steve806

-

Posts

157 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by steve806

-

Eric The advice under heading 'ignore' in post 12 says to send a copy of my letter to the landowner to the parking company so that is what I did.

-

Eric, I am a bit confused by your response. I was encouraged to read other threads and followed advice from keywords which suggested I should write to the landowner and copy in the Car Parking Company to: 1. Refute the debt 2. Ask if they had given legal authority to the Car Parking Company 3. ask how the figure of £100 was calculated Are you saying this was the wrong thing to do? best Steve

-

Hi All Following research on the site and kind advice given I wrote to Brighton Met College who own the car park and sent a copy to UK Car Park Management. In my letter I advised the college I did not accept the charge was fair and reasonable. I asked if they had given authority to take legal action on their behalf and asked how the charge of £100 was made up. To date the college have not responded but this morning I received a letter from CPM. In paragraph 1 they reassert their position that I was illegally parked. In paragraph 2 they advise that although they do not own the land they have a legal contract with the landowner that entitles them to issue PCN's. Paragraphs 3, 4 and 5 provide a lengthy explanation of how the the charge has been set in accordance with Parking Eye v Beavis, has then been ratified by the Supreme Court and as a consequence has ended the debate regarding the genuine pre-estimate of loss. They advise that if my claim is for disproportionate fee it cannot be used as a reason for appeal. They encourage me to read a copy of the judgement which provides clarity for the Parking Industry and warning that in court they will refer to this judgement in evidence. I guess this is probably a standard set of paragraphs to all disputes? Am I correct? Paragraph 6 states that a decision has been made and I should now pay the debt owed. They advise as I have not engaged with the IAS Standard Appeal within 21 days I can now only appeal through the Non Standard Appeal Service. They commit to engaging with the service if I submit an appeal within 21 days. Last paragraph states how I should pay and warns of extra charges if I don't. Should I respond to them? Should I chase the landowners for a response to my letter? Advice welcomed.

-

today I have received a 'Formal Demand' which says payment is overdue and that if I do not pay within 28 days of the date of this notice the fee will rise from £100 to £149. Of course the notice is dated 5th July and didn't arrive until 11th July so 6 days lost already. Continue to ignore?

-

Hi All Can anyone offer advice on my next steps? I have until Thursday to appeal to the IAS. thanks Steve

-

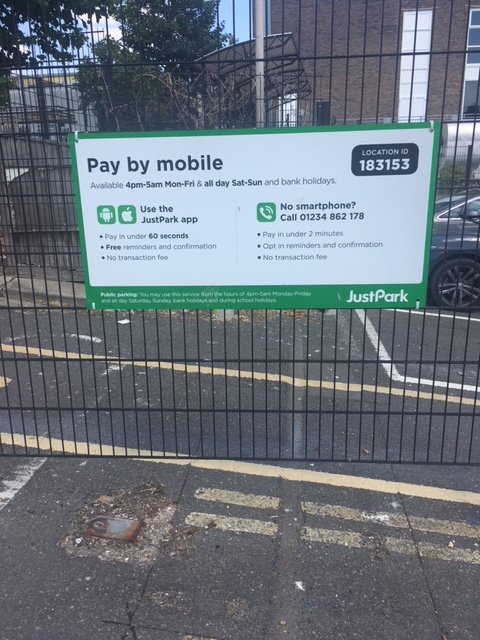

For PCN's received through the post [ANPR camera capture] please answer the following questions. 1 Date of the infringement 21st April 2018 2 Date on the NTK [this must have been received within 14 days from the 'offence' date] 2nd May 2018 3 Date received 7th May 2018 4 Does the NTK mention schedule 4 of The Protections of Freedoms Act 2012? [y/n?] Y 5 Is there any photographic evidence of the event? Y 6 Have you appealed? {y/n?] post up your appeal] Y Have you had a response? [Y/N?] post it up Y 7 Who is the parking company? UK Car Park Management 8. Where exactly [carpark name and town] Brighton Met College, Brighton For either option, does it say which appeals body they operate under. IAS Signage photos below:

-

Hi All For personal reasons I have not been able to deal with this earlier. this is the original letter from CPM and response to my appeal. In the text of this post is my appeal. I will be posting photos of signage later today. Any advice appreciated. Dear Sir/Madam I write to appeal PCN XXXXX for Vehicle Registration XXXXX on Saturday XX April 2018. On the 21st April 2018 I entered the car park at XXXX. After parking I attempted to pay using your telephone number but your system stated the car park was full and would not allow me to make a payment. The car park was not full and there were many empty spaces. A number of other people were gathered in the car park attempting to pay when I arrived. I and a number of other drivers left notes in our windscreens explaining that we had attempted to purchase a parking ticket but had been unable to do so. I would request that you review both your system for the date concerned and the above average number of PCN’s that will have been issued as a result of your system failure which will support my statement. I would hope that given the circumstances I have outlined UK Car Park Management will recognise that my failure to purchase a ticket is as a consequence of a failure in your payment system and cancel this PCN. I look forward to your response. CPM Appeal.pdf

-

Hi All In May I visited Brighton and went to park at the MET College as I had done many time before. However, instead of the college managing the car park it was now managed by CPM. The essential difference being that you used to pay in cash but now you have to pay over the phone to Just Park (not that you could tell how much as no signs showed the tarrif). After parking in the half full car park I saw a number of people in discussion in the middle of the car park. I approached and asked what was going on and they advised that they were all trying to call Just Park to pay for parking and kept being told the car park was full . After much discussion everyone agreed we would park and leave a note on our cars advising we had tried to pay and would be happy to pay if contacted. A week later I received a PCN for not buying a ticket. I had wrongly assumed the site would have a parking warden but of course the ticket was issued based on photographing my car on entry and exit so my note was never seen. I appealed the PCN based on the message saying the car park was full and requested they review their tickets for the afternoon as there would be an above average number of tickets issued due to the other people who also left messages. Today I have received a letter rejecting my appeal on the basis that the car park was full as other people had paid in advance for the spaces so by parking I was obstructing other drivers from using their designated areas. It says I should have refrained from parking and contacted CPM for advice. I repeat the car park was half full when I arrived and almost empty when I returned to my car. The recorded message did not explain why the car park would be full and I dont recall adequate signage explaining this in the car park. Can anyone give any advice on how I might appeal to the IAS? thanks Steve

-

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Thanks for the advice. I am likely to actually have to go into court to defend my statute barred position? -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

I assume that I photocopy the version for Lowells before I sign the document that I send to the court? I have begun viewing other posts and based on what I am reading I am surprised they are pursing this all the way into court as they seem to fail for much shorter periods over the 6 years than my 6 months. Is it there policy just to take a punt in court with all these cases? -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

I am about to send off my directions Questionaire to the court. I am of course ticking no to mediation but have a couple of questions if anyone can advise. 1. -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Hi All Received a letter from Lowells today. It reads: Please find enclosed a copy of the Directions Questionaire we have now lodged with the court. You will receive a copy direct from the court for completion and return. The court will use the information contained in both our copies to make decisions about how the case should proceed. The attached Directions Questionaire is acknowledging their willingness to attend mediation. Is this a normal tactic from Lowells and how should I respond? As ever thanks for any feedback/advice. Steve -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Received a letter from Lowells today. It reads We confirm receipt of your defence. We note that you believe the account to be statute barred, and as such,you consider that our client should not pursue the debt any further. We have raised your dispute with our client and will contact you once we have a response. Our client is keen to resolve the matter and will consider any payment or settlement proposal you wish to make. in the event that a settlement cannot be reached, it is likely we will be instructed to continue dealing with this claim as a defended matter through the county court. We hope this will not be necessary and look forward to hearing from you. Any thoughts? -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Name of the Claimant ? Lowell Portfolio 1 Ltd Date of issue – 21st February 2018 What is the claim for – 1. The claimant entered into a Consumer Credit Act 1974 regulated agreement with Vanquis under account reference *************** (*The Agreement') 2. The defendant failed to to maintain the required payments and arrears began to accrue. 3. The Agreement was later assigned to the claimant on 15/2/2013 and notice given to the defendant 4. Despite repeated requests for payment, the sum of £4000 remains due and outstanding. And the claimant claims a) the said sum of £4000 b)interest pursuant to s69 County Courts Act 1984 at the rate of 8% per annum from the date of assignment to the date of issue, accruing at a daily rate of £0.900, but limited to one year, being £300 c) Costs Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ? Yes - at this point I challenged debt as statute barred based on last payment date. Claimant response detailed in thread What is the value of the claim? £4500 Is the claim for - a Bank Account (Overdraft) or credit card or loan or catalogue or mobile phone account? Credit Card When did you enter into the original agreement before or after 2007? Mid 2007 Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Debt purchaser Were you aware the account had been assigned – did you receive a Notice of Assignment? Aware account has been assigned through chasing letters but cannot recall if received Notice of Assignment Did you receive a Default Notice from the original creditor? Don't remember Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? Not sure Why did you cease payments? Financial difficulties, Loss of job, marriage breakdown, evicted from rental property What was the date of your last payment? 26/8/2011 Lowell state CoA April 2012 Was there a dispute with the original creditor that remains unresolved? No Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management plan? Discussed financial problems with Vanquis in response to letters chasing lack of payment. Vanquis were not helpful. -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Thank you for the advice. I will follow as requested. May I ask, does the fact that the claimant has put the wrong date for assignment of debt have any effect on their claim? -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Today I received a Claim Form from the County Court Business Centre. Particulars of Claim Defendant entered into a Consumer Credit Act 1974 regulated agreement with Vanquis under account reference ************** Defendant failed to maintain the required payments and arrears began to accrue The agreement was later assigned to the claimant on 15/2/2013 and notice given to the defendant Despite repeated requests for payment the sum of ***** remains due and outstanding. Note: they have changed the date of assignment to 2013 from all previous correspondence which stated 2012 and the SAR response which stated same. Any advice on my next steps greatly appreciated -

Claimimg Vanquis card charges

steve806 replied to steve806's topic in Provident and associated companies.

I wasn't aware I needed to calculate the interest, Advice on that would be appreciated. And yes it does refer to to other post. -

Claimimg Vanquis card charges

steve806 replied to steve806's topic in Provident and associated companies.

Thanks. By spreadsheets do you mean a list of all charges with dates and descriptions? -

Hi All I am struggling to find the standard letter to reclaim charges. Can someone kindly post me a link please. thanks steve

-

Hi All Had ROP on a Vanquis credit card between 2007 and 2011 of almost £400. I defaulted in 2011 and the debt was sold to Lowell in 2012 and is still outstanding. Can I claim back the ROP as it is over 6 years old? Can I claim from Vanquis even though the debt has been sold to Lowell? If I can reclaim would Vanquis pay me or or pay Lowell to reduce the balance)? Is there a standard letter to claim? Do I need to calculate interest or will Vanquis do that? Any advice gratefully received. regards Steve

-

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

As Lowells claim the cause of action date is April 2012 when they say the card defaulted but kind advice given on this site suggests the cause of action date is August 2017 when the last payment is made we seem to be at an impasse. Lowells have said they will give me until 2nd February to contact them or they may proceed with court action so what should I do know? -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

are you saying I can reclaim all the default charges? they total more than 25% of the outstanding debt. How would I go about that? How do I reclaim ROP charges? Sorry if being thick but can I claim charges back from vanquis when they have sold the debt? Is my next action to write back to lowell and dispute the cause of action date based on the view 1st missed payment is the initial cause of action stating i will defend in court on that basis or do i wait until Lowell issue a court claim? -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Don't know if its is relevant but Vanquis statement shows they began charging me the following with effect from June 2011: OVER LIMIT CHARGE DEFAULT FEE PLAN INT FREE LATE PAYMENT CHARGE DEFAULT PLAN INT FREE BILLED FINANCE CHARGES DEFAULT INTEREST BILLED FINANCE CHARGES PURCHASE INTEREST these charges were applied for 6 months with the last charges in January 2012. I made a payment in June, july and August but nothing since then. I wondered: 1. Does the fact I was getting 'default charges' from 2011 have any bearing? 2. Why do the charges stop in January 2012 but according to Lowell the default wasn't until April 2012? Also, There are ROP fees on the account from October 2007 until March 2011. Can these be reclaimed? Again, any advice on what to do next welcomed -

Lowell claim form - Vanquis CC statute barred!!

steve806 replied to steve806's topic in Financial Legal Issues

Just received a response from Lowell. they state: "S5 states that an action founded on simple contract shall not be brought after the expiration of six years from the date on which the cause of action accrued. The account was taken out on September 2007 and went in to default in April 2012 as a result of non payment. it was at this time the initial 6 year limitation commenced as this was the initial cause of action. This would allow till April 2018 so the debt is not statute barred." The last payment made on the account was 26th August 2011 and previous advice on this thread said that meant the statute barred date was August 2017. I am now a bit confused. Can someone advise which is correct and give some advice on next steps please? -

unknown cabot/Mortimer CCJ - old WElcome debt - now AEO letter

steve806 replied to steve806's topic in Financial Legal Issues

At this time I have only submitted DSAR. Unless I have misread the advice I understood this was my move until receiving the AOE form from the court. Which arrived yesterday. Is now the time to make an offer to Mortimer to meet the terms of the original CCJ and offer £50 a month or threaten to suspend? And what potential value is the DSAR now? Very confused about what to do next so any advice gratefully received.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS