Vulture_Bank

-

Posts

273 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by Vulture_Bank

-

-

just to put a link to events in parliament today concerning vulture funds and a private members bill getting an unopposed second reading.

all speakers found the existence of thes funds abhorrent.

-

today the Debt Relief (Developing Countries) Bill 2009-10 private members bill

Type of Bill:Private Members' Bill (Ballot Bill)Sponsor:Andrew Gwynne

got a 2nd reading unopposed {sadly due the the forthcoming election it could eventually fall by the wayside unless it is effectively "fastracked"}

vulture funds purchase sovereign debt and make vast fortunes via the british courts[very similar in theory to the way companies like cabot etc purchase debt ]

all parties in parliament find this procedure abhorrent.

http://services.parliament.uk/bills/2009-10/debtreliefdevelopingcountries.html

the point is these MP's who speak positive about this bill including Andrew Gwynne need to be made aware of the debt purchasing companies and their dubious tactics etc here in the UK

-

The judge said that he accepted it was a fiche copy of an application form. He also said that as there was a statement from 8 years ago (the last time) I used the account with a balance of 6kish on it, he was happy with that.

The case law and acts were not commented on once. No argument was entered into and I felt I was just talking to myself.

To rub salt into the wound a representative from Cabot attended and presented a bill for an overnight hotel stop and train fair of £400. This was granted too. Don't forget we were in a small claims court here?

Stebiz

how did this get into small claims court when the amount is clearly over £5,000?

no need to say in open forum

-

after todays debacle of the rbs share price ( down approx 65%) to 11.8 pence ?

the following post might be of interest to rbs credit card holders

http://www.consumeractiongroup.co.uk/forum/show-post/post-1928576.html

-

Failure to notify cardholders of the transfer of receivables could delay or reduce payments on your notes.

No notice has been given to cardholders of any transfers previously effected, and no notice is

expected to be given to the cardholders of any future transfers of receivables to the receivables trustee. The receivables trustee has agreed, amongst other things, that notice of the transfers will not

be given to cardholders unless RBS’ long-term senior unsecured indebtedness as rated by Moody’s, Standard & Poor’s or Fitch Ratings were to fall below Baa2, BBB or BBB, respectively. The lack of notice has several legal consequences that could delay or reduce payments on your notes.

Until notice is given to a cardholder and, where necessary, a legal transfer of the receivable is made, the cardholder will discharge his or her obligation under that designated account by making payment to the relevant originator.

Until notice is given to a cardholder who is a depositor or other creditor of that originator, equitable set-offs may accrue in favour of the cardholder against his or her obligation to make payments to that originator under the designated account. These rights may result in the receivables

trustee receiving reduced payments on the relevant receivables. The transfer of the benefit of any receivables to the receivables trustee will continue to be subject both to any prior equities that a

cardholder has and to any equities the cardholder may become entitled to after the transfer. Where notice of the transfer is given to a cardholder, however, some rights of set-off may not arise after the

date notice is given.

Failure to give notice to the cardholder means that the receivables trustee would not take priority over any interest of a later encumbrancer or transferee of the relevant originator’s rights who

has no notice of the transfer to the receivables trustee where such later encumbrancer or transferee gives notice. This could lead to a loss on your notes.

Failure to give notice to the cardholder also means that the relevant originator or the cardholder could amend the credit card agreement without obtaining the receivables trustee’s consent. This

could adversely affect the receivables trustee’s interest in the receivables, which could lead to an

early redemption of or a loss on your notes.

now in view of the fact that RBS today became a "penny stock"

the following statement seems very interesting

"unless RBS’ long-term senior unsecured indebtedness as rated by Moody’s, Standard & Poor’s or Fitch Ratings were to fall below Baa2, BBB or BBB, respectively. The lack of notice has several legal consequences "

-

suggest you refer to this thread in particular the generous offer made by pt2537 on post 5 !!!

"halsbury eat your heart out "

-

MBNA have ramped up my interest rate from 14.9% to 29.9% (they wanted 34.9% but I argued) on £9.5k - this is crucifying me.

I know the T&Cs (which I am waiting for an enforceable copy of) generally say they can increase rates but this is getting ridiculous - I have never been so much as 5 minutes late with a payment.

Are they legally allowed to keep ramping it up?

And are they breaching something as they never show the APR on the statements/online banking - it just shows the monthly rate.

What can I do?

in simple terms when foreign companies such as MBNA i(capital one ??) increase the interest rate to these "extortionate" levels when people fall on hard times as many people in authority MP's press etc need to be made aware of what is going on ..........

if they were to default you (presuming they came up with a valid agreement)

does anyone think applying for a time order would work ??

http://www.insolvencyhelpline.co.uk/debt_factsheets/time_orders.php

-

-

HI vulturebank,

I believe that you are wrong. If the CCA did "supersede" the LOP then the LOP would have been repealed or amended. Alternatively the CCA would have made specific reference to assignment of debts that would have superceded the LOP.

However, neither of these things has happened.

The CCA, in defining a creditor merely says that it is the person providing credit or:-

"or the person to whom his rights and duties under the agreement have passed by assignment or operation of law"

The rights and duties of a creditor under the agreement are still passed as an absolute assignment under the Law of Property Act. The CCA has made no change to that.

When it comes to equitable assignment, despite what has been said, this does still exist. An equitable assignment may exist where the requirements for an absolute assignment (as laid out in the LOP) are not saitisfied. The main practical consequence of an equitable assignment is that the assignee must include the assignor in any court action against the debtor. So, if a DCA has a debt under an equitable assignment then they must include the OC as a co-claimant (Weddell and Another [1988] 1 Ch 26).

There is often talk here about the likes of Cabot claiming they have taken the rights but not the duties to the debt under the LOP. This is, of course, rubbish.

Although it is a general rule that while the benefit of a contract may be assigned the burden cannot and this is what the likes of Cabot are trying to rely on they are wrong.

This is due to the nemo dat rule (Nemo dat quod non habet - "no one [can] give what he does not have" ). In other words, an assignor can assign no greater or different right than he actually has nor can an assignee obtain a greater or different right than that held by the assignor.

Basically, you can only assign something you own. When a contract is made a party does not own an obligation that it has to another party (that is actually a benefit which belongs to the other party). Since you do not own an obligation then you cannot assign it following the nemo dat rule. This is where they are coming from saying that they only purchased the rights and not the obligations.

However,agreements under the CCA are rather different from most contracts. The statute claearly points out the definition of a creditor and also lists the obligations that are required from them in order to gain the benefit of the contract.

The courts have also clearly stated that if a creditor does not follow these obligations exactly then they are not entitled to the benefit of the contract:-

1.In the case of Dimond v Lovell [2000] UKHL 27, Lord Hoffmann said , at page 1131:-

“Parliament intended that if a consumer credit agreement was improperly executed, then subject to the enforcement powers of the court, the debtor should not have to pay.”

2.Sir Andrew Morritt, Vice Chancellor in Wilson v First County Trust Ltd [2001] EWCA Civ 633 said at para 26 that in the case of an unenforceable agreement:-

“The creditor must…be taken to have made a voluntary disposition, or gift, of the loan monies to the debtor. The creditor had chosen to part with the monies in circumstances in which it was never entitled to have them repaid;”

3.When this case was appealed to the House of Lords on a matter regarding the Human Rights Act (Wilson & Ors v Secretary of State for Trade and Industry [2003] UKHL 40), Lord Nicholls of Birkenhead said:-

49 The message to be gleaned from sections 65, 106, 113 and 127 of the Consumer Credit Act is that where a court dismisses an application for an enforcement order under section 65 the lender is intended by Parliament to be left without recourse against the borrower in respect of the loan… when legislation renders the entire agreement inoperative, to use a neutral word, for failure to comply with prescribed formalities the legislation itself is the primary source of guidance on what are the legal consequences. Here the intention of Parliament is clear.

As a result, the obligation of the creditor under the CCA is an intrinsic part of the benefit. In this case the assignee must take the obligation as well as the benefit. If this were not the case then the assignee would have gained a right over the debtor greater than and different from the right of the assignor. Following the nemo dat rule they cannot do this.

Hope this has been useful and/or interesting

thanks for the excellent post

-

however their could be a fatal flaw here if the deed of assignment was not witnessed

the deed of assignment is a 4 or 5 page document

-

Law of Property (Miscellaneous Provisions) Act 1989 (c. 34)

Deeds and their execution.

1.—(1) Any rule of law which—

- (a) restricts the substances on which a deed may be written;

- (b) requires a seal for the valid execution of an instrument as a deed by an individual; or

- © requires authority by one person to another to deliver an instrument as a deed on his behalf to be given by deed,

is abolished.

(2) An instrument shall not be a deed unless—

- (a) it makes it clear on its face that it is intended to be a deed by the person making it or, as the case may be, by the parties to it (whether by describing itself as a deed or expressing itself to be executed or signed as a deed or otherwise); and

- (b) it is validly executed as a deed by that person or, as the case may be, one or more of those parties.

(3) An instrument is validly executed as a deed by an individual if, and only if—

- (a) it is signed—

- (i) by him in the presence of a witness who attests the signature; or

- (ii) at his direction and in his presence and the presence of two witnesses who each attest the signature; and

- (i) by him in the presence of a witness who attests the signature; or

- (b) it is delivered as a deed by him or a person authorised to do so on his behalf.

(4) In subsections (2) and (3) above "sign", in relation to an instrument, includes making one's mark on the instrument and "signature" is to be construed accordingly.

(5) Where a solicitor or licensed conveyancer, or an agent or employee of a solicitor or licensed conveyancer, in the course of or in connection with a transaction involving the disposition or creation of an interest in land, purports to deliver an instrument as a deed on behalf of a party to the instrument, it shall be conclusively presumed in favour of a purchaser that he is authorised so to deliver the instrument.

(6) In subsection (5) above—

- "disposition" and "purchaser" have the same meanings as in the [1925 c. 20.] Law of Property Act 1925; and

- "interest in land" means any estate, interest or charge in or over land or in or over the proceeds of sale of land.

- (7) Where an instrument under seal that constitutes a deed is required for the purposes of an Act passed before this section comes into force, this section shall have effect as to signing, sealing or delivery of an instrument by an individual in place of any provision of that Act as to signing, sealing or delivery.

(8) The enactments mentioned in Schedule 1 to this Act (which in consequence of this section require amendments other than those provided by subsection (7) above) shall have effect with the amendments specified in that Schedule.

(9) Nothing in subsection (1)(b), (2), (3), (7) or (8) above applies in relation to deeds required or authorised to be made under—- (a) the seal of the county palatine of Lancaster;

- (b) the seal of the Duchy of Lancaster; or

- © the seal of the Duchy of Cornwall.

(10) The references in this section to the execution of a deed by an individual do not include execution by a corporation sole and the reference in subsection (7) above to signing, sealing or delivery by an individual does not include signing, sealing or delivery by such a corporation.

(11) Nothing in this section applies in relation to instruments delivered as deeds before this section comes into force.

- (a) the seal of the county palatine of Lancaster;

- (a) restricts the substances on which a deed may be written;

-

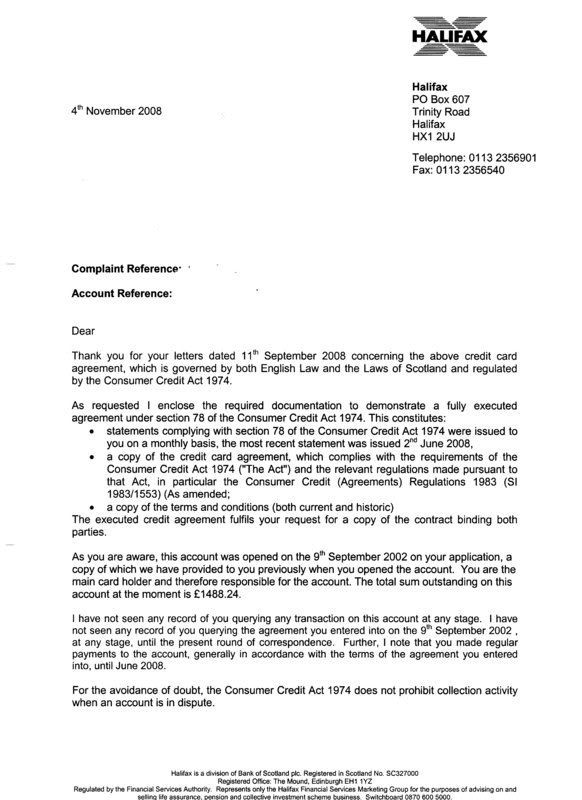

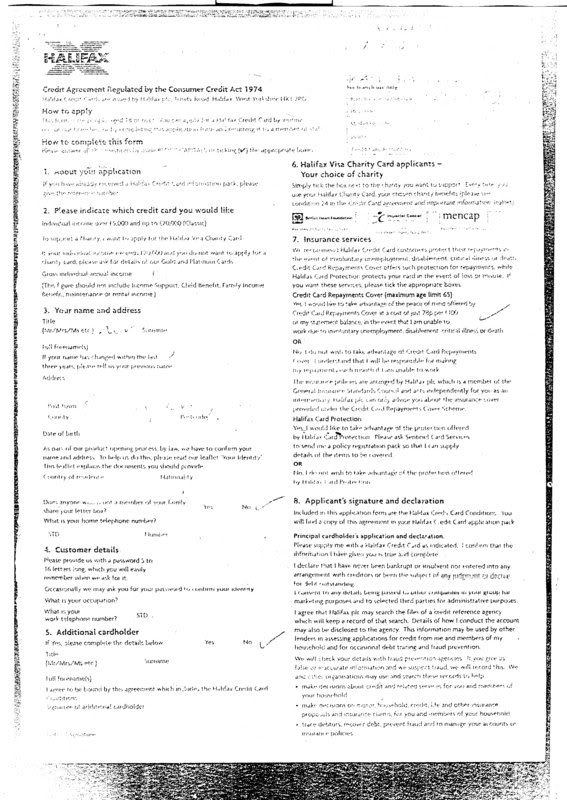

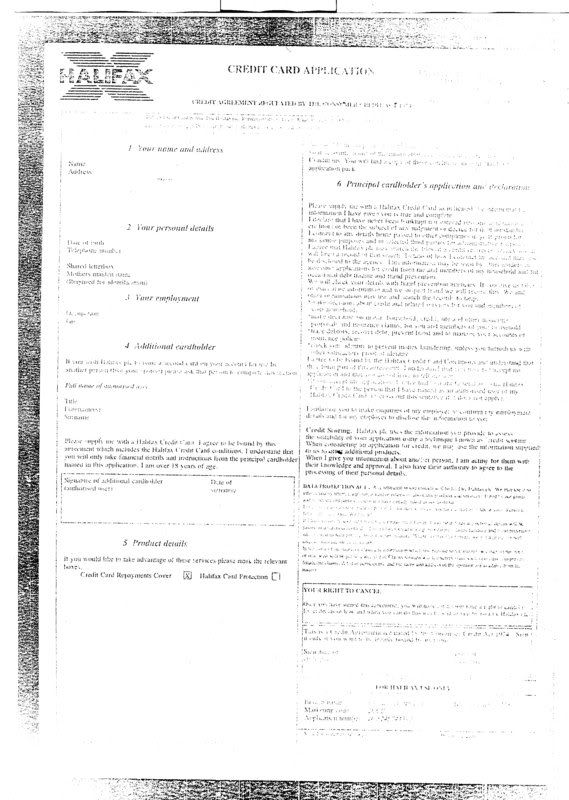

Hi

Received my CCA from Halifax today, As you look at it its not my scanner this is how i received the paper work.

I haven't added the terms & condictions as there the latest version, and not the terms and conditions that i took out originally.

Gaz

I HAVE BEEN TOLD THAT HALIFAX have been sending out a lot of the "same " cut and paste letters recently signed by different members of staff.

how do the laws of scotland apply ????? in england

-

At one point, a while ago, we were under the impression that an application form was not enforceable for the reasons you state. It turns out that that may be the case, but only if a contract was never executed afterwards - in that case the application form would not be evidence that a contract existed.

In your case, though, the application form is actually dual-purpose - it is an application form but it is also a credit agreement. Once it is signed, [can you explained why party you are referring to here , the applicant or the original creditor]it becomes the contract and is no longer 'pre-contractual'

any update on this thread

have been reading it but have noticed that the two halves of the document on post 1 do not fit together properly , part 1 has the start of a signatory box for the creditor, but it does not show on part 2

-

If I may offer comment in this matter; from my experience while the CPR and relevant PDs appear to be unequivocal in providing for original documents to be made available for inspection at the disclosure stage and at the hearing, in practice the defunct “Best Evidence” rule is no longer applied by the Courts in favour of copy documents being acceptable – however the weight of evidence given to copy documents (certified in writing as true and accurate copies) can be considered less than if the originals are produced. Should an actual witness take oath and give evidence as to the accuracy of a copy document - subject to cross – this will bolster the weight given the copy document.

Notwithstanding the above; I have known cases when the Court has ordered the original credit agreement to be lodged with the Court or the Claim will be struck out, when the DCA has been unable to provide legible T&Cs and at final trial when originals where produced by a Claimant bank without any T&Cs attached.

I would suggest that the disclosure stage is a great opportunity make or break a Claim – particularly against an Assignor DCA etc.

Hope this helps.

Regards - RS

Richard

can i develop a hypothetical situation from the above post imagine the copy agreement was dated say , (pushing the situation to the extreme) 1993, would i be correct in assuming that;

"Should an actual witness take oath and give evidence as to the accuracy of a copy document "

then that person must have been employed by the company in the relevant year 1993 in this case,,,,

consequently the defendant might have a right to demand proof of this fact ??? relating to the years of service ???

-

"MELTON MOWBRAY" "PORK-PIES" ?

remember in AUGUST 2007

Barclays dismisses fears over debt problems - Liverpool Daily Post.co.uk

-

in the Usa (due to lobbying by a major US bank) it is believed [the law was changed in the last few years ] that people now pay their credit cards before their mortgage. ........... yes it is hard to believe.

moreover in the usa if you own two properties [not one ] you can go to court and get the judge to change the terms of your mortgage -- interest rate etc ....

-

BBC NEWS | Business | Barclays faces investment lawsuit

Barclays faces investment lawsuit

quote "Barclays is being sued in a New York court over claims it moved loss-making investments from its own accounts to those held by outside investors.

The losses to investors are alleged to total hundreds of millions of dollars.

The case is being brought by a French company which claims it was told these investments - known as "SIV-lites" - were super-safe and offered a AAA or AA rating.

But Barclays denies the allegations and told BBC File On 4, that the action has "no merit."

The case against Barclays centres on two complex investments - one called Golden Key and the other called Mainsail - which the bank created to sell to outside investors.

The company alleges that in the summer of 2007, at a time when the sub-prime crisis was growing, Barclays arranged for hundreds of millions of dollars worth of mortgage-based securities to be transferred from its own accounts to the two SIV-lites.

The French company's US lawyer Geoffrey C Jarvis said that Barclays should have known in June 2007 that such mortgage-based investments were "substantially impaired."

He added: "I can't say what Barclays knew because they haven't told me but if they didn't know they were certainly reckless in not knowing."

Barclays refused to discuss the case with the BBC but in a short statement said: "This action has no merit and we will contest it vigorously."

"

-

I beleive Prof Roy Goode and Francis Bennion may have some influence on this subject.

see gareth thomas MP's 's statement regarding the banks being unable to enforce any agreement whilst in default, under section 78 cca and the fact that

http://i283.photobucket.com/albums/kk289/42man_2008/HOC-1.jpg

http://i283.photobucket.com/albums/kk289/42man_2008/HOC1-1.jpg

since gareth thomas is part of the government it is suggested that the

songs to be sung should be "sung from the same hymn sheet" :

hence the potential minor shareholder in say RBS (eg current management of RBS etc etc ) should act in accordance with the statement made by gareth thomas regarding banks themselves entering into default.

-

Not a legal source but may help with regard to microfiche etc:

Document Scanning Scotland, Edinburgh, Glasgow, UK - DDSR Digital Document Scanning & Retrieval

quoting from above

"The Civil Evidence Act (1995) introduces a flexible system whereby all documents and copy documents, including computer records, can be admitted as evidence in civil proceedings. A judge will still have to be persuaded to treat that evidence as reliable, therefore organisations will have to prove the authenticity and reliability of the record."

assuming the The Civil Evidence Act (1995) came into effect some time in 1996

the question is is this law retrospective ??

meaning if the agreement was dated 2004 it does not apply ??

-

on the subject of assignment here is an interesting paragraph

remember these words were said circa 1902 ??? slightly before the cc act 1974

" Legal assignment of an equitable chose:Although section 136 LPA 1925 appears to apply in terms only to legal things in action, it is thought that the use of the word "trustee" in the list of persons who may be liable in respect of the thing in action militates against a restrictive interpretation. There is also some case law to support the view that equitable things in action are included in its scope. In one of the leading cases (Torkington v Magee [1902] 2 KB 427 at 430-431), Channell J said:

"I think the words "debt or other legal chose in action" mean debt or right which the common law looks on as not assignable by reason of its being a chose in action, but which a Court of Equity deals with as being assignable". "

-

RE HODGSON / CABOT SOLICITORS

the solicitors regulation authority -- code of conduct rule 11

Litigation and advocacy

states " Introduction

Rule 11 imposes additional duties on you if you are a solicitor, an REL or an RFL whenever you exercise a right to conduct litigation or act as an advocate. "Court" in this rule has a wide meaning – see rule 24 (Interpretation). References to appearing or acting as an advocate apply when you are exercising rights of audience before any court, not just if you have been granted rights of audience in the higher courts. The rule only applies in a modified form to overseas practice – see 15.11.

Rule

11.01 Deceiving or misleading the court

- (1) You must never deceive or knowingly or recklessly mislead the court.

(2) You must draw to the court's attention:- (a) relevant cases and statutory provisions;

- (b) the contents of any document that has been filed in the proceedings where failure to draw it to the court's attention might result in the court being misled; and

- © any procedural irregularity.

[*](3) You must not construct facts supporting your client's case or draft any documents relating to any proceedings containing:

- (a) any contention which you do not consider to be properly arguable; or

- (b) any allegation of fraud unless you are instructed to do so and you have material which you reasonably believe establishes, on the face of it, a case of fraud. "

[*]Solicitors Regulation Authority - Code of Conduct: Rule 11

- (a) relevant cases and statutory provisions;

if it were me if the above is deemed relevant i could contact the solicitors regulation authority

and in any court case present a copy of the section of halsbury regarding assignment

- (1) You must never deceive or knowingly or recklessly mislead the court.

-

I've got a question regarding the contents of my S.A.R to Experian. In amongst all the paperwork one of the account numbers supplied, which relates to my RBS entry, is not the same account number as what it should be. So I queried it with Mr Hancock, and his reply was this...

"The account numbers RBS (Mint) submit to us are encrypted and so may not be recognisable. If you require further information about this entry I suggest that you contact them directly..."

Well, the account number they have supplied looks very much like an account number and certainly doesn't look encrypted. And it certainly doesn't look like my account number, apart from the first 8 digits.

Should I really be making a big deal with this? The rest of the details "look" like mine.

p.s. great thread, I would never have thought to S.A.R the CRAs without this

the account number could well be a new account number designated to the account by rbs on default [or charge off ??] of the account (naturally without your knowledge ) mbna do this and the matter is currently being investigated by higher authorities ................... are mbusa involved in the rbs account ?

-

I've got a question regarding the contents of my S.A.R to Experian. In amongst all the paperwork one of the account numbers supplied, which relates to my RBS entry, is not the same account number as what it should be. So I queried it with Mr Hancock, and his reply was this...

"The account numbers RBS (Mint) submit to us are encrypted and so may not be recognisable. If you require further information about this entry I suggest that you contact them directly..."

Well, the account number they have supplied looks very much like an account number and certainly doesn't look encrypted. And it certainly doesn't look like my account number, apart from the first 8 digits.

Should I really be making a big deal with this? The rest of the details "look" like mine.

p.s. great thread, I would never have thought to S.A.R the CRAs without this

there is a well known mathematical formula as to whether a 16 digit number can potentially be a valid credit card account number and it is very easy to determine

-

just so we all remember

1.8 What if an agreement is entered into before 31 May 2005?

If a regulated agreement is executed before 31 May 2005, it is subject to the 1983 Regulations but not the 2004 Regulations.

If it is executed after that date, but is signed by one or more parties before then, it may benefit from transitional provisions

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

Friends father died with no will but debts

in Financial Legal Issues

Posted

sorry to say this but i have seen a recent set of credit cards terms and conditions -- with a section --- if/when you die and the company definitely wanted their money owing if/when you die ---- suggest you get a set of t & c from santander and check it out.