mister_gayle

-

Posts

18 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Everything posted by mister_gayle

-

Sorry I dont know wy it came out in a block of text, I am trying to edit it but it doesnt save.

-

Hi guys, Really need your advice and help on this please.I took a payday loan out with Tower Credit in July 2010 and never paid it back in full for whatever reason at the time.I applied for a payday loan with them last week and I was declined as I had an old account with them, I had totally forgot that I had taken a loan with them.Today I checked my bank account and they have taken the full amount from my new card, they got these details last week when I applied with them.I spoke to my bank to query this and they stated that if I had an agreement with them for a loan, then they are in their rights to take money from my card. I spoke to Tower Credit and they stated that they tried to contact me to advise me of the old loan I had, they also went on to say that it states in their T&Cs that if no agreement has been arranged to pay them back then they are in their rights to take the full amount from my card.I disputed this and said that surely by now my agreement with them would be void and they would pursuing repayment via a debt agency or imposing a default on my file. They said they applied for a CCJ and all the documents were sent to me.Surely this cannot be correct or legal, can it How can they save my new details and take money from it, without my permission??Isnt my agreement with the loan void ? So why can they take money for an agreement that is not in place ?I will have to check credit expert tonight, however if there is a CCJ or default on my file, are they allowed to take money from my card with permission or agreement ?Please can you advise on what I can do ?Thank you.

-

Hi Guys, I have been a user for a good while and had so much info and advice, so thank you all.What I wanted to know was some clarification on removing a default, I have searched on here and other forums but it seems to be conflicting info.Could someone please confirm if the creditors need to provide a copy of the default notice served or just them saying they sent a default notice sufficient, would this stand up in court ?I am in the process of disputing a default and will request a CCA and copy of the default notice and just wanted full and up to date confirmation.Thank you in advance.

-

I have 5 defaults, all coming off next year - bad choices when at Uni.I have a vanquis card, dont know how I got it but they accepted me. What I am doing is using it but paying the full balance off, that way the high APR doesnt affect me as it being paid off fully. This will show up on my report that payments are up to date and building history.Dont know how relevant the credit score is on Credit Expert, but it is going up slowly. Before I had the card I had 295 points, 3 months later I now have 575.

-

Thanks for this, ill let you know how it goes

-

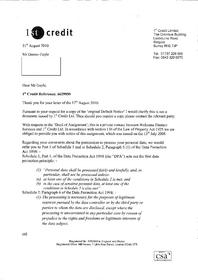

Ok thanks - I have composed this Thank you for your response on behalf of 1st credit dated 17/08/2010. However I still don’t believe you have understood all of my previous communications, in which I have requested a copy of the original Consumer Credit Agreement. Thus far you have only provided me with 1 page of the agreement. In view of you failing to comply fully and properly with my original request, you are in default and I consider the matter to be in dispute. The Consumer Credit Act is fundamental to your business and I cannot believe that you do not know how to comply fully and properly. My only conclusion from your actions is that you are deliberately seeking to mislead me, contrary to your obligation under the OFT Guidance. Yours sincerely / What do you suggest regarding the default notice ?

-

Ok thank you, I will use that. Do you have a template or example I can use ? Can you also advise why what they have sent is not sufficient, so I can state this in the letter I am composing

-

The attached document in post 8 is what they sent me, they have sent that to me twice. Do you have a template or example letter, or should I just simply send a CCA again but state they have not sent the correct document ?

-

Thanks No only the front page they sent ? How would you advise in how to proceed in responding to them ?

-

Surely someone one ?

-

Anyone ?

-

Is it true about 1st Credit not having the default notice, surely if they are looking after the account for Welcome Finance they would have all documents ? Also is it true with what 1st Credit have said about processing my data ? Can someone please advise on how I should respond. Thanks

-

1st Credit response to my 2nd letter

-

CCA -

-

-

How do I make the CCA viewable, I have uploaded it but it appears very small

-

LOL how do I make the images appear larger, so you can see my letters

-

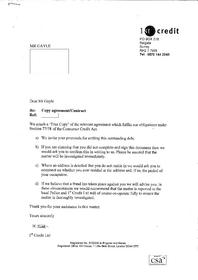

1st of all I would like to say I have been a lurker of this forum for ages now and have gained some great knowledge. Even my mum has used some templates letters from here and done well. So would like to thank you all and if there is a way I can donate then please let me know. I don't have many problems with my credit apart from one account I had with Welcome which is now being looked after by 1st Credit. I honestly dont remember receiving a default notice from them, so seeked the advice of this forum and got the info I needed. I 1st sent the CCA request, requesting my CCA, deed info and default notice. They replied with pretty much automated letter and attached a copy of the agreement. CCA Request response from 1st Credit, as you can see they didn't even respond to my requests for default notice and any deed info. Signed agreement, is this the correct document they have sent ? I rang them (bad mistake) and asked about my letter, they were just so rude and always talking over me. I would suggest to anyone NOT to ring the,. I was asking why the leter they sent made no reference to any deed info and copy of default notice. They kept saying "ive read your letter and we have sent you your CCA" got no where and I said ill be sending another letter. Again seeked the advice and info from this forum and sent 1st Credit this letter. It is quite long, if its best to scan it and upload admin please say. Thanks to ffcous, who I got most of this letter from 8) ******************************************** Dear Sirs, Client: 1st Credit Limited Debt: Welcome Financial Services Balance: £XXXXXX Client Ref: CRE XXXXXXX Thank you for your response on behalf of 1st credit dated 12/08/2010. However I don’t believe you have understood my previous communication dated 09/07/2010. In which I specifically requested the following: 1. You must supply me with a true copy of the alleged agreement you refer to. This is my right under your obligation to supply a copy of the agreement under the legislation contained within s.78 (1) Consumer Credit Act 1974 (s.77 (1) for fixed sum credit). Your obligation also extends to providing a statement of account. I enclose a £1 postal order in payment of the statutory fee. 2. You must supply me with a signed true and certified copy of the original default notice 3. Any deed of assignment if the debt was sold on The response given in your letter dated 12/08/2010 only addressed point 1. Points 2 and 3 have been ignored. Due to the nature of this I will now grant you with a further 10 days to complete my request before I take this up with court action which will result in yourselves defaulting and I will make sure the public are aware of this case. Upon signing my contract with you, I only gave you permission to log my account dealings whilst the contract was in place. If you read the wording of that contract it states quite clearly that I "give permission for Welcome Financial Services to supply credit reference agencies with information relating to the conduct and payment history of my account." I neither agreed to any other purposes, nor did I agree for that clause to include the term "in perpetuity". As you are aware, I am afforded principled rights under the Data Protection Act (Data Protection Act), Schedule 1, Part 1 ("The Principles") in relation to the manner in which my data is collated, stored and processed. Of particular note, are Principles 3, 4 and 5: “3. personal data shall be adequate, relevant and not excessive in relation to the purpose or purposes for which they are processed. 4. personal data shall be accurate and, where necessary, kept up to date. 5. Personal data processed for any purpose or purposes shall not be kept for longer than is necessary for that purpose or those purposes.” In my case, you are still processing data after the cancellation of the contract, whether or not this is a simple renewal process of the default flag, daily or by other timing factor. As that contract is no longer in situ, then my written permission has also ceased from the date of cancellation. This is confirmed in Principle 2 of the Data Protection Act, which states: "2. Personal data shall be obtained only for one or more specified and lawful purposes, and shall not be further processed in any manner incompatible with that purpose or those purposes." I emphasise the term "specified and lawful purposes" as in ‘those specified within the contract’, and no more. I also emphasise the term "shall not be further processed". May I also advise you of my findings regarding this so called legal right to place an adverse entry on my credit file for up to six years. One of your colleagues advised me that “it is law to keep a default on file” I was amazed to hear this and that you have staff employed advising customers this incorrect information. I have taken the matter up with the Credit Reference Agencies, and they had claimed that they had a “legal right” to maintain this type of adverse entry for up to six years. When I challenged them to quote me the exact Statute that includes this so-called “legal right”, they remained remarkably quiet. Only after my continued insistence of disclosure did they eventually concede that, whilst they have no statutory right, it is

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS