simo67

-

Posts

24 -

Joined

-

Last visited

1 Follower

-

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

thnak you for merging threads, its been a while but has cropped up again due to SAR and PPI requests -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Hi, It's been a good while since I sourced your assistance and donated so must be due again dependant on my outcome but expecting something here and could be fun too. Sorry for the initial long read but has been going on nearly a decade now and decided I really want to do something about it and go back for damages where non compliance is taking place and prepared to follow it through with guidance from the CAG genies and gurus. Looking for assistance on next steps forward relating to old debt and unfair interest charges on account with Barclaycard and as title suggests has been bounced about over a number of years. All other creditor accounts from same time period 2009-2014 settled in full with 0% interest charges -HSBC, Halifax/BOS for accounts, loan and credit card. End result is I wish to take Barclaycard to court for applying unfair interest charges to an account knowing the client had significant debt issues due to a significant life event as per FCA rules about treating clients in debt. I also want to take RW to court for failings and non-compliance with GDPR at a minimum and hoping if I get justice with B/C can then sue RW for impact on my PI and my available credit lines (none) for 6 years. I currently have the FCA going back to Barclaycard as their final response to my complaint raised Jan 2017 seeking £200k in damages and responded to in April 2017 by B/C and the same as SAR request from Oct 2016 went to a different and old address (another DP non-compliance) and not where my SAR and complaints letter were addressed from. I have only just seen this letter as obviously I never received it and advised FCA as such. Informed FCA as only received B/C response letter in April 2019 via the FCA then the 6-month time limit for raising my complaint to FCA should begin at that point. For an added bonus as found when sorting out old paperwork a couple of old letters from Mercers Debt collections (trading as dormant company in 2008/2009/10 so asking how can that be?) notifying me of default of CCA and then initial payment plan in 2009. These complaints relate to having a look for PPI via Resolver and seemingly opening a can of worms but more maggots I'd say. Background - Barclaycard credit card account from 1986 - and now sitting as default in Experian since 17/12/2014 with robbersway /hoist finance/MKDP LLP (all same) and they have begun again to attempt to recover something recently after I had complained about Barclaycard via resolver as still attempting to access my data after 4 previous SAR attempts including 2017 ICO upholding my complaint , Barclaycard in April 2017 stating they were sending me £325 for unintentional non-compliance with DPA-1998 and have never received that cheque from them as promised. Unfair interest charges relate to a period of August 2009 and Dec 2013 where because of significant life event (legal separation) a 200 distance from family and massive costs a debt of £2,356 was agreed in payment plan after harassment from B/C and Mercers(B/C) and I don't have the writing (yet) to prove it and where I paid by DD £60 per month and stopped DD Dec 2013 with an estimated outstanding balance of £30. From that point, I suddenly discovered the account balance was the same as four years ago £2,356 and following initial complaint, there has been a plethora of non-compliance with CCA1974(2006) and or DPA-1998 regarding Barclaycard. They stated they sent account statements and updates to interest terms to (an old address) as they state they never received my updated address and continued to send letters there for however long and majority of time have responded to complaints the same way even after updates from Wescot and RW never to complainent address from which submitted. Barclaycard have also stated in one response that they closed the account in May 2010, had transferred the account to Wescot 10th November 2014 and this ceased 15th January 2015 , transferred the account to MKDP LLP on 12/02/2015 yet in Equifax credit report states as being closed by B/C on 17/12/2014 and defaulted by Hoist on same day and balance is now £400 higher at £2,717 so pretty confusing to follow the plot and their storylines. Noodle has Default date in May 2015 submitted request to change and awaiting Experian credit report. My actions at the moment Barclaycard 1) to raise complaint with ICO for continued non-compliance with DPA/GDPR - being registered this week -failing to comply with SAR request and sharing my information to others. I want my data. 2) FCA complaint continuing at present – no updates back yet from FCA. Robinson Way - 1) raise Non-compliance with GDPR with ICO for a) ignoring my implicit consent to suitable and acceptable method of communication or ways of processing my PI (never consented to email and certainly not without additional controls when sharing PI and financial info and notified any and all creditors in writing including B/C 2013/2014 I only consent to written communication by post) by attempting to chase alleged account balance > It's only because I look in my spam email to see what magical offers I'm missing out on that I noticed email as my web filter really does removes the crap. As they refused to acknowledge my complaint and continued to send via email I sent my complain to all their senior executive emails addresses and no doubt riled them. If anyone wants those senior exec email addresses and got a lovely reply from one advising me he was in the Maldives and included his mobile number (complete lack of security awareness) please let me know ? they're not hard to guess. They responded with and trying to quote legitimate interest with a screen shot of GDPR regs and continuing to do so. b) raise non-compliance with GDPR as RW have not fulfilled my SAR as there is no data relating to account assignment , they have only included 4 out of the 20 letters they have sent as a copy even though in the SAR response they have listed around 20 letters sent to client and the notes are a joke just mainly copied from letters of my complaints and no account balance statements from either them or BC. I think I have enough to begin GDPR complaint there as not satisfactory response and will get this going this week. Really want to get them on FCA complaints as well as Shoud be statements and notice of assignment/purhcse of debt. Wescots response that they were only ever data processors and not controllers are a sticking point as I have a Barclaycard response stating that the account was transferred to Wescot 10th Nov 2014 and 15 Jan 2015. They have not responded to my SAR yet but have until 28th June to comply. If anyone want to see anything/docs (around a 100 now) with my PI covered then please let me know. Will be looking at RW website for cookie consent compliance when using a mobile device to see if I can add to me complaint with the ICO. Any other tips, processes to begin with would be more than welcome, of you managed to stay awake for this long. -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Have created my non response to SAR complaint giving BC 14 days to respond and sending by by guaranteed delivery 1pm for arrival Friday 28th Oct. I will post an update on whether I get a response by 12th Nov and thanks for all your advice so far. -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

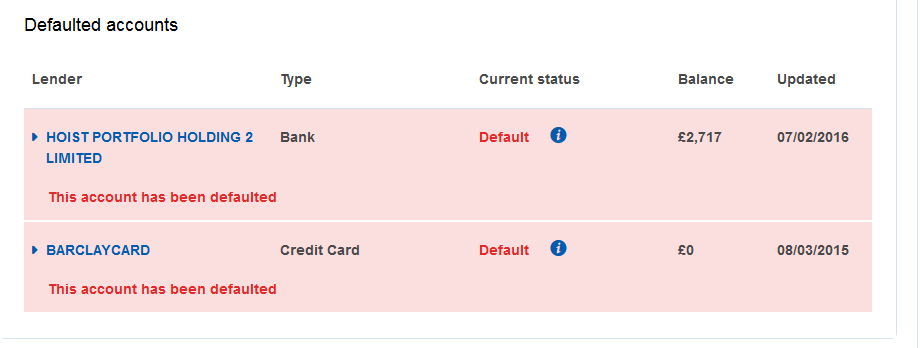

Is this allowed? I'm beginning my compliants to FSO and ICO and was checking my credit report, this makes it look like 2 accounts in default and while they are in continous breaches of Consumer credit act, debt ecovery and DPA. I was never notified in writing by either company. Sharklycard will not even respond to my SAR request and complaints and not once have they complied with any timeframes for requests and complaints. I think it is best to begin complaints but I cannot really begin court proceeding for recovery of illegal penalty and over credit limit charges umtil they provide me with data, any advice is warmly received and greatly appreciated.

-

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Update - as per 8th June no response/ non-compliance again, then a response from Robinson Wray stating they are waiting for a response from client (BC) early Aug. Then a letter dated 31st Aug from Robinson Wray stating that their client BC has no record of me sending a SAR. Advising me to do this Postalorder/cheque for £10 etc and putting a 14 day hold on my account before collection activities resume. Imagine my suprpise when upon searching Royalmail.com and tracking my recorded delivery there was lovely signature from P Jones of BC. I want to reply to Robinson way with the following ' Why is your client lying?' 'Why is there still a persistant culture of deception and dishonesty ? and provide evidence of further non-compliance with screenshot printed off for the tracking signature acceptance of delivery along with scanned copies of my receipts for tracker and standing order Summary Help or advice 1) Should I reply and say go away, I'm off to the FSO and ICO and begin complaints procedure and let the authorites rule in the matter? 2) Should I request immediate removal of the default on my credit report? 3) any further advice on steps to take - should I continue to pursue with RW and BC? 4) I will add to RW initial comms that any contact regarding payment of said account will be considered harassment and reported to relvant authorities looking forward to your knowledge and advice, always been great help in the past. and lovely image of Barclaycard signature acknowledgement of SAR received

-

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Thanks for prompt responses if RW have made the debt re appear by adding a new default date then write with a copy of the mercers DN and give RW 14 days to removed the account else you'll report them to the ICO and seek compensation I am writing letter now but in response to Did you remedy the account after receiving the DN in aug 09? If no then they cant re-default you almost 7 years later for the same debt I agreed a 0% interest payment plan with B/C Nov 2009 taking mercers out of equation but as B/C reneged on that plan after around 3 months and that has meant the debt by end 2013 was the same as at Aug 2009. Can they re-default me now as I made payments for 4 year. I have not made another payment since and have been to and froing with B/C Wescot, R/W. I will write to HC advising of such. -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Just noticed on Clearscore that Hoist / BC have put a default on my credit score, can I have this removed as mercers served me with default notice on 5 Aug 2009 -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Hi, nothing yet received from SAR to B/C but they still have time now have received letter from Howard Cohen and Co Solicitors (B/C Robbersway/ HPH2 and H/Cohen) dated 11/05, received 18/05 saying I have 10 days to the date of this letter to respond with acceptable proposals for payment. The letters headed ' Notice of Pending Legal Action' but is signed with a scanned signature , this is not correct is it. Should I ignore or how should I reply to them? -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Hi Slick, Thanks SAR sent, will keep you posted when reply received -

Decade long bull with Barclaycard/Mercers/Wescot and then RW/Hoist/MKDP

simo67 replied to simo67's topic in Barclaycard

Thanks for all the valuable inputs and recommendations. I am pretty sure the debt is still owed by BC as Robinson Way mention reverting back to client in the letters I received. From what I have seen BC have just re added interest back on all my payments from end 2009 until Dec 2013 so balance stayed around the same. A SAR is being done now and I will send recorded delivery later today - is it best to send to Churchill place address? I will ignore BC and DCA Two final questions 1) As I have now received a true copy of my original 1986 credit agreement on 18th April 2016, is the debt enforceable or because timeframes were not met for requests now not enforceable? 2) In my letter received 18th April from Robinson Way the date on the letter is listed as 15th Feb 2016. This to me is either a mistake or a fraudulent action to cover up failing to deal with complaint within the required timeframe of 5 6 days. What would you recommned I do with that letter, send a copy to the FSO/Police? as I do not believe it is a genuine mistake but a deliberate action taken to cover up failing to comply -

I have had a Barcalycard since 1986, in 2008 during separation I went into debt with all creditors. With all creditors I agreed a payment plan with 0% interest /charges. All other creditors have stuck to this and all have been settled. With Barclaycard I agreed verbally (yes I know) the plan and balance of £2536. In Nov 2013 when I calculated a £30 balance I stopped direct debit and lo and behold I had an outstanding balance of £2576. I have complained and received replies beyond the 56 days and failing to address my complaint and saying they have no record of this during 2014/2015. They have tried to add further charges bringing in Wescot and Robinson Way with the alleged account balance now at £2717.91. I sent a CCA request to which they failed to comply within the 12 days, and as I had just moved house BC sent a blank agrement reply to my old address and a reply to my new address they could not verify who I was and to call them I have fended off both Wescot and Robinson Way with breaches of consumer credit act, consumer rights and DPA reaches. Eventually I received a letter on 18th April 2016 from Robinson Way with a copy of my original credit agreement. I know during 2008 late penalty and over credit limit charges were put on the account at £12.50 each and they have consistently failed to comply with timeframes for requests and complaints. Now Robsinson Way have given me 14 days to detail a payment plan (something I am not prepared to do) I have paid this debt and am not paying for it again. Thanks in advance for your words of wisdom

-

Bugs/Viruses/Malware etc

simo67 replied to a topic in Technical Computer/IT/Console/SatNav Questions

Adobe Issues Emergency Flash Patch (January 22, 2015) Adobe has released an emergency patch for Flash on Thursday, January 22 to address a vulnerability that is being actively exploited (see story below). The most current versions are now Flash Player 16.0.0.287 for Windows and Mac OS X, Flash Player 11.2.202.438 for Linux, and Flash Player Extended Support Release 13.0.0.262. ISC: https://isc.sans.edu/forums/diary/OOB+Adobe+patch/19217/ http://krebsonsecurity.com/2015/01/flash-patch-targets-zero-day-exploit/ http://www.scmagazine.com/adobe-issues-emergency-fix-for-flash-player-vulnerability/article/393977/ http://www.computerworld.com/article/2873541/adobe-fixes-just-one-of-two-zero-day-flaw-in-flash-player.html I work in IT and 50% of my time is around Cyber security I can advise around personal safety but would say this at some point you will be breached or hacked whether that is on your personal PC, Tablet or Smartphone. Also any data you have provided to any financial, insurance, retail institution, etc will not be protected from a persistant, deliberate or mailcious hack. If they are sensible enough, they will use segregation at a physical and logical layer for systems and user access, which may dilute the information but will not prevent some of it being hacked. I just hope there is not enough out there to allow easy fraud and directly addressed phising. I have seen hardware adapted like a USB mice with key logging techology inside and other trojans.Excel still has a vulnerability (will not be patched) that if using a macro enabled spreadsheet can give instant remote access to attacker with hidden calls to functions (it went through on Mac, Win 7 and Win 8 "PROTECTED" by Symantec, Windows Defender, AGV and MS Security Essentials all up to date. Good site for news is SANS.Org -

Thanks for the quick replies and now understand this is outwith the UK and covered under Dutch regulations, thought as a UK resident and national I would be covered by UK regulations. I still intend to complain to ABM AMRO about their lending practices /(risky loans procedure earnings to loan ratio) and chasing the debt , they seem to have a similar process in The Netherlands to here in UK, bank first then ombudsmen. wished I'd known about this site back in 2009 and more about DCA.

-

Just received a cheque yesterday for £60.20 for having CPP for around 2 years on a credit card a long time ago. I pretty much used the wording in the claim form. I was misled / not made aware that I was already sufficiently covered under existing banking/credit card regulations. 2 letters, 2 replies sent back, 2 mins of my time and a £60 refund / result. Thanks to people from CAG and like minded people bringing this out in the open.

-

Update , I received a true copy of my original credit agreement (ABM AMRO) via a scanned attachment from Lindorff Credit BV (Dutch DCA). I requested a copy of the deed of assignment giving Bluestone the right to collect on behalf of ABM/AMRO (Lindorff) and to prove who was the owner of the debt after re requesting and stating it had not been provided. I received end of last month a copy of the master service agreement from Lindorff Credit BV giving multiple companies the right to act on their behalf including Bluestone. As the date was 1st December 2012 , I have now replied that all payments collected/demanded from me by Bluestone between the 1st June 2009 and 1st Dec 2012 were collected illegally and were a direct breach of the consumer credit act and DCA guidelines. I went on to say this and hope it was the right approach, would appreciate feedback here: All payments collected illegally will be requested via legal action if necessary in UK courts to be refunded with each payment having 8% compund interest from date payment was made, plus the £400 of overdraft fees incurred by me during this time period to enable me to make these illegally collected payments, plus 46 emails at £14.95 each and 25 hours of research at £19 per hour, any legal costs incurred by solicitor. I went onto say a copy of this with the details sent by Bluestone will be sent to Trading Standards and FCA . I then went onto say if he wished to offer a settlement figure , due consideration would be given to it.

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS