not-impressed

-

Posts

16 -

Joined

-

Last visited

-

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

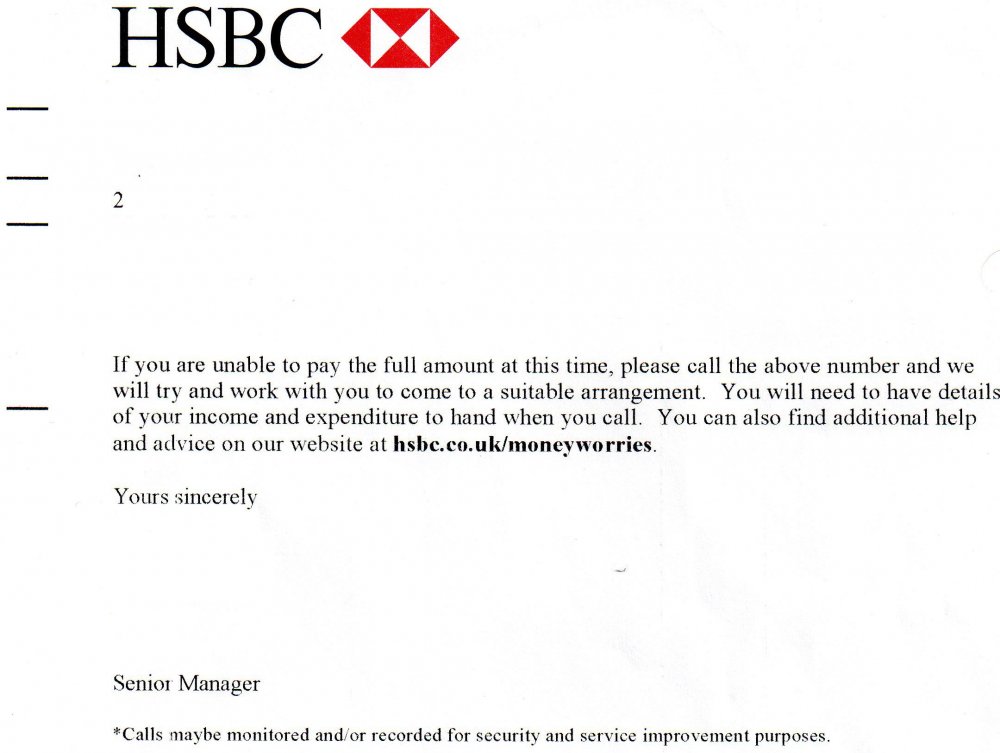

I believe the following details in the Final Demand are incorrect The Default Notice referred to was never sent (It has never been provided in any SAR response) - This was deeply confusing. I understand that a Notice served under Sections 76(1) and 98(1) of the CCA1974 must be issued, but is this one? Other examples I've seen clearly state what they are and include reference to Sections 76(1) and 98(1) of the CCA1974 in the header. The Final Demand letter provided 18 days of notice for full repayment or an arrangement. The 'Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies' guidelines which I believe apply, and they are obliged to follow, state 28 days notice is required. The 'Help is available' section of the letter states they would try to work with me to come to an arrangement. They refused to. Subsequent correspondence on this point from HSBC stated only a full repayment would have been satisfactory. This completely contradicts what the Final Notice letter said and is the cause of the issuing of the default. Further thoughts on this greatly appreciated.

-

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

I'm exploring other avenues to resolve this now including BCOBS for which there seems to be very little guidance available. Is this an effective route? I'm also aware of the following but not sure how they all fit together in the context of my situation. The guidelines on filing defaults ("Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies"). Do both apply in the case of registering a default against overdraft arrears? Should this situation also be covered by the FCAs consumer credit Sourcebook which includes the following in CONC 7 : Arrears, default and recovery(including repossessions) Section 7.3 : Treatment of customers in default or arrears (including repossessions): lenders, owners and debt collectors 7.3.6 - Where a customer is in default or in arrears difficulties, a firm should allow the customer reasonable time and opportunity to repay the debt 7.3.8 - An example of where a firm is likely to contravene Principle 6 and ■ CONC 7.3.4 R is where the firm does not allow for alternative, affordable payment amounts to repay the debt 7.3.8 FCA due in full, where the customer is in default or arrears difficulties and the customer makes a reasonable proposal for repaying the debt or a debt counsellor or another person acting on the customer's behalf makes such a proposal. 7.3.9 - A firm must not operate a policy of refusing to negotiate with a customer who is developing a repayment plan -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Many thanks for your response. Really helpful. I'm not clear on the relationship between the CCA and the guidelines on filing defaults ("Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies"). Do both apply in the case of registering a default against overdraft arrears? Should this situation also be covered by the FCAs Consumer Credit Sourcebook which includes the following in CONC 7 : Arrears, default and recovery(including repossessions) Section 7.3 : Treatment of customers in default or arrears (including repossessions): lenders, owners and debt collectors 7.3.6 - Where a customer is in default or in arrears difficulties, a firm should allow the customer reasonable time and opportunity to repay the debt 7.3.8 - An example of where a firm is likely to contravene Principle 6 and ■ CONC 7.3.4 R is where the firm does not allow for alternative, affordable payment amounts to repay the debt 7.3.8FCA due in full, where the customer is in default or arrears difficulties and the customer makes a reasonable proposal for repaying the debt or a debt counsellor or another person acting on the customer's behalf makes such a proposal. 7.3.9 - A firm must not operate a policy of refusing to negotiate with a customer who is developing a repayment plan -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thank you. So they were not at all accurate in stating they'd fulfilled their obligations under the CCA 1974? They should have sent notices under Sections 76 (1) and 98 (1) and given me more of an opportunity to come to an agreement with them? I'm aware the "Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies", states that "The lender must have notified you of their intention to register a default against you at least 28 days before doing so, in order to give you time to make an acceptable payment or reach an agreement with them on an arrangement. " It also states "If an arrangement is agreed (see Principle 3 above), a default would not normally be registered unless the terms of that arrangement are broken. " So as the bank had agreed to my repayments it should not have subsequently registered a default? I'll check the paperwork but I don't recall any mention of Sections 76 (1) and 98 (1) I've noticed that there appears to be later versions of the CCA (2006?) Why is it that they don't appear to have replaced the 1974 version? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thank you. So the bank simply made a mistake in referring to issuing a Default Notice. They weren't actually required to issue one, just a final demand? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

A little more detail on this is that a bank issued a Final Demand for repayment of an overdraft balance referring to a default notice they had never sent. They have subsequently stated that as they'd issued other warnings (in other letters) that they might register a default with the CRAs, they'd fulfilled their obligations under the Consumer Credit Act, despite stating in writing they'd sent a default notice which they had not sent. The Final Demand letter provided 18 days of notice for full repayment or an arrangement. The guidelines which I believe apply and they are obliged to follow, are the Principles for the Reporting of Arrears, Arrangements and Defaults at Credit Reference Agencies, state 28 days notice is required. They then repeated to me in letters on several occasions that they'd registered a default with the CRAs despite not actually registering it until 6 months after they'd stated they had registered it. In the interim I made an agreement with their collections department to completely repay the outstanding arrears with a lump sum of half the amount and 4 payments to cover the rest in total. At the point I made this agreement to the point I'd repaid the amount owed they didn't register anything with the CRAs. It was only when the full repayment was made (or within a few days of the final early repayment being made) that they registered the default and at that point only 2 of the 3 CRAs were notified of a default. . They refuse to remove the default. I believe they have acted very unfairly and unlawfully. Can anything be done? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Is the issuing of default notices on current account overdrafts (that were authorised but have become 'unauthorised') covered by the Consumer Credit Act 1974 (or if this has been updated, by a more recent version) or something else? If something else, what guidelines to the issuing of default notices and subsequently defaults on overdrafts apply? Thanks in advance -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

An update since August. I'm seeking advice on what to do next. Approach the FCA? Legal action via BCOBS? My objective remains the same; the removal of the default notice applied by HSBC after their incorrect assertion that a Default Notice had been issued and their unfair treatment in offering me a clearly empty promise of the possibility to make an arrangement to pay. In addition to this there are numerous inaccuracies in the dates associated with their issuing the default. Having requested that my complaint was referred to an ombudsman I have just received the final decision. Frustratingly , this didn't seem to even address some of the points I raised in my letter to support the request that the complaint was looked at by an ombudsman (full letter further below). Most confusingly the background section of the final decision document states "Mr M says he was never sent a default notice; HSBC says he was." This is confusing as, to my knowledge, HSBC have never claimed they did ever send a Default Notice, despite the Final Demand clearly stating one had been sent. I asked the FOS to provide evidence of this and the following was their response, which actually draws from another section of the Ombudsman's Final Decision. "As you are aware from previous correspondence, we do not have a copy of the default notice. This was made clear when I came to my formal view and also in the final decision where it is said ‘Mr M says he never received a default notice. I accept that’. If there is any further information you would like, you would have to contact HSBC directly". I also got in touch with the Adjudicator (letter below) with regard to their comment during a phone call that I had "taken HSBC's comments too literally" the Adjudicator replied "I appreciate that you feel that the default is not accurate or in fact fair, and if I am honest I can understand why you feel this way. However, this does not mean to say that HSBC was wrong to apply the default as it did. You have said that you do not entirely agree with me when I have said you may have taken what HSBC said in its letter to literally. First of all, please accept my apologies if this came across the wrong way – I did not say this with the intent of causing offence, rather just my opinion on what I thought had happened." I raised a Subject Access Request on FOS to get all of the information they'd received from HSBC and as part of that I received a letter 0f 12 June 2015 from HSBC to the Financial Ombudsman which stated "I am aware Mr M remains unhappy that a default has been registered with the Credit Reference Agencies (CRA's) in respect of his Current Account. It is Mr M belief that we did not issue a Default Notice to him and as such, the default should be removed as it is a true and accurate record of his account conduct." I'm not even sure what is meant by the second part of that sentence. The letter goes on to state that "Mr M did not contact us until after the Final Demand was issued. The repayment proposal was insufficient to prevent the account from being passed on to recovery services as only full repayment of the outstanding balance within 18 days of the issuing of the Final Demand would suffice." I have subsequently been in touch with HSBC to seek clarification of the issuing or otherwise of a Default Notice and they have replied to state that as the case had been raised with the FOS and the Adjudicator had made their decision they were not obliged to reply and would not do so and any further correspondence would be filed and not replied to. I won't be accepting the Ombudsman's decision so now I'm now bound to that are HSBC obliged to respond to any requests for information? Here's is my letter requesting that the case is reviewed by an Ombudsman which summarises the main issues I believe to be relevant. Letter to FOS Adjudicator I would like to request that my case is referred to an Ombudsman for further consideration please. Your summary was that ; "You have said you would like the default that HSBC applied removed from your credit file. On review of everything provided to me, I cannot agree with you. This is because there is a legal obligation for information that is reported to the credit reference agencies to be a true and accurate reflection of the account. In this case, the default has been applied correctly and I cannot require HSBC to remove it." I would like to challenge this finding as I don't believe it is fair and reasonable that HSBC has registered a default with credit reference agencies against me for three reasons. In addition to this, and based on the information HSBC has provided me, what has been reported to credit reference agencies is inaccurate and is therefore not a true and accurate reflection of the account. I would also like to highlight that during our conversation on the 20th June 2015 you stated that I had taken the communications from HSBC "too literally" which I don't believe is a valid perspective when assessing the clarity of HSBC's communication with me and fails to take into account the confusion created by the inaccuracies in their communications both in writing and verbally. My reasons for requesting that my case is referred to an ombudsman are as follows. Firstly, the Final Demand letter from HSBC referred to a Default Notice it appears was never sent. This means the correspondence from HSBC that claims a Default Notice had been sent was incorrect and completely misleading and was therefore problematic for my understanding of the process. HSBC have subsequently been unable to provide any evidence of ever having issued the notice they said they had sent but have instead claimed they have fulfilled their obligations under the Consumer Credit Act 1974. I believe they are also obliged to treat me reasonably and fairly and referring in writing to correspondence they have not sent to me is misleading and therefore entirely unfair and unreasonable. Secondly, the letter from HSBC of 22 May 2015 goes on to state that "As the Final Demand letter had already been sent, only repayment of the full outstanding balance would have prevented the account from being passed to HRS and a default from being registered with the CRA's." However, as mentioned previously, the Final Demand letter clearly states that "If you do not make full payment or make a suitable arrangement with us...we may take additional action to recover this amount..." and under the Help is available section "If you are unable to pay the full amount at this time, please call the above number and we will try and work with you to come to a suitable arrangement." The only conclusion I can draw is the offer of help in coming to a suitable arrangement in the Final Demand letter was entirely disingenuous and for the purposes of clear, unambiguous communication and fairness should not have been included. I'd like to reiterate at this point that I called having read the letter in good faith and was denied an opportunity to come to an agreeable repayment plan that HSBC's own correspondence offered. It now appears from their response of the 22 May that this was never a genuine opportunity. As mentioned previously HSBC also declined my request to clarify this by email following the call. I requested this as the advice given in the letter and the conversation differed so greatly and I was confused by the unclear explanation of the process and the lack of transparency around the process. HSBC stated during my call that my only option would be to wait for the account balance to be transferred to HSBC Repayment Services in 9 days time. Against this timescale, this would presumably mean a default date of 15 October. As the default was actually registered in retrospect on the 18 November why was the opportunity to honour the statements in HSBC's Final Demand letter and arrange a payment plan denied so quickly? Why also was my request to clarify the situation denied? Thirdly I understand that Section 4 of The Information Commissioners Office "Data Protection Technical Guidance Filing defaults with credit reference agencies" document states "It is an accepted industry standard to record only serious ‘defaults’ with credit reference agencies. " Given the fact I made an attempt to come to an arrangement HSBC had offered but unreasonably denied, and the default amount was comprised of approximately 70% fees (an annual summary of account charges with a date of 02-Oct-2014 confirms total fees and interest charged from 02 October 2013 to 01 October 2014 of £480.38 - a substantial proportion of the amount registered by HSBC as the default balance of £628.) and all of the inconsistencies in HSBC's communication, I don't consider this default to have been fairly applied in accordance with that guideline. I'd like to reiterate the immense personal impact this situation has had on me as a 42 year old with aspirations to be a home owner and with an otherwise excellent credit history and a long history with HSBC. At my age a default recorded against my credit reference files will have a catastrophic impact upon my future as this will effectively make home ownership of any sort impossible. The action of registering a default against me which I sought to avoid by calling to discuss an acceptable repayment plan is grossly at odds with HSBC's values and stated aim of being "Dependable, and doing the right thing". The HSBC values state that "At HSBC we put great emphasis on our values. We want to ensure that our employees feel empowered to do the right thing " Communicating openly, honestly and transparently, welcoming challenge, learning from mistakes Listening, treating people fairly, being inclusive, valuing different perspectives I feel strongly that HSBC have fallen short of their promise. In addition to this, HSBC appear to have made numerous mistakes in a variety of the dates and details they have provided to me and have not accurately recorded the default with the credit reference agencies. I'm not at all clear on why the default date of 18 November 2014 has been used and retrospectively applied in March 2015 . It appears that, despite HSBC twice confirming in writing the default had been applied in November 2014 no default was registered until after 31 March 2015 when the credit reference agencies were advised of the default. I spoke with Experian on the 21 January 2015 and they confirmed a default had not been registered and indeed no information had been received from HSBC at all. This position only changed in my Experian credit file in April 2015 (Experian records mark the Default satisfied date as 31 March 2015 and that the records were updated 05 April 2015). Had it been clear that a default was not to be registered for more than 4 months from the date HSBC said they had registered the default I could have made mortgage or other credit applications without a default impacting on my chances of securing a mortgage or loan. Neither, surely, does this achieve the stated aim of providing a "true reflection of how the account was maintained." Particularly as HSBC has never registered any other details with the credit reference agencies since I became a customer in 1992 and the default details registered do not include any of my repayments. If the account closure process of an account closing 180 days after it enters the collections process was applied, that should mean the date that the account was in default should be 12 September 2014 (180 days after the stated date of entry into the collections process of 12 March 2014 - mentioned in HSBC's letter of 22 May 2015). I therefore contest the accuracy of the date of the default and additionally the failure of HSBC to keep the default balance up to date. No repayments appear in the credit reference agency reports and I understand from section 29 of the Information Commissioners Office's document "Data Protection Technical Guidance Filing defaults with credit reference agencies" document that "Default records should show the original amount of the default as a snapshot in time and should reflect subsequent payments by showing the current balance of arrears.. . The current balance should be filed both by those who file monthly account information and those who file only defaults. It should be updated regularly. " In addition to this section 30 "When ‘in collection’ " states "Where debts are passed for collection to internal or external debt collection departments or agents, the lender is responsible for keeping the record of the default and any outstanding balance accurate up to date. " I also understand that the Data Protection Act 1998, in the data protection principles, sets 'legally enforceable standards for organisations'. The principles require, among other things, that: • personal data is processed fairly and lawfully; • personal data is adequate, relevant and not excessive in relation to the purpose or purposes of processing; • personal data is accurate and, where necessary, kept up to date; As already stated the personal data provided by HSBC to the credit reference agencies is not accurate. There also appears to be a discrepancy with regard to the end date of my account. My account end date is registered as 31 March 2015 with the credit reference agencies. To this I'd like to reiterate that the letter from HSBC of the 22 December 2014 states "I have looked carefully at our records and can see the Bank Account ending 3380 was closed on 18 November 2014..." HSBC's letter of the 22 May states that the End Date was the date the final payment was made but I actually called HSBC repayment services to make an early final payment of £28.25 on 02 Apr 2015 How can my account be closed both in November 2014 and in March 2015 and why was it closed before the final payment? In addition to this the closure of my account has been registered with Equifax with no mention of a default and consequently no change to my credit report which I believe to be vexatious. In addition I certainly don't believe that HSBC have fulfilled your statement that "information that is reported to the credit reference agencies to be a true and accurate reflection of the account." I would like to reiterate my request that, for all of the reasons outlined above, the default is removed from my credit reference agency reports. Yours sincerely Thanks for reading and all advice greatly appreciated. -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

They've emailed back in response to my question "I have a question on the data provided by the SAR. Can you confirm that this will provide all of the data provided by HSBC including calls and transcripts?" With this response "I can confirm that our Information Rights Officer will deal with any Subject Access Requests. As mentioned in the email below, nobody is entitled to see our full file. Also if there are any files which are commercially sensitive, these will not be sent." -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thanks for all of the help so far. I requested that the FOS provide me with all information they have and they've replied to say "As per your request, I can send you the material information I used when coming to my formal view of your complaint. However, if you would like to see all of the information we have, you would have to make a Subject Access Request. More information about this is below. Please note, neither party is entitled to see a full copy of our files. We cannot always provide you with all the information you may wish to see, but you can make a subject access request under the Data Protection Act 1998." I'll go ahead and raise a SAR as they should then provide the information HSBC provided. I'll also submit a SAR to HSBC (but as the account is now closed will they simply say they're not obliged to provide the information?). The response from FOS above isn't entirely clear to me. What information is being referred to above that can be witheld? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thanks for reading my post and responding.Your guidance is very much appreciated. You are correct, I'm a little late to this forum but I have now read all of the customer service guidelines (Guidance note - Dealing with Customer Service Departments) I've avoided phone contact wherever possible however and have not initiated any calls (and tried to keep any calls to me to a minimum) but will follow the advice to the letter in the future. Should I continue with the FOS? Would you advise against raising with the IC? Do dealing with either of these organisations prejudice in any way my ability to resovle this through BCOB? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Hello CitizenB Thanks for taking the time to read my post and respond. This was the first decision from the FOS made by an Adjudicator. They verbally told me during a call that I'd taken HSBC's communications 'too literally' which I was obviously stunned by. Worth mentioning this when I ask the FOS to review my complaint? I have already asked them (just now) to provide a record of everything HSBC has sent them. If this approach doesn't work I assume contacting the ICO (some of the details of the Default appear incorrect) and approaching the FCA quoting BCOB would be the next step? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thank you for your advice. Unfortunately I was a little late to the subjects of SAR's. The default balance was about 75% unauthorized overdraft fees after my account was downgraded. There were also irregularities in the date of the default with one letter in September last year stating that the Default had been registered with CRA's at that point. No defaults were registered however until April 2015. -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thank you. I'll do a SAR. I did state some of the BCOB to the FOS but they've not responded to those specific points. What is most frustrating about this situation is that I called in good faith to arrange a repayment to be told there was nothing I could to although the Final Demand letter I responded to stated twice that HSBC would try to help. No Default Notice was ever issued (but the Final Demand letter referred to one) but again, FoS believe this to be unimportant as pre-demand and final demand letters were provided. In addition the registered default gives an incorrect start date to the account and uses the same date as the default date. As I opened my account in 1992 are there likely to be any data protection implications? -

Removal of a default notice applied by HSBC

not-impressed replied to not-impressed's topic in HSBC Bank

Thank you for reading my post and responding. I've not requested a SAR. I understand that this may not be possible as the account has closed (it was closed in November of last year)? If that's not the case then I will do that asap.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS