JHGlover

-

Posts

27 -

Joined

-

Last visited

-

If anyone does find a decent solicitor who deals with this type of law, and are good, let me no........... why the up front fees

-

why is it wyen you write something something changes, i have just been informed by my parent that he has contacted Swift to explain his loosing his job, it would seem he has missed his last payment and swift will be sending him a letter to put down his expenditure etc: is there any advice out the on how to complete this or will Swift be favourable, and rip him off aggain by lowering his payments and extending the loan and of course adding more interest ??

-

Currently no fight but am preparing for one, my parents have not as yet defaulted, but sure as eggs is eggs they will not be able to continue to keep up the repayments, i have advised they send for SAR which we are waiting for, once we get this information we can start to look at any details that will be required to to for unfair or unenforcable CA, it will be interesting to find out what details are sent, certainlay as the interest rate seems to be increasing whenever Swift feel the urge, so will be looking to claim back the PPI, and any other outragous fees, like broker fees, we have also asked for the original CA, be intyeresting to see if they send an original or, one thats been changed to fit with Swifts usual tactics. but we do have the original to compare with, is there any documentation i should be looking for in the SAR that swift may feel like omiting ?? also should they have recieved statements from swift about how their account stands??

-

Hello you all, qestion, can a claim still be made on PPI if a claim has been paid during the 3 year term, but would it still be claimable, if the term was only for 3 years but payments are being collected for the 15 year term of the loan.

-

I am hoping this will all come to light when.if we recieve the documents from the SAR ferom what i can gather no letters have been recieved pertaining to this.

-

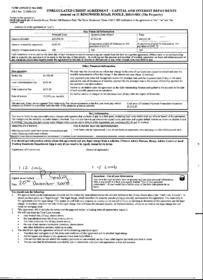

I have the Agreement number, but have been informed that the payments have been £545.00 for the first 36 months however on the CA its states he should have been paying £515.95 for the first 36 months , i have been informed it has been reduced to £512.00 for the next 144 months but on the CA it states it should be 485.72, i have asked parent to check his bamk statements to see what he has been paying for the last 3 years, surely there is some discrepency here

-

I am checking with my parents if they have recieved any otherecorrespondence from Swift with relation to an account number, however as i have stated there is no account number on the credit agreement, , and sorry didnt read the letter fully, to notice the CA info

-

Thanks sparkie, but as i stated there is no account number, also is there a letter for requesting the a copy of the original credit agreement and if so is there a fee

-

I was just about to do a SAR letter, but i cant seem to find any indication of an agreement number, the only indication of numbers is the top left of the form that i posted earlier, that says FORM UNRCAP [1 Nov 2005] [V8.5 Rev 7 ] 20061215 the latter numbers look like a date to me. but no indication of agreement number, anyone have any idea how i would correspond with them, secondly i would like to get a copy of the CA from Swift just to see if they have a copy, i think there is a letter and a fee to pay for this i believe can some one please enlighten me, thanks

-

I contacted the FOS today and was advised they couldnt investigate my issue due to the fact that the loan was prior to April 2007, they said i would need to contact OFT, which i subsequently found out dont deal with individual cases, they then directed me to consumer direct, who were helpful to a point and advised they would get trading standards to contact me, i also approached some of the online solicitors who stated they wouldnt take the case due to the loan being unregulated, being prior to April 2007 & also because it was a secured loan, so this company that act like loan sharks seem to be able to get away with taking away a house from pensioners with no recourse, comments please

-

Sparkie, excuse my ignorance, but how would i find a public access barrister

-

Thanks sparkie can you or anyone else recomend a good barrister that i can contact to look into this case.

-

Sparki were you refering to my post In my opinion this agreement is unenforceable, for so many reasons I cant count, It is impossible to understant the manner in which payments have been calculated.....it is without doubt a multiple agreement partly regulated by the CCA 1974...therefore the interest rate on the PPI should be shown an an APR in any event and it is not.......if the PPI is taken out of the amount of credit by the misselling it would affect the whole agreement and would in my view be declared void. My Advice Get genuine good legal advice off a good consumer law lawyer sparkie

-

this PDF should work Scan0002.pdf

-

I think i have it worked out, come someone take a look and see if its enforcebal

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS