davey77

-

Posts

2,650 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by davey77

-

-

lexis200 - Tell me more...

Tell me more too

-

That's ok if you are just starting out and it's good to build a pile of correspondence as evidence but eventually it's a pointless task.

After getting through aprox 11 DCAs per account over 2.5 yrs i have found it's best to go after the OC (original Creditor) unless the account has been sold outright.

Fine to send a CCA request to a DCA to put them into check but it's most likely that many of the letters sent to DCAs (particularly in-house ones) are not even read for the most part.

The only solution a DCA wants is £££$$$ cash. Nothing else will get them communicating in a professional manner.

But then again.. you may get lucky

By all means keep writing.. i'm an old hand and 30 odd DCAs later i like to use my printer for nicer jobs like printing photos of next door's cat.

-

-

Onwards and upwards.. waiting for a reply from another one now...

-

Sent this to a Solicitor this morning:

"I am currently seeking legal advise on the best way forward in dealing with Credit Agreement issues i have with 3 Lenders and am writing to ask if you would kindly offer your opinions and/or the direction to take.

Long term situation is as a Carer on Maximum Carer\'s Allowance + Income Support. (looking after my elderly mother).

HFC Bank Credit Card (09 June 2004) Balance: £5,035. CCA1974 (s77-79) response: Single page application form. Signatures of Lender and Borrower, No Prescribed Terms. Just T&Cs leaflet.

RBS (Mint) Credit Card (22 May 2004) Balance £5,190.

CCA1974 (s77-79) response: As Above

American Express Credit Card (15 June 2004) Balance £1,500. CCA1974 (s77-79) response: As Above

Previous Solicitors claim letter (s60, s127, Wilson) to discharge liability ignored for the most part. Legal Aid exhausted.

D.O.B: *******

Status: Single

Savings/Assets: Nil "

Reply:

"I regret that we are unable to advise in circumstances where legal advice has already been obtained - it would be unprofessional of us to do so."

So i said:

"Perhaps i was unclear.. Legal Aid exhausted and Solicitor is no longer dealing with my cases in any way."

Reply:

"We are unable to assist. It is our policy not to take over cases part way through."

Probably just the fact that my issues are not going to make them very much money but they didn't have the professional courtesy to say so. And yes, they did make the last sentence blue.

-

Hi joemay, well had a little look at your thread i would say the chances of a write off (no matter how dire the circumstances) are slim to say the least. Especially with the likes of Halifax and their in-house Blair, Olivier and **** on the case.

I tried that and got nowhere with many creditors. Requests for a write off were ignored or responded to with 'we cannot write this off at this time' etc

I think it's a good idea that if you did ask for a write off then head it without prejudice so it can't be used against you later but if you feel your agreement is invalid then i would pursue that line rather than waste too much time on asking for mercy from organisations that don't know what that word means.

The only thing that is sure fired to get them to considering wiping out a debt is publicity: Major newspapers, Tv or BBC Watchdog intervention and that's hard to get as i have tried myself.

I would just concentrate on any unlawful charges aspect and start building a case against them to get an LBA sorted when you are ready to do so. Can't remember if you have gone down the CPR 31.16 route.. that's always worth a try.

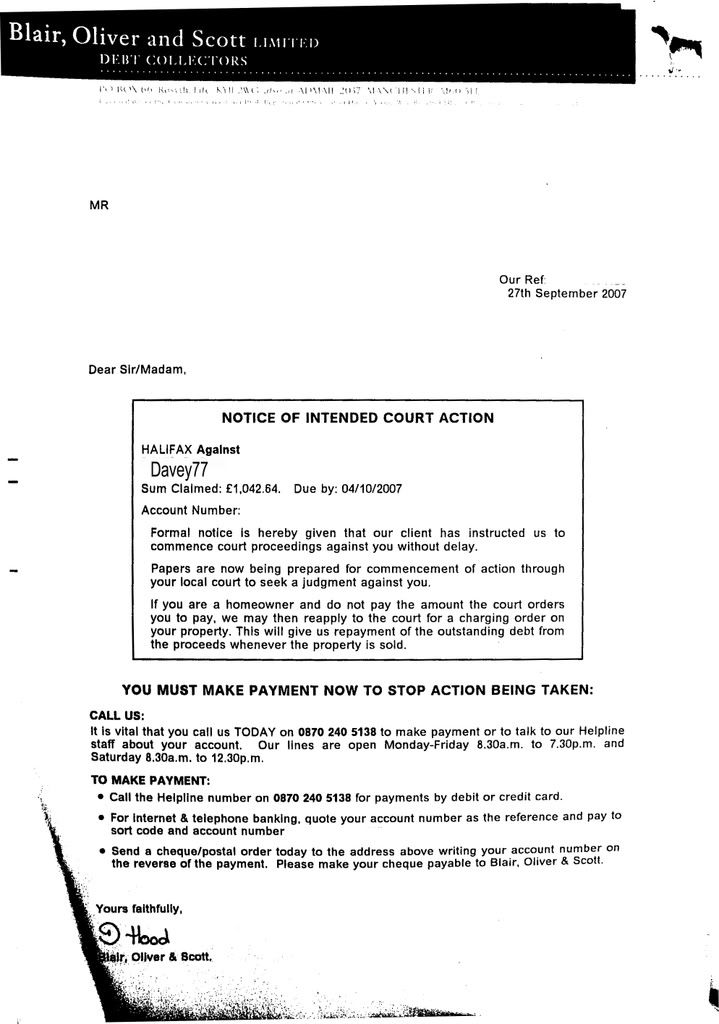

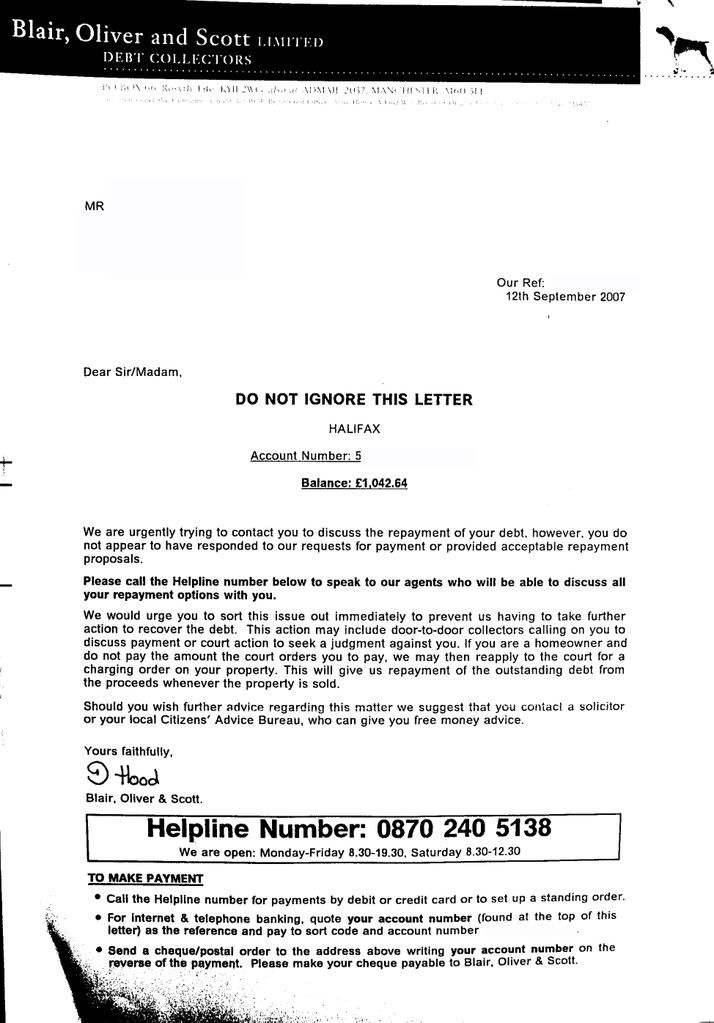

I would also not bother too much corresponding with BOS. They never reply from my experience. Here are a few examples that you will probably get if you haven't had them already:

http://i157.photobucket.com/albums/t42/davey77_2007/5copy.jpg

http://i157.photobucket.com/albums/t42/davey77_2007/1copy-1.jpg

http://i157.photobucket.com/albums/t42/davey77_2007/6copy.jpg

I would send them at some point if you don't get anywhere a final letter along these lines of:

" As i have already made my position clear i fail to see the need to reiterate the situation and suggest that you recommended to your 'client' that they commence Legal Action (as stated in your previous correspondence on more than one occasion) as we have reached an impasse and this matter cannot be amicably resolved otherwise.

I shall therefore look forward to receiving your client’s Claim through the (name) County Court at the earliest opportunity and any other template communication from you that i feel is not pertinent shall be read and filed for future evidence but not replied to as you may consider this is my final response."

Adapted to your needs and after that deal with the organ grinder (Halifax) directly and not their Monkey (BOS).

-

1

1

-

-

For anyone battling to get fairness and impartiality with the FOS i suggest going through reallymadwoman's other very helpful threads:

-

Good luck with it anyway david999.

This has already been posted elsewhere put putting it up here for others to read:

-

I did disagree with the adjuicators conclusion and it is now being reviewed by an actual "ombudsman" in which i hope the know more abaout the law than their adjudicators..

They are not interested in the law. They are interested in protecting their buddies (former work colleagues) in the banking industry

I imagine when the banks legal department recieved the adjudicators conclusion, they must have been more suprised than me, i'm assuming there having a party, considering this claim is for £100k loss of investment and business.

They would have been more surprised if the FOS upheld any part of your complaint as the Bank generally expect the FOS to back them up as a matter of normality.

It begs the question, who are these adjudicators and what qualification do they hold?

http://www.financial-ombudsman.org.uk/about/panel-ombudsmen.html

Former bankers, building society workers and associated "independent" sorts

Some of you's could end up with th is same adjudicator investigation your cases, so i'm just letting you's know what your up against.

Part of my evidence was based on knowlege of the building indusrty and how it works, the adjudicator admitted on the telephone "he has no knowlege of the building industry or how it works" So How the hell can he then judge the stage payments did not delay the build???.

on the breach of contract i asked him.

If a person is in court, accused of a crime, and the accused stands up and says "yes it was me, i did it, but i didn't mean it" does the judge then stand up and say "oh everybody!, he didn't mean it, it was a wee accident, off you go home now, and don't let it happen again"

The adjudicators reply was " you can't compare that to your case"

In future i wouldn't have conversations over the phone with them as what they say on the phone and what are willing to say in writing can well be different or watered down (the burden of proof then being on you that what they stated on the phone actually took place etc)

Just a final point.

During the process of applying for this loan the bank asked me to make projected estimations of costs, so in may 2007 i produced estimated cost showing a cash balance of £6000 at the end of the build,, the build started May 2008 and finshed end of November 2008,, this is 18 months, 1.5 years between the estimation and the completion,,

on completion there was £3000 left in the bank. taking into consideration, "1.5 years" "inflation" change in econemy" The Adjudicator asked me "where's the missing money" "where is the missing £3000" as you can imagine, i nearly fell of my seat when i read this..

In otherwords implying you were committing fraud!

I immediatly challenged him to present my estimation and actual costs to any bank or financialy expert with knowlege of the building industry and suggested they would be very pleased with these numbers, in fact they would be suprised this project never finished over budget, never mind actualy having £3000 left at the end.

Adjudicators reply: refused my challenge and refued to comment.

Sounds like the FOS

I hope the "ombudsman" who will review my case He or She has the full knowlege of the law, and the knowlege to judge this case, and if not, they would atleast investigate the points they lack knowlege in, before giving their decision.

david999

They know exactly what they are doing im afraid. I would seriously consider not doing much with the FOS and going straight to Court with all this personally.

-

...My cynical minds rings alarm bells here thinking, 'hmm, did he leave and take up new employment with a certain 'financial institution'? I bet he/she no longer is employed by the Ombudsman service. To me, yet another seemingly error of judgement by an unbiased body!

Michael

Probably the other way around.. the employee's previous role was most likely within the finance industry/banking sector before he/she started work at the FOS and therefore partly why you get these types of decisions.

-

They know the Law.. they just choose to ignore it quite often. The FOS stance is (and one that seems backed up by the government) that they "take account of the law but do not enforce it" which is what i have had quoted to me and which is a joke to say the least.

More on the lovely FOS and what i think of them is here for your interest:

http://www.consumeractiongroup.co.uk/forum/general/183738-why-does-fos-take-2.html#post2016037

You can often get a different opinion of an actual Ombudsman compared to an Adjudicator it has to be said, so good luck with that..

-

subscribing.

Well done!

Thanks!

Just to say.. haven't heard a peep out of them (and of course don't expect to either). 8-)

-

Explain to a thickie the precise implications of this please?

It means the Rankines will have to go out and get a proper job now

-

They want £35 per statement?! No way.. Do you have that in writing? If so i would make complaints about that to TS/OFT.

If you want the statements and everything else they have on you i would send a SAR. That's £10 and you will (should) get everything they hold on you.. including statements for the life of the account.

-

Was bound to happen eventually

-

So the bank admits breach of contract and the FOS don't even take that admission into account.

That whole saga stinks to high heaven. I hope you made it clear you didn't accept the FOS findings. An FOS decision is only legally binding when the two parties agree to it. And you have to be careful that, even though you disagree, the FOS don't write to you stating 'you agree with our decision'.

"Accidently ommited from the legal contract" says the FOS.. exactly. A LEGAL CONTRACT that the opinion of an FOS employee has no legal bearing upon.

-

So the bank admits breach of contract and the FOS don't even take that admission into account.

That whole saga stinks to high heaven. I hope you made it clear you didn't accept the FOS findings. An FOS decision is only legally binding when the two parties agree to it. And you have to be careful that, even though you disagree, the FOS don't write to you stating 'you agree with our decision'.

"Accidently ommited from the legal contract" says the FOS.. exactly. A LEGAL CONTRACT that the opinion of an FOS employee has no legal bearing upon.

-

hmmm sorry but at a quick glance looks ok to me.. both signatures and monthly payments, total amount payable showing etc

As it says at the bottom right.."the lender shoud have given you a copy 7 days before signing it etc', although even if they didn't i don't see how you could prove that conclusively.

All i can suggest is that you check the APR amounts/figures for major discrepancies.

Others may have further thoughts..

-

I did ask a couple about tenant requirements with a poor credit file and they said any blemish on a credit file would mean they require a guarantor

Yeah sure.. could ask them to do a trial run as it were (without having a property to go for) and see what comes back. I might be pleasantly surprised.

Then i just need to find an agent that doesn't think most on carers allowance/benefits are dodgy

I'll sort those adds out!

Got to get out of Devon that's for sure!

Cheers

-

-

Can't really say what approach they will take with you to be honest. They will probably do what ever makes them the most money which is the plan B. i suspect. Hitting you with charges as much as possible.

Suppose it's tricky to get a new account (with a large overdraft) and ditch lloyds is it?

-

Well if you put your cursor over that FOS link you'll read what this site thinks and if you want to know what i think of them then here is something to read sometime:

http://www.consumeractiongroup.co.uk/forum/general/183738-why-does-fos-take.html

-

-

{kind=link}

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

BOS/Halifax

in Debt Collection Agencies

Posted

Looks like this one?

http://www.consumeractiongroup.co.uk/forum/halifax-bank-bank-scotland/208820-section-78-write-off.html