seanj70

-

Posts

35 -

Joined

-

Last visited

Content Type

Profiles

Forums

Post article

CAGMag

Blogs

Keywords

Posts posted by seanj70

-

-

...

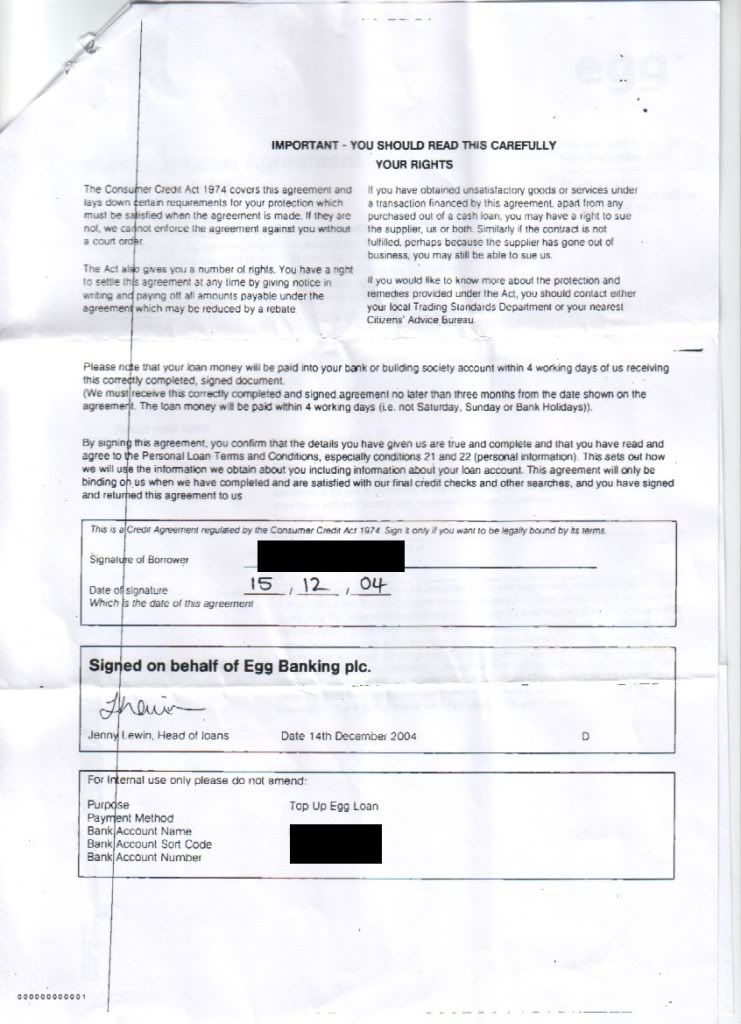

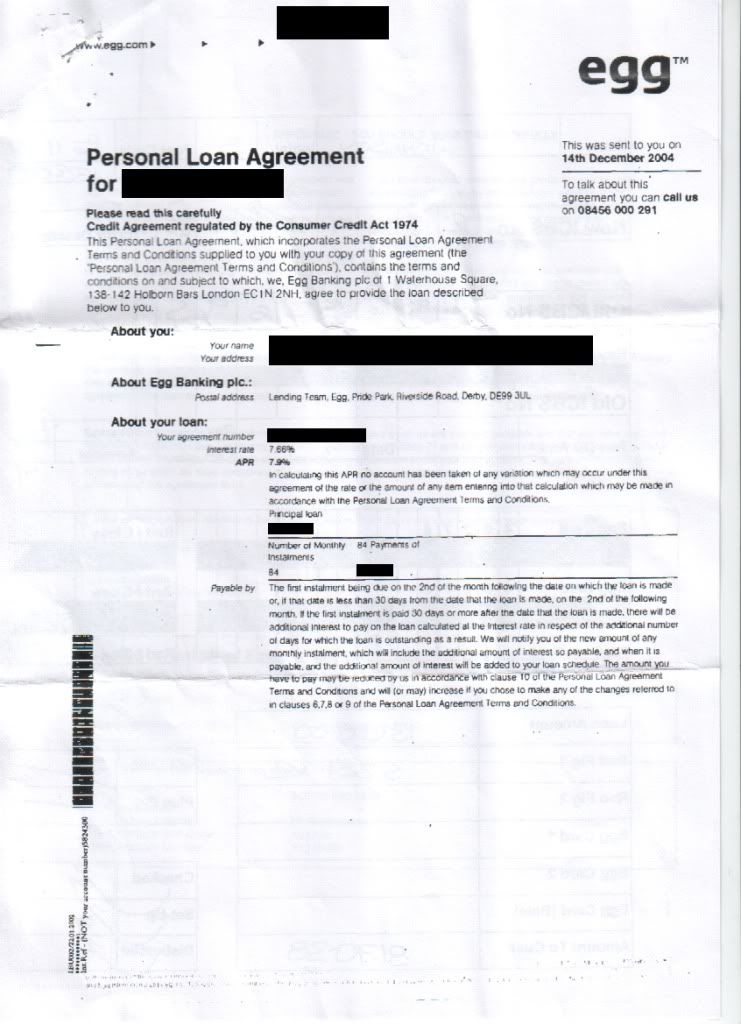

There were no prescribed terms and conditions in the body of the two pages, no additional documentation. Additionally, there was no cooling off period and no mention of the total credit to be paid.

...

so, although it mentions Terms and Conditions it's wrong cos they weren't supplied to me? and they should be part of what they sent me?

also, the total credit to be paid would be the loan ammount plus the interest right?

and there should be a mention of cooling off in the supplied docs - what if they subsequently provide the terms and conditions and they generically mention a cooling off period?

i'm sure i've never seen a total amount to be paid thou!

thanks for your help. even if they do come back eventually, a month or two of dispute and no payments will be very helpful right now

-

after a request for my CCA from Egg (via Cap Quest collection agency) i received the following.

there are no detailed clauses as i've seen on some of the Egg Credit Card agreements posted.

any help / advise would be greatly apreciated.

http://i679.photobucket.com/albums/vv156/sean23uk/egg2a.jpg

-

-

many thanks, you comments have been useful.

here's my proposed letter, what do you think? does it need anything adding / removing?

thanks for your time

I refer to my letter dated 23rd June 2009 which was delivered via recorded delivery to your offices on 24th June 2009.

In my letter dated 23rd June 2009 I made a formal request for a true copy of the credit agreement relating to the above account, together with any other documentation the Act requires you to provide, under section 77(1) and section 78(1) of the Consumer Credit Act.

The Consumer Credit Act allows 12 working days for this request to be carried out before your company enter into a default situation. This period has expired.

As you are no doubt aware section 77(6) states:

If the creditor fails to comply with Subsection (1)

(a) He is not entitled, while the default continues, to enforce the agreement.

Therefore as at 9th July 2009 this account became unenforceable at law.

The lack of a credit agreement is a very clear dispute and as such the following applies:

-

You may not demand any payment on the account, nor am I obliged to offer any payment to you.

-

You may not add further interest or any charges to the account.

-

You may not pass the account to a third party.

-

You may not register any information in respect of the account with any credit reference agency.

-

You may not issue a default notice related to the account.

Any default notices or adverse comments your company has recorded on my credit reference file should be immediately removed.

This letter should be treated as a statutory notice under section 10 of the Data Protection Act to cease processing any data in relation to this account with immediate effect. This means you must remove all information regarding this account from your own internal records and from my records with any credit reference agencies. Should you refuse to comply, you must within 21 days provide me with a detailed breakdown of your reasoning behind continuing to process my data.

It is not sufficient to simply state that you have a ‘legal right’; you must outline your reasoning in this matter and state upon which legislation this reasoning depends.

Failure to respond favourably to this letter within seven (7) days of receipt will result in immediate litigation being commenced against your company without further notice.

I would appreciate your due diligence in this matter.

Yours faithfully

-

You may not demand any payment on the account, nor am I obliged to offer any payment to you.

-

also found this in a non-compliance of CCA request response - if it worth adding this?

This letter should be treated as a statutory notice under section 10 of the Data Protection Act to cease processing any data in relation to this account with immediate effect. This means you must remove all information regarding this account from your own internal records and from my records with any credit reference agencies. Should you refuse to comply, you must within 21 days provide me with a detailed breakdown of your reasoning behind continuing to process my data.

It is not sufficient to simply state that you have a ‘legal right’; you must outline your reasoning in this matter and state upon which legislation this reasoning depends.

-

so is the following true? and if so can i take things further to try and get the debt written off?

The lack of a credit agreement is a very clear dispute and as such the following applies:

* You may not demand any payment on the account, nor am I obliged to offer any payment to you.

* You may not add further interest or any charges to the account.

* You may not pass the account to a third party.

* You may not register any information in respect of the account with any credit reference agency.

* You may not issue a default notice related to the account.

what if a default notice had already been issued on the account previously?

if they are not entitled to record anything with credit ref agency can stuff be removed that is already recorded?

-

i've read some places that the following regarding the offence is no longer true?

The Consumer Credit Act allows 12 working days for this request to be carried out before your company enter into a default situation. If the request is not satisfied after a further 30 calendar days, your company commit an offence. These time limits expired on XXXXXXXX and XXXXXXXX respectively.

As you are no doubt aware subsection (6) states:

If the creditor under an agreement fails to comply with subsection (1)—

(a) He is not entitled, while the default continues, to enforce the agreement; and

(b) If the default continues for one month he commits an offence.

if so, then does this mean that the debt is unenforcable after the intial 12 day period, rather than waiting until the further 30 days?

-

so pressumably it'd show on my credit file?

-

i have to hefty debts one a credit card and the other an unsecured loan.

i've been repaying for sometime and about a year ago, due to finacial difficulties, entered into repayment plans with frozen interest on them.

i'm currently requesting copies of the CCA, neither of which I have ever signed.

is there any chance of these debts being unenforcable if they are unable to supply the CCAs despite me making payments for a few years?

{kind=link}

{kind=link}

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS

can someone check my Egg Loan CCA

in Egg

Posted

does this template need to highlight why it's in despute (these points you mention - cooling off, no signed terms, etc) or simply send as is?

thank you muchly