mkb

-

Posts

1,084 -

Joined

-

Last visited

-

Days Won

2

1 Follower

-

Thanks again, DX CCA & CPR requests posted today. Told him to get proof of posting & send first class. Will do MCOL when he comes back. If I'm honest, he probably wouldn't have the fight for an irresponsible lending case. I mentioned a DRO to him & he seemed quite interested in that - it would take the pressure off him but I made sure he knows he has to deal with this first.

-

He's gone back home to get his wife up & dressed but he remembers making the £2 payments by standing order years ago. He has absolutely no recollection of any 39p payments ! He won't phone from his house because he doesn't want his wife getting stressed but he'll be able to phone when he comes back round to me. He's going to ask his bank for copies of his bank statements for the period 2012 - 2015 so he'll be able to confirm/deny with evidence.

-

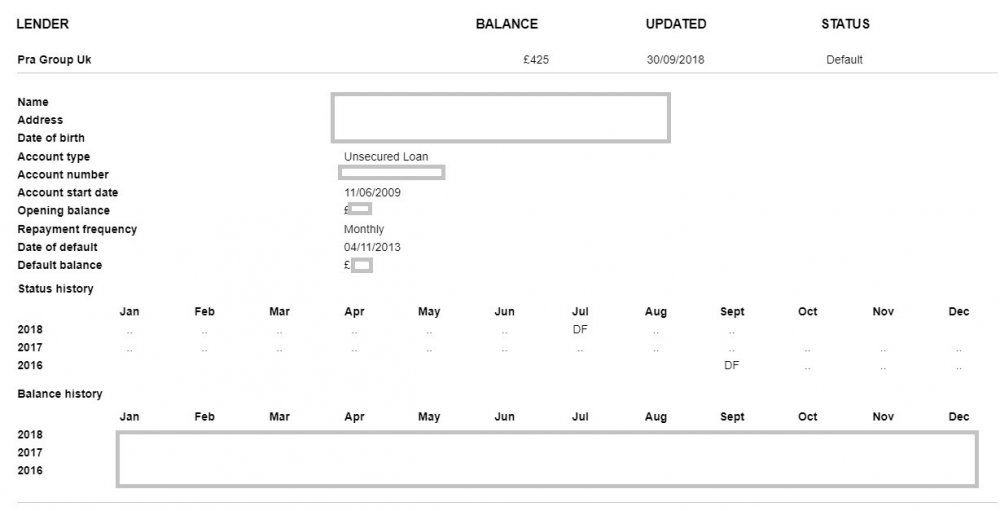

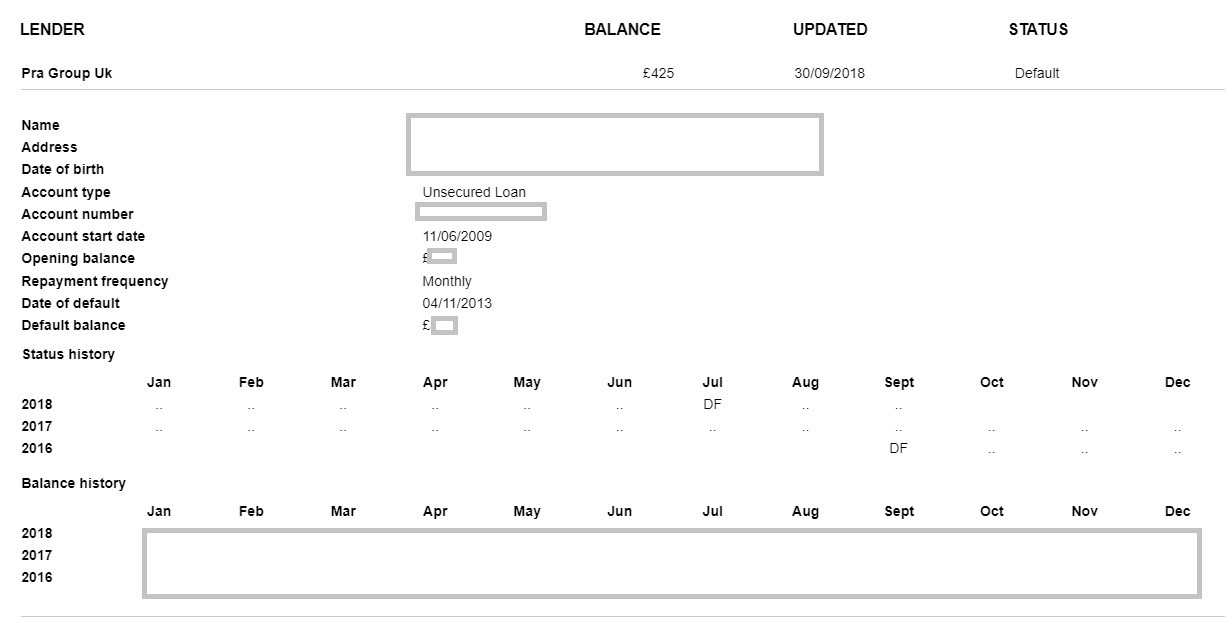

Credit file shows nothing other than below Interesting to see two Defaults were recorded yet no letters of Default have been received. He rang PRA to ask for last payment date. They said there was a payment on 12/06/2014 for 39 pence but that there had also been payments of £2 also in 2014. He got them to email me a copy of the payment schedule from 2011 showing erratic payments of sums he has no recollection of making. He acknowledges he was trying to make payment but categorically denies making payments of 39p a month at any time. I guess since he admits to making the £2 payments, there's no denying the debt nor is it SB. He asked for the initial loan balance but nobody appears to have that information. I'm stuck for ideas now so please, any and all help is welcome Ultimately if he has to accept a CCJ, it'll be another £5pm on account of his limited income.

-

I'll tell him to ring Prov in the morning. He doesn't have any paperwork earlier than 2017 - he says he binned most of the letters. He feels fairly sure he hasn't paid anything since giving up work in 2010 but can't prove it. I'll get him to check his credit file when he gets round here in the morning. Hopefully it's SB & all this can then go away.

-

Thanks DX Been reading the SB defence letter to DCAs. Should he use the same letter to the OC via the N1 ? Is there anything else he needs to do in the meantime other than to ask for CCA & CPR 31.14 ?

-

Just been on the phone to him & he doesn't think he's paid anything toward this debt since 2010 so it seems to me that they are out of time & the debt should be SB. Since a SAR would take him over the 33 day limit, what can he do ?

-

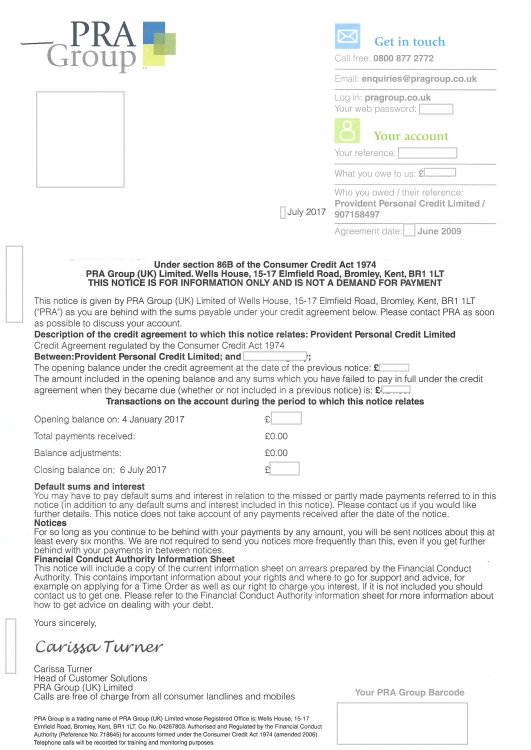

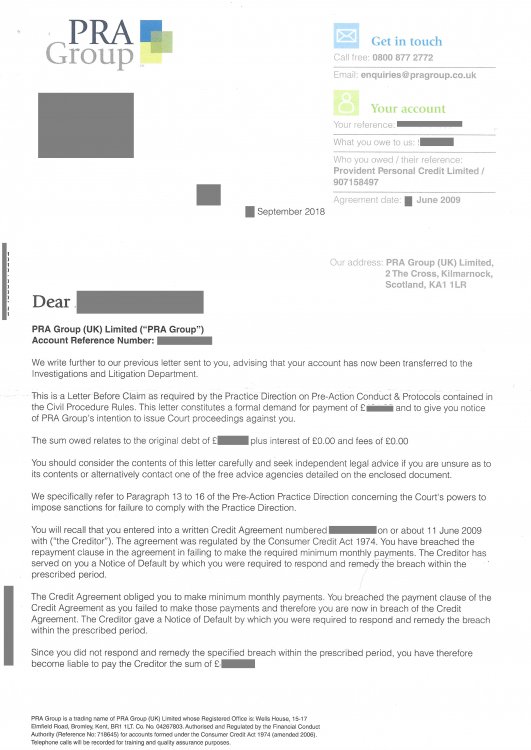

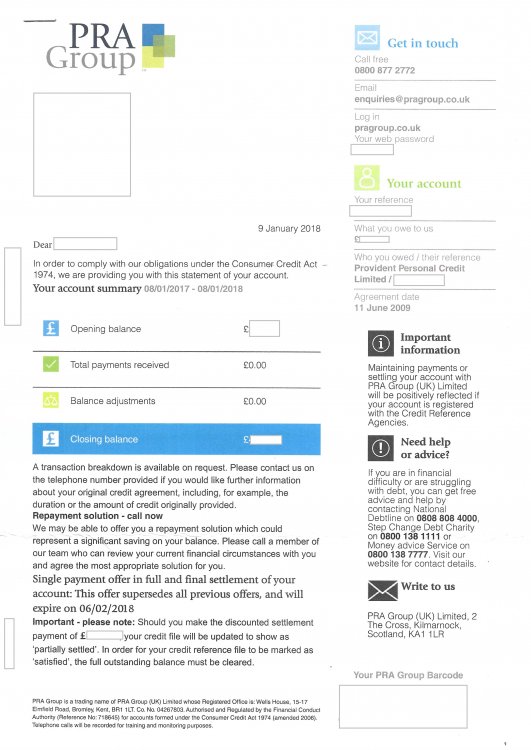

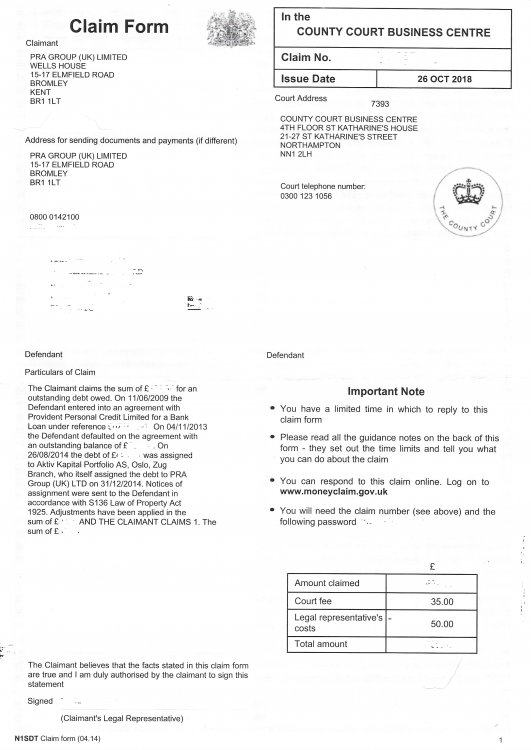

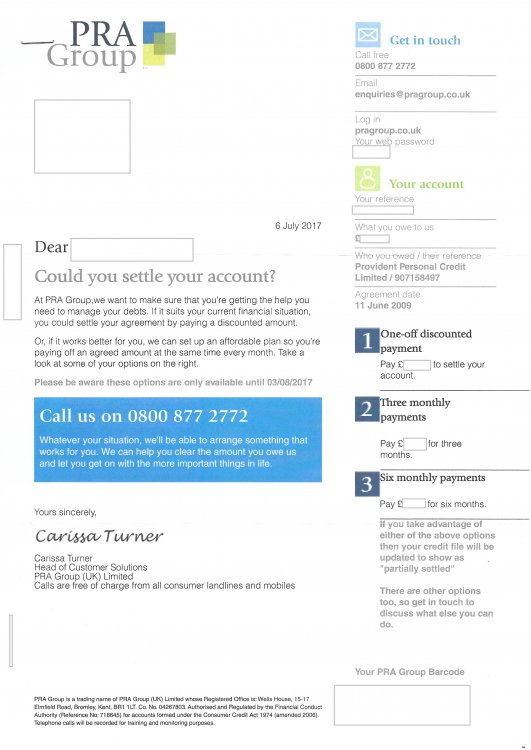

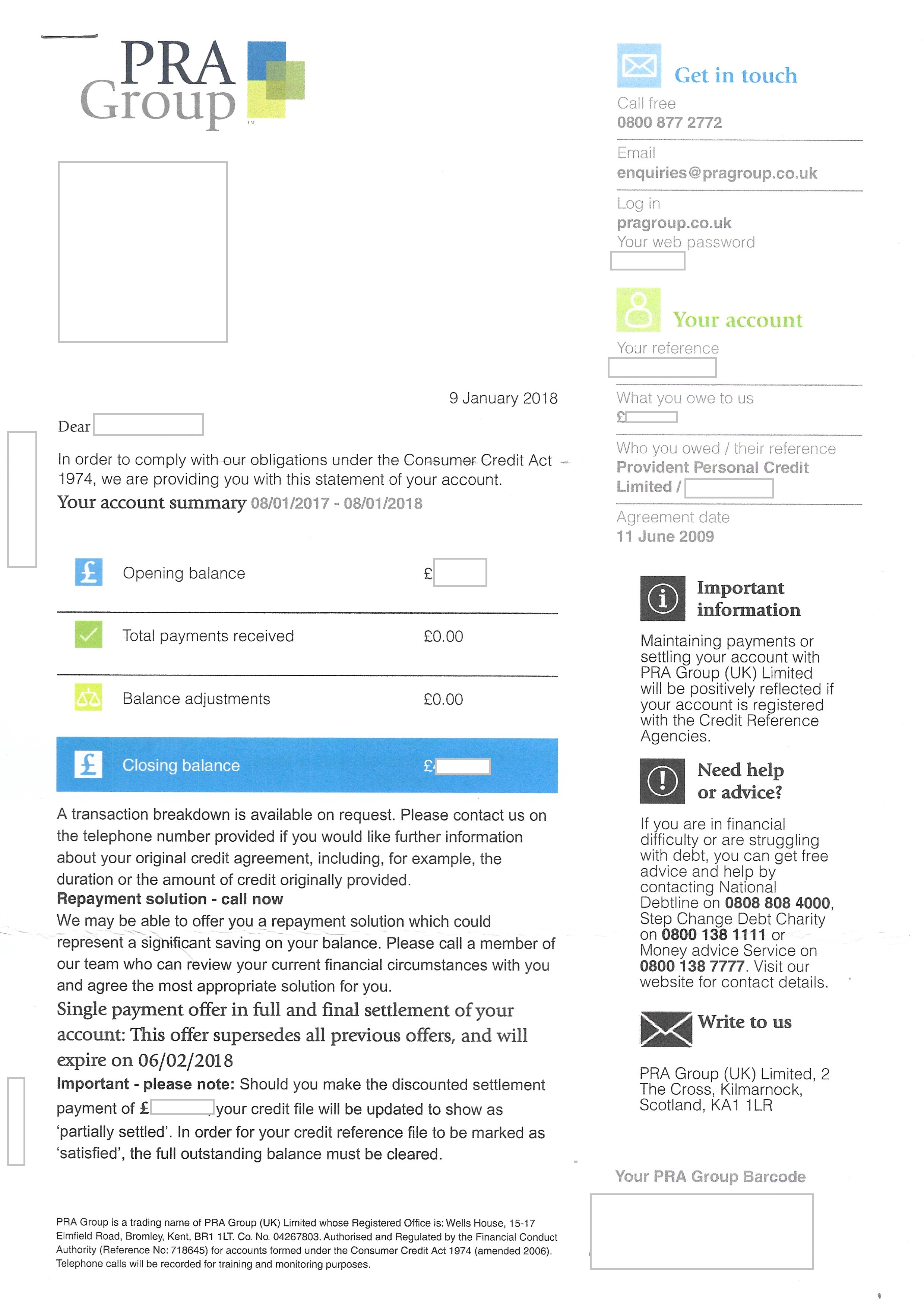

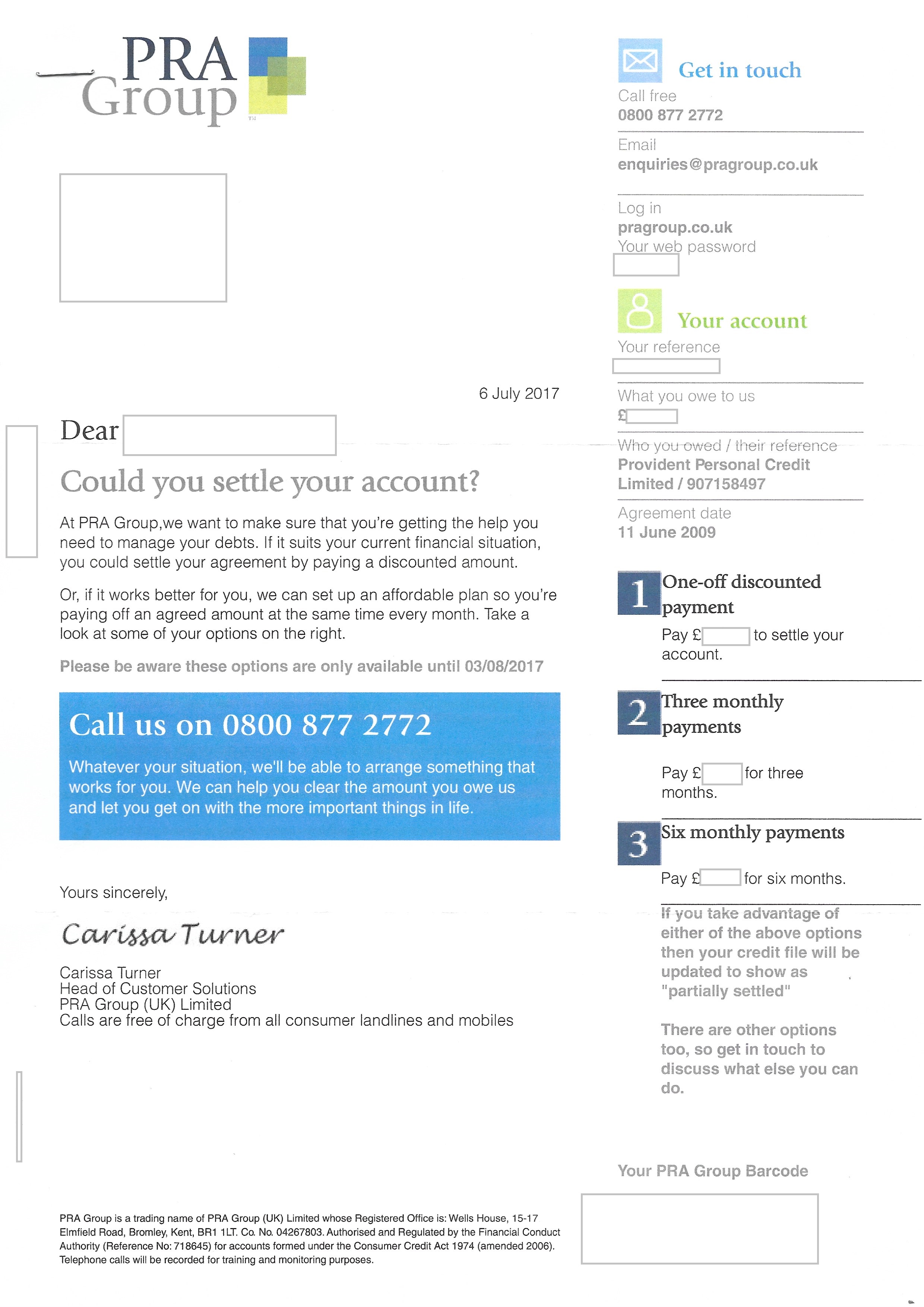

Name of the Claimant ?PRA Group (UK) Limited Date of issue – top right hand corner of the claim form – this in order to establish the time line you need to adhere to. 26/10/2018 Date of issue XX + 19 days ( 5 day for service + 14 days to acknowledge) = XX + 14 days to submit defence = XX (33 days in total) - 28/11/2018 ^^^^^ NOTE : WHEN CALCULATING THE TIMELINE - PLEASE REMEMBER THAT THE DATE ON THE CLAIMFORM IS ONE IN THE COUNT [example: Issue date 01.03.2014 + 19 days (5 days for service + 14 days to acknowledge) = 19.03.2014 + 14 days to submit defence = 02.04.2014] = 33 days in total Particulars of Claim What is the claim for – the reason they have issued the claim? Please type out their particulars of claim in full (verbatim) less any identifiable data and round the amounts up/down. The Claimant claims the sum of £425 for an outstanding debt owed. On 11/06/09 the Defendant entered into an agreement with Provident Personal Credit Limited for a Bank Loan under reference *********. On 4/11/2013 the Defendant defaulted on the agreement with an outstanding balance of £430. On 26/08/2014 the debt of £420 was assigned to Aktiv Kapital Portfolio AS, Oslo, Zug Branch, who itself assigned the debt to PRA Group (UK) LTD on 31/12/2014. Notices of assignment were sent to the Defendant in accordance with S136 Law of Property Act 1925. Adjustments have been made in the sum of £0.40 AND THE CLAIMANT CLAIMS 1. The sum of £425 Have you received prior notice of a claim being issued pursuant to paragraph 3 of the PAPDC (Pre Action Protocol) ? 2 identical letters were sent claiming to be "Letter before Claim as required by the Practice Direction on Pre-Action Conduct & Protocols contained in the Civil Procedure Rules" The first of these letters was dated March 2018 & the second in September 2018. What is the total value of the claim? £510, incl court fees & legal fees Is the claim for - a Bank Account (Overdraft) or credit card or loan or catalogue or mobile phone account? Doorstep loan - not a Bank Loan as claimed in the POC When did you enter into the original agreement before or after April 2007 ? 2009 Is the debt showing on your credit reference files (Experian/Equifax /Etc...) ? Yes Has the claim been issued by the original creditor or was the account assigned and it is the Debt purchaser who has issued the claim. Original creditor Were you aware the account had been assigned – did you receive a Notice of Assignment? No memory of such but as sent back to OC, prob not applicable Did you receive a Default Notice from the original creditor? No letters marked Default Have you been receiving statutory notices headed “Notice of Default sums” – at least once a year ? No Why did you cease payments? Had to give up work to become full time carer for disabled wife. What was the date of your last payment? Not sure Was there a dispute with the original creditor that remains unresolved? No but seeing as OC has already obtained CCJ's for 2 other loan a/c's, it seems particularly odd that they have come for such a small amount & after such a long time. Did you communicate any financial problems to the original creditor and make any attempt to enter into a debt management planicon? No What you need to do now. Answer the questions above If you have not already done so – send a CCA Request to the claimant for a copy of your agreement Posted 30/10/18 ======================================================= Hi, a dear friend has asked me to help him as he got court papers this morning & he's in a panic. He doesn't have access to computer or scanner so everything will be uploaded/discussed via myself. Since 2017, the only paperwork received has been: 1. Account summary, dated January 2018 and letter marked "not a demand for payment" 2. LBC dated March 2018 incl account summary 3. Letter marked "Not a demand for payment" incl letter offering to accept reduced sum in full payment 3. LBC again dated September 2018 incl account summary 4. N1 claim There is no paperwork saved before Jan 2017 so a CPR 31.14 request for the original agreement, assignment & reassignment letters as well as the default notice will be posted tomorrow. His only income is Income Support and Carer's allowance & he already has 3 CCJ's of which 2 are to PRA re Provident which they secured in Feb 2017. He pays each of them at £5 per month. In view of the fact that their paperwork doesn't appear to be in order, I wondered if he had a chance of successfully defending the claim. Your opinions would be helpful. I have uploaded all the documentation. Interestingly, every piece of paperwork has his correct address on it apart from the September LBC & the actual N1 claim ! Ok, so it's only the last letter of the postcode they got wrong but it strikes me as odd that it's been right up until now - my cynicism alarm bells rang when I noticed it, lol

-

Useful info as always dx - thanks

-

Well quite but it proves how they need checking on & how knowing one's rights under the law, aided by the knowledgeable folks at CAG, is enormously helpful in putting the case to them

-

Result & many thanks for the support dx

.thumb.jpg.9f1078d75b01658796e5b3b8634f3636.jpg)

-

LOL, postie's just delivered & there's a letter from Prov ! It's just a letter setting out how their complaints process works but at least it confirms my letter has been received. Will update thread as & when my complaint gets dealt with in case it helps anybody else in a similar situation.

-

Thanks dx but if I have no proof of delivery, surely Prov will keep on doing nothing but supplying Experian with incorrect information. Are you saying just wait the 28 days then slam a complaint into the ICO, citing s7 Interpretation Act ?

-

Hi I feel as if I should know how to do this by myself but age is catching up with me & the brain's not as sharp as it once was so any help will be greatly appreciated. I went bankrupt in 2010 & was discharged in 2011. When checking my credit file with Equifax - all ok but Experian have a default with Provident marked against me, dated 2011 ! Prov were definitely included in the BR & I know they are wrong to have marked the default after the date of the BR so I wrote to them demanding they rectify the information they provide to Experian, posted recorded delivery & good old RM didn't get a signature to show whether it had been delivered ! What do I do now ? Do I send the same letter, this time by Special Delivery ? Do I do nothing & wait for 28 days then if no response from Prov, complain to the ICO stating s7 Interpretation Act ? Do I send the same letter, this time by Special Delivery but pointing out the 28 days started from the date of the original letter ? As I said, any help will be greatly appreciated. After 6 years of waiting, it's a pain in the proverbial not to have a shiny clean credit file

-

citizenB

mkb replied to BankFodder's topic in Consumer Forums website - Post Your Questions & Suggestions about this site

Seen the news & wanted to say thanks for the help you offered when my financial life was in a mess. The advice & suggestions of CB (as well as Ellen & AndyOrch) have helped me enormously & I know for sure I'm not alone in that. CAG is losing a gem but all the best for the future CB -

Risking your home for the sake of £1800 is madness. Arrange an affordable payment plan with the water company, set up a standing order to pay it on time each month & move on with your life.

.jpg.b66272a716aec5d4b6cb115972d2740b.jpg)

Latest

Our Picks

Reclaim the right Ltd

reg.05783665

reg. office:-

262 Uxbridge Road, Hatch End

England

HA5 4HS