Feedy

-

Posts

9 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by Feedy

-

Ok Sorry Fair enough I did not get any advice last time I thought a new thread might get some advice.

-

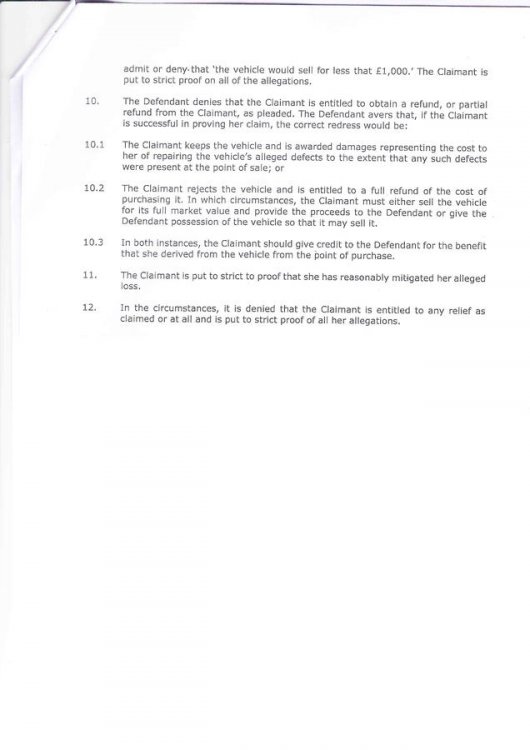

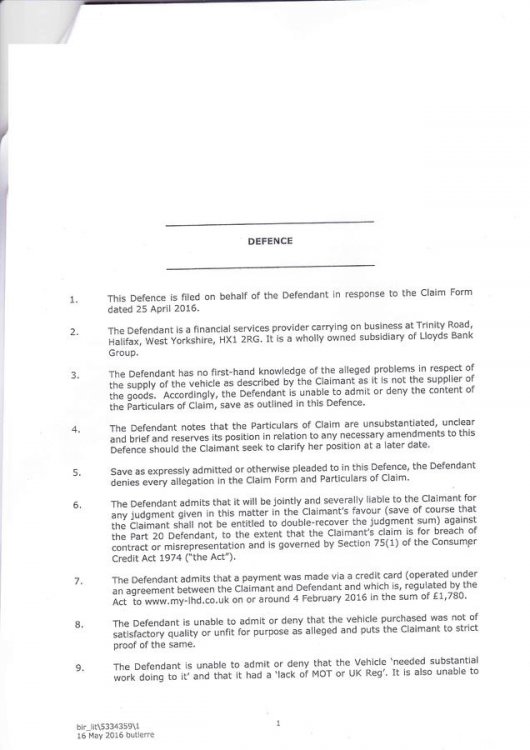

I received this Defence attached below in the Mail today for a small Claims case. Halifax have already agreed in Writing to offer us a Full Refund in email and by letter, But we wanted an option to keep it. We have since had it in writing that the Vehicle was to be scrapped if we accepted this offer. "If you accept the full refund, we entitled to have the vehicle in exchange, however, on this occasion we would be happy for you to dispose of it and provide us with proof it has been destroyed" at first this was original and only offer. "I refer to our previous correspondence regarding the above transaction. The Bank is now in a position to offer you £8900.00, in full and final settlement of your claim under Section 75 of the Consumer Credit Act 1974. This offer is made on the condition that you sell the vehicle on and provide evidence of this. Any funds received will be deducted from our settlement figure. If you do not accept this offer or you have additional information which you would like us to consider please contact me so we can discuss this further. You may wish to seek legal advice, if so please contact your solicitor. Another option is to speak with your local Citizens Advice Bureau or Money Advice Centre. If this offer is acceptable to you please contact us on the telephone number below. Alternatively you can scan the signed acceptance form attached and email it to us, if you would prefer to complete the form and return it to us. Please be advised, in addition I have today requested an interest calculation relating to this transaction. I will confirm to you in writing within 28 days any interest refund to be applied to your account and this will show on your statement. I look forward to receiving your reply." No offer of a Repair or costs for it was offered. Only once we submitted a Court Claim So we where Right to Ask for a Partial Refund (Purchase discount) provided that it was not more than any other remedy. it was cheaper than offering us a Full Refund. Vehicle is in such condition that it is worth close to scrap Value. I believe the only reason they have defended the claim is because they have now included the Part 20 Defendant (Dealer we bought the Vehicle from) are they allowed to do this. I have enough evidence for every part of there defence.

-

Rejected Lloyds Banking group final Offer today, for a Section 75 Claim, as it does not cover all our expenses or the option for Partial refund which is what we asked for and get to keep the Vehicle. They have copies of all the Failed MOT and Repair quotes and Email correspondence with the Dealer we bought the car from. We now putting in a Money Claims online claim. what information should I put in the short statement. ?

-

Dealer was given the chance to repair and that what we wanted , He even agreed to repair it at first but took the offer back. if its under so many days since you bought it 2 days in my case you can reject it anyway.

-

Car was bought through LHD Drive Uk Company as part of the Contract we wanted Warranty and Full Inspection of the Vehicle. We agreed to collect the Vehicle from Germany and Bring it back to the UK and Register it Myself to save money .We Had already paid for it when I saw it. and on the Drive Back I noticed Brakes system need replacing and many other issues, Took it for Mot lots of issues popped up. LHD Dealer agreed to Collect and Repair it but took the offer back when he Found out the Cars Location in the UK. Dealer Rejected my Formal Repose and told me the Warranty was not Valid till the Car was UK Registered and It was a third Party Sale. Invoice Mentions The LHD Drive company Terms and Conditions "The car is sold to you by (LHD Uk company) and you pay the purchase price to (LHD Uk company) " Key Points from my formal letter "Vehicle is not of satisfactory quality- On the 20/2/16 I discovered that it was not of satisfactory quality for age mileage and Price As part of my agreement with you told me you Inspected it. The issues brought up on the MOT refusal certicate( copy enclosed) and advisories show the vehicle is not of satisfactory quality, these issues would have been noticed had you had your Agent properly inspect the Vehicle. You told me it had Full Service History but it only has limited service history and you told me that the vehicle was good condition for age and mileage Having had a further inspection inspection we have been told there is also an engine oil leak and possibly engine piston issues. [The Consumer Rights Act 2015 requires dealers to supply goods of satisfactory quality.] Vehicle is not as described- misdescribed as having a Service and having the Calmbelt and Waterpump replaced and top top condition. [The Consumer Rights Act 2015 requires dealers to supply goods to be as described] Vehicle not fit for purpose- The vehicle is clearly unroadworthy and not fit for purpose and not safe to drive. You are therefore you are in breach of contract. [The Consumer Rights Act 2015 requires dealers to supply goods fit for purpose] You had already agreed to collect the Vehicle and Repair it but when you found out that I lived ______ you took this offer back. The purchase invoice mentioned my address when I bought the Vehicle. Contacted Lloyds, Sent them All Emails and Letters I had and Copy of MOT. and they requested Breakdown of Faults and costs to repair it. Provided this to them over 2 Weeks Ago. and Waiting for a response. Deposit was paid on my Halifax Credit Card.

-

When you Say hounding them. what Methods are best Phoning, Email ? At what point do you take it to the Small Claims Court ? The Financial ombudsman is so backed up already and I still have 4 Weeks to Wait. My case with all the evidence I have is pretty Clear cut.

-

I asked for the Money to Repair the Vehicle to the state that it should of been Sold in and if there had been a Full Inspection carried out on it. . Lloyds Asked for a full Repair Quote and Breakdown of what was Wrong with the Vehicle from Local Garage. #As there is list a mile long. We have not paid for repairs or got the work done Yet .We are waiting for outcome from LLoyds. We want to get it repaired if Possible but It might have to be full Purchase amount refunded.

-

We Asked for Repair Costs. At the moment the Repair Quote is £3407.55 Prices may increase when the work is Carried Out due to unforeseen breakages According to my Quote. One of many issues is Engine is in need of recondition or replacement and It might Vary. Engine was covered under Warranty.

-

this is about a Vehicle that needs around 3,500 - 4000 Costs in Repairs or a Full refund. its been over 2 Weeks since I sent the required Extra Information to Claims Team that they asked for . Today I received this email. "I have checked with management and your file is still under review and hope to have a decision to you by next week. Should you have any further queries, please do not hesitate to Is contact us." I Received this email about 6 Days ago "I am sorry to learn of the difficulties that you are experiencing with this merchant. Section 75 of the Consumer Credit Act 1974 covers purchases made using the card costing between £100 and £30,000, where a misrepresentation or breach of contract has been proven. Please be assured that a complete review of your claim is in progress and I will update you as soon as possible. " I was told on the Phone 7 - 10 Days it has been over that. Really not happy about the amount of time they are taking. Is there anything further I should do at this stage ? Its causing a lot of issues in the House and costing us money. I am planning on going Small Claims Route if I need to. as I am pretty sure it is clear cut case It has been just over 4 weeks since Lloyds where made aware of the Issue. .

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS