SHERLOCK

-

Posts

384 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by SHERLOCK

-

Hi, Thanks for replies. I was surmising on fees as the £275 & £75 was all I could find. The council have just said that the amount owed is £180.00, with no breakdown. I think my daughter will need to go in and ascertain actual charges. Should Jacobs have issued a 'further notice of enforcement ' letter to the new address without previous letters? Assuming they sent them, maybe to previous address. Regards, Sherlock

-

Hi, It was more threat of ccj re: credit file. Lady at council says no final notice for council tax was sent and daughter is on the system at new address as at 1/5/15 as landlord registered her at the address. Regards, Sherlock

-

Posts have crossed lookinforinfo. I agree it was avoidable however, my daughter is going to apply for mortgage shortly and doesn't want it going any further obviously. Do you think a letter of complaint, offering the £75 will be the route? Regards, Sherlock

-

Hi DX, Paid April instalment 15th - May 15th. Moved out end of May so does owe something (2 weeks I assume) CT was £126.00 month. Council are saying that the chasing is for the balance. The further notice of enforcement just states £495.00 owed, no breakdown on fees / c tax / dates etc. Am I right in thinking a notice of enforcement is entered once an agreement is in place and is broken? So no idea what a further notice of enforcement is. No agreement was entered into and this is the first letter received. Regards, Sherlock

-

Hello, Been a while since been on here. Advice for my daughter please. She moved out of a property May 2015 and received a 'further notice of enforcement ' sent to her new address today. Bill was £495. Rang council - apparently £185 council tax £310 agent fees. My daughter didn't officially notify the council she was moving out but did start paying council tax immediately from new property. I guess my question is where does responsibility lie? Can fees be challenged? It turns out CT owed is not outstanding amount, is actually less but apparently you pay a full month and then it is refunded! No letters were passed on to my daughter from old address and council says Agents must have been searching for my daughter. Couldn't make it up, she is on electoral registered and paying council tax in her name. Any / all advice is welcome please as to next step. I have told my daughter not to contact Jacobs, go to council, pay outstanding CT over counter in cash and hand them a letter of complaint about Jacobs as she hasn't received any letters. Are there any forms on this site relevant or will it be ad-hoc letter? Regards, Sherlock

-

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

multiple replies for some reason!! -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

multiple replies for some reason!! -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

multiple replies for some reason!! -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

multiple replies for some reason!! -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Hi Andrew, Rhia, OK, I worked out my compounded interest and submitted to Barclaycard (received nothing yet), however, also sent the repayment request for Morgan's notice and a redrafted 'Tomlin Order' with the figure reduced by the repayment amount. Cabot agreed to it, returned the order signed, and all I have to do now is sign it and send it back. £400 charges increased with compound interest to £1350. I think this is maybe the best I could hope for without going to court, although I am sure this is still a healthy profit for Cabot on this account. It is also a reasonable monthly payment. Not sure what happens with the Monument / Barclaycard request? Would it be the case that Cabot have ok'd this with Barclays? Thanks, Sherlock -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

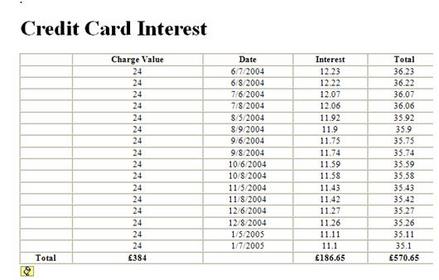

They're a real pain in the *rse me thinks. Struggling with the compound interest thingy, can someone enlighten me?? Heres a list of charges + dates, regards, Sherlock

-

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Thanks Rhia, can you inform me where you got the compound calculator please, will have to go down that route me thinks. I will put it to Cabot, they seem to be the one's sending out statements etc. but will fall back with Barclaycard if they have a problem with it. As an aside, I went to hand in a request for an extension to the stay (had 3 previous to this) and was told that they are now charging 40 pounds a time. I asked why I hadn't been charged before and they said they hadn't been charging out of error. They have now sent out lots of letters to various businesses to inform them of this new stance!! Anyway, I didn't pay it so it is destined for a hearing now. Regards, Sherlock -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Don't think the charges and interest will cover 4000 so will need to obtain largest amount possible. 2 payments per month of 24 pounds each between 06/2004 and 01/2005. Was using the 'complex-credit-card-calc' but it says: The calculations do not compound the interest, i.e. interest on previous unlawfully charged interest has not been included. While we are at it, I saw a solicitor this morning (family friend, unpaid) and his best advice (he doesn't cover consumer law) after looking through my papers was to work out a reduced figure and monthly payment, and write my own Tomlin Order! Suggestions? -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Hi all, I am just recalculating the charges/fees on this credit card account and would like to know where / how is my interest worked out - I have 2 interest rates- merchandise interest at 1.666% and Cash interest at 1.999% monthly. Thanks, SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Lots of information Rhia thank you, however, Morgan / Cabot haven't actually taken ANY money off the account balance, Monument/B'card did this but only to break the debt down to actual money items purchased and fees that had been added. Morgans claim is for the full amount of 3900. With any/all charges taken off the debt amount (without interest ) would be nearer 3000. Thanks again, SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

I haven't counterclaimed because I wanted to get the whole thing rendered unenforceable. cASH INTEREST 1.999% and MERCHANDISE INTEREST 1.666% (MONTHLY) Morgan's state they refund to the account as a process in preparation for assignment where they split different items into different accounting books, however this does not represent a decrease in the balance of the account!!!!!!! cabot still claiming the 3900. Problem is how do I put together a case to get it thrown out, gonna look for the interest calculator. IS IT A CASE OF LISTING ALL THE ERRORS WITHIN THE CLAIM, EXPLAINING THEIR RELEVANCE TO THE CLAIM, AND THEN ASKING FOR A DISCONTINUANCE ON THE OFFICIAL FORMS? SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

yep, def SC. Got all paperwork in front of me now. Looking back my original defence was to rely on the case of Wilson & Ors 2003 and sect 61 CCA 1974 and Sch.6 of the 1983 Regs. I requested various documents and, as stated in above post, they said they do not have to send them as they had not been referred to / no requirement to provide in law or at all! This was also the case with the DoA, but they said they will send it once it is retrieved from their archive (not received as yet, letter dated 14th July 2010). I do have recourse with regard the charges applied 400 pound over 7/8 months. and this also renders the claim amount (as on original claim form) redundant. Additionally, they sent statements for '03 - '05, and they state that no earlier statements are available because they have been destroyed by the assignor. On this note they also state the statements show a complete record of the accrual of the outstanding balance because as at that date 31st October 2003 the account had a zero balance - However, when I looked within a credit file showing this account, where there is a series of zero's (to outline missed payments) half way thru, it shows a 1 and a 2, indicating that within the period prior to '03 I missed payments and as such will have been charged. cash and purchase interest and fees were continuing to be added from when I made my last payment June '04 -Feb '05. The bal 3100 ended on 3900. To the rear of the statements, apparently, Monument credit all charges back to the account (1000 pound) prior to assignment to show a bal of 2950. Morgan are claiming for the full balance 3900. I am of the mind to try to get the claim thrown out as there are too many anomolies (IS THIS POSSIBLE) any thoughts, Regards, SHERLOCK. -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

OOOOOOOOOOOHHHHHHHHHHH Rhia, that hurts! Hiya cups I tried the documents thing (unofficial route) and they insist that the documents i requested were NOT part of the claim. Also, part 1 rules this out for small claims: Scope of this Part 31.1 (1) This Part sets out rules about the disclosure and inspection of documents. (2) This Part applies to all claims except a claim on the small claims track. Notice to admit or produce documents 32.19 (1) A party shall be deemed to admit the authenticity of a document disclosed to him under Part 31 (disclosure and inspection of documents) unless he serves notice that he wishes the document to be proved at trial. stayed til 8th Oct, gonna have to sort asap, getting bogged down again!! SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Fair shout pmhcfc, so what do you suggest?? Rocket science it aint, but then why am I, and 100's like me, having to defend these claims and the like with 'application form / reply card' agreements. If I refuse to pay where does that leave me with regard their County Court Claim? Are you suggesting I just don't pay UNTIL I get the requested info, and then only if they are legally correct? OR just plain refuse to pay on the basis that the 'reply card' does not conform?? I have to at least prove this though, right? awaiting instructions, SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Hi all, received reply (I was warned) of Morgans' stance with regard the CPR Request and their apparent requirement to not provide documents 'because they are not mentioned in the statement of case'. This is in regard to the DN (not required under S87 (1) of the CCA 1974) Termination Notice original creditor 'assigned balance' confirmation (not required under the Law of Property act or at all) With regard the Deed of Assignment, this is also not referred to but will however be retrieved and a copy sent. I haven't received a reply to the Notice to Admit. Having received this knock back and having sent the OC a 'letter before action' and reported them to the ICO (haven't received reply of any sort), what do I have to do to retrieve the wished for documents. I still don't get why when I SAR Barclay's that Morgan's sent me my statements....any ideas?? I am ploughing thru the Manchester thread!! Thanks , Sherlock -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

should I be putting these up by the way or is it too late to worry? They're gonna get it recorded tomorrow anyway! -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Hi Rhia, you say the original agreement, are you referring to the pictured document above (thread 133) or another document I should be getting, i.e. is there a document that Providian will have signed and sent to me? Incidentally, these were my requests under CPR Rules: 1, the Default Notice 2, the Termination Notice 3, Original Creditor ‘assigned balance’ confirmation letter. 4, the Deed of Assignment* / Sales Assignment* *where this may be contained within a master agreement that does / doesn’t contain my account then please be specific and where any sales sub-agreement for this specific account is mentioned in a paper schedule or other media but is, or may be, sold under the auspices of the master agreement mentioned above, please also provide evidence of this along with legible account details. And my Notice to Admit Facts Request: 1 that the Credit Agreement supplied does not contain the prescribed terms as per s 61(1)a of the Consumer Credit Act 1974; and 2 that any Default Notice as per s 88 of the Consumer Credit Act 1974 has not been supplied to the defendant; and 3 that the amount claimed as per your (the claimant) Particulars of Claim are incorrect (and to be determined); Barclays having provided a (part) list of default charges applied to the account that have since been viewed as penalties and as such refundable (with interest). Oh yes and this........... WITHOUT PREJUDICE I am of the mind that; due to the apparent inability / wilful retention / non – production of documents, incorrect amounts claimed and further requests / delays evident, a respectful discontinuance be made with regard this court claim. Thanks again, SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Letters Done And Sent -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

OK People, my letters defo have to go off today. Received 2 letters y'day. One from Solicitors and one from Barclaycard(Bear in mind I sent Barclays a 'Letter Before Action' for all my info under the DPA). Barclaycard sent me a 'list of all the default charges applied to the account for the last 6 years which covers the information you are looking for'. (identical letter to the reply I got for my initial subject access request under the DPA) Amazingly, it was Morgan that sent me a letter with the Providian accounts (changes to Monument from Jan '04) relating to the account from 2003 to 2005 and apparently these show 'a complete record of the accrual of the outstanding balance because as at Oct 2003 the account had a zero balance. No earlier statements are available because they have been destroyed by the assignor (Barclays), in accordance with standard banking retention policy (6 years). The final statement also show Barclays internal accounting processes in preparation for assignment where they split different items into different account books. This does not represent a decrease in the outstanding balance. (about a £1000 difference where 'credits' have been applied such as 'Purchase Fin Chg Credit', 'Late Fee Credit, 'Cash Finance Charge Credit' etc.) Quote - 'In our opinion, we have now provided sufficient documentary evidence to prove our case and invite you to consider signing the previous enclosed Tomlin Order'. a few points to consider: Am I to assume they keep a copy of the 'agreement' dated 2000, yet destroy other paperwork between this and the 6 yr deadline? Who is my argument with and do Morgan have the right to access my account statements? Do I alter my letters in anyway, am I still to proceed with my requests for ALL my info. Is it correct that they shouldn't be going into court without original DN, Notice of Assigment etc. (what if these were destroyed?) are Morgan correct to state they have enough to 'prove' their case? Before charges applied, account was at 3000, account suspended and 7 months later 4000! Thanks again for all your advice, SHERLOCK -

Cabot Financial - Defending a court claim

SHERLOCK replied to SHERLOCK's topic in Financial Legal Issues

Can't quite decipher the 'reputation' note received......can anyone enlighten me on the sender?? SHERLOCK

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS