything back to normal. I can no longer login to my online account as it was confirmed by customer services online access has been deleted for security purposes. I agree with this move, though it means for the time being I have no easy way of checking my tarrif/bill. Email Confirmation of new fraudulent plan - See Attachment 3. [ATTACH=CONFIG]55753[/ATTACH] Sunday 18th January 2015 I call Vodafone support to catch up on 'RETURN' status of the package from DPD. Note that from the moment "return to consignor" was requested the DPD tracking page no longer updates (I guess it has a new consignment number). It's apparently on it's way through returns so I'm told. The billing team confirm my account is still set to bill £48.50 on the new plan(contract), and that it can't be changed until the Fraud team are done investigating. As a precaution the advisor did tell me to cancel my direct debit which I have done. The fraudsters try to trick me into releasing my account details (since they no longer have web access to my account). They send me this bogus email, hoping I'd click on the link and submit my information. They sent it twice an hour later, I guess they are pretty pi$$ed they didn't get their iphone6: - See Attachment 4 [ATTACH=CONFIG]55752[/ATTACH] Wednesday 21st January 2015 - 11:30am I use the Vodafone support chat to find out more about what is going on. The agent confirms the handset has arrived back at the warehouse. My account is still set to the new contract (£48.50)....! I've also reached the point at which I want to leave Vodafone once this mess has been fixed. See Attachment 5: [ATTACH=CONFIG]55751[/ATTACH] Sunday 25th January 2014 - 4:44pm Vodafone Forum Staff send me a special form link to escalate my issue ... a.k.a golden ticket. A WRT Reference is supplied: #9227428 I am then given the following response: Thanks for your email here. I understand that you wish to cancel the upgrade which has been done on your account without your consent. I can see that a fraud case is already raised on your account and the team is investigating on this matter. As the dedicated team is checking on this we can't comment on this issue at this point of time. As soon as the investigation is complete the team will let you know. Any corrective measures, (if required) will be taken by the team and your account will be made up to date. It may take up to 4 - 5 more working days for the team to complete the investigation. You can get back to us after this timeframe for any update if you don't get any update by this time. Your patience and cooperation in this matter will be appreciated. Kind regards, ###### Customer Service Agent (eForum) Wrapping it up 5 days on since that last update, did I get a call or any correspondence from the Vodafone team? .... No. Has my plan reverted back to what it was (sim 30day) .... No. Do they have their phone back? ... Yes. Vodafone, you can't deny I have tried everything to make sure this matter is resolved and that I am not billed incorrectly. Were the phone truly stolen (delivered to fraudster) I could understand the need for a longer investigation, but the handset is back with you yet my account is still set on a 2 year contract for £48.50 p/m. Vodafone reps, I need help with the following please: Some form of direct communication with you. I'm done with talking to web chat support, general telephone support, and eForum - I keep going around in circles. A REAL update from the fraud team. I know customers cannot contact them directly, but internal staff can - I don't want to hear another generic "they need x days" statement... they have the handset! Revert my account to what it was, sim 30 day, and provide me with a PAC code - I'm moving on, a PAC code once activated should properly terminate my account. Thanks for reading! Dal

Hello CAG! You know, there are times when we all have to deal with 'not so good' customer service but in the end matters end up being resolved with some persistence. However with Vodafone customer support I've never felt soo helpless. I have followed their process to the letter, and thus so far it has got me nowhere. I need a Vodafone rep to action on this and get it sorted. Background: June 2012 - I sign up to Vodafone as a new customer, 24 month contract (Iphone 4). June 2014 - Contract ends, I do not change anything. October 2014 - I decide to DOWNGRADE to a sim 30 day contract plan (£11.ono) as this suits my needs and I don't want to upgrade. My plan is changed as requested, no long term contract. - See Attachment #1 [ATTACH=CONFIG]55754[/ATTACH] Everything WAS GOOD - until... Mid January 2015 a fraudulent upgrade order is placed on my account. I have a 'full-fat' version of my issue in a thread with attachments over at the Vodafone eForum... which sadly has got me NOWHERE. ## I'll need to PM the rep the forum link as I can't post the link on here ## Monday 12th Jan 2015 Text message received on my mobile thanking me for the upgrade. What upgrade? I try to login into the online portal to make sure all is well. I can't login, I'm able to reset my account, seems someone changed the username (email address), added an extra character. Price plan still shows 1mth Sim only, £11.50 ... so I think nothing of it, perhaps a glitch. Wednesday 14th Jan 2015 - 10pm DPD email received confirming that my Vodafone package is to sent out tomorrow. What the hell? - even worse... it has my name on the package and an address based in Birmingham... I do NOT have any connection with that address, nor do I live in Birmingham! I try logging into the online portal, once again my username has been changed. I managed to get access back, and now my bill has bumped up to £48.50!!... from what I can see it's a two year contract on an iphone 6! What the fraudster didn't know, was that I received the DPD delivery email, therefore I was able to change the delivery day to one FULL week later so that he/she would not get it tomorrow. Once delivery had been changed, I spoke to Vodafone web support, called lost/stolen dept on the phone and even filled in a online 'Fraud Claim' form on their site to cover all bases! Thursday 15th Jan 2015 - 8.30am Call the Vodafone Lost/Stolen dept for an update, they confirm DPD has got the package and is returning it back to Vodaphone... SUCCESS! - See Attachment #2 They also mentioned the fraudulent order was placed via the web portal. Finally I am told the non-contact Fraud team will need 7-10 days to investigate before my account is returned back to normal. [ATTACH=CONFIG]55755[/ATTACH] Thursday 15th January 2015 - 7:00pm I receive an automated email from Vodafone in the evening confirming my new 'fraudulent' plan - I know at this point I need to wait 7-10 days for the fraud team to do their thing and put everything back to normal. I can no longer login to my online account as it was confirmed by customer services online access has been deleted for security purposes. I agree with this move, though it means for the time being I have no easy way of checking my tarrif/bill. Email Confirmation of new fraudulent plan - See Attachment 3. [ATTACH=CONFIG]55753[/ATTACH] Sunday 18th January 2015 I call Vodafone support to catch up on 'RETURN' status of the package from DPD. Note that from the moment "return to consignor" was requested the DPD tracking page no longer updates (I guess it has a new consignment number). It's apparently on it's way through returns so I'm told. The billing team confirm my account is still set to bill £48.50 on the new plan(contract), and that it can't be changed until the Fraud team are done investigating. As a precaution the advisor did tell me to cancel my direct debit which I have done. The fraudsters try to trick me into releasing my account details (since they no longer have web access to my account). They send me this bogus email, hoping I'd click on the link and submit my information. They sent it twice an hour later, I guess they are pretty pi$$ed they didn't get their iphone6: - See Attachment 4 [ATTACH=CONFIG]55752[/ATTACH] Wednesday 21st January 2015 - 11:30am I use the Vodafone support chat to find out more about what is going on. The agent confirms the handset has arrived back at the warehouse. My account is still set to the new contract (£48.50)....! I've also reached the point at which I want to leave Vodafone once this mess has been fixed. See Attachment 5: [ATTACH=CONFIG]55751[/ATTACH] Sunday 25th January 2014 - 4:44pm Vodafone Forum Staff send me a special form link to escalate my issue ... a.k.a golden ticket. A WRT Reference is supplied: #9227428 I am then given the following response: Thanks for your email here. I understand that you wish to cancel the upgrade which has been done on your account without your consent. I can see that a fraud case is already raised on your account and the team is investigating on this matter. As the dedicated team is checking on this we can't comment on this issue at this point of time. As soon as the investigation is complete the team will let you know. Any corrective measures, (if required) will be taken by the team and your account will be made up to date. It may take up to 4 - 5 more working days for the team to complete the investigation. You can get back to us after this timeframe for any update if you don't get any update by this time. Your patience and cooperation in this matter will be appreciated. Kind regards, ###### Customer Service Agent (eForum) Wrapping it up 5 days on since that last update, did I get a call or any correspondence from the Vodafone team? .... No. Has my plan reverted back to what it was (sim 30day) .... No. Do they have their phone back? ... Yes. Vodafone, you can't deny I have tried everything to make sure this matter is resolved and that I am not billed incorrectly. Were the phone truly stolen (delivered to fraudster) I could understand the need for a longer investigation, but the handset is back with you yet my account is still set on a 2 year contract for £48.50 p/m. Vodafone reps, I need help with the following please: Some form of direct communication with you. I'm done with talking to web chat support, general telephone support, and eForum - I keep going around in circles. A REAL update from the fraud team. I know customers cannot contact them directly, but internal staff can - I don't want to hear another generic "they need x days" statement... they have the handset! Revert my account to what it was, sim 30 day, and provide me with a PAC code - I'm moving on, a PAC code once activated should properly terminate my account. Thanks for reading! Dal -

Hello. I am in need of a bit of advice so figured this was probably the best place to try besides CAG (and their office is closed today apparently so they are no good for me really) I recently transfered some cash from my savings account to my current account to book a holiday. Paid for it. I'm not sure if I am going to be able to go now. I left over £1000 in my account for spending money. When trying to withdraw our spending money at the bank this morning, I was told insufficient funds. Obviously I went into the bank and was told a counter withdrawal was made yesterday for £1000. I ask how on earth this can happen, as surely a cash withdrawal would require ID. Apparently not, they just ask security questions. I asked what kind of security questions and the manager seems a bit reluctant to tell me, but it turns out simple things like address would suffice. I am getting slightly wound up at this point and ask if they used anything else to verify this withdrawal. He tells me that they dont have chip and pin machines in branch as a signature suffices.. . however my card never left my possession all day so how they could even have had a card to verify the signature is a mystery he offers to check the cctv footage but claims this could take up to a fortnight. Probably the wrong thing to do, but at this point I walked out as to be honest, I felt like I was going to completely snap. There are more security measures in place to use a cash machine than take out larger transactions over the counter! Unbelievable. I have never tried to draw out cash at the counter before anywhere, but is this the same with all banks? If so I completely understand why my grandfather used to keep bundles of cash around the house. I used to laugh at him when he said he didn't trust banks to keep his money safe and would rather take the risk of keeping it himself I got home and contacted the fraud team, who reckon theres nothing they can do as it was an in branch transaction. They can open an investigation but it can take weeks to get a reply/refund. Now, I may have to go down this route, but is there anything I could do to try and get an immediate refund? I don't feel its fair for the bank to penalize ME for their lack of security. I am currently asking around to see what cash I can lend from friends to see if I can still go on holiday. I have transferred my wages to my partners bank account until the fraud team sort this out as clearly I cannot trust my money to be in nationwide right now. .unfortunately I don't get paid til the end of the month though I am absolutely foaming at all of this. Especially the day before I am meant to be going away. I don't feel I have actually done anything wrong, yet I have no access to my own money :S

-

Many people will have been watching Tesco's recent debacle. I have lost over £5000 with the share price fall, over the last 4 months. Tough, you may say. The reality is that I bought my shares based on the financial accounting data published by Tesco in their annual report. Yesterday, I watched the new CEO Dave Lewis, parachuted in from Unilever. He said the "accounting errors" appear to have been undertaken for several years. They have declared £265 million in profits they actually don't have, and won't have. A definition of fraud is: " the intentional misrepresentation or concealment of an important fact upon which the victim is meant to rely, and in fact does rely, to the harm of the victim". I'd say that is exactly what Tesco have done. I'm tempted to issue a county court claim against them, for fraud. Any thoughts, please?

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS